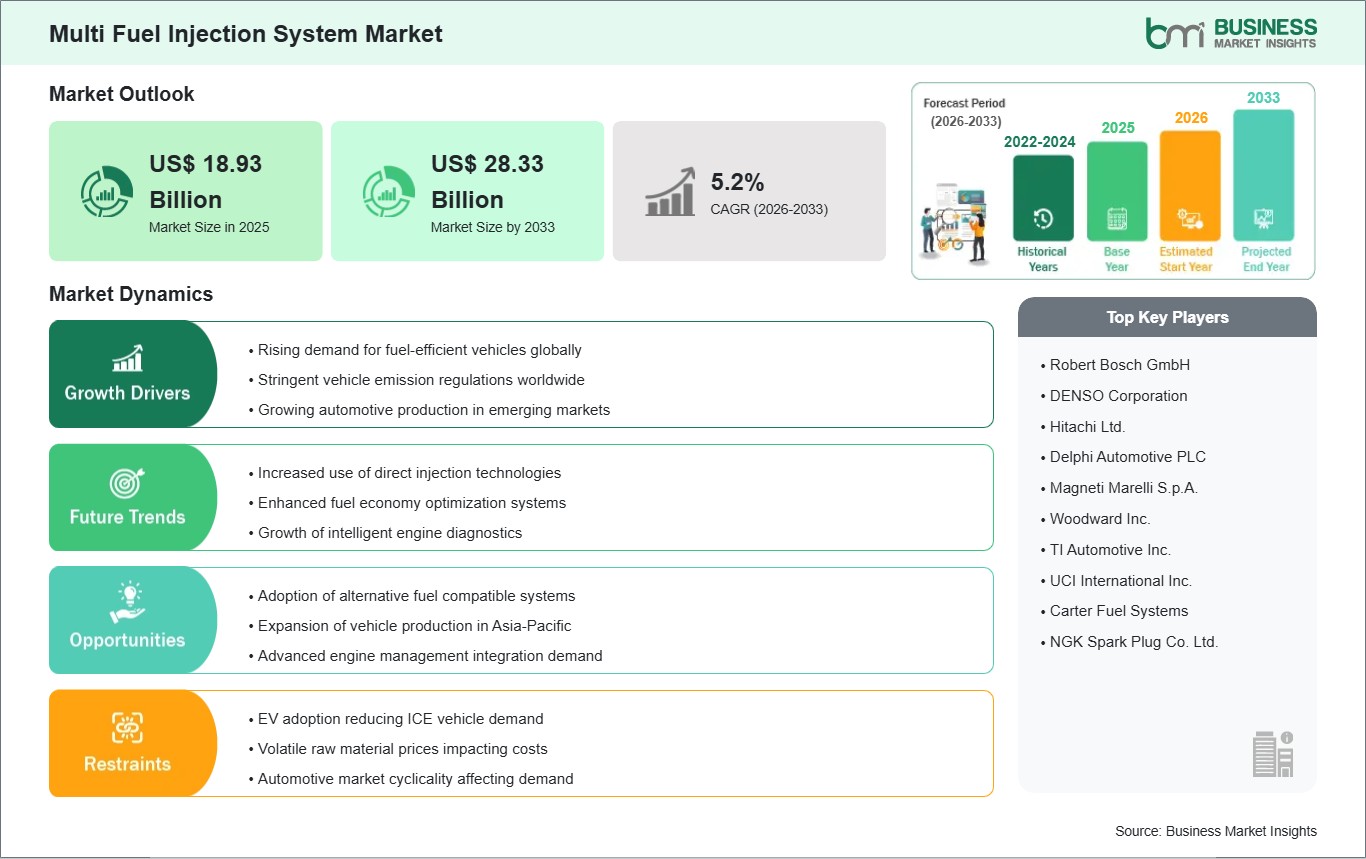

The Multi Fuel Injection System market size is expected to reach US$ 28.33 Billion by 2033 from US$ 18.93 Billion in 2025. The market is estimated to record a CAGR of 5.2% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Multi fuel injection systems are engine fuel delivery architectures designed to meter and inject different fuel types with precision under varied combustion requirements. They support controlled spray formation, air-fuel mixing, and combustion stability across powertrains that use gasoline, diesel, or hybrid operating strategies.

Automotive manufacturers are refining injection strategies to meet tighter efficiency and emissions objectives without compromising drivability or engine response. This requirement is expanding deployment of injection platforms that deliver precise fuel dosing, flexible calibration, and compatibility with evolving combustion control logic across passenger and commercial vehicles.

Segmentation highlights clear variation across vehicle class, fuel preference, and injection configuration. Passenger vehicles account for broad system integration, while commercial applications emphasize durability and fuel management consistency. Gasoline and diesel architectures retain distinct engineering pathways, and direct, port, throttle, and sequential systems serve different combustion and packaging needs.

Technology development is moving toward higher-pressure operation, finer atomization, software-led injection control, and better responsiveness under transient engine loads. These improvements strengthen combustion efficiency, support cleaner exhaust outcomes, and help manufacturers adapt internal combustion platforms to hybridized vehicle architectures with more complex duty cycles.

The competitive environment is defined by engineering capability, calibration expertise, manufacturing scale, and the ability to support multiple fuel pathways within one product roadmap. Suppliers are positioning through injector performance, pressure handling, control integration, and platform flexibility aligned with regional emissions and vehicle development requirements.

Multi Fuel Injection System Market - Strategic Insights:

Get more information on this report

Multi Fuel Injection System Market Segmentation Analysis:

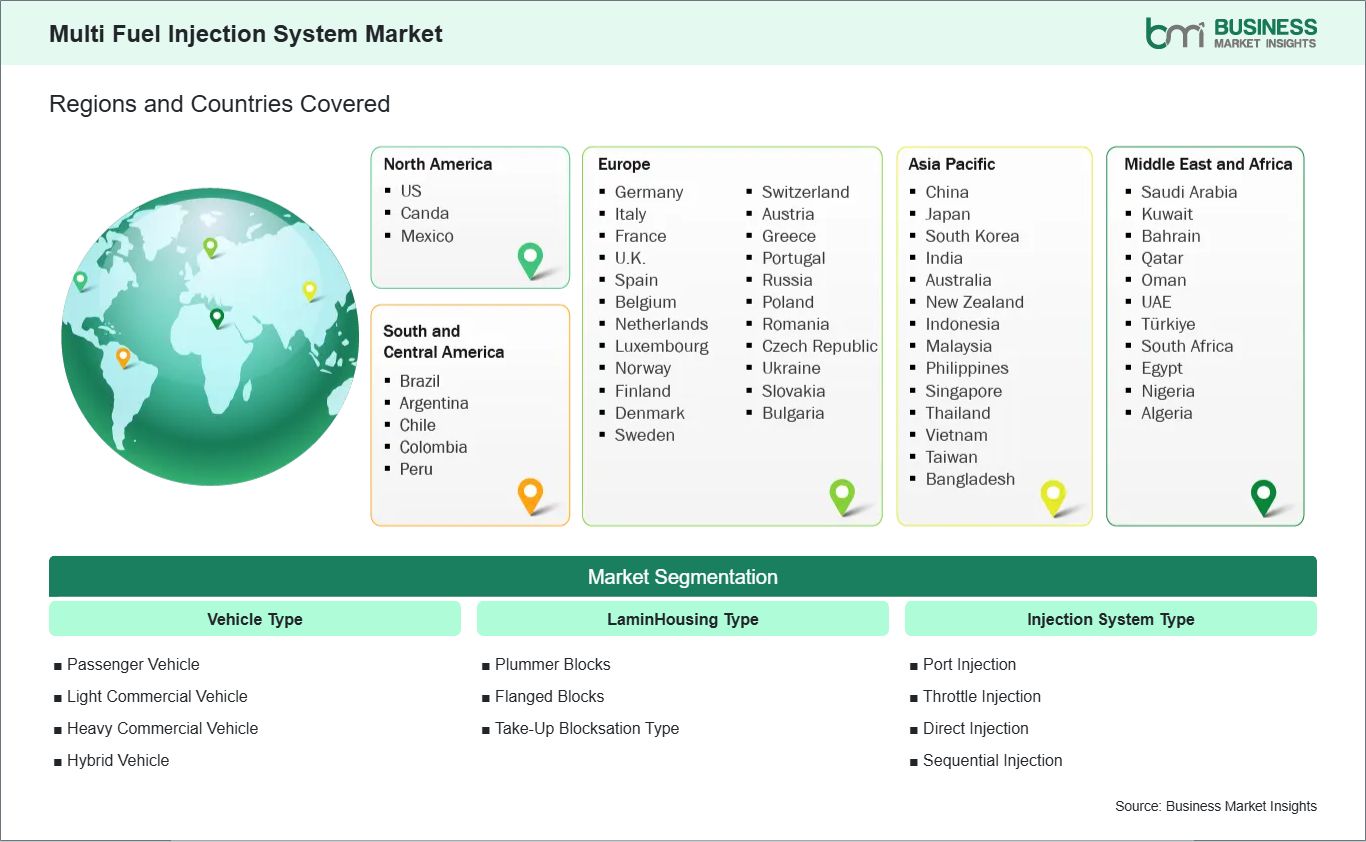

The multi fuel injection system market is segmented by vehicle type, fuel type, and injection system type across automotive fuel delivery requirements.

By Vehicle Type

Passenger Vehicle: Leads integration through high production volumes and emission-focused engine optimization.

Light Commercial Vehicle: Favors dependable injection control for mixed-duty urban and regional transport cycles.

Heavy Commercial Vehicle: Prioritizes robust fuel metering under sustained load and long-haul operation.

Gasoline: Supports fine atomization and responsive combustion control in modern spark-ignition engines.

Diesel: Sustains precise high-pressure delivery for torque-oriented compression-ignition performance.

By Injection System Type

Port Injection: Maintains mixture uniformity through intake-port fuel delivery.

Throttle Injection: Serves simpler engine layouts with centralized fuel introduction.

Direct Injection: Enhances combustion precision through in-cylinder fuel delivery control.

Sequential Injection: Improves timing accuracy by coordinating injection with engine firing order.

Multi Fuel Injection System Market Drivers and Opportunities:

Emission Compliance and Combustion Efficiency Requirements Advancing Precision Injection Systems

Stricter powertrain calibration targets are pushing manufacturers toward injection systems that deliver tighter control over fuel quantity, timing, and spray behavior. That need is accelerating use of advanced injection hardware across gasoline, diesel, and hybrid platforms, where combustion quality directly influences efficiency, exhaust treatment performance, and engine refinement in increasingly regulated vehicle programs.

The impact extends across engine architecture, software calibration, and component sourcing decisions throughout the automotive value chain. As vehicle programs demand more accurate combustion management under mixed operating conditions, injection technologies gain strategic relevance. Their role becomes especially important where manufacturers seek durable compliance pathways while maintaining performance expectations across passenger, light commercial, and heavy commercial applications.

Alternative Fuel Compatibility and Hybrid Powertrain Integration Opening New Product Pathways

A notable opportunity is emerging from injection platforms configured for broader fuel compatibility and hybrid operating logic. Suppliers are developing systems that support finer control under start-stop cycles, variable load transitions, and fuel-specific combustion behavior, enabling use cases that extend beyond traditional gasoline and diesel engine configurations toward more adaptable multi-fuel vehicle architectures.

Future scope is linked to vehicles that require flexible fuel delivery performance without sacrificing calibration precision or packaging efficiency. As automakers broaden combustion strategies within hybrid and alternative-fuel programs, suppliers can expand through modular injectors, pressure systems, and control software. This direction can widen application range while reinforcing the industry's shift toward versatile and efficiency-oriented fuel system design.

Multi Fuel Injection System Market Size and Share Analysis:

The Multi Fuel Injection System market size is expected to reach US$ 28.33 Billion by 2033 from US$ 18.93 Billion in 2025. The market is estimated to record a CAGR of 5.2% from 2026 to 2033. This expansion reflects continued engineering investment in cleaner combustion, calibrated fuel delivery, and adaptable injection architectures suited to evolving vehicle powertrain requirements.

By segment, passenger vehicles hold a central position because they represent the broadest base for injection system integration across global automotive production. Gasoline systems maintain wide relevance in spark-ignition programs, while diesel continues to anchor demand in torque-focused vehicle categories. Direct injection retains strong visibility as manufacturers seek sharper combustion control and improved engine responsiveness.

Application leadership is concentrated in mainstream road vehicles where engine efficiency, drivability, and emissions management remain decisive product considerations. Passenger transport applications account for broad deployment, while freight-oriented vehicle classes sustain demand for durable fuel metering under sustained operating loads. Hybrid vehicle programs also reinforce market relevance by requiring precise injection coordination within blended propulsion strategies.

Multi Fuel Injection System Market Report Highlights:

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Robert Bosch GmbH

DENSO Corporation

Hitachi Ltd.

Delphi Automotive PLC

Magneti Marelli S.p.A.

Woodward Inc.

TI Automotive Inc.

UCI International Inc.

Carter Fuel Systems

NGK Spark Plug Co. Ltd.

Get more information on this report

Multi Fuel Injection System Market Report Coverage and Deliverables:

The " Multi Fuel Injection System Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Multi Fuel Injection System Market Geographic Insights:

The Multi Fuel Injection System market shows diverse regional adoption patterns influenced by emissions policy direction, vehicle production structures, fuel preferences, and supplier integration depth. Across the global landscape, manufacturers are balancing efficiency targets with combustion system flexibility, creating demand for injection technologies that can support multiple fuel strategies while remaining compatible with changing engine architectures.

North America demonstrates steady momentum through demand for advanced gasoline injection systems, hybrid-compatible engine management, and durable solutions for light and heavy vehicle categories. Product development in the region is shaped by the need for performance consistency under varied operating conditions, with manufacturers emphasizing precise calibration, emissions control alignment, and integration across broad model portfolios.

Asia Pacific remains an important manufacturing center for automotive fuel system deployment due to its wide vehicle assembly base and range of powertrain configurations. The region supports both conventional and evolving multi-fuel pathways, encouraging suppliers to offer scalable injection platforms that serve high-volume passenger vehicles, commercial fleets, and hybrid models within diverse regulatory and operational environments.

Europe reflects strong engineering focus on combustion precision, reduced particulate output, and system efficiency within tightly controlled vehicle programs. Beyond Europe, emerging markets in the Middle East and Africa and South and Central America are building relevance as vehicle parc diversification and industrial mobility requirements create room for adaptable injection systems that can address fuel variability and durability expectations.

Get more information on this report

Multi Fuel Injection System Market Research Report Guidance:

The Multi Fuel Injection System report includes qualitative and quantitative data in the market across product, procedures, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover market segments by product, procedures, application, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Multi Fuel Injection System Market News and Key Development:

The multi fuel injection system market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

May 2026: Standard Motor Products, Inc. (SMP) is pleased to share that its Standard Gasoline Fuel Injection program continues to expand. The comprehensive Standard Gas Fuel Injection program includes over 1,100 all-new, not remanufactured, Gasoline Direct Injection (GDI), Multi-Port Fuel Injection (MFI), and Throttle Body Injection (TBI) Injectors, along with GDI High-Pressure Fuel Pumps, Fuel Feed Lines, Fuel Pressure Dampers, Fuel Pressure Sensors, Fuel Pressure Regulators, Service Kits and more. When OE fails, professionals trust Standard® to deliver Fuel Injectors and related components that perform and last.

February 2025: Toyota Motor Corporation announces that it has developed a new fuel cell (FC) system, its third-generation fuel cell system (3rd Gen FC System), as part of its continued efforts toward the realization of a hydrogen society. The all-new 3rd Gen FC System is designed to meet the particular needs of the commercial sector with the same durability as conventional diesel-powered engines. In addition to passenger vehicles, the 3rd Gen FC System will be expanded for use in heavy-duty commercial vehicles and is planned for introduction in markets mainly in Japan, Europe, North America, and China after 2026 at the earliest.

Key Sources Referred:

United States Environmental Protection Agency (EPA)National Highway Traffic Safety Administration (NHTSA)European Commission Directorate-General for Mobility and TransportMinistry of Road Transport and Highways (MoRTH)United Nations Economic Commission for Europe (UNECE)Company filingsAcademic studiesTechnical journalsRegulatory and standards documentation

The List of Companies - Multi Fuel Injection System Market

Robert Bosch GmbH

DENSO Corporation

Hitachi Ltd.

Delphi Automotive PLC

Magneti Marelli S.p.A.

Woodward Inc.

TI Automotive Inc.

UCI International Inc.

Carter Fuel Systems

NGK Spark Plug Co. Ltd.

Frequently Asked Questions

How big is the Multi Fuel Injection System Market?

The Multi Fuel Injection System Market is valued at US$ 18.93 Billion in 2025, it is projected to reach US$ 28.33 Billion by 2033.

What is the CAGR for Multi Fuel Injection System Market by (2026 - 2033)?

As per our report Multi Fuel Injection System Market, the market size is valued at US$ 18.93 Billion in 2025, projecting it to reach US$ 28.33 Billion by 2033. This translates to a CAGR of approximately 5.2% during the forecast period.

What segments are covered in this report?

The Multi Fuel Injection System Market report typically cover these key segments-

Vehicle Type (Passenger Vehicle, Light Commercial Vehicle, Heavy Commercial Vehicle, Hybrid Vehicle)

LaminHousing Type (Plummer Blocks, Flanged Blocks, Take-Up Blocks)ation Type (Stator, Rotor)

Injection System Type (Port Injection, Throttle Injection, Direct Injection, Sequential Injection)

What is the historic period, base year, and forecast period taken for Multi Fuel Injection System Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Multi Fuel Injection System Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Multi Fuel Injection System Market?

The Multi Fuel Injection System Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Robert Bosch GmbH

DENSO Corporation

Hitachi Ltd.

Delphi Automotive PLC

Magneti Marelli S.p.A.

Woodward Inc.

TI Automotive Inc.

UCI International Inc.

Carter Fuel Systems

NGK Spark Plug Co. Ltd.

Who should buy this report?

The Multi Fuel Injection System Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Multi Fuel Injection System Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Multi Fuel Injection System Market

Get Free Sample For Multi Fuel Injection System Market