01

Market Summery

Executive Summary and Global Market Analysis

Military sensors are advanced electronic and electro-mechanical devices designed to detect, monitor, measure, and transmit critical battlefield information across land, air, naval, and space defense environments. These sensors play a vital role in modern military operations by supporting intelligence gathering, target acquisition, surveillance, reconnaissance, navigation, threat detection, electronic warfare, missile guidance, and situational awareness. Military sensors are integrated into a wide range of defense systems including radar systems, unmanned platforms, armored vehicles, naval vessels, missile systems, fighter aircraft, satellites, and soldier-worn equipment to enhance operational effectiveness and mission precision.

The market is experiencing strong growth due to increasing global defense spending, rising geopolitical tensions, and accelerating modernization of military infrastructure worldwide. Defense agencies are increasingly investing in advanced sensing technologies to improve battlefield awareness, precision targeting, and integrated command-and-control operations. The growing deployment of unmanned aerial vehicles (UAVs), autonomous combat systems, missile defense systems, and next-generation surveillance platforms is significantly boosting demand for high-performance military sensors. In addition, rapid advancements in infrared sensing, electro-optical systems, radar technologies, MEMS sensors, LiDAR, acoustic sensing, and AI-enabled sensor fusion are supporting the development of intelligent battlefield systems capable of operating in complex combat environments.

However, market growth is constrained by several technological and operational challenges. Military-grade sensors require highly sophisticated manufacturing processes, ruggedized designs, and extensive testing to ensure performance reliability under extreme battlefield conditions. High procurement and integration costs, along with long defense procurement cycles, may limit adoption among budget-constrained defense organizations. Furthermore, cybersecurity risks, electromagnetic interference vulnerabilities, supply chain disruptions related to semiconductor components, and stringent export regulations can create deployment and operational challenges for defense contractors and military agencies.

Despite these challenges, the market outlook remains highly positive due to continuous innovation in defense electronics and sensor technologies. Emerging opportunities are being created through the development of AI-powered sensing platforms, multi-domain battlefield networks, autonomous surveillance systems, and next-generation electronic warfare solutions. The growing focus on border security, missile defense, space-based surveillance, smart soldier systems, and integrated battlefield management infrastructure is expected to create sustained long-term demand for advanced military sensors globally. Additionally, increasing investments in sensor miniaturization, edge computing, real-time data analytics, and secure communication networks are accelerating the deployment of highly intelligent and connected defense sensing ecosystems.

03

Segment Analysis

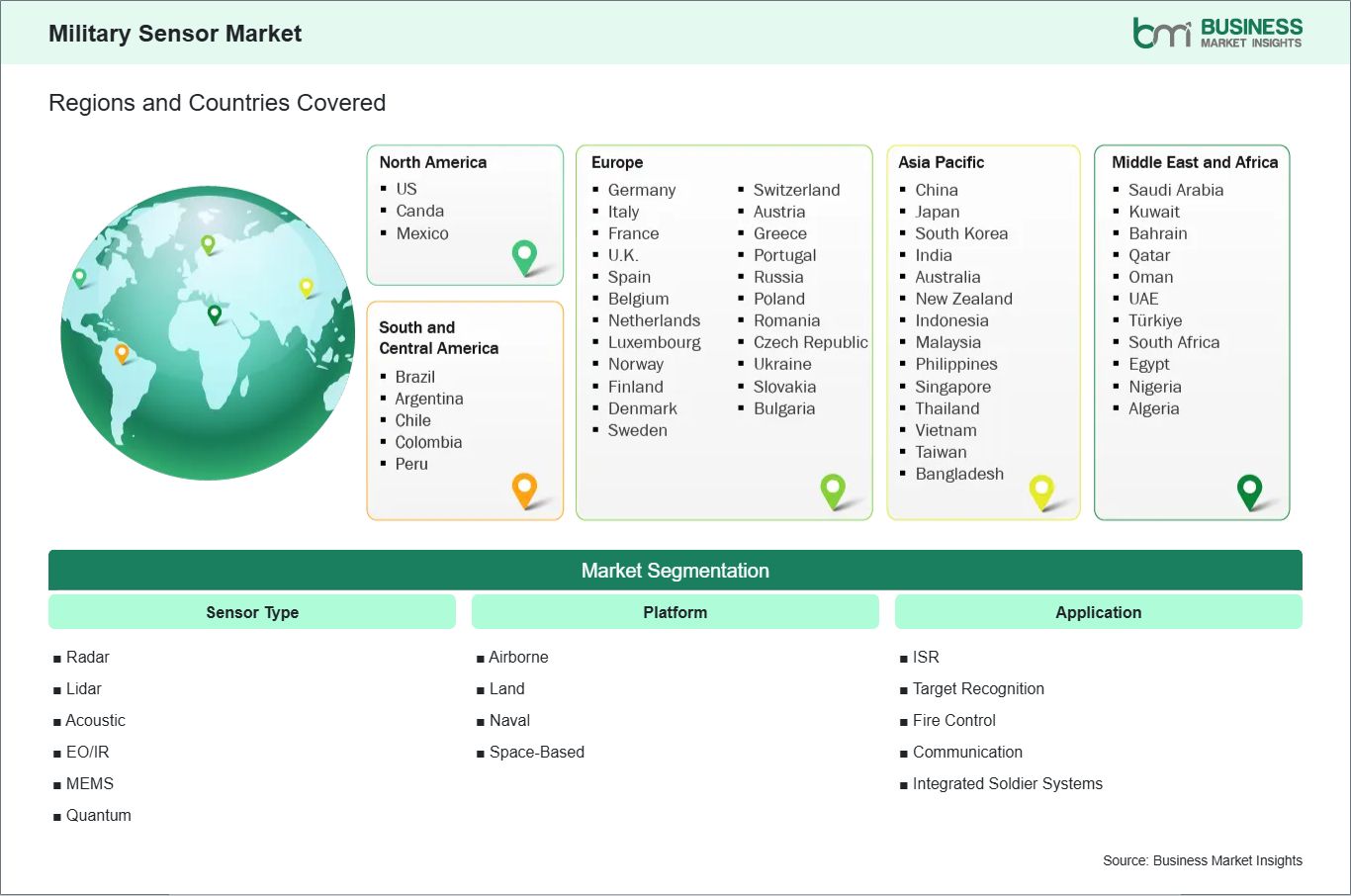

Military Sensor Market Segmentation

The military sensor market is segmented based on sensor type, platform, application, and technology, reflecting the growing demand for advanced sensing and surveillance solutions across modern defense operations.

By Sensor Type

- Radar Sensors: Advanced radar systems used for air defense, missile warning, threat detection, battlefield surveillance, target tracking, and navigation across airborne, naval, and land-based military platforms

- LiDAR Sensors: Laser-based sensing technologies used for terrain mapping, autonomous navigation, target recognition, obstacle detection, and precision-guided military operations

- Acoustic Sensors: Sensors designed for gunshot detection, submarine tracking, perimeter security, battlefield monitoring, and tactical threat identification in combat environments

- EO/IR Sensors: Electro-optical and infrared sensing systems used for thermal imaging, night vision, reconnaissance, surveillance, target acquisition, and intelligence gathering applications

- MEMS Sensors: Miniaturized micro-electromechanical sensors integrated into drones, missiles, navigation systems, and soldier equipment for motion sensing, inertial guidance, and positioning applications

- Quantum Sensors: Next-generation sensing technologies leveraging quantum mechanics for ultra-precise navigation, magnetic field detection, submarine detection, and GPS-independent military operations

By Platform

- Airborne: Sensors integrated into fighter aircraft, military helicopters, UAVs, airborne early warning systems, and surveillance drones

- Land: Ground-based sensing systems deployed in armored vehicles, military vehicles, border surveillance systems, and soldier modernization programs

- Naval: Sensors used in submarines, naval vessels, autonomous underwater vehicles, and maritime surveillance systems

- Space: Space-based sensors integrated into satellites and missile warning systems for strategic defense monitoring and global surveillance

By Application

- Intelligence, Surveillance, and Reconnaissance (ISR): Sensors used for real-time battlefield monitoring, intelligence gathering, and reconnaissance operations

- Target Recognition and Tracking: Advanced sensing systems supporting precision targeting, threat tracking, and missile guidance applications

- Navigation and Communication: Sensors integrated into navigation systems, GPS-denied environments, and secure battlefield communication networks

- Electronic Warfare: Sensors designed for signal interception, electromagnetic spectrum monitoring, and threat detection operations

- Combat Operations: Sensors supporting tactical engagement, autonomous weapon systems, and integrated combat missions

- Other Applications: Includes border security, disaster response, search and rescue, and training simulation systems

04

Market Forces

Military Sensor Market Drivers and Opportunities

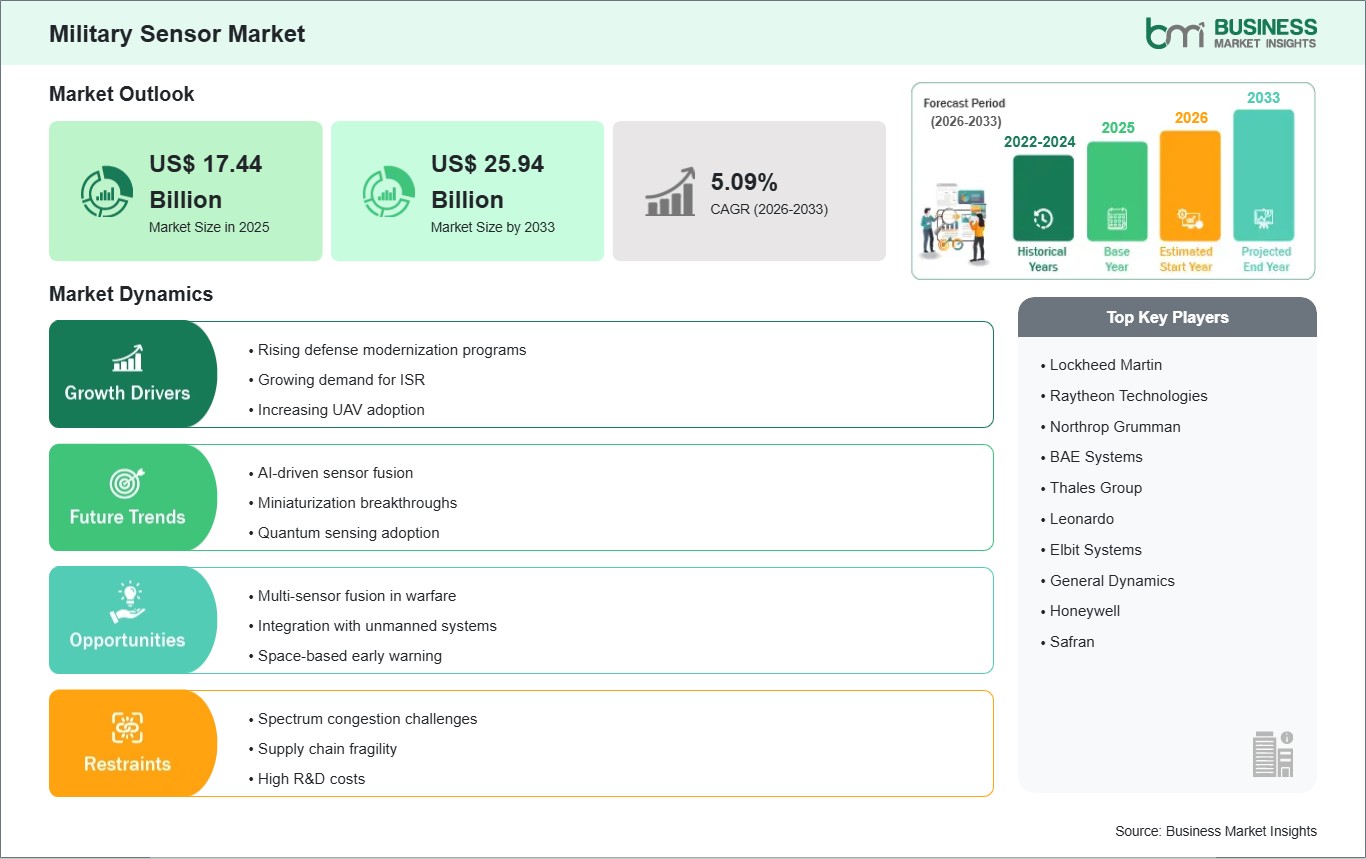

Rising Demand for Advanced Battlefield Awareness and ISR Capabilities

The military sensor market is witnessing significant growth due to the increasing need for advanced battlefield awareness, intelligence gathering, and real-time surveillance capabilities across defense operations. Modern military missions require highly accurate and reliable sensing systems capable of detecting threats, tracking enemy movements, and supporting strategic decision-making in complex combat environments. Military sensors are increasingly deployed across airborne, naval, land-based, and space defense systems to improve operational efficiency and mission effectiveness.

The growing adoption of unmanned systems, missile defense infrastructure, and network-centric warfare strategies is accelerating demand for high-performance sensing technologies. Governments worldwide are heavily investing in integrated ISR systems, border surveillance infrastructure, autonomous drones, and AI-powered battlefield management systems to strengthen national security and defense readiness. In addition, rising geopolitical tensions, territorial disputes, and asymmetric warfare threats are driving demand for next-generation military sensors capable of operating in electronic warfare and GPS-denied environments.

Expansion of AI-Enabled Sensor Fusion and Autonomous Defense Systems

Significant opportunities are emerging in the military sensor market through advancements in artificial intelligence, sensor fusion technologies, and autonomous defense systems. Defense organizations are increasingly focusing on connected battlefield ecosystems that integrate multiple sensors to provide real-time situational awareness and predictive threat analysis. AI-powered military sensors equipped with machine learning algorithms and edge computing capabilities are enabling improved target recognition, autonomous navigation, and enhanced battlefield coordination.

The growing deployment of autonomous drones, robotic combat vehicles, smart munitions, and space-based surveillance systems is creating new growth opportunities for defense electronics manufacturers and sensor developers. In addition, increasing investments in electronic warfare resilience, cyber-secure communication systems, and next-generation radar technologies are supporting the development of highly intelligent defense sensing platforms. Vendors focusing on miniaturized sensors, AI-enabled analytics, and multi-domain sensing integration are expected to gain a competitive advantage as military organizations continue to modernize defense infrastructure globally.

05

Size and Share Analysis

Military Sensor Market Size and Share Analysis

The Military Sensor Market is projected to grow from US$ 17.44 Billion in 2025 to US$ 25.94 Billion by 2033 , registering a CAGR of 5.09% from 2026 to 2033.

By sensor type, radar sensors account for a significant market share due to increasing deployment in air defense systems, missile tracking infrastructure, and battlefield surveillance applications. Image sensors are witnessing strong demand driven by growing adoption of electro-optical and infrared technologies in drones, armored vehicles, and surveillance systems. Sonar sensors continue to gain traction due to rising investments in naval modernization and underwater warfare capabilities.

By platform, the airborne segment dominates the market owing to increasing deployment of UAVs, airborne ISR systems, and next-generation fighter aircraft equipped with advanced sensing technologies. Land-based sensing systems maintain strong adoption across armored vehicles, border surveillance infrastructure, and tactical battlefield operations. Space-based sensors are expected to witness rapid growth due to rising investments in satellite surveillance, missile warning systems, and space defense initiatives.

By application, the ISR segment holds the largest market share due to increasing demand for real-time intelligence gathering, reconnaissance operations, and situational awareness across defense missions. Target recognition and tracking applications are experiencing significant growth driven by advancements in precision-guided weapon systems and AI-enabled battlefield analytics. Electronic warfare applications are also witnessing increasing adoption due to the growing importance of electromagnetic spectrum dominance in modern warfare.

07

Report Coverage

Military Sensor Market Report Coverage and Deliverables

The "Military Sensor market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

- Military sensor market size and forecast at global, regional, and country levels for all market segments covered under the scope

- Military sensor market trends, as well as drivers, restraints, and opportunities

- Military sensor market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the military sensor market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Military Sensor Market Geographic Insights

The military sensor market demonstrates diverse regional adoption patterns influenced by defense modernization programs, geopolitical developments, and increasing investments in advanced military electronics and surveillance systems.

North America holds a dominant position in the market due to high defense spending, advanced defense technology infrastructure, and continuous investments in next-generation sensing and surveillance systems. The United States continues to invest heavily in missile defense systems, ISR platforms, AI-enabled combat systems, and space-based surveillance technologies. Increasing deployment of advanced radar systems, electro-optical sensors, and electronic warfare technologies across military operations is further supporting market growth across the region. Canada is also expanding investments in border surveillance systems, Arctic defense infrastructure, and autonomous military technologies to strengthen national security capabilities.

Asia Pacific is witnessing substantial market growth driven by rising geopolitical tensions, military modernization initiatives, and increasing indigenous defense manufacturing activities. Countries such as China, India, Japan, and South Korea are heavily investing in advanced radar systems, missile guidance technologies, naval surveillance systems, and unmanned defense platforms. The region is increasingly focusing on AI-powered battlefield systems, integrated air defense infrastructure, and autonomous surveillance technologies to strengthen strategic defense preparedness. Rising investments in smart defense electronics, satellite surveillance systems, and electronic warfare capabilities are further accelerating market expansion across Asia Pacific.

Europe is also experiencing notable market growth due to increasing defense cooperation, rising investments in NATO defense programs, and modernization of military communication and surveillance systems. Meanwhile, Middle East and Africa countries are strengthening border security and missile defense capabilities, contributing to increasing adoption of military sensing technologies across the region.

10

Industry Activity

Recent Developments

The military sensor market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the military sensor market are:

- In May 2026, Northrop Grumman Corporation was awarded a U.S. Army contract for second phase development of its Improved Threat Detection System (ITDS). The award follows the Army’s early decision to choose the company’s discriminating technology demonstrated in successful first phase ITDS flight tests against competing systems. The ATHENA sensor in ITDS provides next-generation, multi-spectral 360-degree threat detection, significantly enhancing pilot situational awareness and aircraft survivability.

- In April 2026, Raytheon has delivered its second sensor to Lockheed Martin for the U.S. Space Force's Next-Generation Overhead Persistent Infrared (Next-Gen OPIR) Geosynchronous Earth Orbit (GEO) Block 0 satellite program. The satellites, commonly referred to as NGG, will provide enhanced missile warning and tracking to address evolving space-based threats.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

Stockholm International Peace Research Institute (SIPRI)

North Atlantic Treaty Organization (NATO)

International Institute for Strategic Studies (IISS)

S. Department of Defense (DoD)

Company Websites

Company Annual Reports

Company Investor Presentations