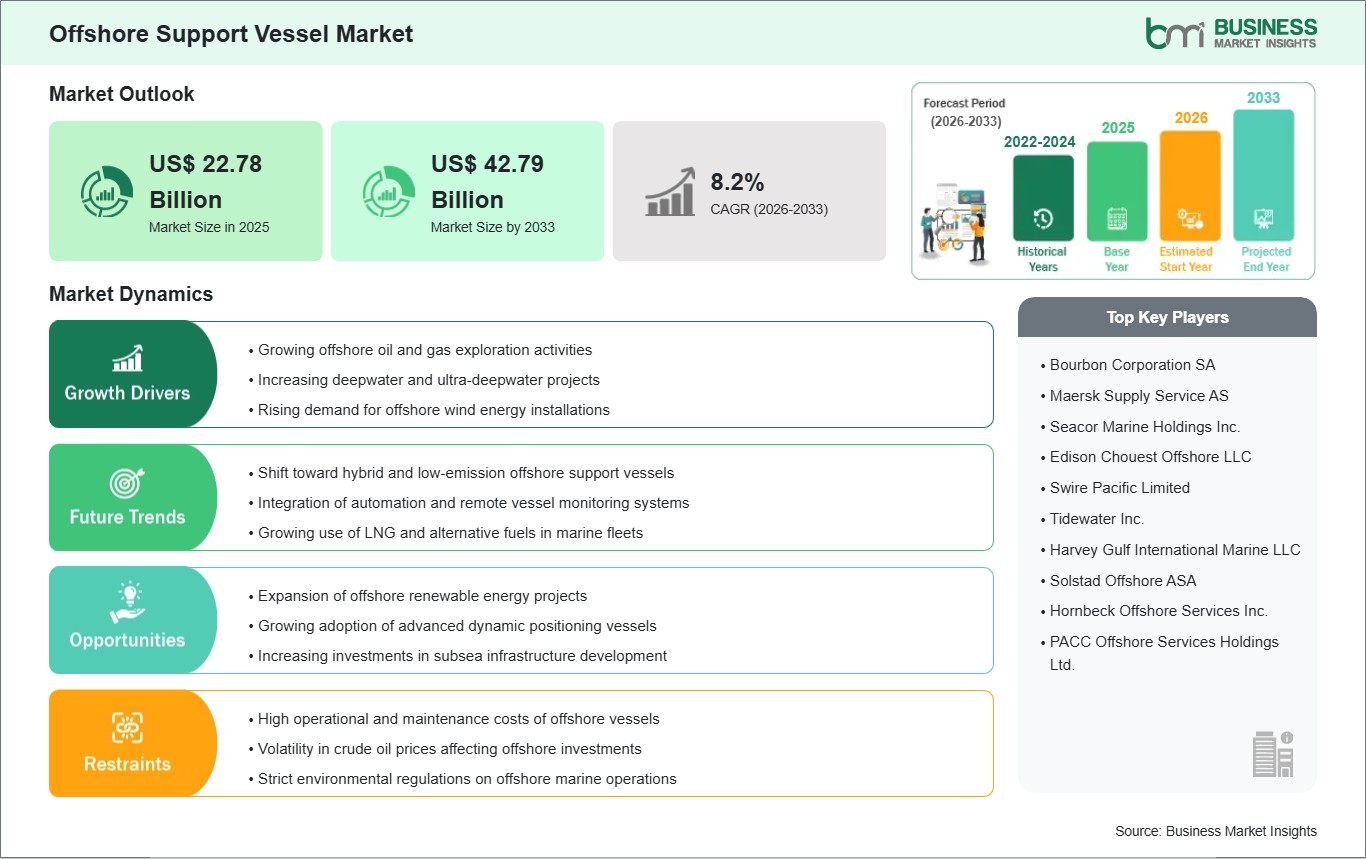

The offshore support vessel market size is expected to reach US$ 42.79 billion by 2033 from US$ 22.78 billion in 2025. The market is estimated to record a CAGR of 8.2% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Offshore support vessels are marine assets designed to transport cargo, manage towing tasks, maintain offshore positions, and assist installation or maintenance work around offshore energy infrastructure. Their operating profile spans drilling campaigns, subsea construction, production support, inspection activity, and marine logistics in demanding sea conditions. These vessels remain central to offshore project continuity because they connect remote field operations with equipment, personnel, and operational readiness.

Market expansion reflects a broader shift toward offshore energy activity that requires dependable vessel availability across exploration, production, maintenance, and asset retirement programs. Operators increasingly prioritize fleet capability, positioning accuracy, deck efficiency, and fuel performance as projects move into deeper waters and more complex offshore environments. The industry also benefits from wider use cases linked to offshore wind construction and decommissioning support.

Within vessel categories, anchor handling tug and anchor handling towing supply vessels retain strategic relevance where mooring control, towing strength, and rig movement support remain essential. Platform supply vessels maintain broad commercial relevance because they support routine cargo transfer, fluid movement, and deck logistics. Application demand remains anchored in offshore oil and gas, while offshore wind and decommissioning continue to widen the service mix across this sector.

Technical development is reshaping fleet standards through dynamic positioning upgrades, hybrid power integration, digital monitoring platforms, and mission-specific deck configurations. Owners are aligning vessel design with stricter operating expectations around emissions, uptime, and safety performance. As charter requirements become more specialized, vessels capable of supporting multiple offshore tasks gain commercial preference and improve asset utilization across changing project cycles.

Competitive conditions are shaped by fleet age, asset versatility, contract coverage, and regional deployment strength rather than simple fleet scale alone. Market participants are refining portfolios through vessel upgrades, selective acquisitions, long-term charters, and repositioning strategies tied to offshore energy demand. This environment rewards operators that can balance technical compliance, vessel availability, and service adaptability across conventional and emerging offshore programs.

Offshore Support Vessel Market - Strategic Insights:

Get more information on this report

Offshore Support Vessel Market Segmentation Analysis:

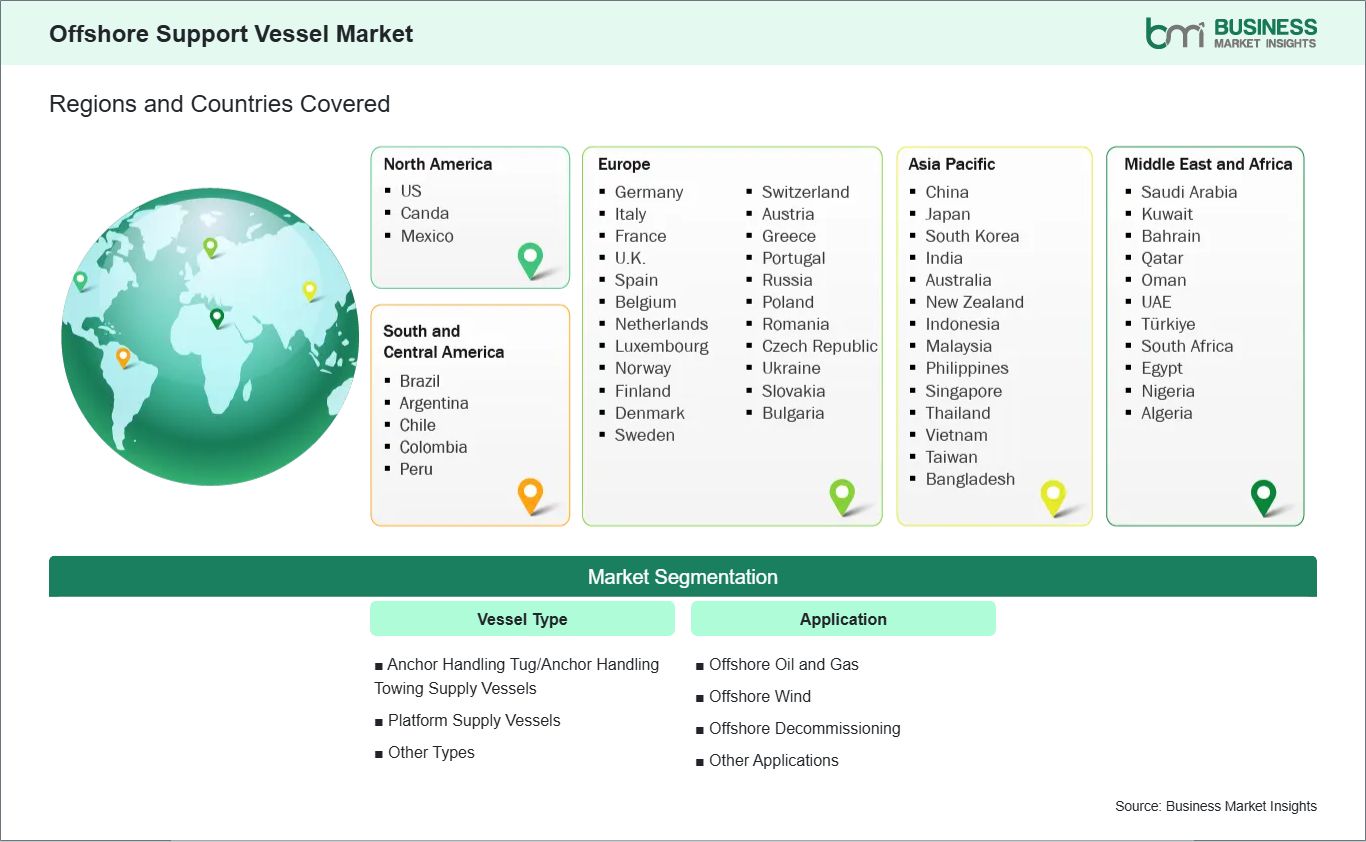

The offshore support vessel market is segmented based on vessel type and application, reflecting its critical role in deepwater exploration, offshore wind farm logistics, and platform maintenance.

By Vessel Type

Anchor Handling Tug/Anchor Handling Towing Supply Vessels: Support rig moves, towing tasks, and mooring operations offshore.

Other Applications: Covers research support, surveillance, emergency response, and marine service operations

Offshore Support Vessel Market Drivers and Opportunities:

Expansion of offshore energy project pipelines

Broader offshore activity creates sustained need for marine assets that can move cargo, support construction schedules, and maintain field continuity. As offshore projects become more distributed across mature and frontier basins, operators require dependable vessel access to reduce downtime and coordinate specialized tasks. This need reinforces charter demand for support fleets that can serve both routine logistics and technically demanding offshore assignments.

The resulting effect is stronger fleet utilization in regions where offshore development plans remain active and service intensity is increasing. In practical terms, vessel selection now reflects project complexity, turnaround expectations, and operating depth rather than simple transport capacity. This makes offshore support vessels more relevant to field economics, execution reliability, and marine coordination throughout the asset lifecycle.

Cross-sector vessel deployment in offshore wind and subsea services

Offshore wind buildouts and subsea intervention programs are creating fresh openings for vessel operators with adaptable fleets and specialized onboard systems. Innovation in deck layout, motion control, remote monitoring, and fuel-ready propulsion is making support vessels more suitable for installation support, inspection campaigns, and maintenance work. These use cases broaden commercial pathways beyond conventional offshore drilling-linked activity.

Over time, this opportunity can extend into multi-service operating models where the same vessel class supports energy, survey, and marine infrastructure work. Such flexibility can improve asset employment across market cycles and widen regional expansion options. As offshore project diversity increases, operators that align vessel design with emerging service needs can strengthen utilization resilience and contract relevance.

Offshore Support Vessel Market Size and Share Analysis:

The offshore support vessel market was valued at USD 22.78 Billion in 2025 and is projected to reach USD 42.79 Billion by 2033, expanding at a CAGR of 8.2% during 2026 - 2033. This trajectory reflects broader offshore activity requirements, stronger vessel utilization in selected service categories, and a shift toward technically capable fleets able to support more demanding operating profiles.

By vessel type, platform supply vessels and anchor handling tug supply vessels account for a substantial share of market activity due to their direct relevance to offshore logistics and rig support. Multi-purpose support vessels are also gaining strategic importance because operators value their adaptability across subsea work, maintenance support, and diversified offshore service requirements.

By application, shallow water activity holds a prominent position because offshore supply, crew movement, and maintenance tasks occur with consistent operational frequency in these zones. Deep-water demand remains highly relevant for technically intensive projects, although vessel requirements there are more selective and closely aligned with specialized offshore development programs.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Bourbon Corporation SA

Maersk Supply Service AS

Seacor Marine Holdings Inc.

Edison Chouest Offshore LLC

Swire Pacific Limited

Tidewater Inc.

Harvey Gulf International Marine LLC

Solstad Offshore ASA

Hornbeck Offshore Services Inc.

PACC Offshore Services Holdings Ltd.

Get more information on this report

Offshore Support Vessel Market Report Coverage and Deliverables:

The "Offshore Support Vessel Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all market segments covered under the scope

Market trends, as well as drivers, restraints, and opportunities

Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Offshore Support Vessel Market Geographic Insights:

The offshore support vessel market shows diverse regional adoption patterns influenced by offshore resource maturity, project economics, marine infrastructure, and the pace of renewable energy development. Global demand is shaped by a mix of conventional offshore operations and newer service requirements tied to offshore wind and subsea maintenance. Fleet allocation decisions increasingly reflect route efficiency, vessel specialization, and charter visibility across operating basins.

North America remains a significant operating region because offshore oil and gas programs require dependable vessel support across production, maintenance, and rig-related tasks. Market activity is supported by established service ecosystems, experienced marine operators, and consistent attention to safety and technical compliance. Demand in this region also reflects the need for vessels capable of responding to varied offshore conditions while maintaining high operational readiness.

Asia Pacific presents a broad opportunity set shaped by offshore exploration, regional shipbuilding capabilities, and expanding marine support requirements in energy and infrastructure projects. The region benefits from an active base of vessel owners and builders that can supply different support classes for diverse offshore assignments. In parallel, renewable energy development and coastal industrial expansion are widening the service envelope for adaptable support fleets.

Europe combines mature offshore operating experience with an evolving emphasis on lower-emission vessel deployment and offshore wind support services. Emerging markets across the Middle East, Africa, and South and Central America are also strengthening their relevance as offshore field development and marine logistics programs advance. Together, these regions are contributing to a more distributed demand landscape where fleet flexibility and localized operating knowledge matter increasingly.

Get more information on this report

Offshore Support Vessel Market Research Report Guidance:

The offshore support vessel market report includes qualitative and quantitative data in the offshore support vessel market across vessel type, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the offshore support vessel market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the offshore support vessel market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the offshore support vessel market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover offshore support vessel market segments by vessel type, application, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the offshore support vessel market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Offshore Support Vessel Market News and Key Development:

The offshore support vessel market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

In March 2026, Brazilian services player Oceanica Engenharia has secured new contracts and extensions for six offshore support vessels with Petrobras for operations in the South American nation for a total sum of $736 million. With these new long-term contracts, which were signed between December 2025 and February 2026, Oceanica’s order backlog has increased to approximately 12 billion reais ($2.3 billion).

In November 2024, Norwegian vessel operator Sea1 Offshore, formerly known as Siem Offshore, has placed an order with Chinese shipyard Cosco Shipping for two next-generation offshore energy support vessels (OESVs) that will be methanol-ready. Based on the ST-245 design by Skipsteknisk, the vessels are methanol-ready and the generators can operate on 100% biofuel. Once delivered in 2027, Sea1 will own a fleet of 19 offshore vessels.

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)(International Monetary Fund )IMFInternational Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - Offshore Support Vessel Market

Bourbon Corporation SA

Maersk Supply Service AS

Seacor Marine Holdings Inc.

Edison Chouest Offshore LLC

Swire Pacific Limited

Tidewater Inc.

Harvey Gulf International Marine LLC

Solstad Offshore ASA

Hornbeck Offshore Services Inc.

PACC Offshore Services Holdings Ltd.

Frequently Asked Questions

How big is the Offshore Support Vessel Market?

The Offshore Support Vessel Market is valued at US$ 22.78 Billion in 2025, it is projected to reach US$ 42.79 Billion by 2033.

What is the CAGR for Offshore Support Vessel Market by (2026 - 2033)?

As per our report Offshore Support Vessel Market, the market size is valued at US$ 22.78 Billion in 2025, projecting it to reach US$ 42.79 Billion by 2033. This translates to a CAGR of approximately 8.2% during the forecast period.

What segments are covered in this report?

The Offshore Support Vessel Market report typically cover these key segments-

Vessel Type (Anchor Handling Tug/Anchor Handling Towing Supply Vessels, Platform Supply Vessels, and Other Types)

Application (Offshore Oil and Gas, Offshore Wind, Offshore Decommissioning, and Other Applications)

What is the historic period, base year, and forecast period taken for Offshore Support Vessel Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Offshore Support Vessel Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Offshore Support Vessel Market?

The Offshore Support Vessel Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Bourbon Corporation SA

Maersk Supply Service AS

Seacor Marine Holdings Inc.

Edison Chouest Offshore LLC

Swire Pacific Limited

Tidewater Inc.

Harvey Gulf International Marine LLC

Solstad Offshore ASA

Hornbeck Offshore Services Inc.

PACC Offshore Services Holdings Ltd.

Who should buy this report?

The Offshore Support Vessel Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Offshore Support Vessel Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Offshore Support Vessel Market

Get Free Sample For Offshore Support Vessel Market