01

Market Summery

Executive Summary and Global Market Analysis

Military radar systems are advanced detection, tracking, surveillance, and targeting technologies designed to support defense and security operations across land, airborne, naval, and space-based platforms. These radar systems play a critical role in modern warfare by enabling real-time situational awareness, threat detection, missile guidance, air defense, border surveillance, navigation, and battlefield intelligence. Military radars operate across multiple frequency bands including HF, VHF, UHF, and multi-band architectures to support long-range surveillance, target acquisition, electronic warfare resilience, and secure military operations in highly contested environments.

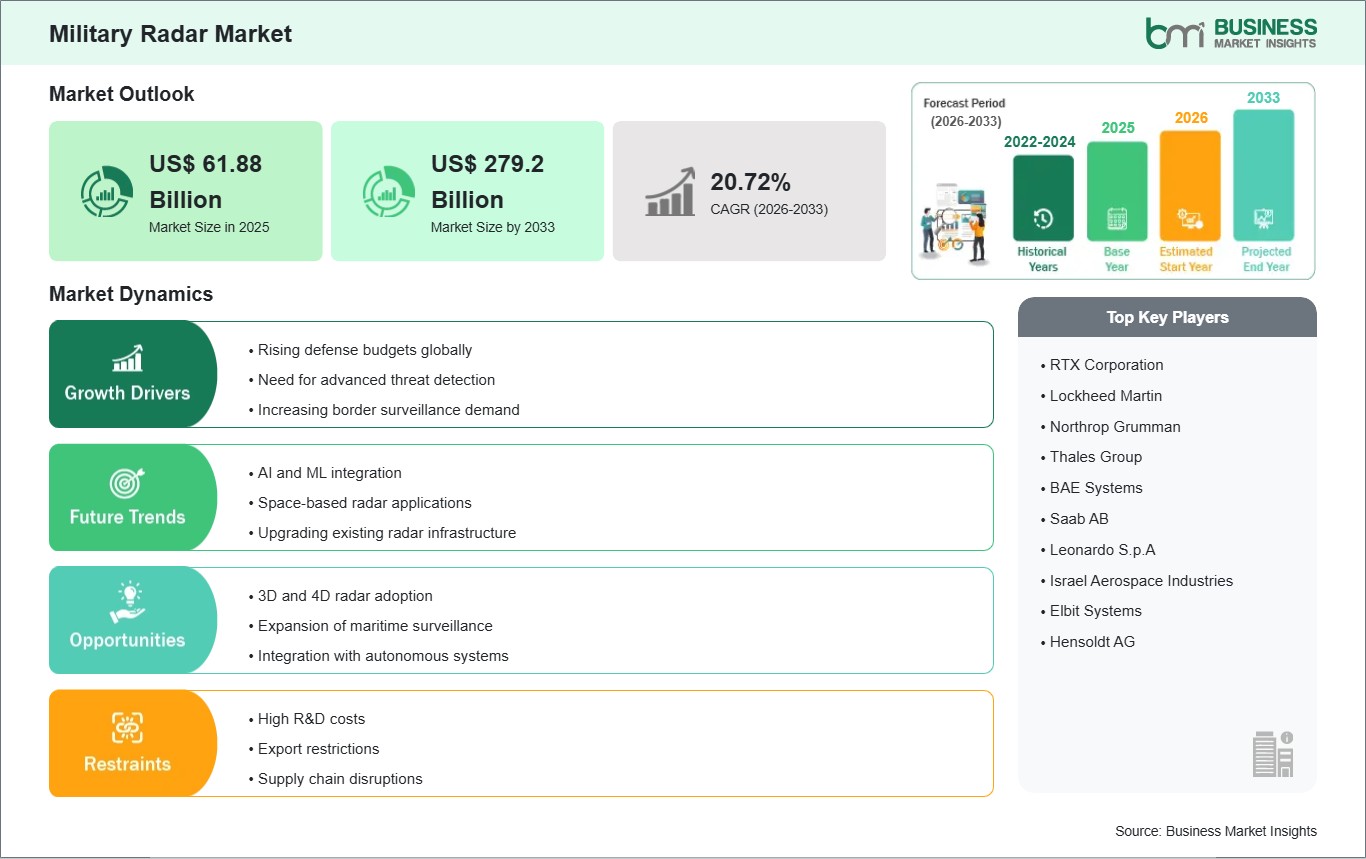

The market is experiencing strong growth due to rising global defense expenditures, increasing geopolitical tensions, and rapid modernization of military infrastructure worldwide. Governments are heavily investing in integrated air and missile defense systems, early warning capabilities, next-generation fighter aircraft, naval combat systems, and space-based surveillance networks. The increasing deployment of unmanned aerial systems, hypersonic weapons, and stealth technologies is further accelerating demand for advanced military radar systems capable of detecting low-observable and high-speed threats. In addition, the growing adoption of network-centric warfare and multi-domain operations is supporting the integration of AI-enabled and software-defined radar technologies across modern defense ecosystems.

However, market growth is restrained by several operational and technological challenges. Advanced military radar systems require substantial investment in research, development, testing, and deployment, making procurement expensive for budget-constrained defense agencies. Radar systems also face technical limitations associated with signal interference, spectrum congestion, electronic countermeasures, and harsh battlefield conditions. Furthermore, long defense procurement cycles, export control regulations, and dependence on highly specialized semiconductor and electronic components can create supply chain disruptions and deployment delays for manufacturers and defense organizations.

Despite these challenges, the market outlook remains positive due to continuous innovation in radar technologies and increasing investments in next-generation defense capabilities. Emerging opportunities are being created through the development of AESA radars, multi-function radar systems, cognitive radar technologies, and AI-powered threat detection platforms. The growing focus on integrated air defense systems, missile interception technologies, space surveillance programs, and electronic warfare resilience is expected to create substantial long-term demand for advanced military radars. Additionally, modernization programs across land, airborne, naval, and space defense platforms are accelerating the adoption of compact, high-frequency, and multi-band radar systems capable of supporting evolving military mission requirements.

03

Segment Analysis

Military Radar Market Segmentation

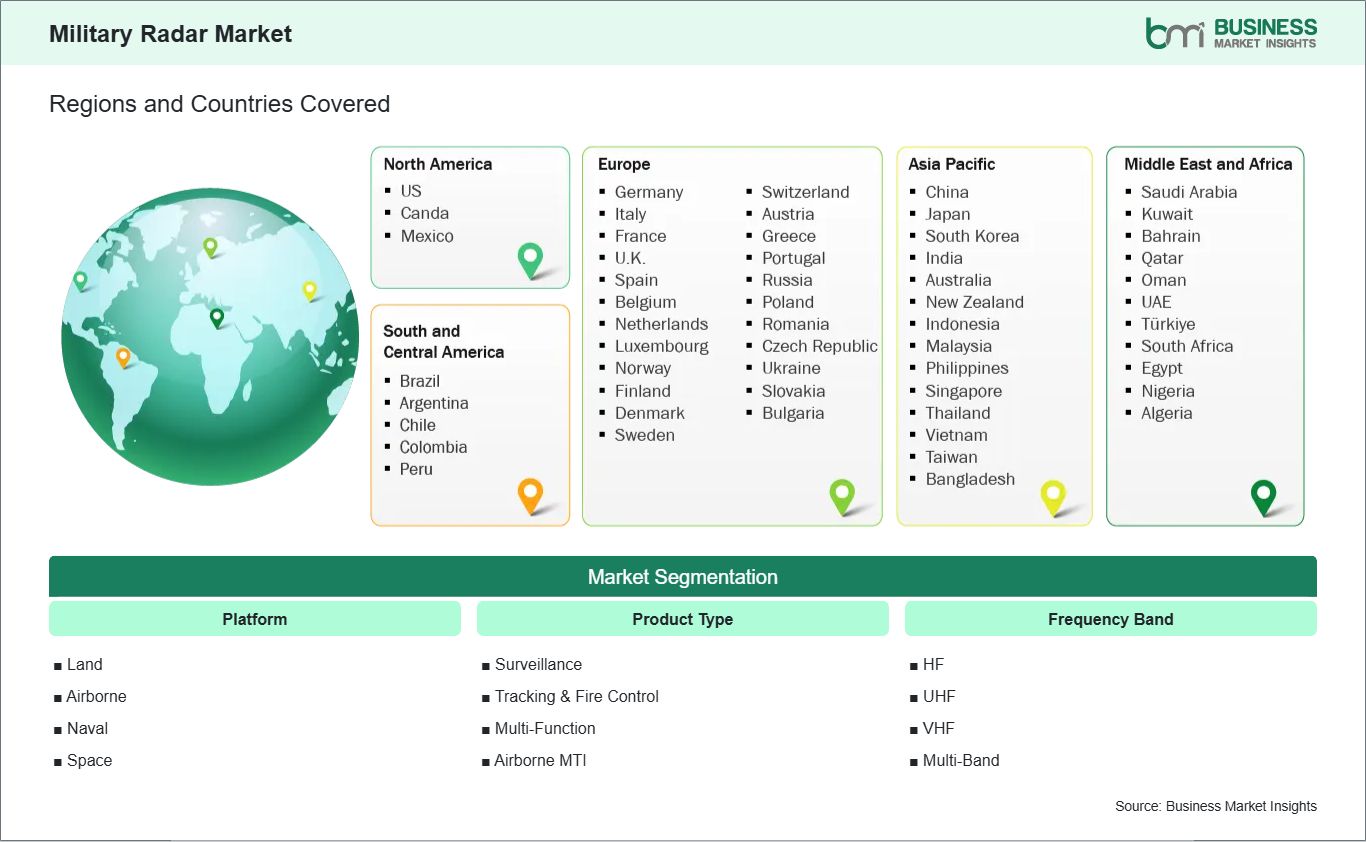

The military radar market is segmented based on platform, product type, and frequency band, reflecting the growing demand for advanced imaging and depth-sensing solutions across multiple applications.

By Platform

- Land: Ground-based radar systems used for border surveillance, air defense, battlefield monitoring, artillery detection, and missile tracking applications

- Airborne: Radar systems integrated into fighter aircraft, UAVs, surveillance aircraft, helicopters, and airborne early warning platforms for target detection and combat operations

- Naval: Radar technologies deployed across warships, submarines, aircraft carriers, and maritime patrol systems for navigation, surveillance, and naval combat operations

- Space: Space-based radar systems supporting satellite surveillance, missile warning, Earth observation, and strategic defense monitoring capabilities

By Product Type

- Surveillance: Long-range radar systems designed for airspace monitoring, border security, maritime surveillance, and early warning operations

- Tracking & Fire Control: Precision radar systems used for target tracking, missile guidance, weapons control, and air defense interception capabilities

- Multi-Function: Advanced radar systems capable of simultaneously performing surveillance, tracking, communication, navigation, and electronic warfare operations

- Airborne MTI: Moving Target Indicator radar systems integrated into airborne platforms for detecting and tracking moving ground and maritime targets

By Frequency Band

- HF: Supports long-range over-the-horizon radar communication and strategic surveillance operations across large geographic areas

- VHF: Enables detection of stealth aircraft, long-range surveillance, and battlefield communication support applications

- UHF: Widely used in military air defense systems, tracking radars, and secure tactical radar communication infrastructure

- Multi-Band: Advanced radar architectures capable of operating across multiple frequencies for enhanced detection accuracy, anti-jamming capability, and mission flexibility

04

Market Forces

Military Radar Market Drivers and Opportunities

Increasing Demand for Integrated Air Defense and Advanced Surveillance Capabilities

The military radar market is witnessing significant growth due to rising global demand for integrated air defense systems and advanced battlefield surveillance technologies. Governments worldwide are strengthening national defense capabilities in response to evolving security threats, increasing border disputes, and rapid advancements in missile and stealth technologies. Modern military operations require highly reliable radar systems capable of delivering real-time situational awareness, threat identification, and precision targeting across multiple operational environments.

The growing deployment of hypersonic missiles, stealth aircraft, drones, and autonomous combat systems is increasing the need for next-generation radar technologies with improved detection accuracy and electronic warfare resilience. Military organizations are increasingly adopting AESA radars, multi-function radar systems, and AI-enabled surveillance technologies to enhance operational effectiveness and support network-centric warfare strategies. In addition, rising investments in missile defense systems, airborne early warning platforms, and integrated command-and-control infrastructure are accelerating demand for advanced radar systems across land, air, naval, and space defense operations.

Expansion of Space-Based Surveillance and Multi-Band Radar Technologies

Significant opportunities are emerging in the military radar market through the expansion of space-based defense surveillance systems and advanced multi-band radar technologies. Governments are increasingly investing in satellite-based intelligence, missile warning systems, and space situational awareness programs to strengthen strategic defense capabilities and monitor evolving global threats. This trend is creating substantial demand for advanced radar systems capable of supporting long-range detection, secure tracking, and high-speed data processing across defense communication networks.

The increasing focus on electronic warfare preparedness and anti-jamming technologies is also accelerating adoption of multi-band radar systems capable of operating effectively in contested electromagnetic environments. Emerging technologies such as cognitive radar systems, AI-driven target recognition, and software-defined radar architectures are creating new growth opportunities for defense electronics manufacturers. Furthermore, modernization of naval fleets, airborne ISR platforms, and integrated battlefield management systems is supporting the deployment of compact, lightweight, and high-performance radar systems. Vendors focusing on electronically resilient, multi-domain, and AI-enabled radar solutions are expected to gain a competitive advantage as defense organizations continue to modernize military surveillance and targeting infrastructure globally.

05

Size and Share Analysis

Military Radar Market Size and Share Analysis

The Military Radar Market is projected to grow from US$ 61.88 Billion in 2025 to US$ 279.2 Billion by 2033 , registering a CAGR of 20.72% from 2026 to 2033.

By platform, the airborne segment accounts for a significant market share due to increasing deployment of fighter aircraft, UAVs, airborne early warning systems, and ISR platforms equipped with advanced radar technologies. Naval radar systems are also witnessing strong demand driven by modernization programs focused on maritime surveillance, naval combat systems, and missile defense capabilities. Land-based radar systems continue to dominate border security, battlefield monitoring, and integrated air defense operations, while space-based radar platforms are gaining traction due to rising investments in satellite surveillance and strategic missile warning systems.

By product type, surveillance radars hold a substantial market share owing to their widespread deployment across air defense, border monitoring, and maritime surveillance applications. Tracking & fire control radar systems are experiencing strong growth due to increasing demand for precision targeting and missile guidance technologies. Multi-function radars are gaining popularity across integrated combat systems because of their ability to perform multiple operational tasks simultaneously. Airborne MTI radar systems continue to witness rising adoption across airborne ISR missions and moving target detection operations.

By frequency band, the UHF segment accounts for a major share due to its extensive use in military air defense and target tracking applications. VHF radar systems are witnessing increased deployment for stealth target detection and long-range surveillance operations. HF systems remain important for over-the-horizon surveillance and strategic monitoring capabilities, while multi-band radar architectures are experiencing rapid growth driven by demand for enhanced electronic protection, mission flexibility, and advanced battlefield performance.

07

Report Coverage

Military Radar Market Report Coverage and Deliverables

The "Military Radar market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

- Military radar market size and forecast at global, regional, and country levels for all market segments covered under the scope

- Military radar market trends, as well as drivers, restraints, and opportunities

- Military radar market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the military radar market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Military Radar Market Geographic Insights

The Military Radar market shows diverse regional adoption patterns influenced by by defense modernization initiatives, geopolitical developments, and increasing demand for secure positioning and guidance technologies across military operations.

North America holds a dominant position in the market due to substantial defense budgets, advanced military technology infrastructure, and the presence of major defense electronics manufacturers. The United States continues to invest heavily in integrated air and missile defense systems, space-based surveillance programs, next-generation fighter aircraft, and electronic warfare capabilities. Increasing deployment of AI-enabled radar systems, naval combat technologies, and missile interception platforms is further driving market growth across the region. Canada is also strengthening radar modernization initiatives to improve Arctic surveillance and national defense preparedness.

Asia Pacific is witnessing significant market expansion driven by rising geopolitical tensions, increasing military modernization programs, and growing investments in indigenous defense manufacturing capabilities. Countries such as China, India, Japan, and South Korea are actively deploying advanced radar systems across air defense networks, naval fleets, and airborne surveillance platforms to strengthen national security capabilities. The region is increasingly focusing on integrated missile defense systems, space surveillance infrastructure, and next-generation combat aircraft equipped with advanced radar technologies. Rising investments in border security, UAV surveillance systems, and naval modernization programs are further supporting market growth across Asia Pacific.

Both regions continue to contribute significantly to the expansion of the military radar market through ongoing investments in advanced surveillance infrastructure, integrated defense systems, and next-generation electronic warfare technologies.

10

Industry Activity

Recent Developments

The military radar market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the military radar market are:

- In May 2026, Raytheon, an RTX (NYSE: RTX) business, has been awarded a contract from the Office of Naval Research to further develop advanced radar software for next-generation naval radars.

- In December 2025, The Danish Acquisition and Logistics Organization (DALO) has selected Lockheed Martin’s TPY-4 next-generation ground-based air surveillance radar to enhance Denmark’s long-range air defense capabilities. Denmark is the fifth nation to adopt the system, joining a growing group of NATO partners integrating advanced radar technology.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

Stockholm International Peace Research Institute (SIPRI)

North Atlantic Treaty Organization (NATO)

International Institute for Strategic Studies (IISS)

S. Department of Defense (DoD)

Company Websites

Company Annual Reports

Company Investor Presentations