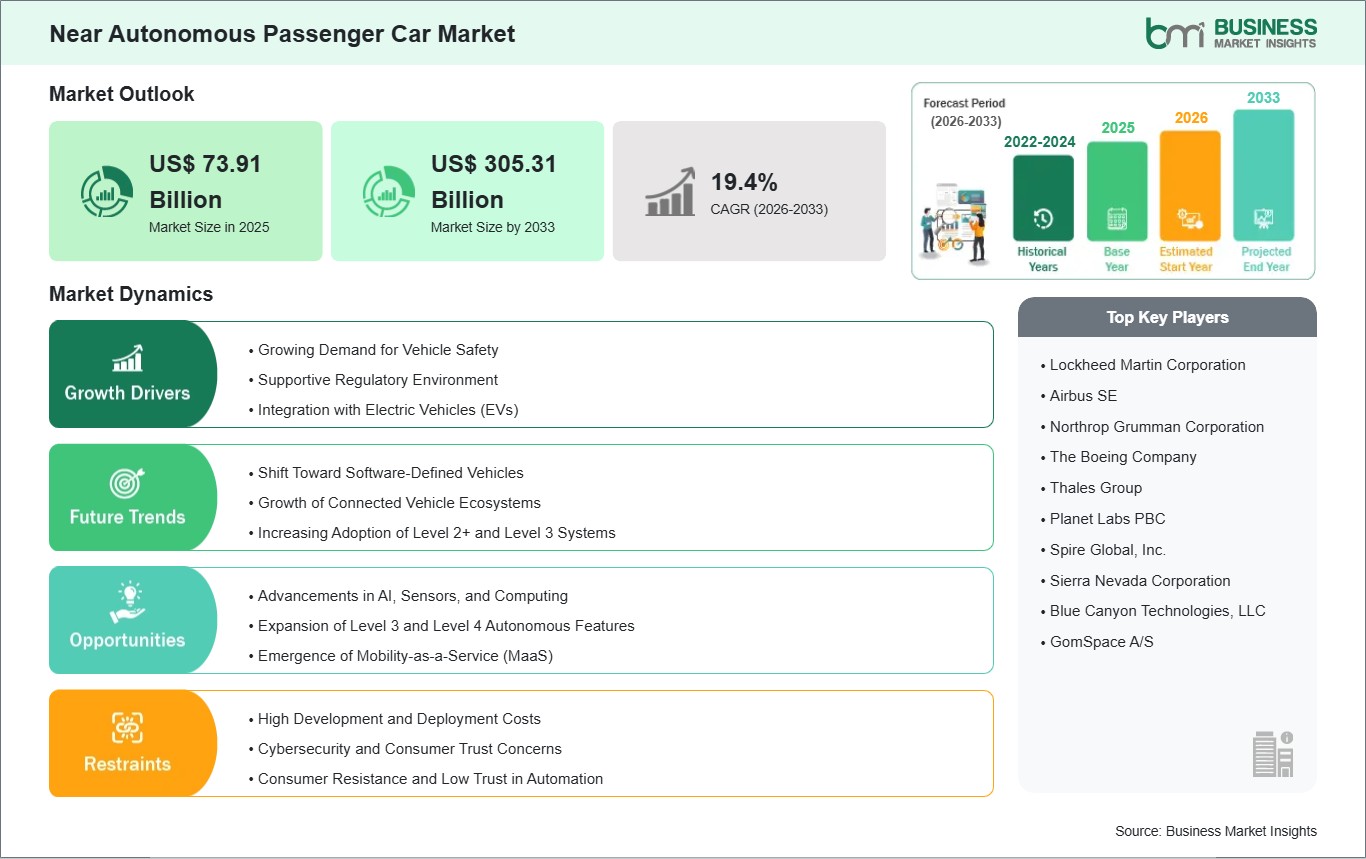

The Near Autonomous Passenger Car market size is expected to reach US$ 305.31 Billion by 2033 from US$ 73.91 Billion in 2025. The market is estimated to record a CAGR of 19.4% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Near autonomous passenger cars combine advanced driver assistance, sensor fusion, and software control to automate selected driving functions under supervised conditions. These vehicles support steering, braking, acceleration, lane positioning, and traffic response through coordinated hardware and software systems that reduce routine driving workload while keeping the driver engaged in oversight.

Market expansion is linked to tighter vehicle safety expectations, stronger consumer interest in convenience features, and broader integration of assisted driving into premium and upper mid-range models. Automakers are positioning supervised automation as a product differentiator, while regulators are advancing assessment frameworks that encourage more consistent deployment of driver assistance capabilities.

Segmentation patterns show broad relevance across hatchbacks, sedans, and SUVs, with SUVs holding strong visibility because they often carry feature-rich electronic platforms. Hardware remains fundamental through cameras, radar, controllers, and sensing modules, while software governs perception logic and decision support. Services are gaining importance as calibration, updates, and validation requirements become more frequent.

Technology evolution is moving toward higher-function supervised driving with better mapping support, improved driver monitoring, over-the-air upgrades, and more integrated vehicle computing architectures. Electric vehicles present a favorable environment for these systems because digital-first platforms simplify software deployment, system coordination, and future feature expansion without requiring a full vehicle redesign.

Competitive intensity is shaped by control over sensing stacks, software maturity, validation capability, and the ability to deliver reliable supervised automation across different passenger car classes. Suppliers and automakers compete through system refinement, feature packaging, update strategies, and ecosystem partnerships that improve performance, user trust, and regulatory alignment within this evolving sector.

Near Autonomous Passenger Car Market - Strategic Insights:

Get more information on this report

Near Autonomous Passenger Car Market Segmentation Analysis:

The near autonomous passenger car market is segmented by vehicle type, component, and propulsion type across supervised driving deployment models.

By Vehicle Type

Hatchbacks: Compact architectures support selective automation in urban-oriented driving environments.

Sedans: Balanced packaging enables refined integration of supervised driving functions.

SUVs: Higher feature bundling strengthens deployment across premium and family-focused models.

Other Vehicle Type: Niche passenger formats adopt automation according to platform capability.

By Component

Hardware: Sensors and control units establish the physical automation foundation.

Software: Perception and decision layers coordinate supervised driving responses.

Services: Calibration, validation, and updates sustain system accuracy over time.

By Propulsion Type

Internal Combustion Engine (ICE): Established model ranges expand supervised features through incremental upgrades.

Electric Vehicles (Evs): Digital platforms ease deeper integration of automated driving functions.

Near Autonomous Passenger Car Market Drivers and Opportunities:

Rising Safety Expectations and Feature Differentiation Expanding Supervised Driving Integration

Passenger car buyers increasingly expect active safety, reduced driving strain, and intuitive control support during congested and highway travel. That expectation is pushing automakers to integrate lane centering, adaptive cruise coordination, and collision mitigation into broader supervised driving packages. As these capabilities become more visible in mainstream product planning, near autonomous systems move from optional enhancement toward a more central value proposition.

The commercial effect reaches vehicle positioning, pricing strategy, and platform engineering across multiple passenger car categories. Brands use these systems to reinforce premium perception, strengthen safety credentials, and support software-led product upgrades. In this context, the market gains relevance wherever supervised automation can improve daily usability without shifting responsibility away from the driver in real-world road conditions.

Software-Defined Vehicle Architectures Creating New Scope for Feature Expansion

A notable opportunity is forming around software-defined passenger cars that can accept performance improvements through remote updates and centralized computing. This architecture supports faster refinement of lane guidance, automated parking, traffic assistance, and driver monitoring functions. It also enables automakers to tailor supervised driving packages across trims and propulsion formats without rebuilding the full electronic foundation for each model line.

Future scope extends into broader feature personalization, stronger service ecosystems, and more scalable deployment across passenger vehicles with different use patterns. Expansion can also emerge from better coordination between hardware, software, and post-sale support. As supervised automation matures, this opportunity can improve lifecycle value, support recurring digital revenue, and widen the strategic role of near autonomous capabilities within the passenger car industry.

Near Autonomous Passenger Car Market Size and Share Analysis:

The Near Autonomous Passenger Car market size is expected to reach US$ 305.31 Billion by 2033 from US$ 73.91 Billion in 2025. The market is estimated to record a CAGR of 19.4% from 2026 to 2033. This trajectory indicates a transition from feature-specific assistance toward more integrated supervised driving packages across passenger vehicle portfolios, supported by stronger software capabilities, richer sensing configurations, and broader consumer familiarity with assisted mobility.

Among vehicle types, SUVs hold a prominent position because manufacturers frequently introduce advanced digital features in this class before extending them to other body styles. On the component side, hardware remains foundational because sensing, processing, and actuation quality directly shape feature reliability. Software is also becoming central as supervised automation depends on continuous refinement of perception, control logic, and human-machine coordination.

By application context, highway and dense-traffic assistance functions command attention because they address repetitive driving situations where support features are most visible to users. Parking and lane management capabilities also sustain strong relevance as they demonstrate automation benefits in everyday ownership. Across propulsion formats, electric passenger cars show notable alignment with these functions because their digital architectures simplify deeper system integration.

Near Autonomous Passenger Car Market Report Highlights:

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Lockheed Martin Corporation

Airbus SE

Northrop Grumman Corporation

The Boeing Company

Thales Group

Planet Labs PBC

Spire Global, Inc.

Sierra Nevada Corporation

Blue Canyon Technologies, LLC

GomSpace A/S

Get more information on this report

Near Autonomous Passenger Car Market Report Coverage and Deliverables:

The " Near Autonomous Passenger Car Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Near Autonomous Passenger Car Market Geographic Insights:

The Near Autonomous Passenger Car market shows diverse regional adoption patterns influenced by regulatory direction, digital vehicle architectures, consumer readiness, and manufacturing strategies. Globally, the sector is moving through a supervised automation phase where automakers refine assisted driving performance while balancing safety validation, feature monetization, and platform scalability across passenger car portfolios.

North America remains influential because the region combines premium vehicle demand, active software development, and evolving assessment standards for advanced driver assistance systems. Passenger car manufacturers continue to introduce supervised driving packages through technology-led trims and subscription-ready platforms. This environment supports deployment models that emphasize user convenience, highway assistance, and stronger integration between sensing, computing, and driver monitoring systems.

Asia Pacific is gaining momentum through large vehicle production bases, fast digital feature commercialization, and strong consumer exposure to connected mobility functions. Several passenger car programs in the region incorporate supervised driving as part of broader software-centric positioning. The region also benefits from a deep electronics supply chain, which supports quicker integration of sensors, controllers, and in-vehicle computing for near autonomous applications.

Europe emphasizes disciplined safety engineering, functional validation, and premium vehicle differentiation, which together support steady deployment of supervised automation in passenger cars. Beyond Europe, emerging markets in the Middle East and Africa and South and Central America are adopting these features more selectively, usually through upper-end models and imported platforms. Their progress depends on affordability, infrastructure compatibility, and the pace of electronic feature localization.

Get more information on this report

Near Autonomous Passenger Car Market Research Report Guidance:

The Near Autonomous Passenger Car market report includes qualitative and quantitative data in the market across vehicle type, component, propulsion type, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover market segments by vehicle type, component, propulsion type, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Near Autonomous Passenger Car Market News and Key Development:

The near autonomous passenger car market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

May 2026: Stellantis and Wayve have entered a strategic technology partnership under which Stellantis will integrate the Wayve AI Driver into its STLA AutoDrive platform, supporting hands-free Level 2++ supervised automated driving across urban and highway environments. The first vehicle integration is scheduled to launch in North America in 2028.

November 2025: MOIA America, LLC, a Volkswagen Group company working on autonomous mobility technology, and Uber Technologies, Inc. announced the start of on-road validation testing of purpose-built, autonomous ID. Buzz vehicles in Los Angeles, marking the next phase of their strategic partnership introduced last year.

Key Sources Referred:

United Nations Economic Commission for Europe (UNECE)OECD International Transport Forum (ITF)National Highway Traffic Safety Administration (NHTSA)United States Department of Transportation (USDOT)Ministry of Industry and Information Technology (MIIT)Company filingsAcademic studiesTechnical journalsRegulatory and standards documentation

The List of Companies - Near Autonomous Passenger Car Market

Lockheed Martin Corporation

Airbus SE

Northrop Grumman Corporation

The Boeing Company

Thales Group

Planet Labs PBC

Spire Global, Inc.

Sierra Nevada Corporation

Blue Canyon Technologies, LLC

GomSpace A/S

Frequently Asked Questions

How big is the Near Autonomous Passenger Car Market?

The Near Autonomous Passenger Car Market is valued at US$ 73.91 Billion in 2025, it is projected to reach US$ 305.31 Billion by 2033.

What is the CAGR for Near Autonomous Passenger Car Market by (2026 - 2033)?

As per our report Near Autonomous Passenger Car Market, the market size is valued at US$ 73.91 Billion in 2025, projecting it to reach US$ 305.31 Billion by 2033. This translates to a CAGR of approximately 19.4% during the forecast period.

What segments are covered in this report?

The Near Autonomous Passenger Car Market report typically cover these key segments-

Vehicle Type (Hatchbacks, Sedans, SUVs, Other Vehicle Type)

Component (Hardware, Software, Services)

Propulsion Type (Internal Combustion Engine (ICE), Electric Vehicles (Evs))

What is the historic period, base year, and forecast period taken for Near Autonomous Passenger Car Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Near Autonomous Passenger Car Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Near Autonomous Passenger Car Market?

The Near Autonomous Passenger Car Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Lockheed Martin Corporation

Airbus SE

Northrop Grumman Corporation

The Boeing Company

Thales Group

Planet Labs PBC

Spire Global, Inc.

Sierra Nevada Corporation

Blue Canyon Technologies, LLC

GomSpace A/S

Who should buy this report?

The Near Autonomous Passenger Car Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Near Autonomous Passenger Car Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Near Autonomous Passenger Car Market

Get Free Sample For Near Autonomous Passenger Car Market