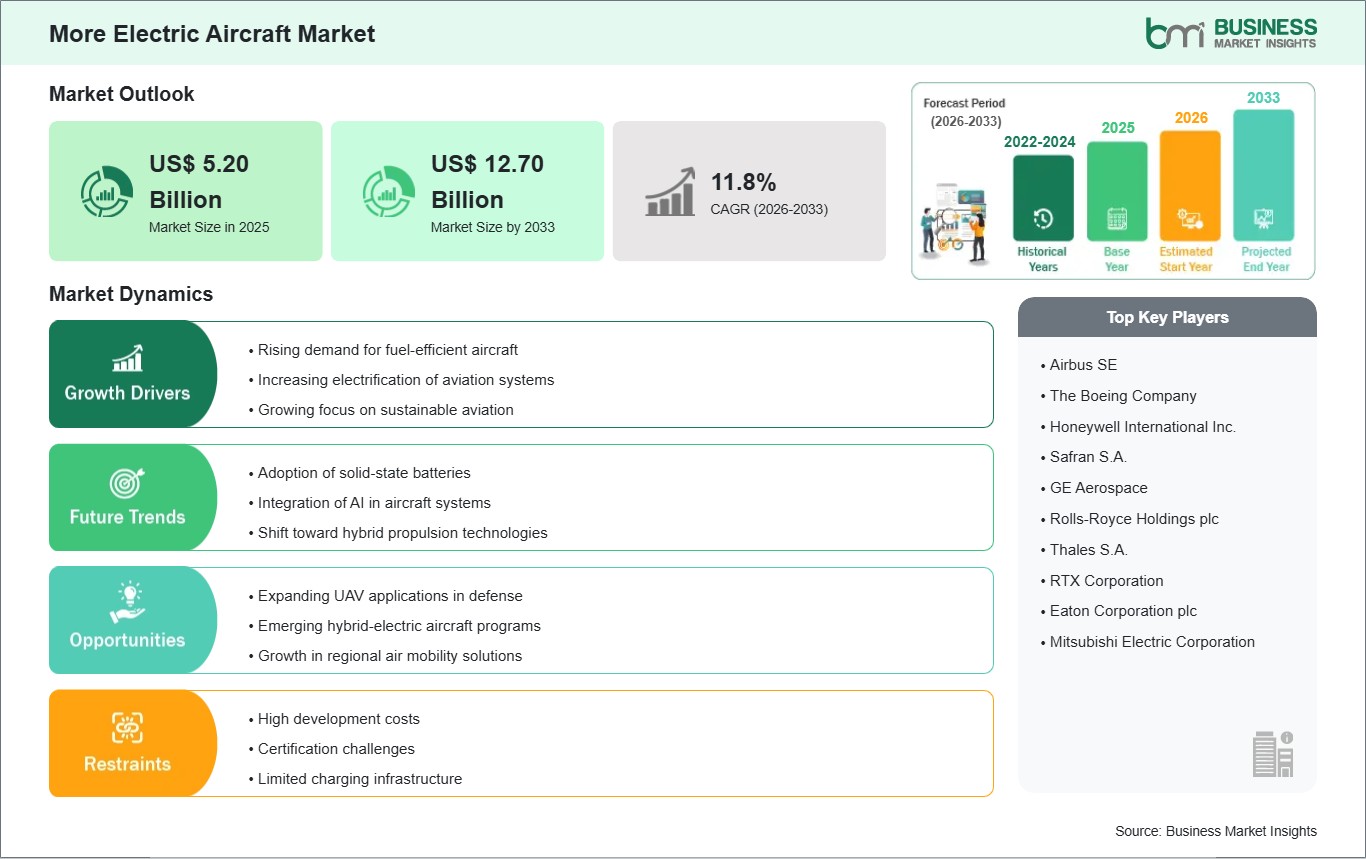

The More Electric Aircraft market size is expected to reach US$ 12.70 Billion by 2033 from US$ 5.20 Billion in 2025. The market is estimated to record a CAGR of 11.8% from 2026 to 2033.

Executive Summary and Global Market Analysis:

More electric aircraft are aircraft platforms that replace conventional hydraulic, pneumatic, and mechanical subsystems with electrically powered alternatives to improve energy efficiency, weight distribution, and system controllability. This architecture uses electric power conversion and distribution to support flight-critical and non-flight-critical functions across fixed-wing and unmanned platforms.

Airframe manufacturers and operators are advancing electrified subsystem integration to reduce fuel burn, simplify maintenance pathways, and support tighter emissions objectives. Electrification also improves response precision in onboard functions, making it attractive for next-generation commercial fleets, defense aircraft, and specialized mission platforms.

Technology segmentation reflects how onboard electrical architectures are becoming more distributed and performance-oriented. Power electronics manage conversion and control efficiency, generators support higher onboard loads, actuators replace hydraulic mechanisms in targeted systems, and electric pumps improve subsystem responsiveness across critical aircraft functions.

Design progress is centered on higher-voltage networks, lighter electrical components, and smarter control integration. These advances enable aircraft programs to shift more onboard functions toward electric operation without compromising reliability, while also opening room for modular architectures suited to evolving commercial, military, and UAV requirements.

Competitive conditions are shaped by subsystem integration capability, certification readiness, thermal management expertise, and electrical reliability under demanding flight profiles. Suppliers compete through component efficiency, compact design, and their ability to align electrified systems with broader aircraft modernization strategies.

More Electric Aircraft Market - Strategic Insights:

Get more information on this report

More Electric Aircraft Market Segmentation Analysis:

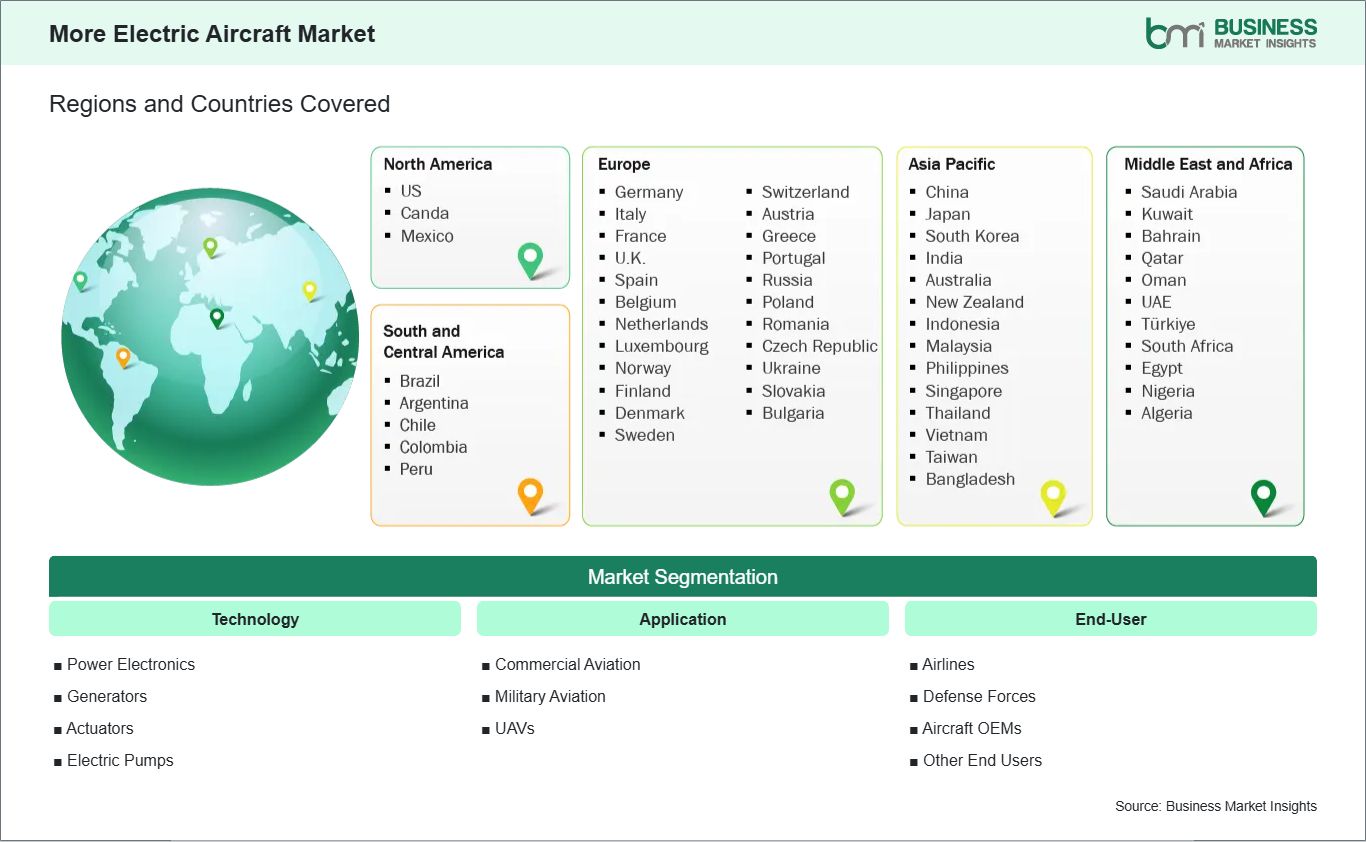

The more electric aircraft market is segmented by technology, application, and end-user across evolving aviation deployment models.

By Technology

Power Electronics: Governs efficient energy conversion across increasingly complex onboard electrical architectures.

Generators: Supports elevated electrical loads in modernized airborne power networks.

Aircraft developers are under sustained pressure to improve efficiency without relying solely on aerodynamic refinement. That need is directing attention toward electrically powered subsystems that reduce reliance on bleed air, hydraulic routing, and mechanically intensive assemblies. As electrical architectures become more capable, OEMs are integrating generators, actuators, and power electronics to support lower system losses and better controllability across modern aircraft programs.

The impact extends beyond component replacement because electrification influences maintenance logic, system packaging, and onboard energy management. In commercial aviation, this shift aligns with long-term fleet efficiency priorities. In defense aviation, the same transition supports higher onboard power availability and system resilience. These combined factors keep more electric aircraft strategies relevant across platform classes and development timelines.

High-Voltage Architectures Opening New Integration Pathways

Interest in higher-voltage aircraft networks is creating room for more capable electrical subsystems and tighter functional integration. Innovation in conversion hardware, thermal control, and compact actuation is allowing engineers to distribute power more effectively across the airframe. This trend is especially relevant where aircraft designers need scalable architectures that support avionics loads, environmental control functions, and mission-specific electrical demands.

Future scope is broadening as electrical designs move from subsystem enhancement to architecture-level differentiation. Expansion opportunities are emerging in retrofit programs, next-generation narrow-body development, advanced military platforms, and UAV configurations requiring compact power distribution. The market stands to benefit as validated electrical components become easier to integrate, certify, and align with long-horizon aircraft modernization programs.

More Electric Aircraft Market Size and Share Analysis:

The More Electric Aircraft market size is expected to reach US$ 12.70 Billion by 2033 from US$ 5.20 Billion in 2025. The market is estimated to record a CAGR of 11.8% from 2026 to 2033. This expansion indicates steady integration of electrical subsystems into aircraft design priorities, supported by the need for efficiency, better controllability, and reduced dependence on legacy mechanical architectures.

By technology, power electronics hold a central position because they regulate conversion, control, and distribution across electrified aircraft functions. Generators also maintain strategic importance as onboard electrical loads expand. Actuators continue to gain attention where aircraft programs seek precise motion control with lower hydraulic dependence, while electric pumps support compact and responsive subsystem management.

By application, commercial aviation represents the leading arena for electrified subsystem deployment because efficiency and lifecycle performance remain central procurement considerations. Military aviation follows with emphasis on power-rich mission systems and operational robustness. UAVs present a distinct growth avenue as compact electrical architectures fit well with lightweight platforms, automated control needs, and evolving mission versatility.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Airbus SE

The Boeing Company

Honeywell International Inc.

Safran S.A.

GE Aerospace

Rolls-Royce Holdings plc

Thales S.A.

RTX Corporation

Eaton Corporation plc

Mitsubishi Electric Corporation

Get more information on this report

More Electric Aircraft Market Report Coverage and Deliverables:

The " More Electric Aircraft Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

More Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

More Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

More Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

More Electric Aircraft Market Geographic Insights:

The More Electric Aircraft market shows diverse regional adoption patterns influenced by industrial capability, certification pathways, fleet renewal strategies, and defense modernization agendas. Across the global landscape, the shift toward electrically powered subsystems reflects a broader effort to improve aircraft efficiency, simplify maintenance-intensive architectures, and support long-term platform evolution in both civil and military aviation environments.

North America holds a strong position because of its deep aerospace engineering base, established aircraft programs, and sustained investment in subsystem innovation. The region benefits from close coordination among OEMs, component suppliers, and defense stakeholders working on higher-power onboard systems. Commercial and military development activity continues to reinforce interest in generators, actuators, and advanced electrical control units.

Asia Pacific is building momentum through expanding aerospace manufacturing capability, rising air traffic requirements, and stronger national interest in indigenous aviation technologies. The region presents opportunities for electrical subsystem suppliers as aircraft programs place greater emphasis on efficiency and platform modernization. UAV development and defense procurement are also contributing to broader acceptance of compact, power-conscious onboard electrical architectures.

Europe remains important due to its concentration of aircraft design expertise and sustained focus on lower-emission aviation technologies. Electrified subsystem development is closely tied to collaborative innovation programs and next-generation aircraft concepts. Beyond the major regions, emerging markets in the Middle East, Latin America, and selected African economies are gaining relevance as fleet expansion, defense acquisition, and aviation infrastructure upgrades create space for more advanced aircraft systems.

Get more information on this report

More Electric Aircraft Market Research Report Guidance:

The More Electric Aircraft Market report includes qualitative and quantitative data in the market across Technology, Application, End-User, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover market segments by Technology, Application, End-User, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

More Electric Aircraft Market News and Key Development:

The more electric aircraft market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

April 2026: Joby Aviation, Inc. announced the completion of the first-ever point-to-point electric vertical takeoff and landing (eVTOL) air taxi demonstration flights in New York City's history, marking the start of a week-long public campaign across the city's existing heliport network. Framed against the most iconic skyline in the world, the campaign offers the first real-world demonstration of how electric air taxis, which are quiet and produce zero operating emissions, will be able to connect the region, linking vertiports, international airports, and communities across the New York metropolitan area.

March 2026: Surf Air Mobility Inc. and BETA Technologies announced an Aircraft Purchase Agreement and strategic partnership intended to accelerate the introduction of safe, reliable, and profitable advanced air mobility solutions. Under the terms of the Aircraft Purchase Agreement, Surf Air Mobility has signed a firm order for 25 all-electric ALIA CTOL aircraft and has the option to add up to 75 additional aircraft to its order. The aircraft will be introduced into Surf Air Mobility's platform for regional operations. This order adds to BETA's growing commercial aircraft backlog and highlights the versatility of its ALIA aircraft across passenger, cargo, and medical use cases.

Key Sources Referred:

International Civil Aviation Organization (ICAO)International Air Transport Association (IATA)National Aeronautics and Space Administration (NASA)European Union Aviation Safety Agency (EASA)Commercial Aviation Alternative Fuels Initiative (CAAFI)Company filingsAcademic studiesPeer-reviewed journalsTechnical conference papers

The List of Companies - More Electric Aircraft Market

Airbus SE

The Boeing Company

Honeywell International Inc.

Safran S.A.

GE Aerospace

Rolls-Royce Holdings plc

Thales S.A.

RTX Corporation

Eaton Corporation plc

Mitsubishi Electric Corporation

Frequently Asked Questions

How big is the More Electric Aircraft Market?

The More Electric Aircraft Market is valued at US$ 5.20 Billion in 2025, it is projected to reach US$ 12.70 Billion by 2033.

What is the CAGR for More Electric Aircraft Market by (2026 - 2033)?

As per our report More Electric Aircraft Market, the market size is valued at US$ 5.20 Billion in 2025, projecting it to reach US$ 12.70 Billion by 2033. This translates to a CAGR of approximately 11.8% during the forecast period.

What segments are covered in this report?

The More Electric Aircraft Market report typically cover these key segments-

Technology (Power Electronics, Generators, Actuators, Electric Pumps)

Application (Commercial Aviation, Military Aviation, UAVs)

End-User (Airlines, Defense Forces, Aircraft OEMs, Other End Users)

What is the historic period, base year, and forecast period taken for More Electric Aircraft Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the More Electric Aircraft Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in More Electric Aircraft Market?

The More Electric Aircraft Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Airbus SE

The Boeing Company

Honeywell International Inc.

Safran S.A.

GE Aerospace

Rolls-Royce Holdings plc

Thales S.A.

RTX Corporation

Eaton Corporation plc

Mitsubishi Electric Corporation

Who should buy this report?

The More Electric Aircraft Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the More Electric Aircraft Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For More Electric Aircraft Market

Get Free Sample For More Electric Aircraft Market