01

Market Summery

Executive Summary and Global Market Analysis

Nanosatellites and microsatellites are compact spacecraft engineered to perform targeted orbital missions with lower build complexity and shorter deployment cycles. Their architecture supports payload flexibility across imaging, communications, sensing, and experimental programs, making them suitable for operators seeking responsive access to space-based capability.

Market momentum is shaped by the need for faster mission execution, lower launch barriers, and adaptable satellite constellations. Government agencies, commercial operators, and research institutions are expanding deployment as smaller platforms allow mission-specific design, phased constellation scaling, and more efficient replacement strategies in low Earth orbit.

Segmentation reveals clear differences in platform use and mission preference. Nanosatellites support cost-sensitive and rapid-cycle programs, while microsatellites accommodate broader payload requirements. Among applications, Earth observation and communication remain central deployment areas, while scientific research, navigation, reconnaissance, and technology demonstration sustain specialized demand across end-user groups.

Technology progress is refining propulsion, onboard processing, miniaturized sensors, inter-satellite links, and mission autonomy within compact form factors. These advances allow smaller spacecraft to handle more sophisticated workloads, extend operational relevance, and support multipurpose constellations that require dependable performance with tighter mass and power constraints.

The competitive environment is defined by platform standardization, subsystem integration, launch alignment, and mission support capability. Participants are differentiating through modular spacecraft design, faster manufacturing cycles, payload accommodation expertise, and the ability to serve defense, civil, commercial, and academic requirements within evolving regulatory and orbital sustainability frameworks.

03

Segment Analysis

Nanosatellite and Microsatellite Market Segmentation

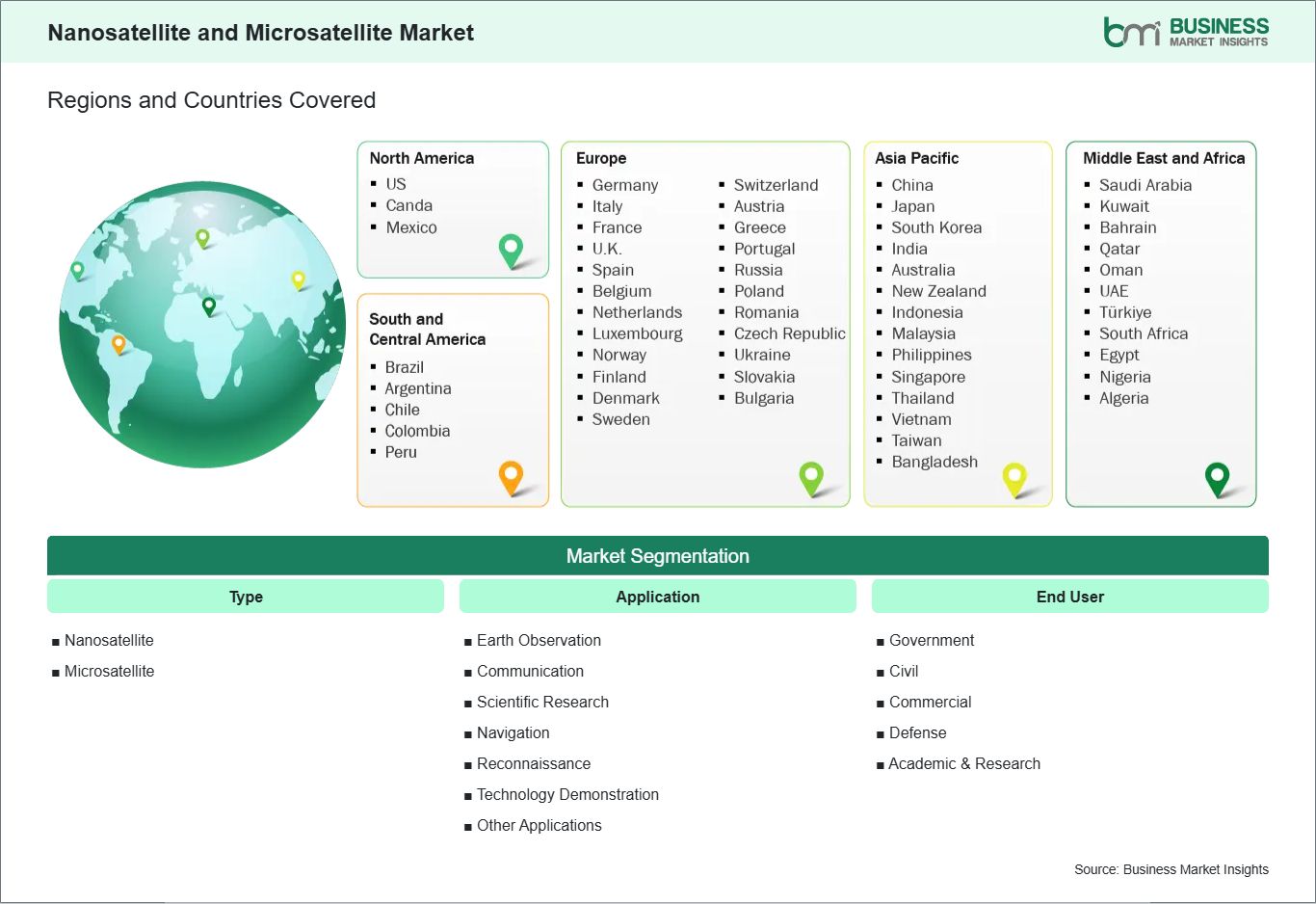

The nanosatellite and microsatellite market is segmented by type, application, and end user across compact satellite mission architectures.

By Type

- Nanosatellite: Fits rapid deployment missions with compact payload and lower platform complexity.

- Microsatellite: Supports larger payload integration with broader operational endurance requirements.

By Application

- Earth Observation: Anchors demand through imaging, environmental monitoring, and disaster assessment missions.

- Communication: Extends connectivity across remote, maritime, industrial, and machine-linked networks.

- Scientific Research: Enables focused experiments with lower mission cost and shorter preparation cycles.

- Navigation: Complements positioning services with targeted augmentation and tracking functions.

- Reconnaissance: Serves surveillance needs requiring persistent coverage and responsive tasking.

- Technology Demonstration: Validates subsystems, payloads, and orbital concepts before wider deployment.

- Other Applications: Includes education, meteorology, signal collection, and niche orbital services.

By End User

- Government: Funds strategic missions spanning security, observation, and public service programs.

- Civil: Uses compact satellites for environmental, meteorological, and institutional mission needs.

- Commercial: Expands constellations for data services, connectivity, and market-facing applications.

- Defense: Prioritizes resilient assets for reconnaissance, communications, and operational awareness.

- Academic Research: Advances experimental missions, training programs, and scientific payload development.

04

Market Forces

Nanosatellite and Microsatellite Market Drivers and Opportunities

Miniaturized Payload Integration and Faster Mission Cycles Accelerating Small Satellite Deployment

Advances in miniaturized sensors, onboard computing, and compact subsystems are reducing the barriers to orbiting mission-capable spacecraft. Operators increasingly need platforms that can be assembled faster, tailored to a focused objective, and launched within shorter planning windows. This requirement is encouraging wider deployment of nanosatellites and microsatellites across observation, communications, and experimental mission profiles.

The effect extends beyond spacecraft manufacturing into launch coordination, data delivery models, and constellation design choices. Smaller satellites are becoming more relevant where mission responsiveness, orbital refresh, and distributed coverage matter more than single-platform scale. This shift strengthens their role across institutions that require lower capital intensity while maintaining operational flexibility and targeted payload performance.

Constellation-Based Services and In-Orbit Technology Validation Creating Expansion Headroom

A significant opportunity is emerging from constellation architectures designed for communications, Earth intelligence, and continuous monitoring services. Innovation in modular buses, software-defined payloads, and shared launch access is widening the range of deployable use cases. These developments support operators seeking to validate new technologies in orbit before scaling them across larger commercial or institutional mission fleets.

Future scope is linked to sectors requiring persistent coverage, rapid revisit capability, and specialized data products without relying on heavier satellite platforms. As service models mature, the market can expand into broader connectivity, monitoring, and defense-linked missions through distributed networks of smaller spacecraft. This trajectory can deepen application diversity while reinforcing the industry's move toward scalable orbital infrastructure.

05

Size and Share Analysis

Nanosatellite and Microsatellite Market Size and Share Analysis

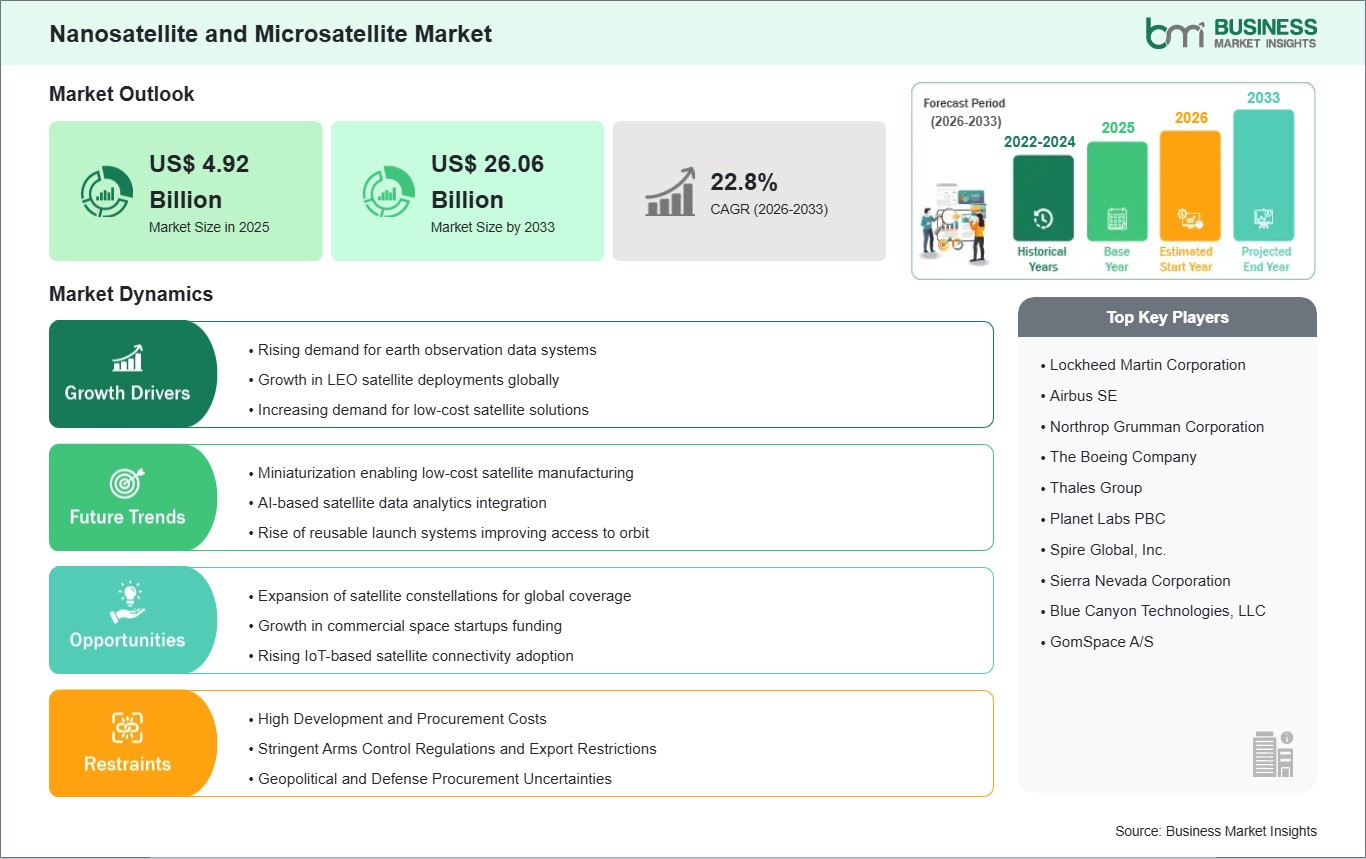

The Nanosatellite and Microsatellite market size is expected to reach US$ 26.06 Billion by 2033 from US$ 4.92 Billion in 2025. The market is estimated to record a CAGR of 22.8% from 2026 to 2033. This trajectory reflects stronger program activity across compact spacecraft platforms, broader constellation planning, and a rising preference for missions that emphasize quicker deployment and focused orbital functionality.

By segment, nanosatellites hold a prominent position because their lower mass profile supports more accessible mission planning and efficient rideshare alignment. Microsatellites remain important where payload accommodation, endurance, or onboard capability requirements are broader. On the end-user side, government and commercial organizations maintain strong relevance as they pursue security, communications, and observation programs through compact spacecraft fleets.

Application leadership is centered on Earth observation, where compact satellites support recurrent imaging, environmental analysis, and rapid event tracking. Communication applications also command substantial attention as operators use smaller spacecraft to extend coverage and specialized network services. Scientific research, navigation, reconnaissance, and technology demonstration continue to reinforce demand through mission-specific deployment needs.

07

Report Coverage

Nanosatellite and Microsatellite Market Report Coverage and Deliverables

The " Nanosatellite and Microsatellite Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

- Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Nanosatellite and Microsatellite Market Geographic Insights

The Nanosatellite and Microsatellite market shows diverse regional adoption patterns influenced by launch access, institutional funding priorities, manufacturing ecosystems, and mission specialization. Across the global landscape, compact spacecraft are gaining relevance because they align with distributed space architectures, phased constellation rollouts, and operational models that favor shorter development timelines and targeted payload integration.

North America maintains a strong position through established launch capacity, defense-linked procurement, and a deep base of private space companies and research institutions. The region benefits from mature satellite design capability and active demand for communication, reconnaissance, and Earth data services. Its market structure supports both recurring constellation deployment and experimental missions that validate new subsystem technologies.

Asia Pacific is advancing through state-backed programs, manufacturing expansion, and rising interest in sovereign observation and communication capacity. The region combines academic innovation with commercial ambition, allowing smaller spacecraft to serve public missions and private service models simultaneously. Countries across this geography are using compact satellites to strengthen technical self-reliance and accelerate participation in the broader space economy.

Europe emphasizes mission quality, sustainability standards, and collaborative space programs that support advanced small satellite deployment. Beyond Europe, emerging markets in the Middle East and Africa and South and Central America are building traction through institutional missions, monitoring needs, and expanding access to regional space infrastructure. These areas are gradually broadening demand for compact spacecraft adapted to civil, academic, and strategic applications.

10

Industry Activity

Recent Developments

The nanosatellite and microsatellite market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

- May 2026: NASA's Small Spacecraft Propulsion and Inspection Capability (SSPICY) mission is the agency's first commercial technology demonstration for in-space satellite servicing and inspection. The mission, led by Starfish Space of Seattle, Washington, advances an innovative approach to enabling commercial inspection of defunct, or inoperable, satellites in low Earth orbit, a precursor to capturing and repairing or removing the satellites. The spacecraft is expected to launch in late 2026 and will begin performing inspections in 2027.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

US Department of DefenseEuropean Space Agency (ESA)China Aerospace Science and Technology Corporation (CASC)Indian Space Research Organisation (ISRO)Israeli Nano Satellite Association (INSA)Company filings and press releasesAcademic studies on small satellite systemsPeer-reviewed aerospace and remote sensing journalsIndustry reports on satellite platforms and launch activityConference proceedings and technical papers