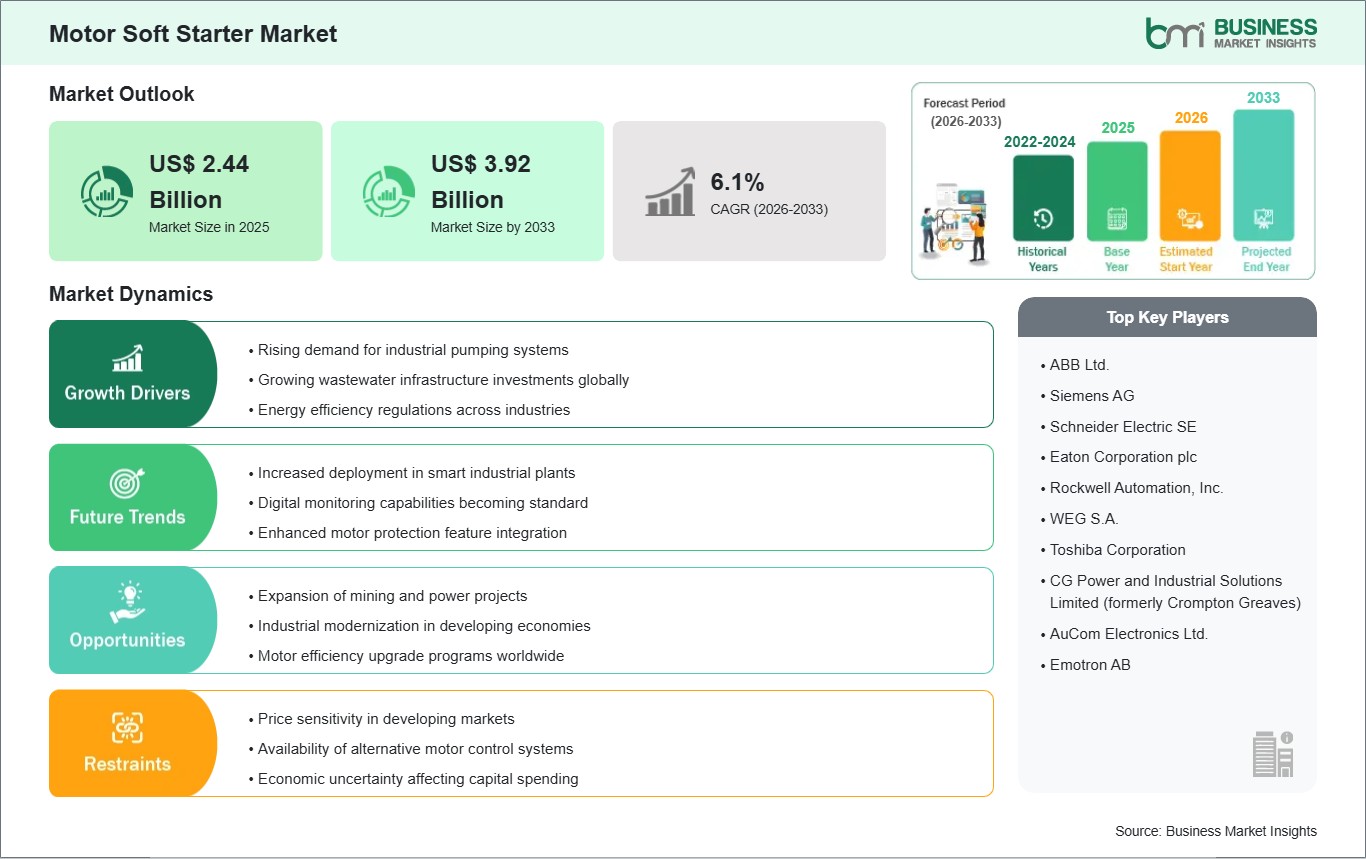

The Motor Soft Starter market size is expected to reach US$ 3.92 Billion by 2033 from US$ 2.44 Billion in 2025. The market is estimated to record a CAGR of 6.1% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Motor soft starters are solid-state motor control devices that reduce inrush current and mechanical stress during startup. They regulate voltage delivery to support smoother acceleration, protect driven equipment, and improve operational stability in electrically intensive systems.

Industrial operators are expanding deployment of these systems to limit torque shock, reduce maintenance exposure, and improve motor longevity. Demand is reinforced by automation upgrades, tighter energy management practices, and the need for reliable starting performance in process-critical environments.

Segmentation highlights clear performance differences across voltage classes, rated power ranges, and application categories. Low-voltage units serve a broad installed base, while medium-voltage configurations address heavier industrial loads. Pumps, fans, and compressors each require distinct control behavior based on startup profile and duty cycle.

Technology development is centered on digital diagnostics, adaptive ramp control, bypass integration, and compatibility with connected control architectures. These refinements improve operational visibility and enable more precise coordination between motor starting functions and wider plant control systems.

Competition is shaped by product reliability, application engineering capability, and breadth of voltage and power coverage. Suppliers strengthen market position through configurable protection features, integration support, and targeted offerings for facilities where startup control directly affects uptime and equipment health.

Motor Soft Starter Market - Strategic Insights:

Get more information on this report

Motor Soft Starter Market Segmentation Analysis:

The motor soft starter market is segmented by voltage, rated power, and application across industrial motor control requirements.

By Voltage

Low Voltage: Anchors broad industrial use through compact design and control flexibility.

Medium Voltage: Fits heavy-duty installations requiring controlled startup under higher electrical loads.

By Rated Power

Up to 750 W: Serves light-duty equipment where soft starting improves component life.

751 W-75 kW: Covers mainstream industrial motors across process and utility systems.

Pumps: Limits hydraulic shock and supports smoother pressure build during startup.

Fans: Enhances airflow system reliability by moderating initial torque and current draw.

Compressors: Reduces drivetrain strain in applications with repeated or demanding starts.

Motor Soft Starter Market Drivers and Opportunities:

Digital Monitoring and Smart Control Integration Opening Higher-Value Use Cases

Motor-driven systems in pumps, fans, and compressors often face startup conditions that strain shafts, couplings, belts, and electrical components. That operating reality is increasing interest in soft starters that can moderate current surge and mechanical shock. Facilities aiming to reduce unplanned maintenance are turning toward controlled starting solutions that align equipment protection with everyday operating needs.

The impact extends beyond startup performance into asset life, service planning, and process continuity. In water systems, HVAC infrastructure, and industrial production lines, smoother motor acceleration reduces wear exposure and supports steadier operation. This makes motor soft starters relevant where operators seek practical motor control improvements without redesigning the broader drive architecture.

Digital Monitoring and Smart Control Integration Opening Higher-Value Use Cases

A clear opportunity is emerging as motor soft starters incorporate diagnostics, communication features, and adaptive control functions. These enhancements allow operators to connect starting behavior with maintenance visibility and process supervision. Use cases are expanding in facilities that want more control granularity for pumping stations, ventilation systems, and compressor packages without shifting every installation toward more complex alternatives.

Future scope lies in broader integration with connected industrial systems, especially where remote diagnostics and operating transparency support faster intervention. Expansion potential is visible across retrofit programs and new installations that prioritize digital oversight. This direction can improve service responsiveness, strengthen control precision, and widen the role of soft starters within modern motor management strategies.

Motor Soft Starter Market Size and Share Analysis:

The Motor Soft Starter market size is expected to reach US$ 3.92 Billion by 2033 from US$ 2.44 Billion in 2025. The market is estimated to record a CAGR of 6.1% from 2026 to 2033. This progression indicates sustained use of controlled motor starting solutions in operations where equipment reliability, reduced electrical stress, and predictable startup behavior remain commercially important.

By voltage, low-voltage products hold the leading position because they fit a wide installed base across industrial and utility applications. In rated power terms, the 751 W-75 kW range commands broad attention due to its relevance across mainstream motor systems. Medium-voltage and higher-power categories remain important in facilities with larger process loads and more demanding starting conditions.

By application, pumps represent the dominant area because startup control directly affects pressure stability, pipe stress, and maintenance frequency. Fans also contribute significantly where steady acceleration supports airflow systems and motor protection. Compressors remain a key application segment, particularly in installations where repeated starts and torque sensitivity require controlled electrical and mechanical loading.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

ABB Ltd.

Siemens AG

Schneider Electric SE

Eaton Corporation plc

Rockwell Automation, Inc.

WEG S.A.

Toshiba Corporation

CG Power and Industrial Solutions Limited (formerly Crompton Greaves)

AuCom Electronics Ltd.

Emotron AB

Get more information on this report

Motor Soft Starter Market Report Coverage and Deliverables:

The " Motor Soft Starter Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Motor Soft Starter Market Geographic Insights:

The Motor Soft Starter market shows diverse regional adoption patterns influenced by industrial motor intensity, infrastructure modernization, automation priorities, and electrical protection practices. At the global level, demand is linked to the need for smoother motor startup across utility networks, manufacturing sites, and process industries. Deployment decisions often reflect the balance between equipment protection, operational continuity, and the degree of control sophistication required in each end-use setting.

North America benefits from mature industrial infrastructure and steady investment in motor control upgrades across water handling, building systems, and industrial automation. Buyers in the region often focus on maintenance reduction, equipment reliability, and integration with established control platforms. Demand remains supported by applications where pumps, fans, and compressors operate under frequent or demanding startup conditions that require dependable electrical moderation.

Asia Pacific presents the broadest deployment environment because of its manufacturing depth, extensive installed motor base, and ongoing industrial expansion. The region sees consistent use of soft starters in factory utilities, commercial building systems, and process industries where motor protection supports uptime. Retrofit demand is also meaningful, as operators seek control improvements that fit existing assets without introducing excessive system complexity.

Europe remains shaped by efficiency-conscious engineering practices and a strong preference for controlled, durable motor operation in industrial facilities and building services. Beyond Europe, emerging markets across the Middle East, Africa, and South and Central America are becoming more relevant as infrastructure expansion and utility development increase the use of motor-driven systems. These regions create additional scope for soft starter deployment where reliable startup performance supports asset protection and service continuity.

Get more information on this report

Motor Soft Starter Market Research Report Guidance:

The Motor Soft Starter market report includes qualitative and quantitative data in the market across Material, Lamination, End-Use, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover market segments by Material, Lamination, End-Use, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Motor Soft Starter Market News and Key Development:

The motor soft starter market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

March 2026: Rockwell Automation announced the launch of the M100 Electronic Motor Starter, extending its motor control portfolio with refined starting capability, functional safety options, and space-efficient panel integration for industrial applications.

March 2025: TECO has launched two new soft starter products to support a range of industrial applications. Designed for motors from 18A to 200A operating at supply voltages up to 575VAC, the TECO RSXi soft starter range uses a compact closed-loop control architecture with two-phase control and internal bypass, allowing motors to run with minimal heat dissipation once they reach full speed.

Key Sources Referred:

International Electrotechnical Commission (IEC)International Organization for Standardization (ISO)Canadian Centre for Occupational Health and Safety (CCOHS)European Chemicals Agency (ECHA)Company filingsAcademic studiesTrade association publicationsTechnical white papers

The List of Companies - Motor Soft Starter Market

ABB Ltd.

Siemens AG

Schneider Electric SE

Eaton Corporation plc

Rockwell Automation, Inc.

WEG S.A.

Toshiba Corporation

CG Power and Industrial Solutions Limited (formerly Crompton Greaves)

AuCom Electronics Ltd.

Emotron AB

Frequently Asked Questions

How big is the Motor Soft Starter Market?

The Motor Soft Starter Market is valued at US$ 2.44 Billion in 2025, it is projected to reach US$ 3.92 Billion by 2033.

What is the CAGR for Motor Soft Starter Market by (2026 - 2033)?

As per our report Motor Soft Starter Market, the market size is valued at US$ 2.44 Billion in 2025, projecting it to reach US$ 3.92 Billion by 2033. This translates to a CAGR of approximately 6.1% during the forecast period.

What segments are covered in this report?

The Motor Soft Starter Market report typically cover these key segments-

Voltage (Low Voltage, Medium Voltage)

Rated Power (Up to 750 W, 751 W–75 kW, Above 75 kW)

Application (Pumps, Fans, Compressors)

What is the historic period, base year, and forecast period taken for Motor Soft Starter Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Motor Soft Starter Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Motor Soft Starter Market?

The Motor Soft Starter Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

ABB Ltd.

Siemens AG

Schneider Electric SE

Eaton Corporation plc

Rockwell Automation, Inc.

WEG S.A.

Toshiba Corporation

CG Power and Industrial Solutions Limited (formerly Crompton Greaves)

AuCom Electronics Ltd.

Emotron AB

Who should buy this report?

The Motor Soft Starter Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Motor Soft Starter Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Motor Soft Starter Market

Get Free Sample For Motor Soft Starter Market