01

Market Summery

Executive Summary and Global Market Analysis

Mine detection systems are specialized sensing platforms designed to identify buried, surface, and underwater explosive hazards across operational environments. They combine detection hardware, signal processing, and deployment mobility to support clearance missions, route assurance, coastal surveillance, and security screening where concealed threats can disrupt movement, infrastructure access, and mission continuity.

Procurement activity across defense and homeland security reflects the need for faster area assessment and safer stand-off operations. Operators increasingly favor systems that reduce manual exposure, improve search precision, and maintain performance across cluttered terrain, shallow waters, and mission zones where conventional inspection methods impose operational delays.

Segment dynamics differ according to mission profile and operating theater. Defense remains central because military formations require route clearance, force protection, and maritime countermeasure capability. Homeland security applications remain relevant in border monitoring and critical site screening. Deployment formats vary by access conditions, scanning range, platform compatibility, and the urgency of threat confirmation.

Technology development is centered on sharper target discrimination, broader environmental adaptability, and stronger integration with mobile platforms. Radar-based systems remain important for subsurface scanning, laser-based systems support airborne and near-surface detection tasks, and sonar-based systems remain essential for underwater mine search missions where acoustic imaging is required.

Competitive conditions are shaped by sensor reliability, platform interoperability, operational range, and ease of field deployment. Suppliers differentiate through multi-sensor integration, environmental performance, and mission-specific engineering, while procurement decisions increasingly reflect the need for adaptable systems that align with modernization priorities and evolving threat detection requirements.

03

Segment Analysis

Mine Detection System Market Segmentation

The mine detection system market is segmented by application, deployment, and technology to reflect mission design and operating conditions.

By Application

- Defense: Prioritizes route security, tactical clearance, and mission-focused threat localization.

- Homeland Security: Focuses on border surveillance and protection of sensitive civilian assets.

By Deployment

- Vehicle Mounted: Extends ground coverage across routes requiring durable scanning mobility.

- Ship Mounted: Supports maritime search operations in contested coastal and harbor zones.

- Airborne Mounted: Enables wider-area assessment with faster access to difficult locations.

- Handheld: Assists close-range verification in confined, irregular, or complex terrain.

By Technology

- Radar Based: Detects subsurface anomalies where buried threat mapping is essential.

- Laser Based: Examines near-surface and airborne search environments with high-resolution sensing.

- Sonar Based: Interprets underwater mine signatures across littoral and deeper waters.

04

Market Forces

Mine Detection System Market Drivers and Opportunities

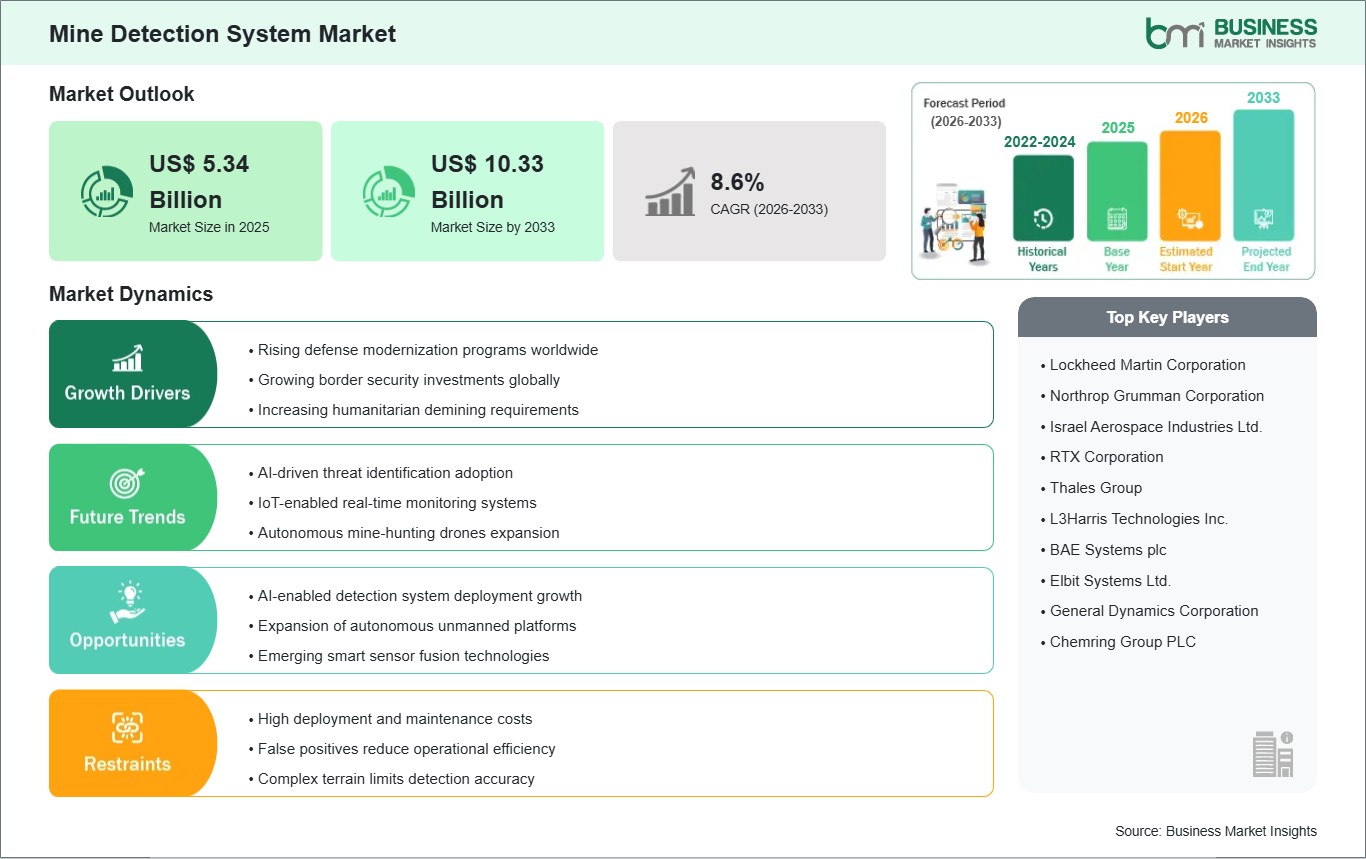

Operational Need for Safer Stand-Off Detection

Threat environments containing buried, floating, or submerged explosives require detection methods that reduce human exposure during search operations. This need is accelerating procurement of mine detection systems across military and security organizations seeking more reliable clearance support. Adoption rises where manual inspection slows movement, complicates mission planning, and exposes personnel to unacceptable operational risk during area verification.

The impact of stand-off detection extends to route assurance, port access, border monitoring, and infrastructure protection. In these settings, operators require systems that can localize threats with greater confidence while preserving mission tempo. This relevance remains strong as security agencies and defense forces seek detection platforms that improve field safety without narrowing deployment flexibility across land and maritime environments.

Sensor Fusion and Unmanned Integration Expanding Use Cases

A notable opportunity is emerging through the combination of multi-sensor detection and unmanned platform integration. Developers are refining systems that merge radar, laser, and sonar outputs with autonomous navigation and remote mission control. This direction supports use cases where difficult terrain, coastal complexity, or underwater access limitations make conventional detection methods slower and less adaptable.

Future scope lies in broader deployment across mixed-environment missions that require scalable sensing and reduced operator burden. As procurement preferences shift toward modular and interoperable systems, suppliers can expand through platform-agnostic solutions tailored to airborne, maritime, and ground-based operations. This trajectory can deepen market reach while improving mission readiness in high-risk and access-constrained scenarios.

05

Size and Share Analysis

Mine Detection System Market Size and Share Analysis

The Mine Detection System market size is expected to reach US$ 10.33 Billion by 2033 from US$ 5.34 Billion in 2025. The market is estimated to record a CAGR of 8.6% from 2026 to 2033. This progression reflects sustained procurement interest in systems that improve detection accuracy, reduce field exposure, and support operational continuity across security-focused missions.

By deployment, vehicle mounted systems maintain a prominent position because they support route coverage, mobility, and equipment integration in demanding field conditions. Airborne mounted systems hold strategic relevance for wider-area assessment, while handheld formats remain important where close-range confirmation is necessary. Ship mounted systems remain closely aligned with maritime countermeasure requirements.

By application, defense represents the leading area of use due to mission-critical demand for route clearance, force protection, and maritime security operations. Homeland security contributes through infrastructure safeguarding, border surveillance, and response preparedness where concealed explosive threats require rapid screening and dependable localization capability.

07

Report Coverage

Mine Detection System Market Report Coverage and Deliverables

The " Mine Detection System Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

- Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Mine Detection System Market Geographic Insights

The Mine Detection System market shows diverse regional adoption patterns influenced by defense readiness priorities, border security requirements, coastal exposure, and legacy contamination concerns. Across the global landscape, procurement decisions are closely tied to the need for reliable detection across land and maritime environments. Market direction also reflects the operational value of systems that can function across variable terrain, shallow waters, and mission scenarios requiring rapid threat confirmation.

North America retains a strong position through sustained investment in modernization programs and mission-capable surveillance systems. Regional demand is shaped by emphasis on route clearance, naval mine countermeasure readiness, and the integration of advanced sensing into mobile platforms. Procurement preferences often favor interoperable systems that can support broad-area search while maintaining compatibility with established operational frameworks and evolving security requirements.

Asia Pacific presents a distinct demand profile supported by maritime security priorities, contested littoral environments, and expanding interest in responsive surveillance infrastructure. Countries across the region are emphasizing systems suitable for coastal monitoring, underwater search, and terrain-sensitive deployment. The market also benefits from wider focus on equipment flexibility, especially where island geography, naval movement, and difficult access conditions influence detection strategy.

Europe reflects demand shaped by security coordination, defense preparedness, and attention to advanced mission support technologies. Beyond Europe, emerging markets in the Middle East and Africa and South and Central America are gradually strengthening interest in mine detection capabilities for border control, infrastructure security, and coastal vigilance. These regions present expansion potential where localized risk conditions require adaptable systems with scalable deployment formats.

10

Industry Activity

Recent Developments

The mine detection system market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

- May 2026: Epiroc is launched a comprehensive set of digital mine planning solutions globally to further strengthen mining companies’ operations. The launch marks a milestone in Epiroc's strategy to consolidate its digital technology acquisitions into one connected offering, bringing together years of integration, development, and deep mining domain expertise.

- September 2025: REPMUS (Robotic Experimentation and Prototyping with Maritime Unmanned Systems) exercise in Portugal - the world's premier event for maritime robotics and unmanned technologies - demonstrated the critical value of collaboration between industry and naval forces in advancing mine countermeasure (MCM) technologies.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

United Nations Mine Action Service (UNMAS)Defense Research and Development Organisation (DRDO)S. Army Humanitarian Demining Research & Development ProgramEuropean Defence Agency (EDA)NATO Support and Procurement Agency (NSPA)Company filingsAcademic studiesDefense procurement updatesTechnical and regulatory publications