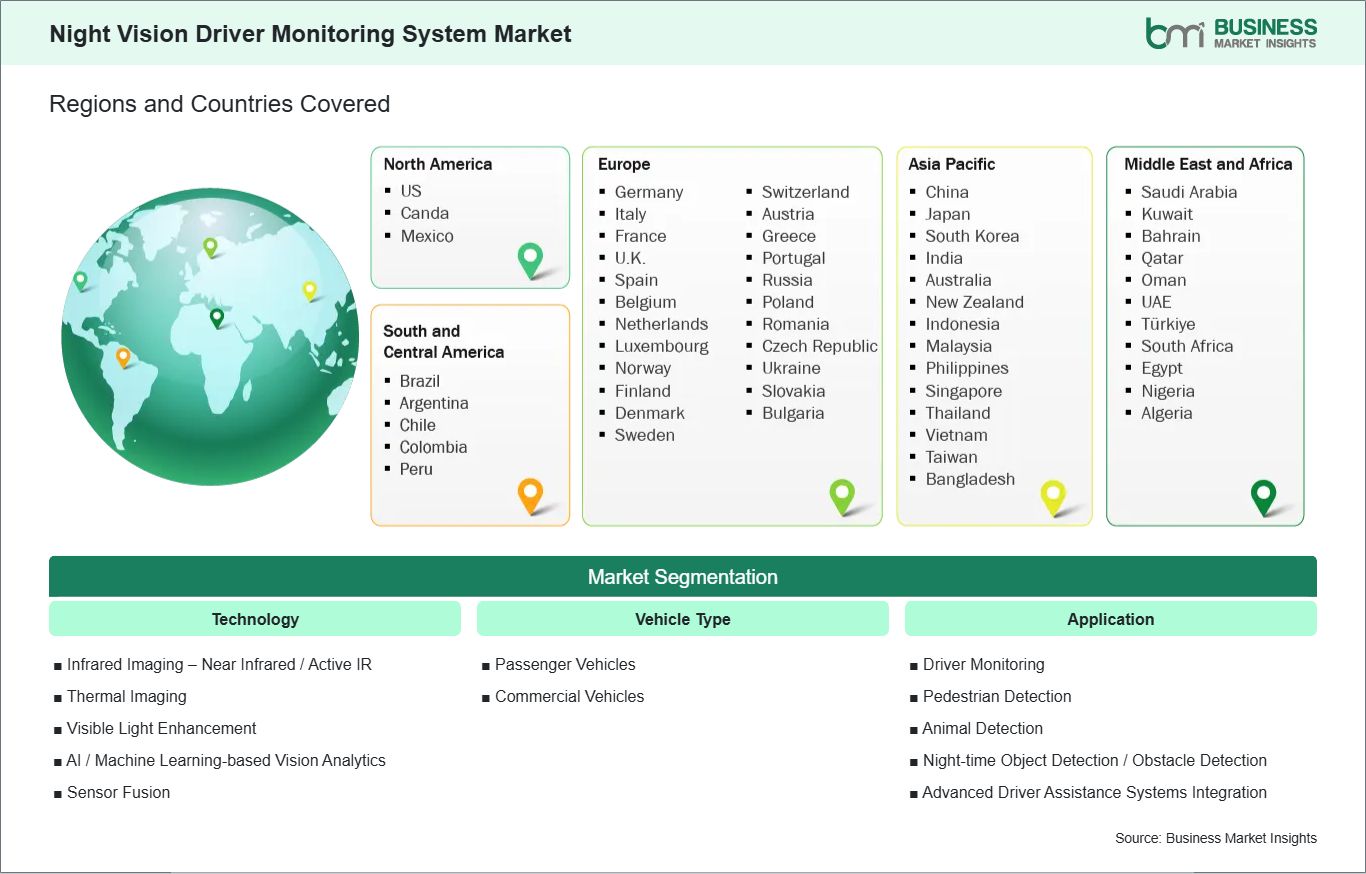

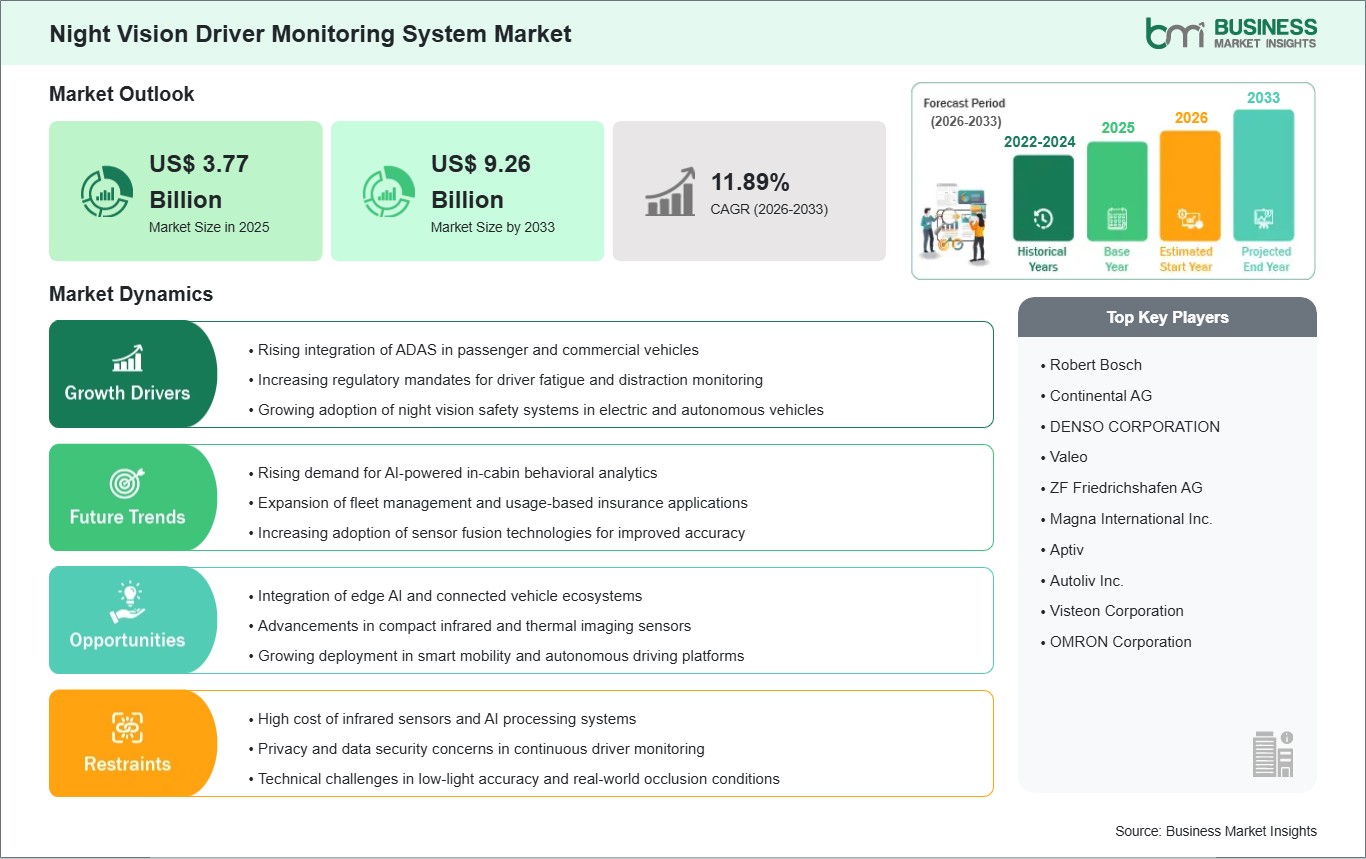

Night Vision Driver Monitoring System Market Segmentation

The night vision driver monitoring system market is segmented based on technology, vehicle type, and application, reflecting the increasing integration of intelligent sensing and AI-driven safety solutions across modern automotive systems.

By Technology

- Infrared (Near-Infrared / Active IR): Utilizes NIR illumination to track driver eye movement, gaze direction, and facial behavior in low-light and night conditions

- Thermal Imaging: Detects heat signatures to monitor driver presence, alertness, and physiological state regardless of visible lighting conditions

- Visible Light Enhancement: Improves low-light cabin visibility by amplifying ambient light for clearer image capture and analysis

- AI / Machine Learning-based Vision Analytics: Applies deep learning algorithms to interpret driver fatigue, distraction, and behavioral anomalies in real time

- Sensor Fusion: Combines multiple data sources such as infrared, thermal, and visible imaging to enhance accuracy and reliability of driver monitoring

By Vehicle Type

- Passenger Vehicles: Includes private cars and SUVs equipped with advanced safety and driver assistance features

- Commercial Vehicles: Covers trucks, buses, and fleet vehicles where driver safety and fatigue monitoring are critical for operational efficiency

By Application

- Driver Monitoring (DMS): Focuses on detecting drowsiness, distraction, and unsafe driving behavior to improve road safety

- Pedestrian Detection: Identifies pedestrians in night-time environments to prevent collisions and enhance situational awareness

- Animal Detection: Detects animals on roads during low-visibility conditions, reducing accident risks in rural and highway areas

- Night-time Object Detection / Obstacle Detection: Identifies road obstacles such as debris, vehicles, or sudden hazards in darkness

- Advanced Driver Assistance Systems (ADAS) Integration: Supports broader vehicle safety systems by feeding real-time driver and environment data into ADAS platforms