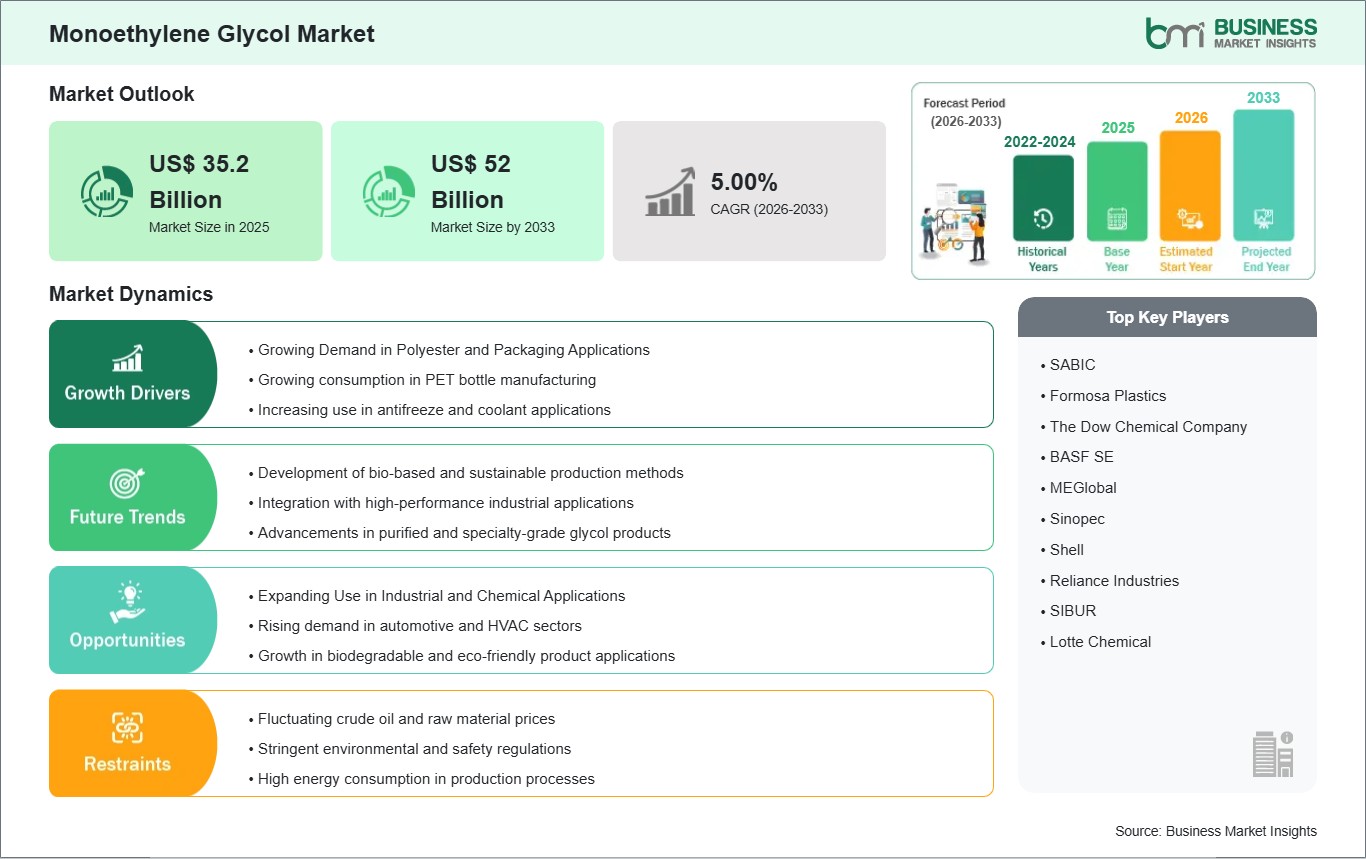

The Monoethylene Glycol Market size is expected to reach US$ 52 Billion by 2033 from US$ 35.2 Billion in 2025. The market is estimated to record a CAGR of 5.00% from 2026 to 2033.

Executive Summary and Global Market Analysis:

There is robust expansion occurring in the monoethylene glycol (MEG) market due to the substantial need for MEG as a feedstock in polyester fiber production, polyethylene terephthalate (PET) resins, and antifreeze products. Polyester production is a major part of the global textile and packaging industries and is being affected by increased demand for clothing, industrial textiles, and PET bottles. The expansion of e-commerce, packaged foods, and beverage businesses has also contributed to increased consumption of PET resins, which affects the demand for MEG. The production of MEG has also benefited from technological improvements to produce MEG economically through processes such as more efficient hydration of ethylene oxide and greater integration of refining. Additional efficiencies have been realised through increased yields and increased product purity. There has been a continued focus on achieving cost efficiencies through increased energy efficiency during large-scale production.

Sustainability and environmental regulations continue to drive the adoption of bio-based MEG and closed-loop recycling initiatives, with Europe and North America leading the charge. Market challenges will continue to revolve around raw material price volatility, energy-intensive production processes, as well as challenges associated with the corrosive properties of MEG, requiring more stringent procedures in handling and storing MEG. Market participants are looking to expand their overall capacity, vertically integrating to their downstream and entering into agreements with polyester and PET manufacturers to enter long-term supply contracts and optimise margin opportunities. In sum, the MEM market outlook is good due to the global climate of industrialisation; stronger manufacturing of textiles and packaging, and governments pursuing sustainable development policies.

Monoethylene Glycol Market - Strategic Insights:

Get more information on this report

Monoethylene Glycol Market Segmentation Analysis:

Key segments that contributed to the derivation of the monoethylene glycol (MEG) market analysis are application and technology.

Application, the monoethylene glycol market is classified into fiber, PET, film, antifreeze & coolant, and others. The PET segment dominated the market in 2025.

Technology, the monoethylene glycol market is segmented into naphtha‑based, coal- and natural gas‑based, bio‑based, and technology providers. The naphtha‑based segment dominated the market in 2025.

Monoethylene Glycol Market Drivers and Opportunities:

Growing Demand in Polyester and Packaging Applications

The monoethylene glycol market is growing significantly due to the increasing use of the product in polyester production, especially polyethylene terephthalate fibers and resins. Monoethylene glycol is mainly used as one of the raw materials in the production of polyester, and polyester is used extensively in various industries. The increasing demand for durable, lightweight, and recyclable packaging materials is driving the monoethylene glycol market, especially in the consumer goods, food and beverage, and industrial packaging industries.

The chemical properties of monoethylene glycol enable manufacturers to produce quality polyester with good strength, clarity, and heat stability. The use of monoethylene glycol in the production of polyethylene terephthalate resin ensures the quality and performance of polyester, enabling the production of polyester fibers, bottles, and films, and providing support to various applications that require quality polyester with good strength, flexibility, and transparency. The increasing trend towards recyclable packaging is driving the monoethylene glycol market, as polyethylene terephthalate is one of the most recycled plastics worldwide.

Beyond packaging and textiles, MEG is also used in antifreeze, heat transfer fluids, and other industrial applications. Its versatility, chemical stability, and cost-effectiveness make it a preferred choice for multiple industrial processes. With the ongoing growth in consumer demand for lightweight and recyclable products, MEG continues to play a critical role in supporting polyester manufacturing, packaging innovations, and related industrial applications worldwide.

Expanding Use in Industrial and Chemical Applications

Monoethylene glycol is increasingly utilized in industrial and chemical sectors due to its versatility as a raw material and solvent. It is used in the production of antifreeze, coolants, and heat transfer fluids, which are essential for automotive, HVAC, and power generation systems. Its ability to maintain low freezing points, resist corrosion, and provide stable thermal performance makes it a preferred choice in these applications.

MEG is also applied in the production of resins, plasticizers, and coatings, contributing to the manufacturing of paints, adhesives, and other chemical products. Its chemical stability and compatibility with various reagents make it an essential intermediate in industrial synthesis. The material`s reliability allows manufacturers to develop customized formulations for specific applications, enhancing product performance and operational efficiency.

Growing industrialization, urbanization, and expansion of chemical and automotive sectors are driving demand for MEG across diverse applications. Its multifunctional properties, including high boiling point, low toxicity, and ease of handling, make it indispensable for modern chemical and industrial processes. As industries increasingly focus on efficiency, sustainability, and high-performance materials, MEG continues to emerge as a key chemical intermediate that supports innovation and operational resilience across multiple global sectors.

Monoethylene Glycol Market Size and Share Analysis:

The monoethylene glycol market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within application and technology, offering insights into their contribution to overall market performance.

By Application, the PET subsegment dominated the market in 2025, driven by its extensive use in polyester fibers and packaging films.

Based on Technology, the naphtha‑based subsegment dominated the market in 2025, supported by its cost-effectiveness and established production infrastructure.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

SABIC

Formosa Plastics

The Dow Chemical Company

BASF SE

MEGlobal

Sinopec

Shell

Reliance Industries

SIBUR

Lotte Chemical

Get more information on this report

Monoethylene Glycol Market Report Coverage and Deliverables:

The "Monoethylene Glycol Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Monoethylene Glycol Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Monoethylene Glycol Market trends, as well as drivers, restraints, and opportunities

Monoethylene Glycol Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Monoethylene Glycol Market

Detailed company profiles, including SWOT analysis

Monoethylene Glycol Market Geographic Insights:

The geographical scope of the Monoethylene Glycol Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

Regional-level dynamics in the monoethylene glycol market reveal diverse growth patterns influenced by industrial capacity, regulatory frameworks, and downstream demand. North America is the dominant region, supported by a mature chemical manufacturing industry, extensive polyester and PET production, and robust regulatory compliance in handling and environmental safety. The United States leads in integrating advanced MEG production technologies to ensure consistent quality and efficiency.

Europe shows steady growth, driven by sustainability mandates, stringent environmental regulations, and adoption of recycled PET and bio-MEG in Germany, France, and the UK.

Asia Pacific is the fastest-growing region, led by China, India, and Japan, fueled by massive polyester fiber manufacturing, booming packaging industries, and infrastructure development. Investments in expanding ethylene oxide and MEG production capacities further strengthen regional growth.

Middle East & Africa demonstrates moderate growth, supported by petrochemical expansion and growing industrialization, though limited local MEG production makes the region reliant on imports.

South & Central America is an emerging market, with Brazil and Argentina leading adoption due to growing textile and packaging sectors, although high cost sensitivity and infrastructure limitations slow market penetration.

Across all regions, growth is shaped by downstream polyester and PET demand, industrial expansion, and increasing focus on sustainable and energy-efficient production solutions.

Get more information on this report

Monoethylene Glycol Market Research Report Guidance:

The report includes qualitative and quantitative data in the Monoethylene Glycol Market across application, technology and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Monoethylene Glycol Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Monoethylene Glycol Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Monoethylene Glycol Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 9 cover Monoethylene Glycol Market segments across application, technology and geography across North America, Asia Pacific, Europe, the Middle East & Africa, and South & Central America. They cover the market revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Monoethylene Glycol Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Monoethylene Glycol Market News and Key Development:

The Monoethylene Glycol Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the monoethylene glycol market are:

In October 2024, Sustainea and Primient announced a strategic co‑location partnership to build what will be one of the largest Bio‑MEG (monoethylene glycol) facilities in the United States (Lafayette, Indiana); the planned plant—backed by about US$ 400 million investment—will produce renewable, plant‑based MEG using Primient`s corn‑derived dextrose as feedstock, targeting sustainable PET and fiber applications.

In November 2025, Sustainea Bioglycols launched a regenerative agriculture project in partnership with Primient to support sustainable corn sourcing near Lafayette, Indiana that underpins its Bio‑MEG supply chain, aiming to improve soil health and reduce environmental impact for future renewable MEG production.

Key Sources Referred:

International Organization for Standardization (ISO)American Society for Testing and Materials (ASTM International)Bureau of Indian Standards (BIS)Environmental Protection Agency (EPA), USAEuropean Chemicals Agency (ECHA)Central Pollution Control Board (CPCB), IndiaMinistry of Chemicals and Fertilizers, IndiaAmerican Chemistry Council (ACC)Indian Chemical Council (ICC)European Chemical Industry Council (Cefic)Specialty Chemical Association of India (SCAI)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Monoethylene Glycol Market

SABIC

Formosa Plastics

The Dow Chemical Company

BASF SE

MEGlobal

Sinopec

Shell

Reliance Industries

SIBUR

Lotte Chemical

About Author— Chemicals and Materials Research Team

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Show More

Frequently Asked Questions

How big is the Monoethylene Glycol Market?

The Monoethylene Glycol Market is valued at US$ 35.2 Billion in 2025, it is projected to reach US$ 52 Billion by 2033.

What is the CAGR for Monoethylene Glycol Market by (2026 - 2033)?

As per our report Monoethylene Glycol Market, the market size is valued at US$ 35.2 Billion in 2025, projecting it to reach US$ 52 Billion by 2033. This translates to a CAGR of approximately 5.00% during the forecast period.

What segments are covered in this report?

The Monoethylene Glycol Market report typically cover these key segments-

Application (Fiber, PET, Film, Antifreeze & Coolant, Other Applications)

Technology (Naphtha-based, Coal- and Natural Gas-based, Bio-based, Technology Providers)

What is the historic period, base year, and forecast period taken for Monoethylene Glycol Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Monoethylene Glycol Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Monoethylene Glycol Market?

The Monoethylene Glycol Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

SABIC

Formosa Plastics

The Dow Chemical Company

BASF SE

MEGlobal

Sinopec

Shell

Reliance Industries

SIBUR

Lotte Chemical

Who should buy this report?

The Monoethylene Glycol Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Monoethylene Glycol Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Monoethylene Glycol Market

Get Free Sample For Monoethylene Glycol Market