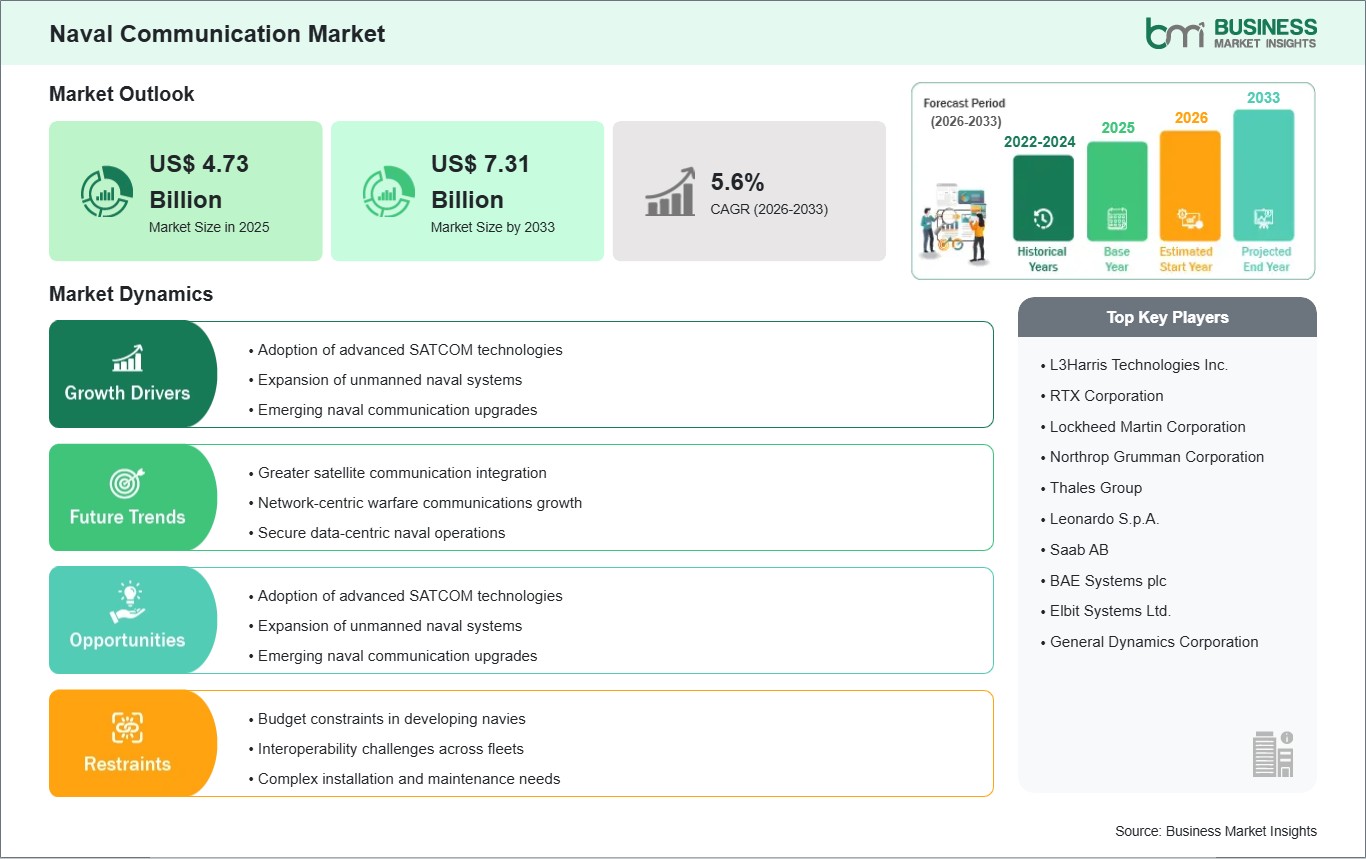

The Naval Communication market size is expected to reach US$ 7.31 Billion by 2033 from US$ 4.73 Billion in 2025. The market is estimated to record a CAGR of 5.6% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Naval communication systems comprise integrated voice, data, and secure networking architectures used across maritime forces to coordinate missions at sea. These systems connect ships, submarines, unmanned platforms, and command centers through radio, satellite, security, and communication management technologies that support operational continuity in contested and routine environments alike.

Procurement activity is being shaped by fleet modernization priorities, wider electromagnetic threat exposure, and the need for uninterrupted information exchange during distributed operations. Naval forces are strengthening communication resilience to maintain command clarity, improve coordination between platforms, and support mission execution where bandwidth availability, signal integrity, and interoperability remain operational priorities.

Segment analysis indicates platform requirements differ significantly across surface vessels, submarines, and unmanned systems. Ships require broad multi-channel connectivity for fleet coordination, while submarines emphasize low-signature transmission and reception. Across applications, command and control and intelligence surveillance and reconnaissance remain central, while routine operations preserve steady demand for dependable onboard and fleetwide communication support.

Technology development is advancing toward software-defined radio architectures, hardened cyber layers, integrated satcom terminals, and centralized communication management environments. These improvements allow naval operators to move between legacy and next-generation networks with greater control, while supporting secure data exchange, lower operator burden, and more adaptive communication behavior across complex maritime operating scenarios.

Competitive conditions are defined by long program cycles, platform-specific integration expertise, and the ability to support secure multi-domain connectivity. Suppliers compete through lifecycle sustainment capabilities, modular system design, cybersecurity depth, and compatibility with naval command frameworks. The market environment therefore favors participants that can align product performance with evolving fleet architectures and mission-specific communication demands.

Naval Communication Market - Strategic Insights:

Get more information on this report

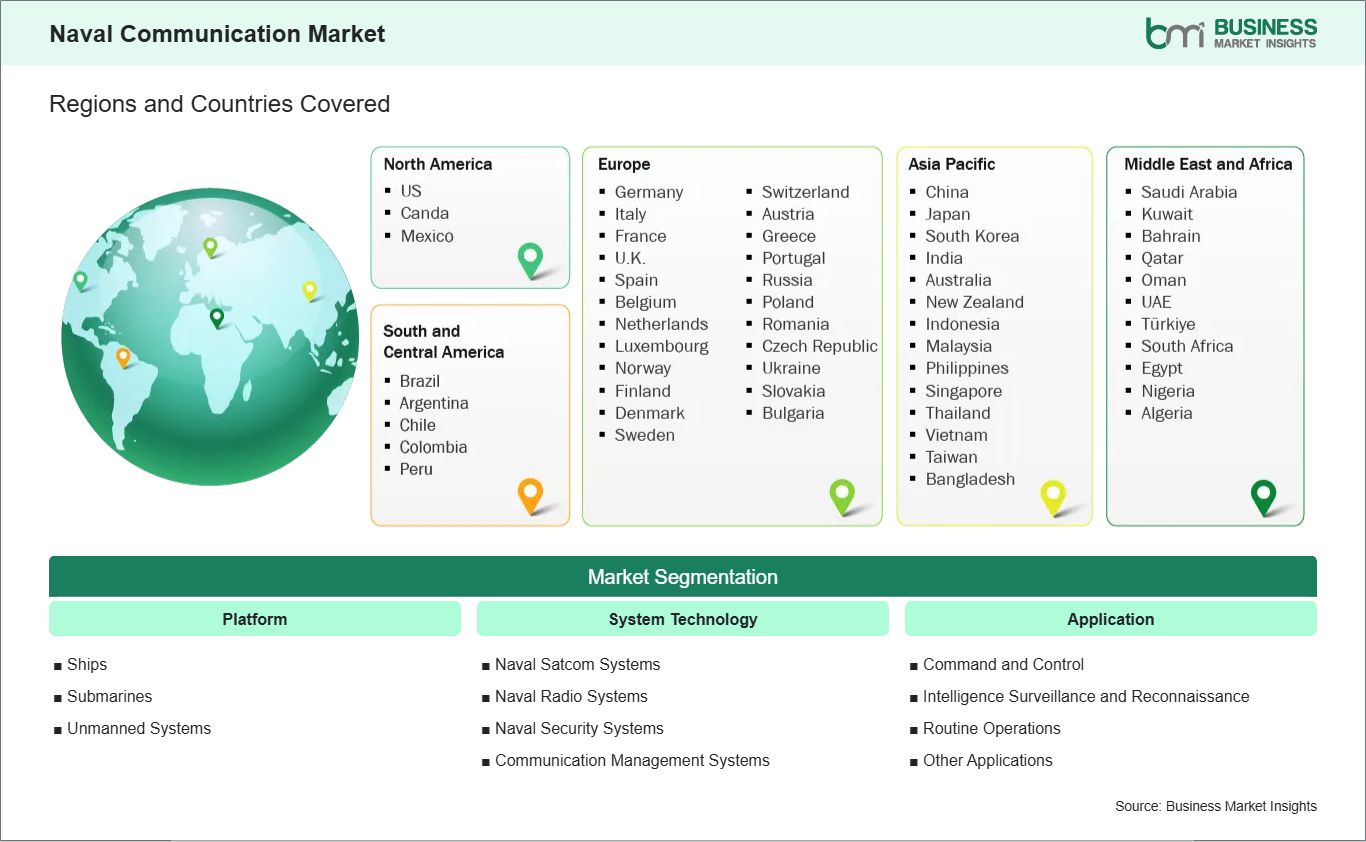

Naval Communication Market Segmentation Analysis:

The naval communication market is segmented by platform, system technology, and application across mission-specific maritime communication environments.

By Platform

Ships: Support fleet coordination through layered external and internal communication networks.

Submarines: Prioritize discreet signal handling under constrained and high-security operating conditions.

Unmanned Systems: Extend remote mission connectivity for autonomous and semi-autonomous naval operations.

By System Technology

Naval Satcom Systems: Enable beyond-line-of-sight exchange across dispersed fleets and shore commands.

Naval Radio Systems: Maintain tactical voice and data communication across dynamic maritime theatres.

Naval Security Systems: Protect transmission integrity through encryption, access control, and cyber hardening.

Communication Management Systems: Unify multiple channels through centralized monitoring and operator control.

By Application

Command and Control: Coordinates platform decisions through secure and continuous information flow.

Intelligence Surveillance and Reconnaissance: Transmits mission data supporting timely maritime awareness and targeting.

Routine Operations: Sustains navigation, logistics, maintenance, and shipboard coordination requirements.

Other Applications: Covers training, distress communication, interoperability, and specialized mission support.

Naval Communication Market Drivers and Opportunities:

Fleet Modernization Programs and Network Resilience Requirements Strengthening System Procurement

Naval operators are modernizing fleet communication suites to support distributed missions, faster coordination, and more secure information handling across maritime theatres. Legacy infrastructures often lack the flexibility needed for synchronized communication between ships, submarines, unmanned systems, and shore assets. This capability gap is encouraging procurement of integrated satcom, radio, and communication management technologies that improve continuity across operational scenarios.

The procurement impact extends into system interoperability, cyber protection, and mission assurance across joint and coalition structures. As fleets adopt more connected operating models, communication systems become more relevant to force readiness and decision execution. This context sustains demand for architectures that support secure transmission, adaptive routing, and multi-platform coordination without compromising operational control in high-pressure maritime environments.

Software-Defined Communication Architectures and Autonomous Platforms Opening New Integration Pathways

A notable opportunity is emerging from software-defined communication environments that allow naval forces to update functions without replacing full hardware stacks. At the same time, unmanned systems are entering broader maritime roles and require communication frameworks that can sustain remote control, secure telemetry, and mission data transfer. These trends support innovation in modular systems designed for flexible deployment across mixed-platform fleets.

Future scope lies in communication architectures that can connect manned and unmanned assets within a shared operational picture while reducing upgrade complexity. Expansion potential is especially relevant where navies seek scalable systems for multi-domain missions and evolving threat profiles. This direction can widen the role of secure communication management, encourage subsystem integration, and deepen the market's relevance across next-generation fleet programs.

Naval Communication Market Size and Share Analysis:

The Naval Communication market size is expected to reach US$ 7.31 Billion by 2033 from US$ 4.73 Billion in 2025. The market is estimated to record a CAGR of 5.6% from 2026 to 2033. This progression reflects sustained investment in maritime network resilience, platform interoperability, and secure information exchange as navies refine communication architectures for more distributed and digitally coordinated operations.

By platform, ships account for a leading position because they require extensive external and internal communication coverage during fleet maneuvers, patrol duties, and mission coordination. By system technology, naval radio systems and communication management systems retain strong relevance due to their central role in tactical exchange, channel orchestration, and continuity across mixed communication environments.

Application leadership is centered on command and control, where communication reliability directly affects mission direction, force synchronization, and operational response. Intelligence surveillance and reconnaissance also maintains substantial importance as naval platforms require dependable transfer of sensed information across command structures. Routine operations preserve a broad usage base through everyday navigation, maintenance, and onboard coordination functions.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

L3Harris Technologies Inc.

RTX Corporation

Lockheed Martin Corporation

Northrop Grumman Corporation

Thales Group

Leonardo S.p.A.

Saab AB

BAE Systems plc

Elbit Systems Ltd.

General Dynamics Corporation

Get more information on this report

Naval Communication Market Report Coverage and Deliverables:

The " Naval Communication Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Naval Communication Market Geographic Insights:

The Naval Communication market shows diverse regional adoption patterns influenced by naval modernization agendas, threat perceptions, platform readiness, and domestic integration capabilities. At a global level, the sector is advancing as maritime forces place greater emphasis on secure connectivity, coordinated fleet behavior, and communication architectures that can function across legacy assets and digitally evolving naval environments.

North America remains a key market because naval communication programs are closely tied to command modernization, mission networking, and information warfare readiness. Procurement emphasis extends across surface vessels, submarines, and unmanned platforms, with strong focus on communication resilience and integration across fleet systems. The region also benefits from established defense contractors and advanced program management structures that support sustained system upgrades.

Asia Pacific is progressing through expanding naval capability programs, wider maritime surveillance requirements, and increased attention to sovereign defense technology development. Regional navies are investing in communication systems that improve fleet coordination across broad maritime zones and support more responsive mission execution. This setting creates demand for adaptable radio, satcom, and secure management solutions aligned with both operational growth and regional industrial participation.

Europe emphasizes interoperable naval communication frameworks shaped by alliance commitments, cyber preparedness, and long-term fleet sustainment requirements. Beyond Europe, emerging markets in the Middle East and Africa and South and Central America are building demand through maritime security priorities, coastal surveillance needs, and selective naval modernization efforts. These regions are adopting communication upgrades with a practical focus on mission reliability, secure control, and platform longevity.

Get more information on this report

Naval Communication Market Research Report Guidance:

The Naval Communication market report includes qualitative and quantitative data in the market across platform, system technology, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover market segments by platform, system technology, application, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Naval Communication Market News and Key Development:

The naval communication market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

February 2026: L3Harris Technologies has received its largest full-rate production contract for communications systems from General Dynamics Electric Boat to deliver 26 shipsets for Virginia- and Columbia-class submarines. By utilizing state-of-the-art technology, these systems will enhance situational awareness and communication across submarine crews.

January 2026: EID is finalising preparations for its presence at Navy Tech 2026 in Gothenburg, Sweden. The company showcase its latest innovations in naval communications and integrated systems. The next-generation naval communications platform, designed to deliver reliable, secure and adaptable command and control solutions for modern naval operations.

Key Sources Referred:

Defence Research and Development Organisation (DRDO)Department of Defense (DoD)Federal Maritime and Hydrographic AgencyInternational Mobile Satellite Organization (IMSO)Armed Forces Communications and Electronics Association (AFCEA)Company filings and official press releasesIndustry reports on maritime communication systemsAcademic studies on naval networking and secure communicationsPeer-reviewed defense and maritime technology journalsConference papers on naval electronics and mission systems

The List of Companies - Naval Communication Market

L3Harris Technologies Inc.

RTX Corporation

Lockheed Martin Corporation

Northrop Grumman Corporation

Thales Group

Leonardo S.p.A.

Saab AB

BAE Systems plc

Elbit Systems Ltd.

General Dynamics Corporation

Frequently Asked Questions

How big is the Naval Communication Market?

The Naval Communication Market is valued at US$ 4.73 Billion in 2025, it is projected to reach US$ 7.31 Billion by 2033.

What is the CAGR for Naval Communication Market by (2026 - 2033)?

As per our report Naval Communication Market, the market size is valued at US$ 4.73 Billion in 2025, projecting it to reach US$ 7.31 Billion by 2033. This translates to a CAGR of approximately 5.6% during the forecast period.

What segments are covered in this report?

The Naval Communication Market report typically cover these key segments-

Platform (Ships, Submarines, Unmanned Systems)

System Technology (Naval Satcom Systems, Naval Radio Systems, Naval Security Systems, Communication Management Systems)

Application (Command and Control, Intelligence Surveillance and Reconnaissance, Routine Operations, Other Applications)

What is the historic period, base year, and forecast period taken for Naval Communication Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Naval Communication Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Naval Communication Market?

The Naval Communication Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

L3Harris Technologies Inc.

RTX Corporation

Lockheed Martin Corporation

Northrop Grumman Corporation

Thales Group

Leonardo S.p.A.

Saab AB

BAE Systems plc

Elbit Systems Ltd.

General Dynamics Corporation

Who should buy this report?

The Naval Communication Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Naval Communication Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Naval Communication Market

Get Free Sample For Naval Communication Market