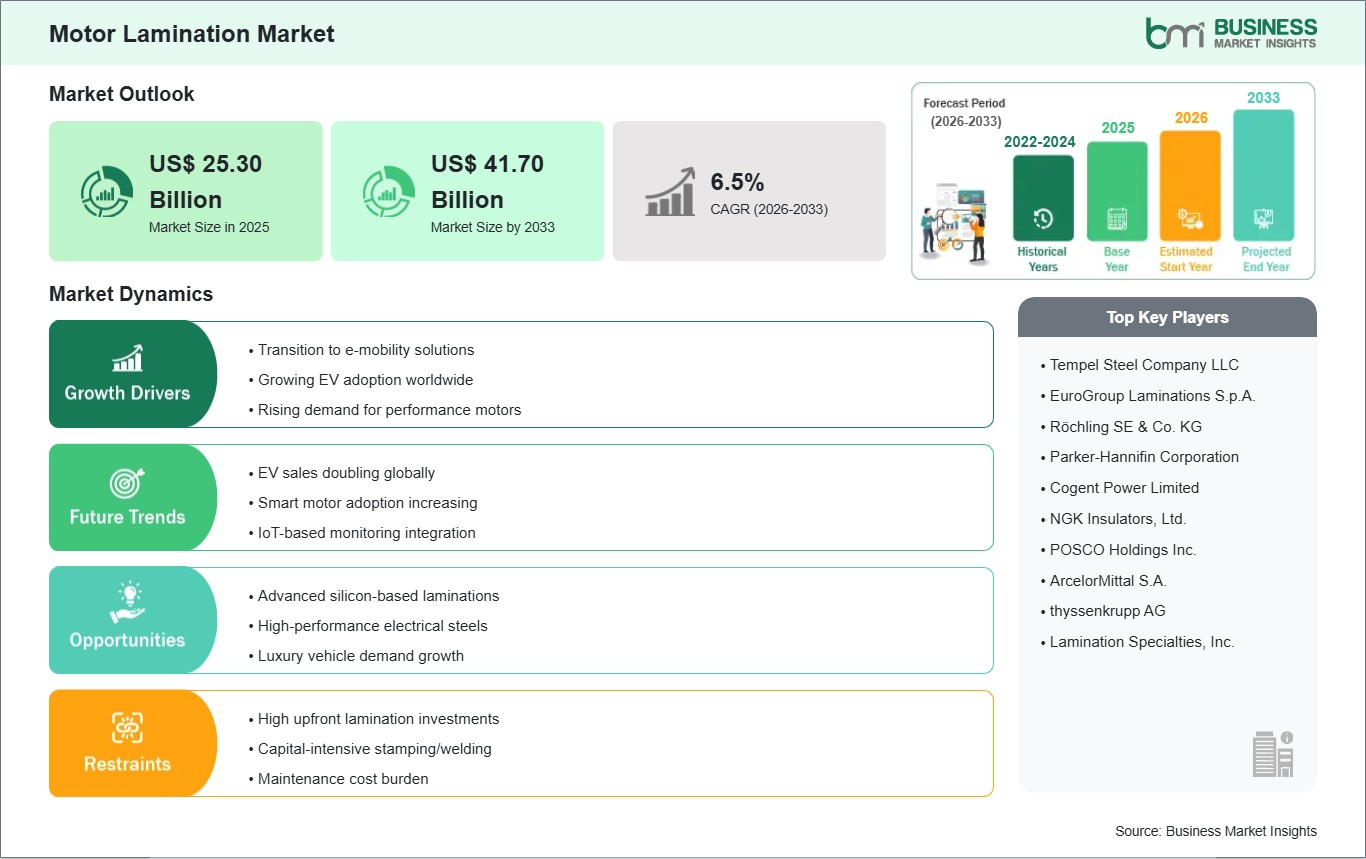

The Motor Lamination market size is expected to reach US$ 41.7 Billion by 2033 from US$ 25.3 Billion in 2025. The market is estimated to record a CAGR of 6.5% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Motor laminations are thin engineered metal sheets stacked to form stator and rotor cores that channel magnetic flux efficiently within electric motors. Their design reduces eddy current losses, supports thermal stability, and improves electromagnetic performance across compact and high-output motor systems.

Demand is being shaped by the broader shift toward electrified mobility, automated production lines, and equipment efficiency standards across industrial operations. Manufacturers are selecting refined lamination materials and tighter fabrication tolerances to improve motor output, lower core losses, and support longer operating cycles in demanding environments.

Segmentation reflects how material properties, lamination positioning, and end-use requirements influence purchasing priorities. Silicon steel remains widely used for balanced magnetic behavior and process compatibility, while specialty alloys and amorphous metal attract attention where efficiency, heat control, or performance differentiation matter more directly.

Technical development is moving toward thinner gauges, cleaner edge quality, advanced coating systems, and materials suited for higher switching frequencies. These changes help motor designers align magnetic performance with compact layouts, especially in applications requiring faster rotation, lower losses, and more reliable temperature management.

Competitive positioning depends on material processing capability, precision stamping quality, stack consistency, and the ability to support sector-specific motor architectures. Suppliers strengthen their standing through manufacturing flexibility, metallurgical expertise, and alignment with customer needs across automotive, industrial, energy, and aerospace programs.

Motor Lamination Market - Strategic Insights:

Get more information on this report

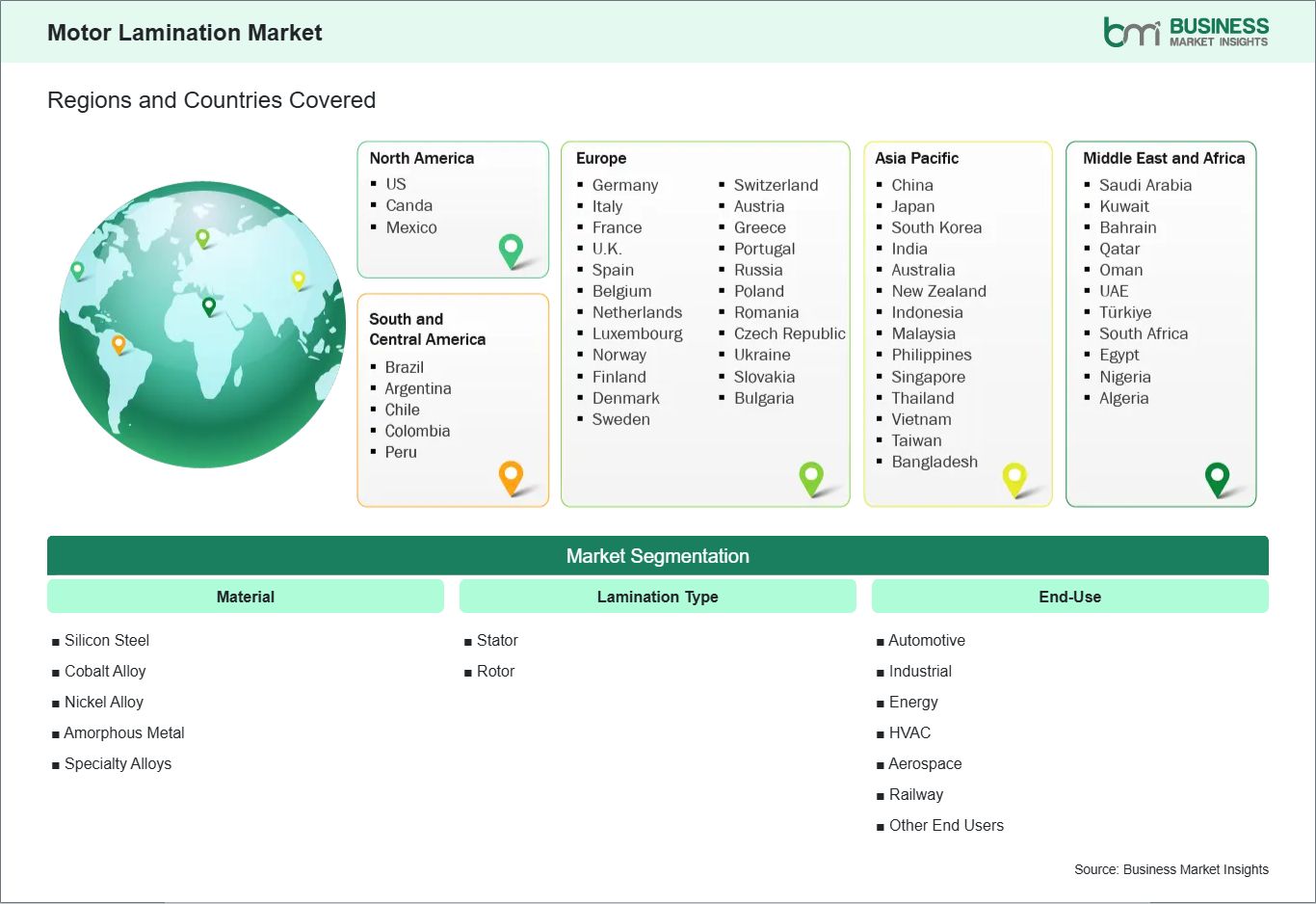

Motor Lamination Market Segmentation Analysis:

The motor lamination market is segmented by material, lamination type, and end-use across diverse motor manufacturing requirements.

By Material

Silicon Steel: Balances magnetic efficiency, manufacturability, and cost across mainstream motor designs.

Cobalt Alloy: Suits high-temperature motors requiring strong magnetic performance under demanding loads.

Nickel Alloy: Supports specialized motors where corrosion resistance and thermal endurance matter.

Amorphous Metal: Reduces core losses in efficiency-focused and high-frequency motor applications.

Specialty Alloys: Addresses tailored performance needs in precision-driven and advanced industrial systems.

By Lamination Type

Stator: Forms the stationary magnetic path central to torque generation efficiency.

Rotor: Enables controlled rotational response through optimized flux interaction and balance.

By End-Use

Automotive: Requires compact, efficient laminations for traction and auxiliary motor systems.

Industrial: Favors durable lamination stacks for continuous-duty and automation-heavy operations.

Energy: Uses advanced cores in generators, drives, and conversion equipment.

HVAC: Relies on stable magnetic performance in compressors, blowers, and fan motors.

Aerospace: Demands lightweight laminations with precise performance under strict operating conditions.

Railway: Supports traction and auxiliary motor assemblies requiring robustness and thermal control.

Other End Users: Includes appliances, robotics, marine systems, and specialized machinery.

Motor Lamination Market Drivers and Opportunities:

Efficiency Standards and Electrification Expanding Precision Lamination Requirements

Stricter efficiency targets across transport, factory systems, and energy equipment are pushing motor designers to refine core construction. That need increases the relevance of motor laminations with lower magnetic losses, tighter dimensional control, and better material consistency. As electric motors become central to propulsion, motion control, and power conversion, buyers are placing greater emphasis on laminations that support efficient flux flow and dependable thermal behavior.

This shift influences supplier selection, production methods, and product development priorities throughout the value chain. Automotive and industrial users seek laminations that improve motor efficiency without compromising manufacturability. Energy and HVAC applications also value stable magnetic performance under continuous operating conditions. These requirements keep advanced lamination solutions commercially relevant across sectors where motor output, durability, and system efficiency remain closely linked.

Advanced Materials and High-Speed Motor Designs Creating New Product Space

The move toward higher-speed motors, compact drive systems, and specialized efficiency targets is encouraging innovation in lamination materials and processing techniques. Amorphous metal, cobalt alloy, and other specialty materials are gaining attention where conventional options cannot fully meet loss reduction or heat tolerance needs. These developments are opening use cases in traction systems, industrial automation, aerospace equipment, and premium energy applications that require differentiated motor performance.

Future scope is widening as manufacturers align material science with stamping accuracy, coating performance, and stack integrity. Expansion potential extends to motors designed for smaller footprints, higher rotational speeds, and stricter energy profiles. The industry can benefit as advanced lamination formats become easier to integrate into serial production, enabling broader deployment across established motor categories and emerging applications with demanding performance thresholds.

Motor Lamination Market Size and Share Analysis:

The Motor Lamination market size is expected to reach US$ 41.7 Billion by 2033 from US$ 25.3 Billion in 2025. The market is estimated to record a CAGR of 6.5% from 2026 to 2033. This trajectory reflects stronger integration of efficient motor cores across electrified transport, industrial automation, HVAC systems, and energy equipment where magnetic precision and loss control influence overall system performance.

By material, silicon steel holds the leading position because it combines magnetic suitability with broad manufacturing acceptance across high-volume motor production. Specialty alloys and amorphous metal remain important in performance-sensitive programs where efficiency, heat resistance, or design specificity outweigh standard material preferences. By lamination type, stator laminations command stronger attention because they shape the stationary magnetic circuit central to motor effectiveness.

By end-use, automotive represents the dominant application area as electrified powertrains and auxiliary motor systems require precisely engineered lamination stacks. Industrial follows closely due to sustained motor usage in automation, processing, and material handling equipment. Energy, HVAC, aerospace, and railway applications also contribute to demand as each segment requires efficient magnetic cores aligned with operational durability, speed control, and thermal management needs.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Tempel Steel Company LLC

EuroGroup Laminations S.p.A.

Röchling SE & Co. KG

Parker-Hannifin Corporation

Cogent Power Limited

NGK Insulators, Ltd.

POSCO Holdings Inc.

ArcelorMittal S.A.

thyssenkrupp AG

Lamination Specialties, Inc.

Get more information on this report

Motor Lamination Market Report Coverage and Deliverables:

The " Motor Lamination Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Motor Lamination Market Geographic Insights:

The Motor Lamination market shows diverse regional adoption patterns influenced by manufacturing depth, electrification agendas, efficiency standards, and downstream motor production priorities. Across the broader global landscape, demand reflects the intersection of transport electrification, factory automation, and energy system modernization. Material selection, stamping precision, and supply chain localization remain central considerations as buyers evaluate performance, production continuity, and cost alignment.

North America maintains a firm market position through its established automotive manufacturing base, emphasis on motor efficiency, and investments in electrified mobility. The region supports demand for advanced lamination materials through domestic production initiatives and specialized industrial applications. Aerospace and railway programs further reinforce the need for precision-engineered stator and rotor cores that can operate reliably under strict quality and performance requirements.

Asia Pacific represents the most expansive manufacturing environment for motor laminations due to its concentration of motor production, electronics assembly, and electric vehicle development. Regional suppliers benefit from integrated supply networks, processing scale, and strong demand from industrial machinery and HVAC equipment. The market also gains support from capacity expansion in energy equipment and transport systems, where efficient core materials contribute to higher output stability and lower operational losses.

Europe remains a technology-focused market shaped by premium motor applications, regulatory attention to energy efficiency, and sustained work on advanced materials. Demand is supported by automotive electrification, industrial modernization, and specialized aerospace programs requiring refined magnetic components. Beyond Europe, emerging markets in the Middle East, Africa, and South and Central America are becoming more relevant as infrastructure upgrades, industrial investment, and transport system development create room for broader deployment of efficient motor core solutions.

Get more information on this report

Motor Lamination Market Research Report Guidance:

The Motor Lamination market report includes qualitative and quantitative data in the market across Material, Lamination, End-Use, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover market segments by Material, Lamination, End-Use, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Motor Lamination Market News and Key Development:

The motor lamination market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

October 2025 Worthington Steel, Inc. announced that its Tempel Steel subsidiary has developed Full Surface Bonding (FSB), a process for bonding electrical steel laminations which, when stacked together, form a motor core. The patent-pending technology is designed to improve performance and manufacturing efficiency in automotive and industrial motor applications.

November 2024: EuroGroup Laminations (EGLA) completed the acquisition of a 40% stake in Kumar Precision Stampings Private Limited. This followed the investment agreement announced on 1 August 2024. Kumar Precision Stampings is a prominent Indian company specialising in the production and distribution of stators and rotors for electric motors, serving various industrial and domestic sectors, including HVAC, railways, home appliances, pumps, and generators. This acquisition represents a strategic expansion for EGLA, enhancing its global industrial business unit and establishing a strong presence in the rapidly expanding Indian market.

Key Sources Referred:

International Electrotechnical CommissionInternational Organization for StandardizationInternational Energy AgencyS. Department of EnergyEuropean Committee for Electrotechnical StandardizationCompany filingsAcademic studiesTrade association publicationsTechnical conference papers

The List of Companies - Motor Lamination Market

Tempel Steel Company LLC

EuroGroup Laminations S.p.A.

Röchling SE & Co. KG

Parker-Hannifin Corporation

Cogent Power Limited

NGK Insulators, Ltd.

POSCO Holdings Inc.

ArcelorMittal S.A.

thyssenkrupp AG

Lamination Specialties, Inc.

Frequently Asked Questions

How big is the Motor Lamination Market?

The Motor Lamination Market is valued at US$ 25.30 Billion in 2025, it is projected to reach US$ 41.70 Billion by 2033.

What is the CAGR for Motor Lamination Market by (2026 - 2033)?

As per our report Motor Lamination Market, the market size is valued at US$ 25.30 Billion in 2025, projecting it to reach US$ 41.70 Billion by 2033. This translates to a CAGR of approximately 6.5% during the forecast period.

What segments are covered in this report?

The Motor Lamination Market report typically cover these key segments-

End-Use (Automotive, Industrial, Energy, HVAC, Aerospace, Railway, Other End Users)

What is the historic period, base year, and forecast period taken for Motor Lamination Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Motor Lamination Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Motor Lamination Market?

The Motor Lamination Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Tempel Steel Company LLC

EuroGroup Laminations S.p.A.

Röchling SE & Co. KG

Parker-Hannifin Corporation

Cogent Power Limited

NGK Insulators, Ltd.

POSCO Holdings Inc.

ArcelorMittal S.A.

thyssenkrupp AG

Lamination Specialties, Inc.

Who should buy this report?

The Motor Lamination Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Motor Lamination Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Motor Lamination Market

Get Free Sample For Motor Lamination Market