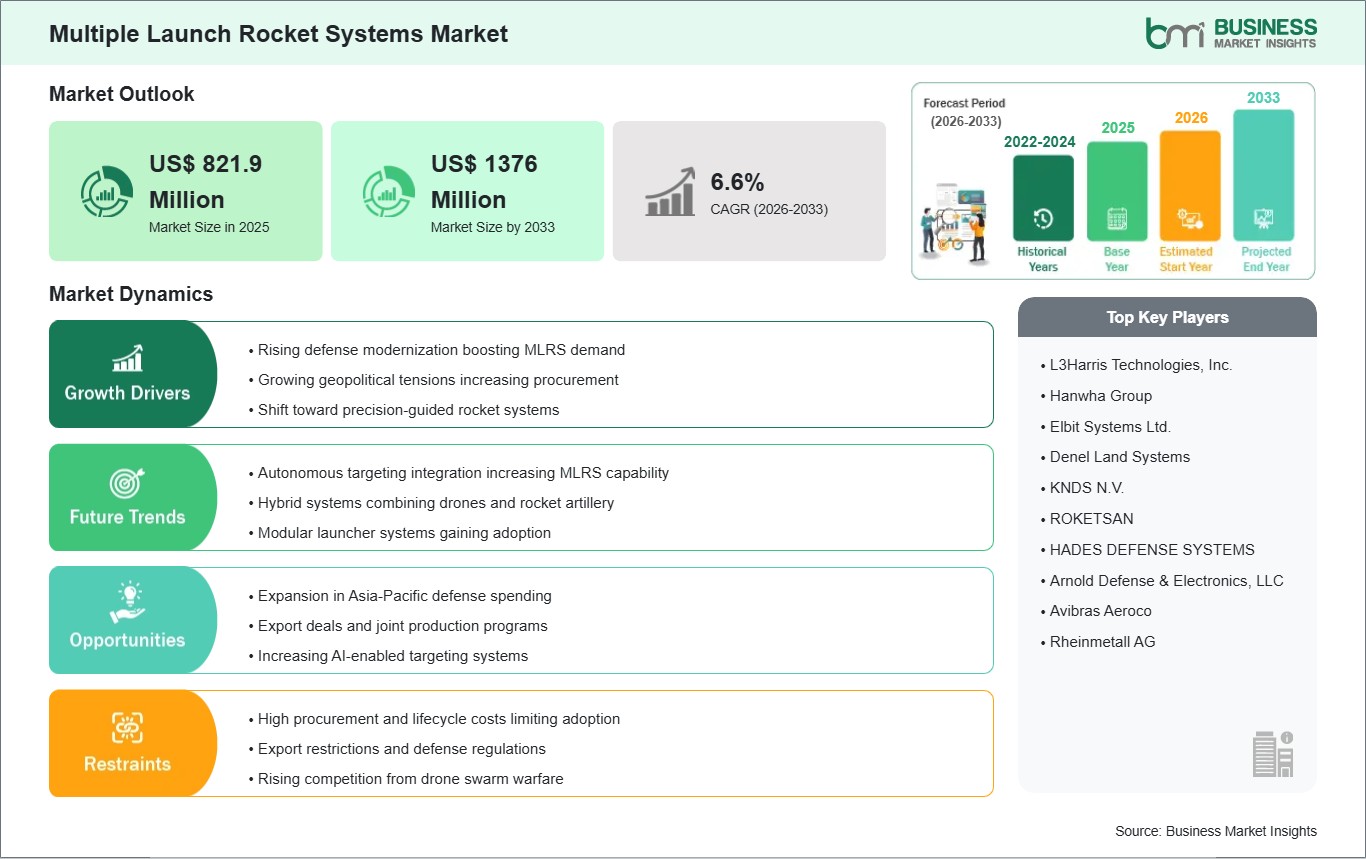

The Multi Launch Rocket Systems market size is expected to reach US$ 1.37 Billion by 2033 from US$ 0.82 Billion in 2025. The market is estimated to record a CAGR of 6.6% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Multiple launch rocket systems are artillery platforms engineered to fire salvos of unguided or guided rockets from a single launcher assembly. They combine mobility, concentrated firepower, and rapid shoot-and-scoot capability, allowing forces to engage area targets, suppression missions, and deep-strike objectives across changing battlefield conditions.

Procurement priorities are shifting toward systems that deliver longer reach, faster deployment, and better interoperability with digital fire-control networks. Armed forces are expanding deployment of launchers that can support precision munitions, dispersed operations, and responsive fires under contested environments where mobility and survivability carry equal importance.

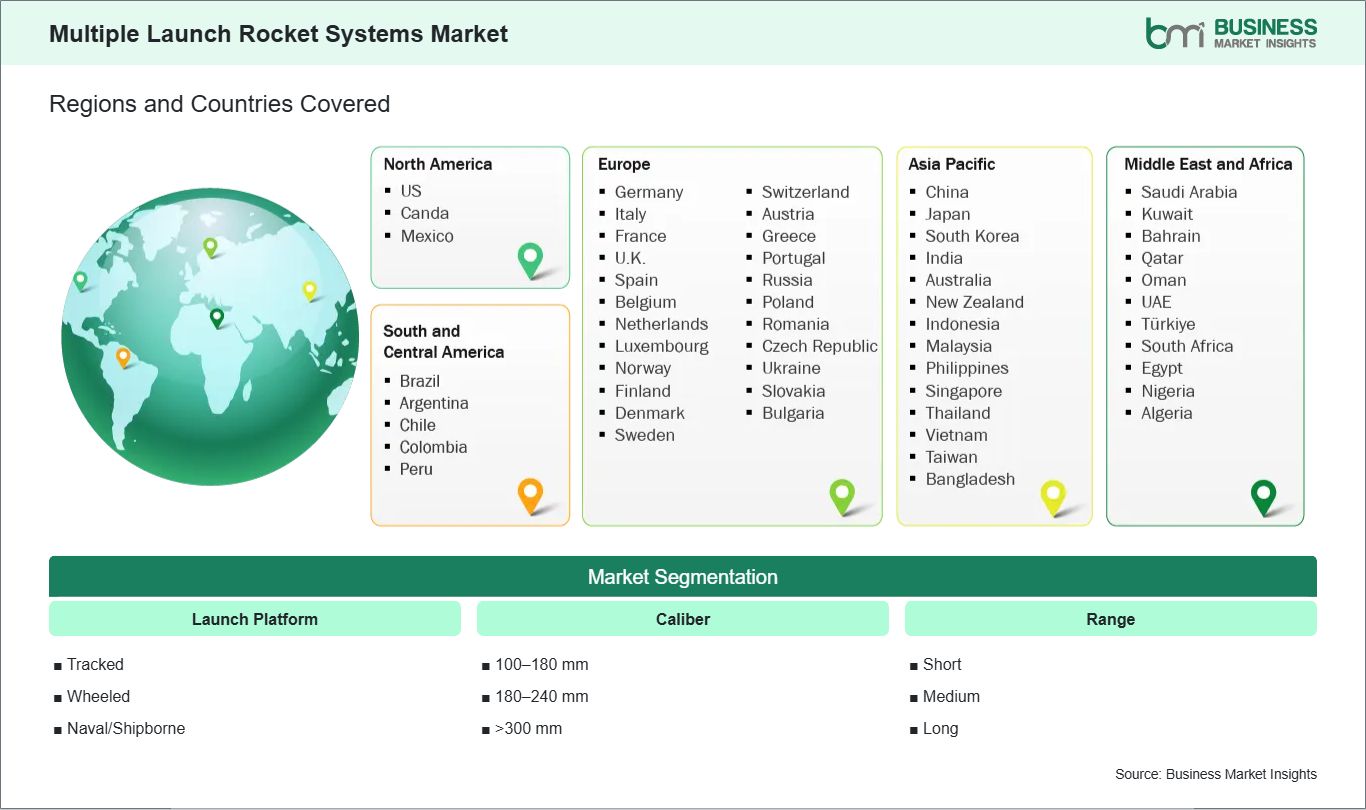

Segmentation reveals distinct operational preferences across launch platform, caliber, and range profiles. Tracked systems align with heavy maneuver formations, wheeled variants suit expeditionary mobility, and naval or shipborne configurations extend rocket artillery utility into littoral missions. Caliber and range categories further differentiate payload flexibility, saturation effect, and mission depth.

Technology progression is centered on modular launch pods, automated targeting interfaces, precision-guided rockets, and compatibility with extended-range munitions. These developments are refining firing accuracy, reload efficiency, and command connectivity, while also enabling operators to transition from legacy saturation roles toward more discriminating and networked strike functions.

The competitive environment reflects emphasis on launcher adaptability, munitions integration, industrial readiness, and lifecycle support. Suppliers are positioning through configurable platform families, digital fire systems, and alignment with national modernization agendas, while procurement decisions increasingly consider domestic production, interoperability, and upgrade pathways.

Multiple Launch Rocket Systems Market - Strategic Insights:

Get more information on this report

Multiple Launch Rocket Systems Market Segmentation Analysis:

The multi launch rocket systems market is segmented by launch platform, caliber, and range across evolving long-range fire support requirements.

By Launch Platform

Tracked: Supports armored formations with protected mobility and sustained battlefield presence.

Wheeled: Enables faster road movement and flexible deployment across dispersed operational theatres.

Naval/Shipborne: Extends rocket fire support into coastal and maritime engagement scenarios.

By Caliber

100-180 mm: Favored for tactical salvos requiring lighter launch loads and rapid firing.

180-240 mm: Balances destructive effect with adaptable mission planning requirements.

>300 mm mm: Serves deep-strike roles demanding heavier payloads and longer stand-off reach.

By Range

Short: Selected for close support, suppression, and localized battlefield shaping missions.

Long: Addresses strategic strike needs against rear-area and high-value targets.

Multiple Launch Rocket Systems Market Drivers and Opportunities:

Rising defense modernization boosting MLRS demand

Operational planning now places greater emphasis on deep fires, rapid repositioning, and synchronized targeting across land forces. That requirement is prompting defense ministries to procure launch systems capable of delivering concentrated rocket effects with shorter response cycles, stronger mobility profiles, and better compatibility with modern command networks supporting high-tempo operations.

The effect reaches beyond launcher acquisition into training, doctrine, munitions planning, and sustainment structures. As armed forces refine battlefield concepts around dispersion and precision engagement, these systems gain greater relevance. Their importance rises in programs seeking responsive strike options that can operate across conventional deterrence, counter-battery fire, and border defense requirements.

Precision-Guided Rockets and Modular Launch Architectures Expanding Upgrade Potential

An important opportunity is emerging from the shift toward modular launchers paired with guided and extended-range munitions. This transition supports use cases where operators need flexible strike packages, scalable launcher configurations, and digital targeting workflows that can adapt to changing mission conditions without redesigning the full fire support architecture.

Future scope lies in upgrade programs that combine new fire-control suites, interoperable munitions pods, and platform-specific mobility enhancements. As procurement strategies favor adaptable systems over fixed configurations, suppliers can widen participation across fresh acquisitions and modernization cycles. That progression can strengthen market depth while raising the strategic value of long-range fires portfolios.

Multiple Launch Rocket Systems Market Size and Share Analysis:

The Multi Launch Rocket Systems market size is expected to reach US$ 1.37 Billion by 2033 from US$ 0.82 Billion in 2025. The market is estimated to record a CAGR of 6.6% from 2026 to 2033. This growth profile indicates sustained procurement interest in mobile rocket artillery, supported by modernization programs, platform upgrades, and the need for launch systems that combine reach, survivability, and networked fire coordination.

By segment, wheeled platforms retain strong visibility because they align with fast deployment doctrines and simplified transport across broad operating areas. Mid-caliber systems also hold an important position by balancing launcher compatibility, payload flexibility, and mission adaptability. Medium-range categories remain central where forces seek operational depth without shifting entirely into strategic missile systems.

Application dominance is concentrated in land-based force modernization, where rocket artillery supports suppression, counter-battery missions, and deep-fire planning. Tactical formations continue to account for broad system relevance, while coastal and expeditionary roles are extending usage patterns. Naval or shipborne concepts add further interest where standoff fires are being integrated into maritime deterrence frameworks.

Multiple Launch Rocket Systems Market Report Highlights:

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

L3Harris Technologies, Inc.

Hanwha Group

Elbit Systems Ltd.

Denel Land Systems

KNDS N.V.

ROKETSAN

HADES DEFENSE SYSTEMS

Arnold Defense & Electronics, LLC

Avibras Aeroco

Rheinmetall AG

Get more information on this report

Multiple Launch Rocket Systems Market Report Coverage and Deliverables:

The " Multi Launch Rocket Systems Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Multiple Launch Rocket Systems Market Geographic Insights:

The Multi Launch Rocket Systems market shows diverse regional adoption patterns influenced by defense doctrine, procurement cycles, platform mobility needs, and munitions integration priorities. Across the wider global landscape, governments are reassessing artillery depth and responsiveness, which is reinforcing interest in launcher families that can support both conventional area fires and more selective long-range strike concepts.

North America maintains a prominent position through established industrial capability, structured modernization pathways, and strong emphasis on interoperable precision fires. Procurement activity in the region favors launch systems with digital targeting support, flexible munitions compatibility, and mobility suited to rapid deployment, reinforcing the role of both legacy platform upgrades and next-generation launcher integration.

Asia Pacific reflects expanding strategic interest as regional security planning increasingly values stand-off firepower and transportable artillery assets. Countries across the region are aligning acquisitions with mobility, terrain adaptability, and deterrence needs, encouraging demand for wheeled and tracked systems that can operate across varied geographies while integrating with broader battlefield surveillance and command structures.

Europe continues to prioritize artillery renewal through alliance coordination, ammunition compatibility, and readiness-oriented force restructuring. Beyond Europe, emerging markets in the Middle East and Africa and South and Central America are evaluating rocket artillery through border security, deterrence, and coastal defense requirements. This mix is widening the sector's regional opportunity set across both replacement programs and first-time capability development.

Get more information on this report

Multiple Launch Rocket Systems Market Research Report Guidance:

The Multi Launch Rocket Systems report includes qualitative and quantitative data in the market across launch platform, caliber, range, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover market segments by launch platform, caliber, range, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Multiple Launch Rocket Systems Market News and Key Development:

The multi launch rocket systems market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

May 2026: Hanwha Aerospace announced that it will supply three additional Chunmoo multiple rocket launcher systems to the Estonian Defence Forces. The supply follows a government-to-government (G2G) contract signed on May 11 between the Korea Trade-Investment Promotion Agency (KOTRA) and the Estonian Centre for Defence Investments (ECDI).

December 2025: L3Harris Technologies has been awarded a follow-on production contract valued up to $200 million to manufacture Guided Multiple Launch Rocket System (GMLRS) Insensitive Munition (IM) propulsion units.

Key Sources Referred:

US Department of DefenseDefense Advanced Research Projects Agency (DARPA)Defence Research and Development Organisation (DRDO)China Academy of Launch Vehicle Technology (CALT)Ministry of Defence of the Russian FederationNATO Support and Procurement Agency (NSPA)Company filingsTechnical and defense journalsAcademic studiesRegulatory and strategic policy documents

The List of Companies - Multiple Launch Rocket Systems Market

L3Harris Technologies, Inc.

Hanwha Group

Elbit Systems Ltd.

Denel Land Systems

KNDS N.V.

ROKETSAN

HADES DEFENSE SYSTEMS

Arnold Defense & Electronics, LLC

Avibras Aeroco

Rheinmetall AG

Frequently Asked Questions

How big is the Multiple Launch Rocket Systems Market?

The Multiple Launch Rocket Systems Market is valued at US$ 821.9 Million in 2025, it is projected to reach US$ 1376 Million by 2033.

What is the CAGR for Multiple Launch Rocket Systems Market by (2026 - 2033)?

As per our report Multiple Launch Rocket Systems Market, the market size is valued at US$ 821.9 Million in 2025, projecting it to reach US$ 1376 Million by 2033. This translates to a CAGR of approximately 6.6% during the forecast period.

What segments are covered in this report?

The Multiple Launch Rocket Systems Market report typically cover these key segments-

What is the historic period, base year, and forecast period taken for Multiple Launch Rocket Systems Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Multiple Launch Rocket Systems Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Multiple Launch Rocket Systems Market?

The Multiple Launch Rocket Systems Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

L3Harris Technologies, Inc.

Hanwha Group

Elbit Systems Ltd.

Denel Land Systems

KNDS N.V.

ROKETSAN

HADES DEFENSE SYSTEMS

Arnold Defense & Electronics, LLC

Avibras Aeroco

Rheinmetall AG

Who should buy this report?

The Multiple Launch Rocket Systems Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Multiple Launch Rocket Systems Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Multiple Launch Rocket Systems Market

Get Free Sample For Multiple Launch Rocket Systems Market