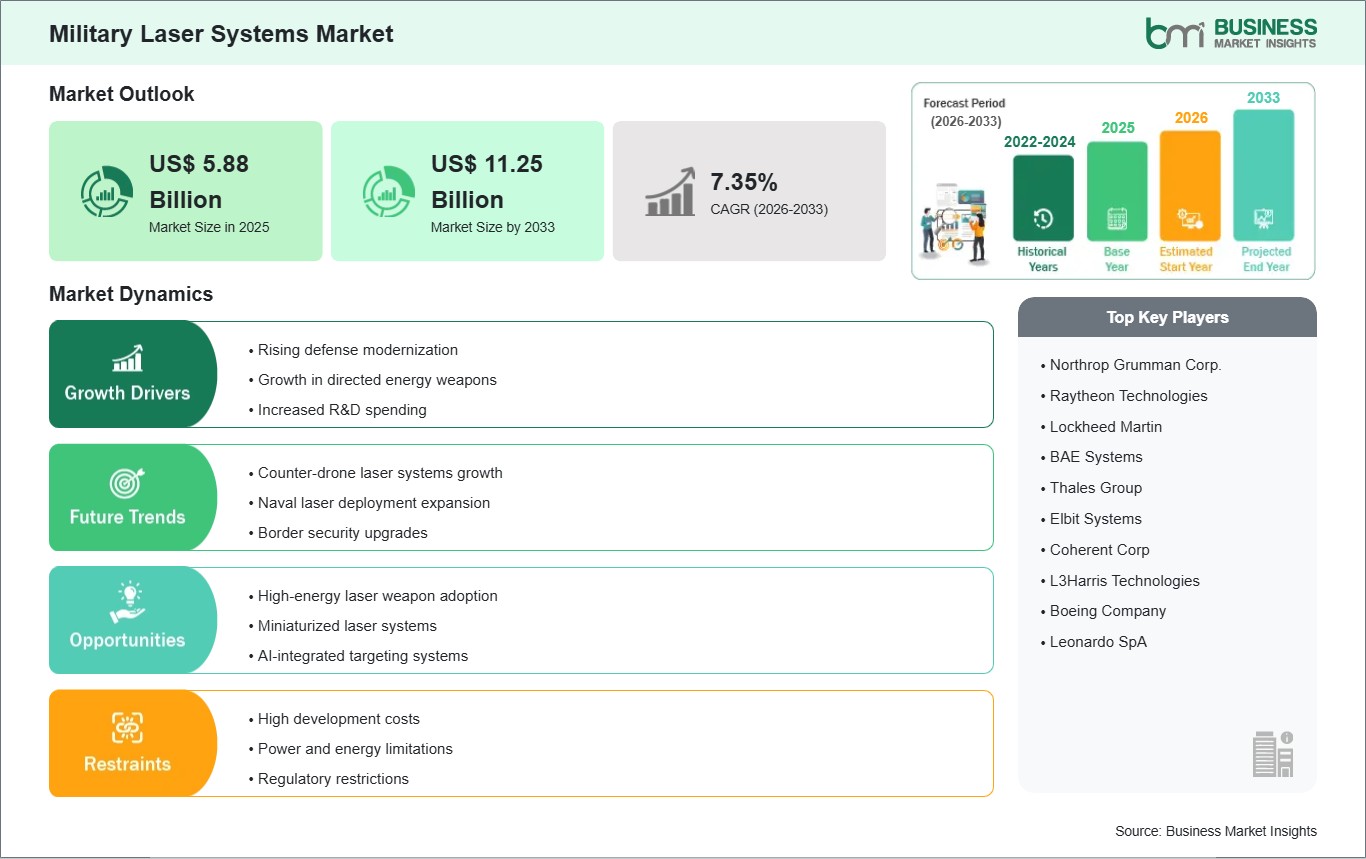

The Military Laser Systems market size is expected to reach US$ 11.25 Billion by 2033 from US$ 5.88 Billion in 2025. The market is estimated to record a CAGR of 7.35% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Military laser systems comprise directed-energy weapons and non-weapon laser technologies used for targeting, ranging, sensing, navigation, and threat engagement across defense missions. These systems convert concentrated light into precise operational effects, enabling armed forces to perform detection, designation, tracking, and interception tasks with greater control. Their role spans both combat and support environments, linking battlefield awareness with strike accuracy.

Procurement momentum reflects the need for faster response against drones, rockets, optical threats, and contested surveillance conditions. Defense planners are prioritizing systems that reduce collateral exposure, improve aiming precision, and strengthen layered protection across mobile and fixed installations. This shift is also supported by broader modernization programs that favor compact, software-integrated, and mission-adaptable architectures.

By type, weapons systems draw attention for counter-unmanned and air-defense roles, while non-weapons systems remain embedded in daily military operations through laser rangefinders, LiDAR, designators, and gyros. Platform distribution is equally broad, with land systems supporting maneuver units, airborne systems enabling precision engagement, naval platforms enhancing layered defense, and space-based concepts attracting strategic interest.

Technology development is moving toward improved beam quality, thermal management, compact power integration, and scalable output across solid-state, fiber, semiconductor, gas, liquid, and free-electron formats. Solid-state and fiber architectures remain central to current deployment pathways because they align with ruggedization and platform integration needs. At the same time, sensing and designation functions continue to benefit from miniaturization and higher processing efficiency.

Competitive conditions are shaped by defense primes, subsystem specialists, and laser technology developers pursuing program wins, demonstrations, and platform-specific integration pathways. The market remains technically demanding, with procurement decisions influenced by reliability, power availability, maintenance practicality, and doctrinal fit. As operational testing expands, differentiation is increasingly tied to mission endurance, control software maturity, and adaptability across multiple defense scenarios.

Military Laser Systems Market - Strategic Insights:

Get more information on this report

Military Laser Systems Market Segmentation Analysis:

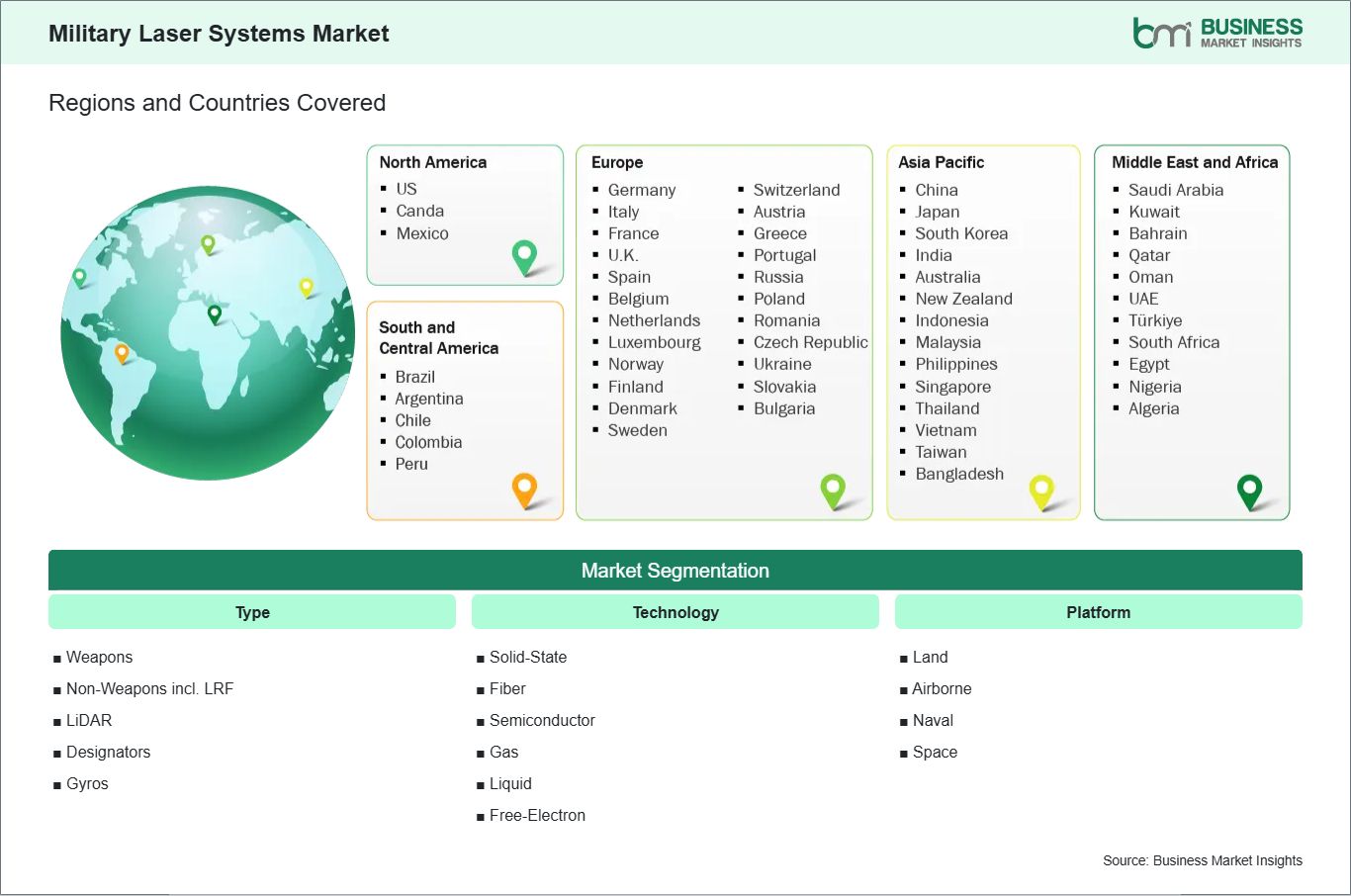

The Military Laser Systems market is segmented by Type, Technology, and Platform. Each category reflects distinct operational priorities, integration pathways, and mission requirements.

By Type

Weapons : Prioritized for counter-drone, missile defense, and tactical air defense missions

Non-Weapons incl. LRF, LiDAR, Designators, Gyros : Embedded across targeting, sensing, navigation, and reconnaissance workflows

By Technology

Solid-State : Favored for compact design and robust field integration

Fiber : Selected for beam quality, efficiency, and modular scaling

Semiconductor : Supports compact subsystems and specialized targeting functions

Gas : Retains relevance in selected high-energy defense applications

Liquid : Evaluated for thermal handling in advanced configurations

Free-Electron : Explored for high-power defense concepts and future naval missions

By Platform

Land : Anchors mobile air defense, surveillance, and targeting operations

Airborne : Extends precision engagement and electro-optical mission support

Naval : Strengthens layered ship defense and maritime tracking capability

Space : Represents an emerging frontier for strategic sensing concepts

Military Laser Systems Market Drivers and Opportunities:

Rising Requirement for Precision Counter-Drone and Layered Air Defense

The spread of low-cost drones, loitering threats, and fast aerial targets has intensified demand for precise interception tools. Military planners need systems that engage rapidly, limit collateral effects, and complement missile-based defenses across layered architectures. Laser weapons align with this need by offering controlled energy delivery, repeatable targeting, and flexible deployment across land and naval formations facing persistent aerial pressure.

This requirement is reshaping acquisition priorities, test programs, and platform integration strategies across major defense budgets. Its relevance extends beyond frontline combat, influencing base protection, convoy security, and maritime screening missions. As armed forces refine doctrines for distributed operations, military laser systems gain stronger relevance as responsive tools that support sustained defensive coverage under evolving threat conditions.

Expansion of Multi-Function Non-Weapon Laser Architectures

Defense modernization is widening the role of non-weapon laser systems that support ranging, designation, navigation, terrain mapping, and sensor fusion. Innovation in compact optics, processing, and beam control is enabling these functions to serve across manned platforms, unmanned systems, and networked mission environments. LiDAR-enabled awareness, designator precision, and gyro-supported stabilization illustrate how utility is extending beyond traditional targeting roles.

Future scope centers on deeper integration with autonomous systems, battlefield networking, and mission-specific payload packages across multiple domains. This expansion can improve navigation resilience, target handoff efficiency, and reconnaissance fidelity in contested environments. As defense forces seek broader functionality from each installed subsystem, non-weapon laser architectures create a wider opportunity base for this sector.

Military Laser Systems Market Size and Share Analysis:

The Military Laser Systems market size is expected to reach US$ 11.25 Billion by 2033 from US$ 5.88 Billion in 2025. The market is estimated to record a CAGR of 7.35% from 2026 to 2033. This trajectory reflects stronger defense emphasis on precision engagement, advanced sensing, and platform-ready electro-optical capabilities that can support both combat and mission-support requirements.

From a segment perspective, non-weapon systems maintain broad operational relevance because rangefinding, designation, navigation, and sensing functions are continuously embedded across defense workflows. Among technologies, solid-state and fiber formats hold a favorable position due to integration practicality, compactness, and efficiency characteristics. On the platform side, land-based deployment remains central because it aligns with maneuver support and mobile protection requirements.

Application leadership is shaped by counter-unmanned defense, target designation, surveillance support, and precision guidance assistance across operational theaters. Land and airborne roles remain prominent because they combine tactical responsiveness with wide mission utility. Naval applications also strengthen the overall market profile as fleets pursue layered protection and optical tracking functions under increasingly contested maritime conditions.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Northrop Grumman Corp.

Raytheon Technologies

Lockheed Martin

BAE Systems

Thales Group

Elbit Systems

Coherent Corp

L3Harris Technologies

Boeing Company

Leonardo SpA

Get more information on this report

Military Laser Systems Market Report Coverage and Deliverables:

The " Military Laser Systems Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas::

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Military Laser Systems Market Geographic Insights:

The Military Laser Systems market shows diverse regional adoption patterns influenced by defense modernization priorities, threat exposure, procurement cycles, and platform integration readiness. Across the global landscape, armed forces are balancing immediate tactical requirements with longer-term investment in directed-energy weapons and non-weapon laser subsystems. This creates a market structure in which sensing, designation, and protection needs evolve differently by theater and operational doctrine.

North America retains a strong position because its defense ecosystem supports experimentation, system integration, and rapid technology transition across land, naval, and airborne programs. Procurement activity is reinforced by counter-drone requirements, layered air defense planning, and sustained interest in scalable high-energy solutions. The region also benefits from an established industrial base capable of advancing optics, beam control, power management, and software-defined mission systems.

Asia Pacific presents a broad opportunity set shaped by rising security competition, military technology indigenization, and increasing emphasis on surveillance and precision engagement tools. Regional demand extends beyond weaponized systems into rangefinding, designation, and navigation support technologies used across air, land, and maritime missions. Procurement approaches vary by country, yet the shared focus on operational responsiveness and platform modernization supports wider sector expansion.

Europe advances through defense collaboration, sensor modernization, and interest in precision effects that can strengthen layered protection without excessive logistical burden. Emerging markets in the Middle East, Africa, and South and Central America contribute through selective procurement tied to border security, infrastructure protection, and force modernization programs. Together, these regions broaden the market by creating demand for both high-energy systems and mission-support laser technologies across varied operating environments.

Get more information on this report

Military Laser Systems Market Research Report Guidance:

The report encompasses both qualitative and quantitative data pertaining to the market, categorized by product, procedures, application, and geographical regions.

Beginning with Chapter 2, the report presents key takeaways that underscore the primary trends and market outlook.

Chapter 3 is dedicated to outlining the research methodology employed in this study.

In Chapter 4, an ecosystem analysis is provided.

Chapter 5 delves into the significant industry dynamics affecting the market, including driving factors, existing challenges, potential opportunities, and emerging trends. This section also includes an impact analysis of these drivers and constraints.

Chapter 6 reviews the market scenario, detailing historical revenue figures and forecasts extending to the year 2033.

Chapters 7 through 10 analyze market segments based on product, procedures, application, and geography, covering regions such as North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. These chapters include market revenue data, forecasts, and driving factors.

Chapter 11 presents a competitive analysis, featuring a heat map of key players within the market.

Chapter 12 offers an industry landscape analysis, detailing business activities such as market initiatives, recent developments, mergers, and joint ventures on a global scale, alongside a competitive overview.

In Chapter 13, comprehensive profiles of major companies operating in the market are provided. These profiles include key facts, business descriptions, product and service offerings, financial overviews, SWOT analyses, and significant developments.

Finally, Chapter 14, the appendix, includes a brief company overview, a list of abbreviations, and a disclaimer.

Military Laser Systems Market News and Key Development:

The market continues to evolve through defense contracts, live demonstrations, and platform integration programs. Recent developments highlight stronger emphasis on high-energy weapons and operationally relevant laser architectures.

In May 2026, Laser Photonics Corporation has announced the introduction of a portable laser system designed for military use, expanding its offerings to the U.S. Department of Defense and other military services. The system was developed in collaboration with its affiliated company Fonon Technologies and is intended for equipment maintenance and field applications. The newly introduced system, known as the DefenseTech MRLS Portable Finishing Laser 1020 (DTMF-1020), is designed for surface preparation on marine and military infrastructure.

In January 2026, Rheinmetall and MBDA Germany have announced plans to establish a joint venture dedicated to the development and production of advanced laser weapon systems. The company will be set up as a GmbH in Germany and will focus initially on naval laser systems. The collaboration builds on the companies long-standing cooperation since 2019 and their successful development of a naval laser demonstrator. This demonstrator has already been integrated on a German Navy vessel and tested under real operational conditions over an extended period.

Key Sources Referred:

World Bank -Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Military Laser Systems Market

Dhananjay is a market research and consulting professional with over 5 years of experience in syndicated reports, consulting assignments, and custom research projects. He holds a Bachelor's degree in Pharmacy and an MBA in Marketing, combining technical domain knowledge with strong business acumen and analytical rigor.

Currently supporting end-to-end research engagements and delivering actionable, data-driven insights across multiple industries, Dhananjay is skilled in market forecasting, market sizing, competitive benchmarking, and trend analysis, with a strong focus on delivering high-quality, decision-ready insights for strategic..

Show More

Frequently Asked Questions

How big is the Military Laser Systems Market?

The Military Laser Systems Market is valued at US$ 5.88 Billion in 2025, it is projected to reach US$ 11.25 Billion by 2033.

What is the CAGR for Military Laser Systems Market by (2026 - 2033)?

As per our report Military Laser Systems Market, the market size is valued at US$ 5.88 Billion in 2025, projecting it to reach US$ 11.25 Billion by 2033. This translates to a CAGR of approximately 7.35% during the forecast period.

What segments are covered in this report?

The Military Laser Systems Market report typically cover these key segments-

Type (Weapons, Non-Weapons incl. LRF, LiDAR, Designators, Gyros)

What is the historic period, base year, and forecast period taken for Military Laser Systems Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Military Laser Systems Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Military Laser Systems Market?

The Military Laser Systems Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Northrop Grumman Corp.

Raytheon Technologies

Lockheed Martin

BAE Systems

Thales Group

Elbit Systems

Coherent Corp

L3Harris Technologies

Boeing Company

Leonardo SpA

Who should buy this report?

The Military Laser Systems Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Military Laser Systems Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Military Laser Systems Market

Get Free Sample For Military Laser Systems Market