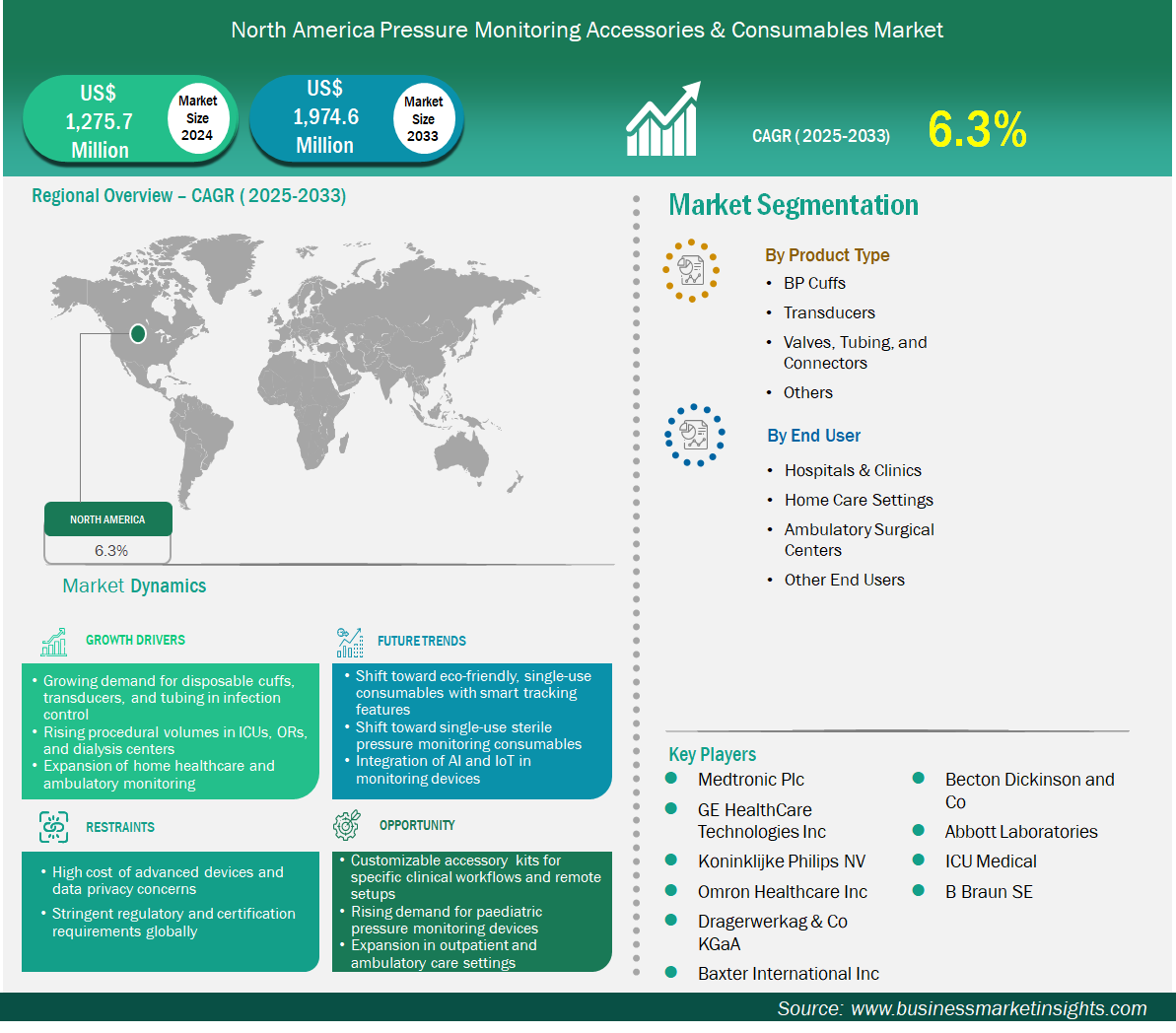

The North America pressure monitoring accessories & consumables market size is expected to reach US$ 1,974.6 million by 2033 from US$ 1,275.7 million in 2024. The market is estimated to record a CAGR of 6.3% from 2025 to 2033.

Executive Summary and North America Pressure Monitoring Accessories & Consumables Market Analysis:

The pressure monitoring accessories & consumables market in North America is experiencing significant growth driven by growing demand for disposable cuffs, transducers, and tubing in infection control, rising procedural volumes in ICUs, ORs, and dialysis centers, expansion of home healthcare and ambulatory monitoring. The pressure monitoring accessories and consumables market in North America is highly mature, strongly regulated, and technologically advanced in both invasive and non‑invasive monitoring methods. Usage is heavily dominated by BP cuffs, which is a direct reflection of the large hypertension burden in the region. Demand is thus largely hospital and clinic-driven through routine diagnostics, preventive screenings, and chronic disease management programs. Besides, transducers, valves, tubing, and connectors are mainly ICU and surgical department consumables, where invasive monitoring is the norm. The market is supported with supportive reimbursement schemes, thus enabling the continued purchase of both reusable and disposable consumables. Infection control measures are very strict, thus aiding the faster transition to the adoption of single‑use products. Distribution channels are very efficient, thus multinational manufacturers are able to have direct dealings with hospital groups and integrated delivery networks. Among the features of digital transducers, smart cuffs, and disposable connectors with traceability features are increasingly being adopted. Replacement cycles, preventive care mandates, and the integration of consumables into connected monitoring systems influence market dynamics.

North America Pressure Monitoring Accessories & Consumables Market Segmentation Analysis:

Key segments that contributed to the derivation of the pressure monitoring accessories & consumables market analysis are product and end user.

By product, the pressure monitoring accessories & consumables market is segmented into BP cuffs, transducers, valves, tubing, and connectors, and others. The BP cuffs segment dominated the market in 2024. This is the largest segment due to their routine use in hypertension screening and chronic disease management across the US and Canada.

By end user, the market is segmented into hospitals and clinics, home-care settings, ambulatory surgical centers, and other end users. The hospitals and clinics segment held the largest market share in 2024. This is the largest segment due to their advanced infrastructure and high patient throughput, making them the primary consumers of monitoring consumables.

North America Pressure Monitoring Accessories & Consumables Market Outlook

The North American pressure monitoring accessories and consumables market narrative is revolving around continuous innovation, regulatory compliance, and integration into digital health ecosystems. Though the BP cuffs will be the largest category, the growth will be gradual, reflecting the maturity of the market. Transducers and sterile tubing sets are predicted to grow faster than the total growth; thus, they will be supported by the expansion of the critical care capacity and the adoption of minimally invasive surgical procedures. Disposable consumables will become more popular as infection control continues to be the top priority, which is supported by the Centers for Disease Control (CDC) guidelines and hospital accreditation standards. Telehealth and remote monitoring will transform product usage, making portable cuffs and simplified connector systems suitable for home use care. The collaboration between manufacturers and integrated health systems will be on bundled procurement, inventory analytics, and cost optimization. Product design and distribution will still be influenced by regulatory frameworks such as FDA approvals and ISO compliance. Overall, the market forecast is steady, with innovation and preventive care strategies being the reasons for sustained demand in both invasive and non-invasive categories.

North America Pressure Monitoring Accessories & Consumables Market Country Insights

Based on country, the North America pressure monitoring accessories & consumables market is segmented into the United States, Canada, and Mexico. The United States held the largest share in 2024.

National-level changes reveal variations between the US, Canada, and Mexico. In the United States, demand is dominated by big hospital networks, outpatient clinics, and community health programs, where BP cuffs are the most used equipment due to the widespread screening of hypertension. Besides, ICUs and surgical centers are the places where transducers and sterile tubing are mostly used, showing the country's advanced critical care infrastructure. Private insurance and Medicare reimbursement are two of the main factors that keep procurement going at a steady pace, while domestic manufacturers' pipelines of innovation are the reason for the smart consumables' adoption. On the other hand, Canada puts more emphasis on preventive care through its publicly funded healthcare system, with a great demand for BP cuffs in primary care and community clinics. Canadian hospitals are the ones that lead the way in the use of disposable transducers and connectors, thus aligning themselves with infection control priorities. Besides, universities like the University of Toronto and McGill University contribute to the development of monitoring technologies, which is a factor that consolidates Canada's position in the consumables goods industry. The US and Canada, thus, make up a mature, innovation-driven market where consumables are vital in both preventive and acute care strategies.

North America Pressure Monitoring Accessories & Consumables Market Company Profiles

Medtronic Plc, GE HealthCare Technologies Inc, Koninklijke Philips NV, Omron Healthcare Inc, Baxter International Inc, Becton Dickinson and Co, Abbott Laboratories, ICU Medical, B Braun SE, and Dragerwerk AG & Co KGaA are among the key players operating in the market. These players adopt strategies such as expansion, product innovation, and mergers and acquisitions to stay competitive in the market and offer innovative products to their consumers.

North America Pressure Monitoring Accessories & Consumables Market Research Methodology:

The following methodology has been followed for the collection and analysis of data presented in this report:

Secondary Research

The research process begins with comprehensive secondary research, utilizing both internal and external sources to gather qualitative and quantitative data for each market. Commonly referenced secondary research sources include, but are not limited to:

Company websites, annual reports, financial statements, broker analyses, and investor presentations

Industry trade journals and other relevant publications

Government documents, statistical databases, and market reports

News articles, press releases, and webcasts specific to companies operating in the market

Note: All financial data included in the Company Profiles section has been standardized to US$. For companies reporting in other currencies, figures have been converted to US$ using the relevant exchange rates for the corresponding year.

Primary Research

Business Market Insights conducts a significant number of primary interviews each year with industry stakeholders and experts to validate and analyze the data and gain valuable insights. These research interviews are designed to:

Refine findings from secondary research

Enhance the expertise and market understanding of the analysis team

Gain insights into market size, trends, growth patterns, competitive dynamics, and future prospects

Primary research is conducted via email interactions and telephone interviews with industry experts across various markets, categories, segments, and sub-segments in different regions. Participants typically include:

Industry stakeholders: Vice Presidents, business development managers, market intelligence managers, and national sales managers

External experts: Valuation specialists, research analysts, and key opinion leaders with industry-specific expertise

Key Sources Referred:

World Health Organization (WHO)

Organisation for Economic Cooperation and Development (OECD)

The World Bank Group

Worldometer

The Lancet

BMC Medical Education

Eurostat

North America Pressure Monitoring Accessories & Consumables Market Strategic Insights

Get more information on this report

North America Pressure Monitoring Accessories & Consumables Market Segmentation Analysis

North America Pressure Monitoring Accessories & Consumables Market Report Highlights

Report Attribute

Details

Market size in 2024

US$ 1,275.7 Million

Market Size by 2033

US$ 1,974.6 Million

CAGR (2025 - 2033)

6.3%

Historical Data

2022-2023

Forecast period

2025-2033

Segments Covered

By Product

BP Cuffs

Transducers

Valves

Tubing

Connectors

Others

By End User

Hospitals & Clinics

Home Care Settings

Ambulatory Surgical Centers

Other End Users

Regions and Countries Covered

North America

United States, Canada, Mexico

Market leaders and key company profiles

Medtronic Plc

GE HealthCare Technologies Inc

Koninklijke Philips NV

Omron Healthcare Inc

Baxter International Inc

Becton Dickinson and Co

Abbott Laboratories

ICU Medical

B Braun SE

Dragerwerk AG & Co KGaA

Get more information on this report

North America Pressure Monitoring Accessories & Consumables Market Company Profiles

North America Pressure Monitoring Accessories & Consumables Market Country and Regional Insights

Get more information on this report

Identical Market Reports with other Region/Countries

The List of Companies - North America Pressure Monitoring Accessories & Consumables Market

Medtronic Plc GE HealthCare Technologies Inc Koninklijke Philips NV Omron Healthcare Inc Baxter International Inc Becton Dickinson and Co Abbott Laboratories ICU Medical B Braun SE Dragerwerk AG & Co KGaA

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the North America Pressure Monitoring Accessories & Consumables Market?

The North America Pressure Monitoring Accessories & Consumables Market is valued at US$ 1,275.7 Million in 2024, it is projected to reach US$ 1,974.6 Million by 2033.

What is the CAGR for North America Pressure Monitoring Accessories & Consumables Market by (2025 - 2033)?

As per our report North America Pressure Monitoring Accessories & Consumables Market, the market size is valued at US$ 1,275.7 Million in 2024, projecting it to reach US$ 1,974.6 Million by 2033. This translates to a CAGR of approximately 6.3% during the forecast period.

What segments are covered in this report?

The North America Pressure Monitoring Accessories & Consumables Market report typically cover these key segments-

End User (Hospitals & Clinics, Home Care Settings, Ambulatory Surgical Centers, Other End Users)

What is the historic period, base year, and forecast period taken for North America Pressure Monitoring Accessories & Consumables Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the North America Pressure Monitoring Accessories & Consumables Market report:

Historic Period : 2022-2023

Base Year : 2024

Forecast Period : 2025-2033

Who are the major players in North America Pressure Monitoring Accessories & Consumables Market?

The North America Pressure Monitoring Accessories & Consumables Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Medtronic Plc

GE HealthCare Technologies Inc

Koninklijke Philips NV

Omron Healthcare Inc

Baxter International Inc

Becton Dickinson and Co

Abbott Laboratories

ICU Medical

B Braun SE

Dragerwerk AG & Co KGaA

Who should buy this report?

The North America Pressure Monitoring Accessories & Consumables Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the North America Pressure Monitoring Accessories & Consumables Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For North America Pressure Monitoring Accessories & Consumables Market

Get Free Sample For North America Pressure Monitoring Accessories & Consumables Market