01

Market Summery

Executive Summary and Global Market Analysis

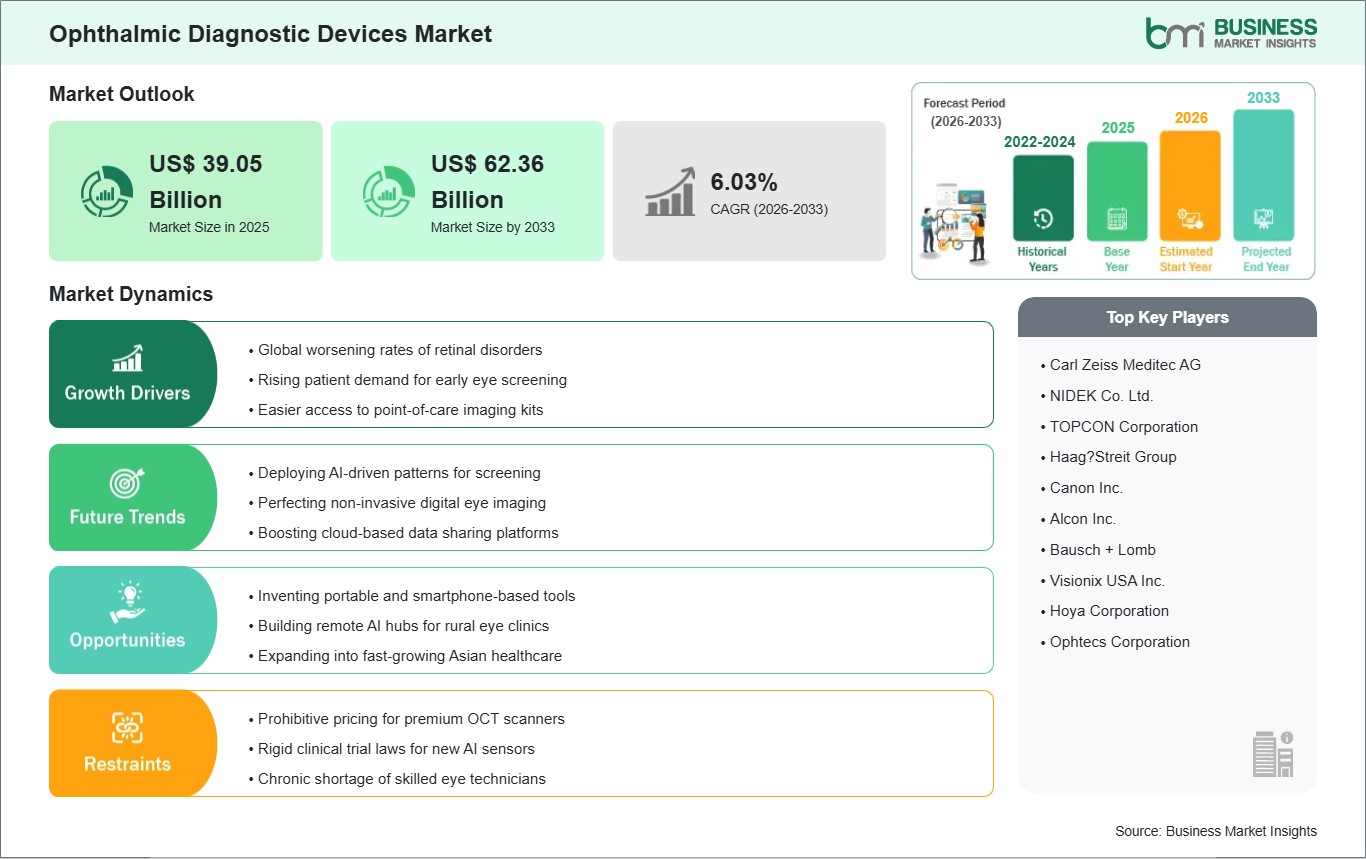

Ophthalmic diagnostic devices are specialized medical instruments used by eye care professionals to identify and monitor various vision-related conditions. These devices are critical for the early detection and management of chronic eye diseases such as glaucoma, cataracts, and macular degeneration. Ophthalmic diagnostics play a vital role in healthcare by providing high-resolution imaging and precise measurements of ocular structures, which are essential for effective treatment planning. The market is primarily driven by the rising global prevalence of vision impairment, a rapidly aging population, and the increasing incidence of lifestyle-related conditions like diabetic retinopathy. Additionally, continuous technological innovations, such as the development of portable diagnostic tools and advanced imaging scanners, are enhancing clinical outcomes and patient experiences.

However, several challenges can restrain market growth, such as the high acquisition and maintenance costs of advanced equipment, limited accessibility to specialized eye care in rural regions, and complex regulatory approval pathways. Despite these hurdles, the market holds significant opportunities driven by the integration of artificial intelligence (AI) in automated screening, the expansion of private eye care networks in emerging economies, and the growing demand for telemedicine-based ophthalmic services. Increased government focus on preventable blindness and rising healthcare expenditure are also expected to open new avenues for market expansion.

03

Segment Analysis

Ophthalmic Diagnostic Devices Market Segmentation

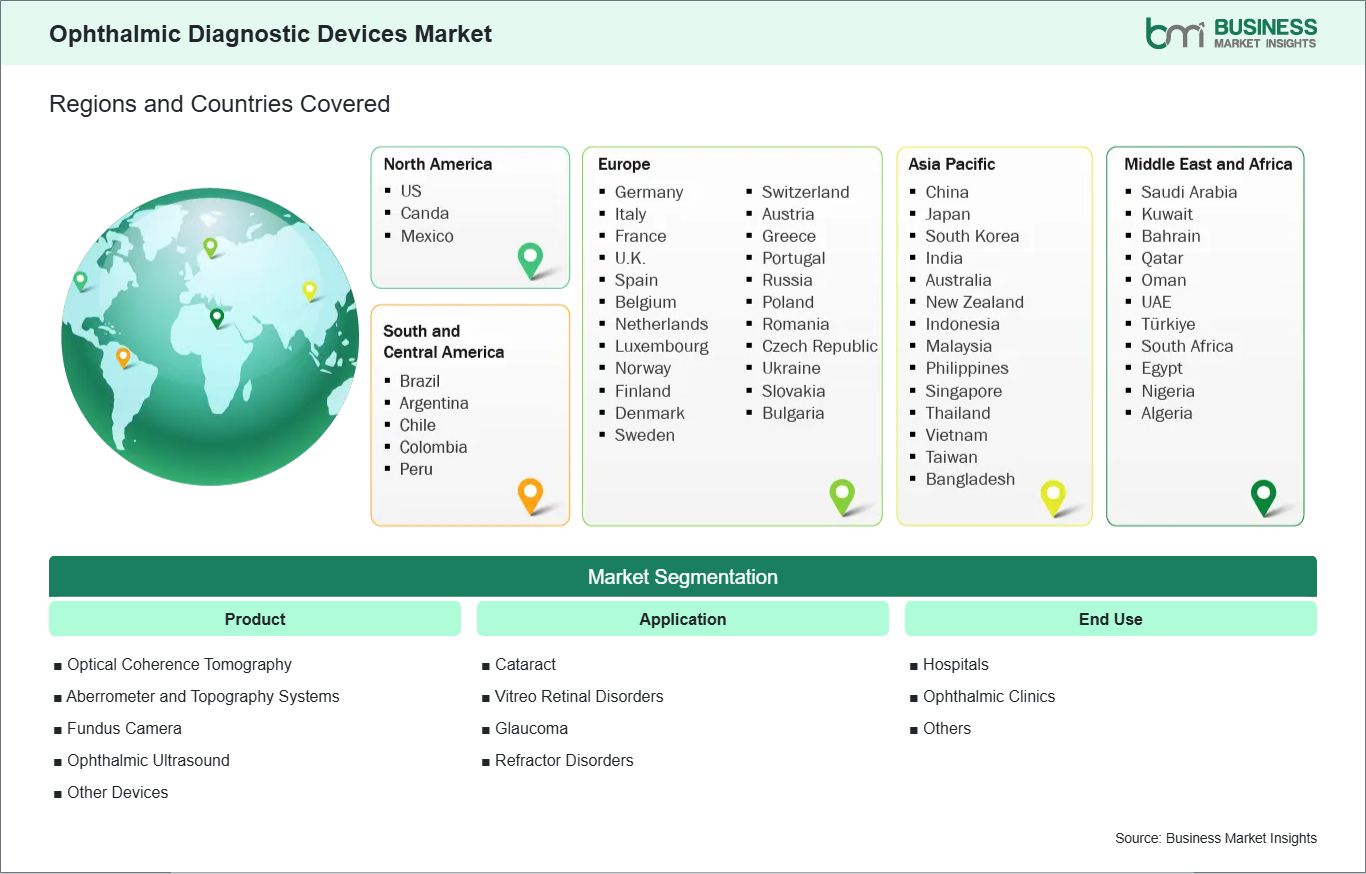

Key segments that contributed to the derivation of the Ophthalmic Diagnostic Devices market analysis are product, application, and end use.

- By Product, the market is segmented into Optical Coherence Tomography, Aberrometer and Topography Systems, Fundus Camera, Ophthalmic Ultrasound, and Other Devices.

- By Application, the market is segmented into Cataract, Vitreo Retinal Disorders, Glaucoma, and Refractor Disorders.

- By End Use, the market is segmented into Hospitals, Ophthalmic Clinics, and Others.

04

Market Forces

Ophthalmic Diagnostic Devices Market Drivers and Opportunities

Rising Prevalence of Ocular Disorders and Aging Population

The rapid increase in the global burden of vision impairment has emerged as a pivotal factor positively driving the ophthalmic diagnostic devices market. As the global population ages, the susceptibility to age-related eye conditions like cataracts, glaucoma, and macular degeneration increases significantly. Furthermore, the rising incidence of chronic conditions such as diabetes is fueling the demand for diagnostic tools to manage diabetic retinopathy.

For instance, according to the World Health Organization (WHO), at least 2.2 billion people globally have a near or distant vision impairment, and in at least 1 billion of these cases, the impairment could have been prevented or is yet to be addressed. This robust patient pool directly supports the growth of the ophthalmic diagnostic devices market, as the need for early, efficient screening solutions continues to increase to meet patient expectations and healthcare demands worldwide.

Integration of Artificial Intelligence (AI) in Diagnostics

The ongoing digital transformation of eye care has become a powerful opportunity for growth in the ophthalmic diagnostic devices market. As diagnostic data becomes more complex, businesses are increasingly relying on AI and machine learning to move toward automated, fast, and reliable screening solutions. AI-powered platforms, known for their speed and pattern recognition capabilities, are uniquely positioned to assist ophthalmologists in handling high patient volumes while reducing the risk of human error.

In recent years, the development of AI-based retinal screening has opened new markets, encouraging early intervention in both developed and emerging economies. High-value imaging data from Optical Coherence Tomography (OCT) and fundus cameras are frequently processed using deep learning algorithms to identify biomarkers for diseases like glaucoma and diabetic retinopathy. This shift often involves the need for diagnostic solutions that can support decentralized care, allowing primary care clinics to perform specialty-level screenings. As healthcare systems adapt to demand-driven models and personalized medicine practices, the demand for AI-enabled diagnostic management is expected to grow steadily.

05

Size and Share Analysis

Ophthalmic Diagnostic Devices Market Size and Share Analysis

The ophthalmic diagnostic devices market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within product, application, and end use, offering insights into their contribution to overall market performance.

For instance, Optical Coherence Tomography (OCT) scanners typically hold a significant share as they are essential for providing cross-sectional tissue visualization for retinal health. This product is widely utilized across various specialist and hospital environments due to its objective measurement capabilities and reliability.

Cataract applications involve the use of diagnostic devices for precise surgical planning and pre-operative measurements. This segment benefits from the high global volume of cataract surgeries and the increasing adoption of advanced biometry systems to improve refractive outcomes.

Ophthalmic Clinics utilize these diagnostic devices to offer accessible, specialized eye care services outside of traditional hospital settings. This end-use segment is growing quickly due to the rise of private eye care chains and the increasing focus on outpatient diagnostic throughput.

07

Report Coverage

Ophthalmic Diagnostic Devices Market Report Coverage and Deliverables

The "Ophthalmic Diagnostic Devices Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

- Ophthalmic Diagnostic Devices market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Ophthalmic Diagnostic Devices market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Ophthalmic Diagnostic Devices market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Ophthalmic Diagnostic Devices market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Ophthalmic Diagnostic Devices Market Geographic Insights

The geographical scope of the Ophthalmic Diagnostic Devices market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

The Asia-Pacific Ophthalmic Diagnostic Devices market is segmented into China, Japan, South Korea, India, Australia, and the Rest of Asia. The Asia-Pacific market is experiencing robust growth, driven by the rapid expansion of healthcare modernization, growing international patient volumes, and the rising demand for early screening services. Major economies like China and India are leading the way, fueled by increasing industrial output, strategic healthcare investments, and the development of specialized eye care facilities in Tier-II and Tier-III cities.

The region is also witnessing increased adoption of advanced diagnostic technologies, including AI-based retinal screening, digital fundus imaging, and portable diagnostic systems, particularly relevant for remote and underserved areas. Capacity expansion, alongside efforts by regional manufacturers to provide cost-effective equipment, is enhancing operational efficiency and patient accessibility. Additionally, the surge in the elderly population and the rise of regional health initiatives (such as India's NPCB) further solidify the region’s position as a key growth hub in the global ophthalmic ecosystem.

10

Industry Activity

Recent Developments

The Ophthalmic Diagnostic Devices market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Ophthalmic Diagnostic Devices market are:

- In July 2025, Huvitz launched OCTavius (ophthalmic diagnostic device). It is a 5-in-1 OCT system that integrates five essential diagnostic functions into a single device—streamlining traditionally complex diagnostic workflows. This innovative solution is drawing strong interest for its ability to improve clinical efficiency while simplifying examinations.

- In September 2025, ZEISS Medical Technology showcased the latest innovations and enhancements to its cataract and corneal refractive workflow solutions, from diagnostics and surgical planning to advanced treatments, at the European Society of Cataract and Refractive Surgeons (ESCRS) conference in Copenhagen, Denmark.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Bank - Global Health IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations