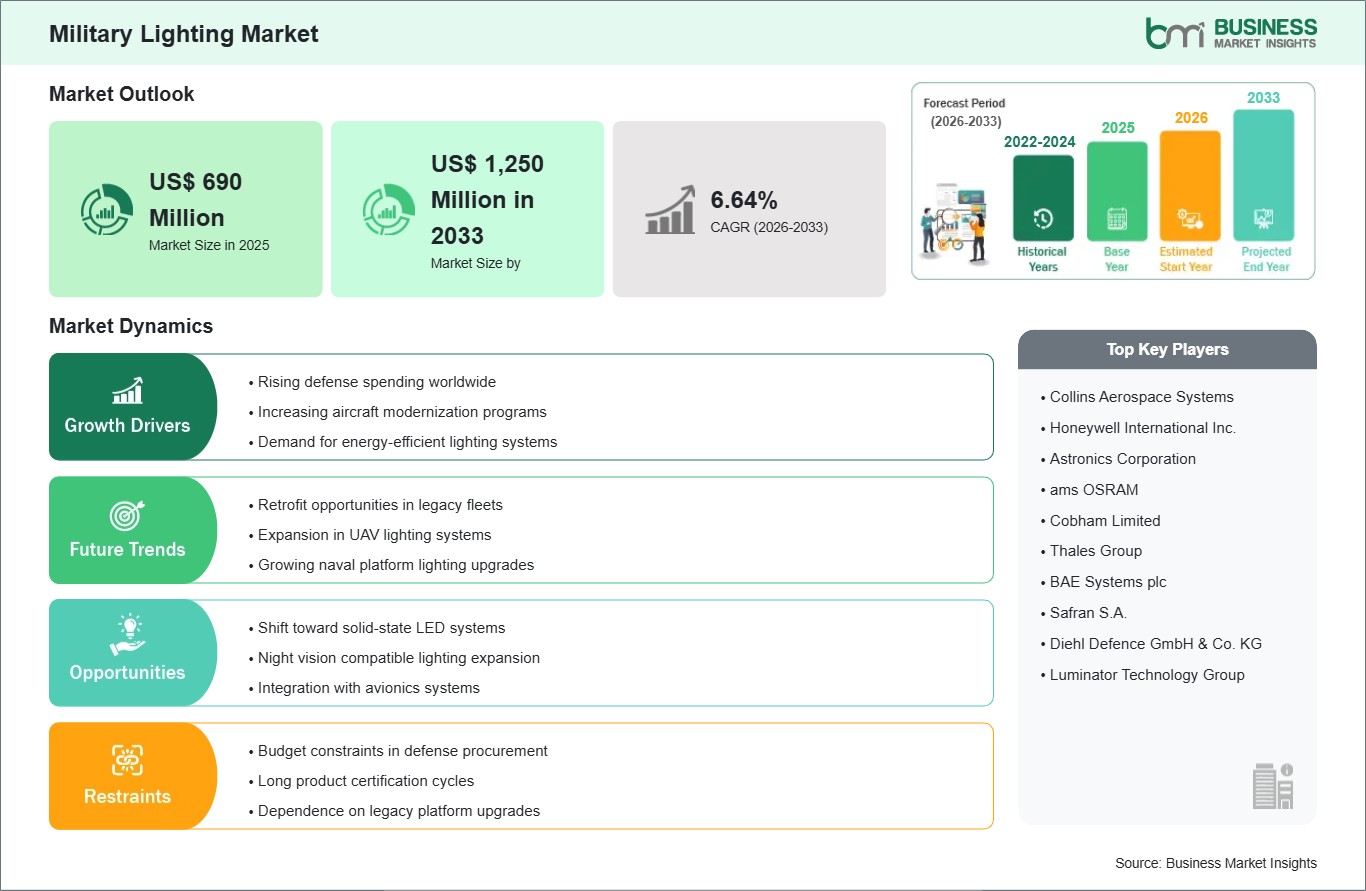

The Military Lighting market size is expected to reach US$ 1,250 Million by 2033 from US$ 690 Million in 2025. The market is estimated to record a CAGR of 6.64% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Military lighting systems encompass illumination, signaling, and visibility-control solutions engineered for defense platforms and mission environments. These systems support navigation, cockpit visibility, perimeter security, convoy movement, and covert operations under demanding operational conditions. Performance requirements typically emphasize rugged construction, spectral control, low power draw, and compatibility with mission electronics. As a result, the sector sits at the intersection of defense modernization, platform survivability, and mission-readiness planning.

Procurement momentum is being shaped by the shift toward lighter, longer-lasting, and lower-signature lighting architectures across defense fleets. Armed forces are refining requirements for night operations, maintenance efficiency, and environmental resilience, which is strengthening the case for upgraded lighting assemblies. Retrofit programs also contribute to deployment, particularly where legacy fleets require improved reliability without extensive structural redesign. This operating context sustains a measured expansion path for the market.

Platform demand remains differentiated by operating environment and mission profile. Airborne applications prioritize weight, vibration tolerance, and cockpit readability, while land systems require durability across tactical mobility and field maintenance scenarios. Naval deployments place greater emphasis on corrosion resistance, deck safety, and signaling consistency. On the end-user side, ground forces represent a broad utilization base, whereas marine and airborne users often require more specialized lighting configurations and certification pathways.

Technology transition within this sector is moving beyond conventional illumination formats toward solutions that deliver tighter control over brightness, heat, and spectral performance. LED systems continue to set the baseline for efficiency and service life, while OLED, micro LED, and tritium-based configurations address specialized visibility and persistence requirements. This evolution is encouraging suppliers to refine modular designs, platform integration methods, and maintenance characteristics rather than competing solely on brightness output.

Competition in the market is centered on qualification experience, platform compatibility, manufacturing consistency, and the ability to support long defense program cycles. Suppliers that align product engineering with mission-specific standards are better positioned in both retrofit and new-platform opportunities. Procurement decisions also reflect sustainment considerations, including replacement intervals, logistics simplicity, and interoperability with broader onboard systems. These factors keep the competitive landscape technically demanding and operationally focused.

Military Lighting Market - Strategic Insights:

Get more information on this report

Military Lighting Market Segmentation Analysis:

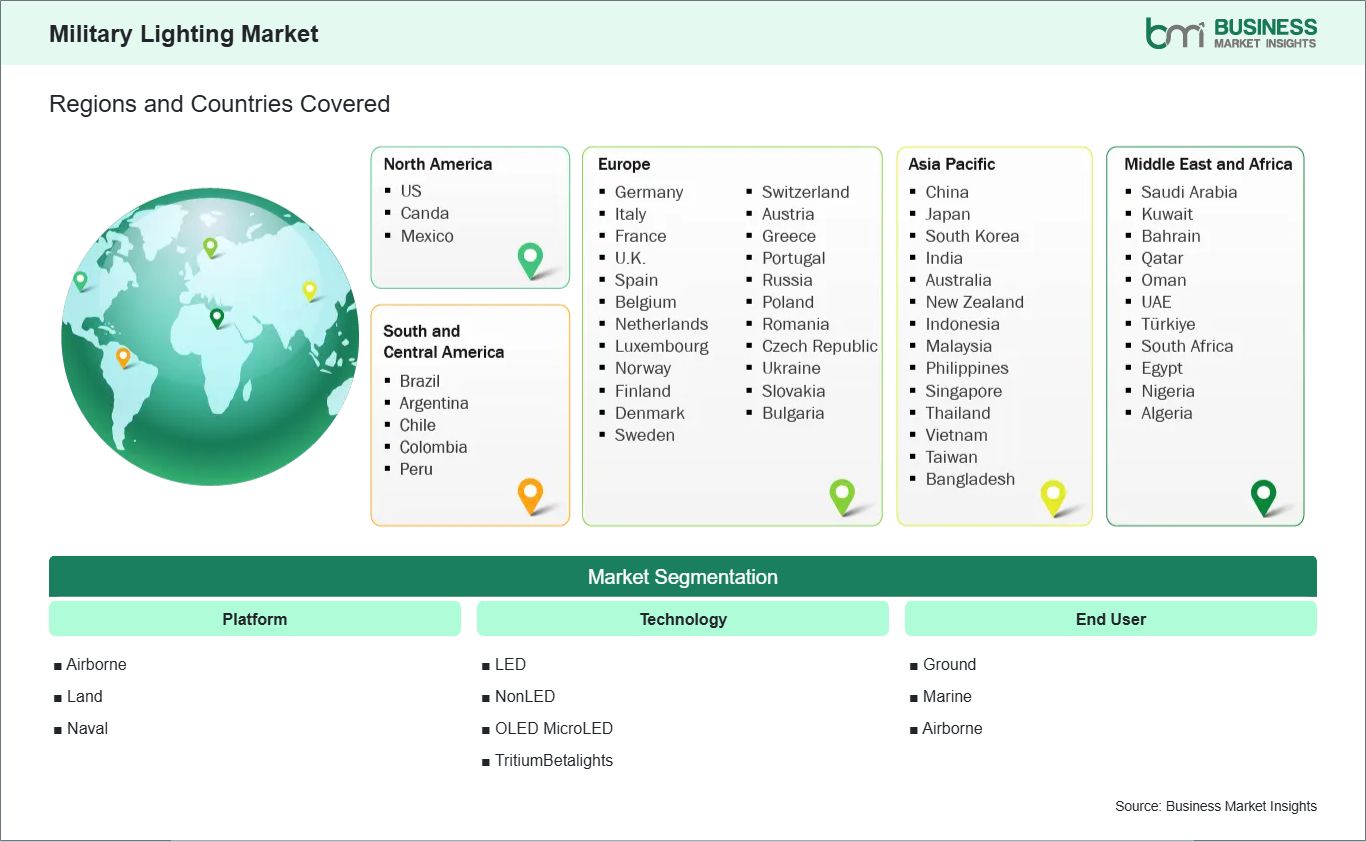

The Military Lighting market is segmented by platform, technology, and end user. Each category reflects distinct performance needs across defense operating environments.

By Platform

Airborne: Requires lightweight assemblies with strict visibility and cockpit integration standards

Land: Prioritizes durability, concealment support, and field-serviceable lighting configurations

Naval: Emphasizes corrosion resistance and dependable deck and signaling performance

Tritium Betalights: Enables passive illumination where persistent low-light visibility is required

By End User

Ground: Uses tactical, perimeter, and vehicle lighting across diverse mission settings

Marine: Depends on signaling, navigation, and deck visibility under harsh exposure

Airborne: Favors certified solutions for cockpit, cabin, and external mission lighting

Military Lighting Market Drivers and Opportunities:

Platform Modernization and Night Operations Readiness

Fleet modernization programs are increasingly scrutiny on lighting performance across aircraft, land vehicles, naval vessels, and fixed defense infrastructure. Mission planners require systems that enhance visibility control, reduce maintenance burdens, and support low-signature operations in contested settings. That requirement is to accelerate the replacement of aging illumination assemblies with more resilient alternatives. Procurement therefore increasingly favors lighting solutions aligned with night-readiness, platform integration, and operational durability objectives.

The effect of this transition extends beyond illumination hardware into maintenance planning, training efficiency, and platform survivability. Lighting upgrades can improve equipment availability by reducing replacement frequency and simplifying service intervals. They also strengthen mission execution where clear signaling and controlled visibility remain critical. This relevance keeps military lighting tied closely to broader defense readiness programs, particularly where legacy fleets must remain operationally credible over extended service lives.

Advanced Solid-State and Low-Signature Lighting Integration

Defense lighting design is moving toward compact solid-state architectures that offer better thermal control, longer service intervals, and improved spectral management. This shift opens opportunities for LED, OLED, micro-LED, and tritium-based configurations in displays, vehicle lighting, cockpit systems, and covert-use cases. Innovation is particularly relevant where operators need precise luminance behavior without compromising mission concealment. These use cases are expanding the technical scope of the sector beyond conventional illumination replacement.

Looking ahead, opportunity will broaden as defense programs seek modular lighting platforms that can be adapted across multiple system classes. Suppliers able to support qualifications, integration, and sustainment across airborne, naval, and land requirements can widen their addressable footprint. The resulting expansion can improve interoperability, streamline maintenance planning, and reinforce mission effectiveness. For industry, this creates room for differentiated offerings built around specialization rather than standard illumination performance alone.

Military Lighting Market Size and Share Analysis:

The Military Lighting market size is expected to reach US$ 1,250 Million by 2033 from US$ 690 Million in 2025. The market is estimated to record a CAGR of 6.64% from 2026 to 2033. This trajectory indicates a steady procurement environment shaped by modernization priorities, platform upgrades, and the need for more reliable lighting systems across defense operations.

Among platform categories, land applications hold a central position because they span tactical vehicles, perimeter systems, transport units, and field infrastructure. On the technology side, LED solutions maintain the strongest share profile due to service-life, power efficiency, and flexibility integration. Non-LED formats continue to serve installed bases, while OLED, micro-LED, and tritium-based options strengthen specialized positioning in mission-specific environments.

From an end-user perspective, ground forces account for the widest range of deployment scenarios, covering mobility, signaling, area illumination, and operational safety requirements. Marine applications maintain importance where navigation and deck conditions require dependable visibility performance. Airborne use remains technically specialized, with emphasis on cockpit readability, external signaling, and compliance with stringent platform standards. These distinctions shape share distribution across the broader market.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Collins Aerospace Systems

Honeywell International Inc.

Astronics Corporation

ams OSRAM

Cobham Limited

Thales Group

BAE Systems plc

Safran S.A.

Diehl Defence GmbH & Co. KG

Luminator Technology Group

Get more information on this report

Military Lighting Market Report Coverage and Deliverables:

The " Military Lighting Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Military Lighting Market Geographic Insights:

The Military Lighting market shows diverse regional adoption patterns influenced by defense modernization priorities, platform mix, and mission-specific operating requirements. Across the global landscape, procurement behavior reflects a move toward efficient, rugged, and low-signature lighting systems that can support readiness without adding avoidable maintenance burden. Demand is also shaped by whether programs focus on new platforms, legacy fleet upgrades, or fixed defense infrastructure requiring more resilient illumination and signaling capabilities.

North America remains a structurally important market because defense programs in the region emphasize system reliability, qualification discipline, and sustained platform support. Airborne, land, and tactical soldier applications all contribute to procurement depth, especially where night operations and compatibility with advanced mission systems are central requirements. Retrofit activity also supports demand, as established fleets continue receiving upgrades intended to improve service life, reduce upkeep complexity, and strengthen operational consistency.

Asia Pacific presents a different expansion pattern, shaped by defense industrial development, broader procurement programs, and the rising importance of indigenous manufacturing capability. The region shows active interest in solutions that balance durability, integration flexibility, and long-term supportability across mixed fleets. Land and maritime requirements are especially prominent in several markets, while airborne programs create demand for more specialized lighting architectures. This combination gives the region a wide application base and evolving supplier landscape.

Europe sustains demand through platform sustainment, technical standardization, and continued interest in mission-efficient upgrades across established defense fleets. Emerging markets in the Middle East, Africa, and South and Central America add a separate layer of opportunity, often centered on fleet readiness, perimeter infrastructure, and modernization of installed systems. In these regions, procurement priorities can differ sharply by mission profile, yet the need for dependable lighting performance continues to support measured industry development.

Get more information on this report

Military Lighting Market Research Report Guidance:

The report includes qualitative and quantitative data in the market across platforms, technology, and end user and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Industrial Boiler market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover market segments by platform, technology, and end user and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Military Lighting Market News and Key Development:

Recent developments reflect sustained defense interest in advanced low-power and high-clarity lighting technologies. The updates below are listed in reverse chronological order and highlight relevant activity across the sector.

In Jan 2025, Bell Textron Inc. has chosen Honeywell Aerospaces LED Landing Search Light for use in the U.S. Armys MV-75 Future Long-Range Assault Aircraft. The landing searchlight is a high-intensity system designed to combine multiple functions into a single unit, specifically developed to reduce pilot workload during complex maneuvers. The LED lighting system has been tailored to the MV-75 FLRAA mission profile through advanced optical design, thermal management, and environmental protection. These enhancements aim to deliver high performance while also lowering overall aircraft weight and long-term operating costs.

In April 2025, STG Aerospace, a Heads-Up Technologies Company, is unveiling its newest innovation, the eco everything's concept, at the Aircraft Interiors Expo (AIX) 2025 in Hamburg, Germany. Building on the success of the saf-Tglo eco E1, the world's first sustainable emergency floor path marking system introduced at AIX 2024, STG Aerospace is expanding these principles across its photoluminescent range by the end of 2025, making eco-friendly solutions available to all customers.

Key Sources Referred:

World Bank -Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Military Lighting Market

Collins Aerospace Systems

Honeywell International Inc.

Astronics Corporation

ams OSRAM

Cobham Limited

Thales Group

BAE Systems plc

Safran S.A.

Diehl Defence GmbH & Co. KG

Luminator Technology Group

Frequently Asked Questions

How big is the Military Lighting Market?

The Military Lighting Market is valued at US$ 690 Million in 2025, it is projected to reach US$ 1,250 Million by 2033.

What is the CAGR for Military Lighting Market by (2026 - 2033)?

As per our report Military Lighting Market, the market size is valued at US$ 690 Million in 2025, projecting it to reach US$ 1,250 Million by 2033. This translates to a CAGR of approximately 6.64% during the forecast period.

What segments are covered in this report?

The Military Lighting Market report typically cover these key segments-

What is the historic period, base year, and forecast period taken for Military Lighting Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Military Lighting Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Military Lighting Market?

The Military Lighting Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Collins Aerospace Systems

Honeywell International Inc.

Astronics Corporation

ams OSRAM

Cobham Limited

Thales Group

BAE Systems plc

Safran S.A.

Diehl Defence GmbH & Co. KG

Luminator Technology Group

Who should buy this report?

The Military Lighting Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Military Lighting Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Military Lighting Market

Get Free Sample For Military Lighting Market