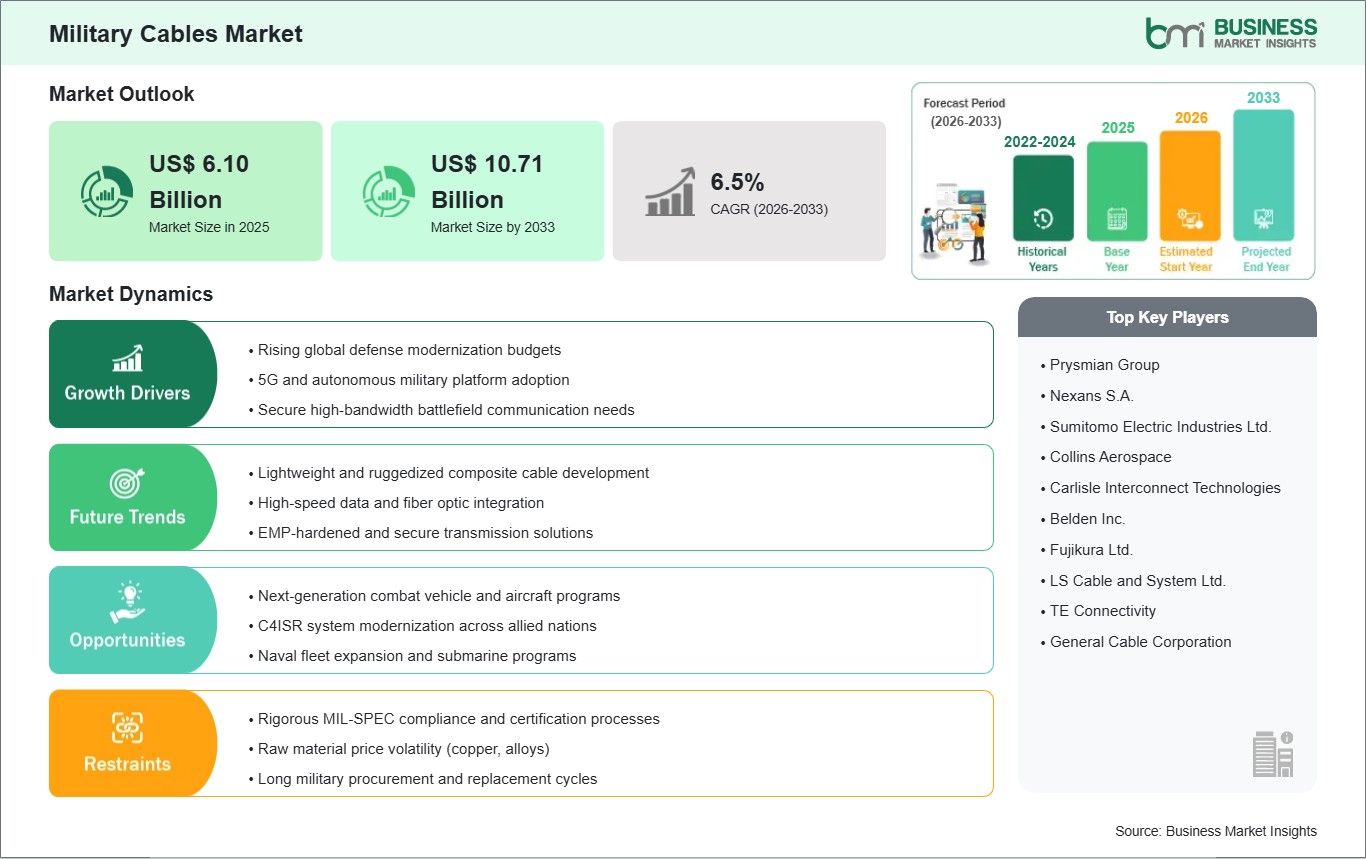

The Military Cables market size is expected to reach US$ 10.71 Billion by 2033 from US$ 6.10 Billion in 2025. The market is estimated to record a CAGR of 6.5% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Military cables are ruggedized transmission assemblies designed to carry power, signals, and data across defense platforms operating under vibration, heat, moisture, and electromagnetic stress. These cable systems are engineered to comply with stringent military specifications, ensuring mechanical durability, shielding performance, and signal continuity in mission-critical environments. Their use extends across battlefield communication networks, onboard electronics, sensor architectures, and weapons integration frameworks where system failure tolerance is minimal.

Procurement emphasis has shifted toward electrically resilient and compact interconnect systems as defense programs incorporate denser electronics, secure data channels, and modular subsystems. Demand is also shaped by modernization cycles across land vehicles, naval vessels, and airborne equipment, where legacy wiring is being replaced with assemblies capable of supporting higher bandwidth and stronger interference protection. This requirement is reinforced by the operational need for dependable connectivity during extended deployments and high-load mission profiles.

Segment expansion is broad, although product selection differs by installation constraints and electrical function. Coaxial cables retain importance in signal-intensive architectures, while twisted pair formats support balanced transmission in communication and control systems. Ribbon cables address compact routing requirements in space-constrained assemblies. Platform demand remains closely aligned with refurbishment programs and the complexity of onboard electronics across ground, marine, and airborne deployments.

Material engineering is becoming a central differentiator as cable manufacturers refine conductor composition for weight control, corrosion resistance, and conductivity retention. Copper alloys remain widely preferred for stable electrical performance, while stainless steel and aluminum variants address specific environmental or mass-reduction requirements. At the same time, insulation systems, shielding layers, and jacket compounds are being optimized to improve survivability under thermal cycling, fluid exposure, and mechanical abrasion.

Competitive conditions are shaped by qualification capability, customization depth, and consistency in meeting defense procurement standards. Suppliers compete on assembly reliability, platform-specific design support, and integration readiness rather than broad-volume commercial scale. The market also reflects longer validation cycles and procurement scrutiny, which favor participants with established defense manufacturing processes and the ability to support retrofit as well as next-generation platform programs.

Military Cables Market - Strategic Insights:

Get more information on this report

Military Cables Market Segmentation Analysis:

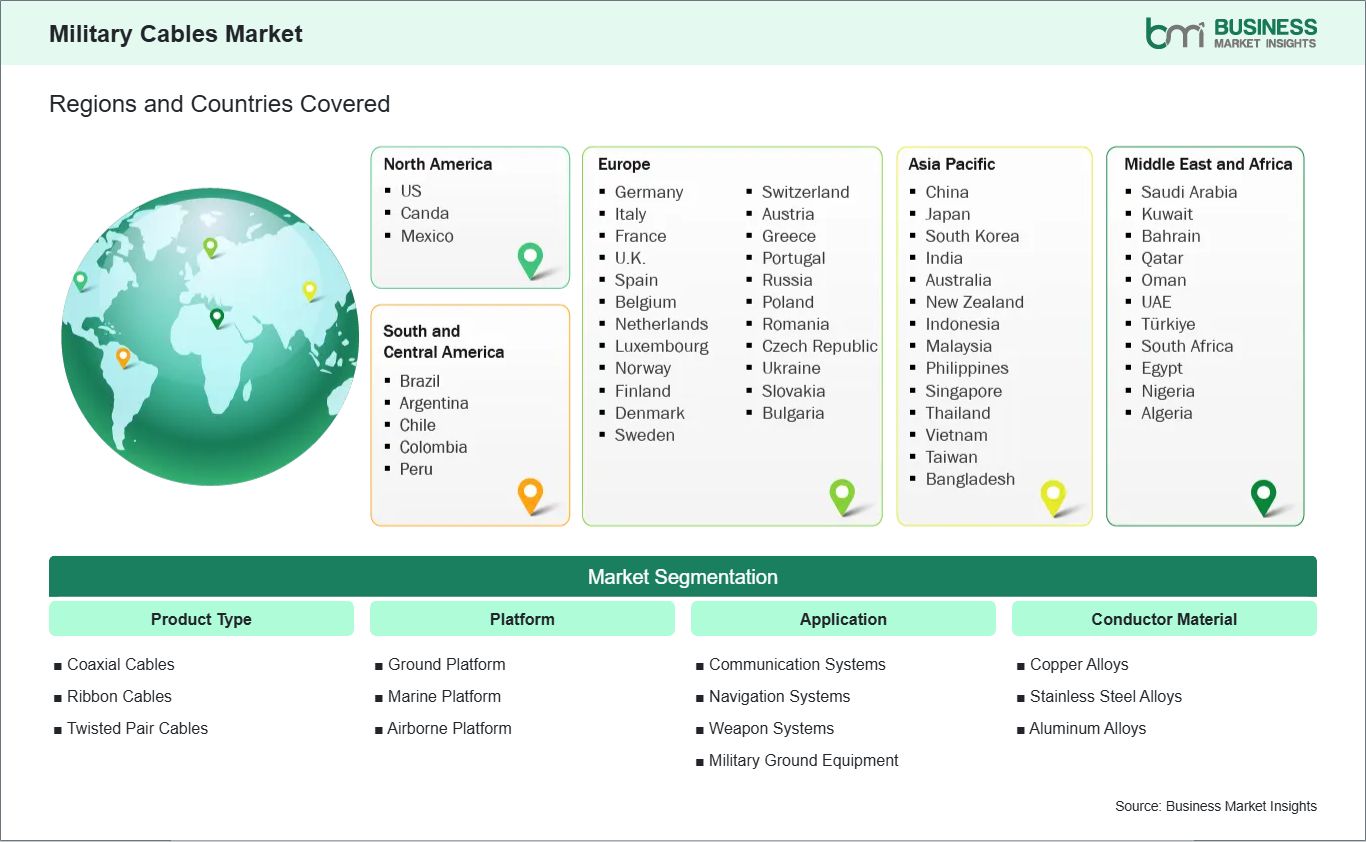

The Military Cables market is segmented by product type, platform, application, and conductor material to reflect deployment-specific performance needs.

By Product Type

Coaxial Cables: Favored for shielded signal transmission in radar, RF, and secure communications.

Ribbon Cables: Suited to dense routing layouts in compact electronic assemblies.

Twisted Pair Cables: Selected for balanced data transfer and interference control.

By Platform

Ground Platform: Accounts for extensive wiring needs in tactical vehicles and mobile systems.

Marine Platform: Requires corrosion-resistant cable designs for saltwater exposure and confined routing.

Airborne Platform: Prioritizes lightweight, high-reliability assemblies for avionics and mission systems.

By Application

Communication Systems: Supports protected signal paths across tactical and strategic networks.

Navigation Systems: Enables dependable connectivity for positioning, guidance, and onboard control units.

Weapon Systems: Endures harsh operating conditions within launch, targeting, and control assemblies.

Military Ground Equipment: Serves field electronics, portable systems, and support infrastructure.

By Conductor Material

Copper Alloys: Preferred where conductivity stability and design versatility are essential.

Stainless Steel Alloys: Applied in demanding environments requiring durability and corrosion tolerance.

Aluminum Alloys: Chosen to reduce cable weight in mobility-sensitive defense platforms.

Military Cables Market Drivers and Opportunities:

Defense Platform Modernization and Electrical System Hardening

Modern defense platforms are integrating more sensors, processors, and secure communication modules, raising the need for cables with stronger shielding, thermal endurance, and routing flexibility. Legacy assemblies often fall short under these requirements, prompting replacement with ruggedized interconnect solutions that preserve signal integrity and electrical continuity across compact and electronics-dense system architectures.

This transition has direct relevance across retrofits and new platform builds, where cable reliability influences mission readiness, maintenance cycles, and subsystem compatibility. As qualification requirements become stricter, procurement decisions increasingly favor cable designs that can withstand electromagnetic exposure, vibration loading, and prolonged service in constrained operational settings without compromising installation efficiency.

Lightweight Materials and High-Performance Cable Engineering

Emerging platform architectures are encouraging innovation in lighter conductor materials, compact cable layouts, and enhanced shielding constructions that support tighter packaging and improved electrical behavior. These developments open new use cases in airborne systems, naval electronics, and mobile defense equipment where reduced mass, corrosion resistance, and stable transmission are critical to sustained system performance.

Future scope extends into next-generation mission electronics, modular upgrade kits, and integrated defense networks that require cable assemblies tailored to demanding installation profiles. Suppliers that advance material science, miniaturization, and qualification-ready customization are positioned to expand program participation as defense organizations seek more efficient and resilient interconnect systems across diverse operating environments.

Military Cables Market Size and Share Analysis:

The Military Cables market size is expected to reach US$ 10.71 Billion by 2033 from US$ 6.10 Billion in 2025. The market is estimated to record a CAGR of 6.5% from 2026 to 2033. This trajectory reflects sustained procurement needs for ruggedized connectivity components that support platform modernization, system reliability, and higher electronic complexity across defense applications.

By product type, coaxial cables hold a leading position due to their suitability for shielded signal transmission in defense electronics. Platform demand remains anchored in ground systems, where extensive wiring architectures support communication units, control modules, and mission equipment operating under mechanically demanding field conditions.

By application, communication systems represent a primary area of use because secure and uninterrupted transmission remains central to defense coordination. Navigation systems, weapon systems, and military ground equipment also sustain meaningful demand as cable performance directly affects data accuracy, signal resilience, and equipment dependability in operational settings.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Prysmian Group

Nexans S.A.

Sumitomo Electric Industries Ltd.

Collins Aerospace

Carlisle Interconnect Technologies

Belden Inc.

Fujikura Ltd.

LS Cable and System Ltd.

TE Connectivity

General Cable Corporation

Get more information on this report

Military Cables Market Report Coverage and Deliverables:

The "Military Cables Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering the areas below:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Military Cables Market Geographic Insights:

The Military Cables market shows diverse regional adoption patterns influenced by defense modernization priorities, platform upgrade cycles, procurement frameworks, and the technical demands placed on mission-critical interconnect systems. Global demand reflects a steady requirement for cable assemblies that can withstand harsh operating conditions while supporting secure communications, navigation, and onboard electronics. Procurement emphasis increasingly centers on durability, interference resistance, and compatibility with dense system architectures.

North America maintains a mature position in this sector due to sustained investment in defense electronics, platform sustainment, and advanced mission systems. The regional market benefits from strong integration capabilities, established qualification practices, and a procurement environment that emphasizes reliability across airborne, land, and naval programs. Replacement demand remains important as operators continue to upgrade legacy wiring frameworks to support higher data loads and improved electromagnetic protection.

Asia Pacific is advancing through defense manufacturing expansion, fleet renewal activity, and broader efforts to strengthen indigenous military capabilities. Regional requirements favor cable solutions that balance rugged performance with weight efficiency, especially in airborne systems and mobile ground equipment. As governments increase focus on domestic production and integrated electronics, suppliers capable of meeting exacting performance standards are finding wider opportunities across both established and developing procurement programs.

Europe presents a technically disciplined market shaped by defense interoperability requirements, naval programs, and specialist aerospace platforms, while emerging markets in the Middle East, Africa, and South and Central America show selective uptake tied to modernization agendas and equipment procurement cycles. In these regions, cable selection is closely linked to environmental resilience, maintenance practicality, and long-service reliability, particularly where systems operate in demanding terrain, maritime conditions, or high-temperature settings.

Get more information on this report

Military Cables Market Research Report Guidance:

The report encompasses both qualitative and quantitative data pertaining to the market, categorized by product type, platform, application, conductor material, and geographical regions.

Beginning with Chapter 2, the report presents key takeaways that underscore the primary trends and market outlook.

Chapter 3 is dedicated to outlining the research methodology employed in this study.

In Chapter 4, an ecosystem analysis is provided.

Chapter 5 delves into the significant industry dynamics affecting the market, including driving factors, existing challenges, potential opportunities, and emerging trends. This section also includes an impact analysis of these drivers and constraints.

Chapter 6 reviews the market scenario, detailing historical revenue figures and forecasts extending to the year 2033.

Chapters 7 through 10 analyze market segments based on product type, platform, application, conductor material, and geography, covering regions such as North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. These chapters include market revenue data, forecasts, and driving factors.

Chapter 11 presents a competitive analysis, featuring a heat map of key players within the market.

Chapter 12 offers an industry landscape analysis, detailing business activities such as market initiatives, recent developments, mergers, and joint ventures on a global scale, alongside a competitive overview.

In Chapter 13, comprehensive profiles of major companies operating in the market are provided. These profiles include key facts, business descriptions, product and service offerings, financial overviews, SWOT analyses, and significant developments.

Finally, Chapter 14, the appendix, includes a brief company overview, a list of abbreviations, and a disclaimer.

Military Cables Market News and Key Development:

Recent developments in the Military Cables market reflect continued emphasis on defense connectivity performance and specialized signal transmission requirements.

In June 2026, Aptiv PLC (NYSE: APTV), a global industrial technology company and Winchester Interconnect, an Aptiv company and leading supplier of high-performance interconnect solutions for mission critical applications, launched a VITA 67.2 RF connector product line that places up to eight high-frequency signal channels directly inside a standard Open VPX backplane slot. By eliminating most of the external coaxial cabling traditionally required in aerospace and defense systems, the connectors make room for more compute, more sensors, and faster signals inside the same enclosure.

In March 2026, Amphenol Socapex, a global designer & manufacturer of interconnect solutions for harsh environments, today announced the release of its USB Type C Active Optical Cable (AOC) extender, an innovative solution that delivers high-speed data, video, and power transmission over long distances where traditional copper solutions fail.

Key Sources Referred:

World Bank: Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Military Cables Market

Prysmian Group

Nexans S.A.

Sumitomo Electric Industries Ltd.

Collins Aerospace

Carlisle Interconnect Technologies

Belden Inc.

Fujikura Ltd.

LS Cable and System Ltd.

TE Connectivity

General Cable Corporation

Frequently Asked Questions

How big is the Military Cables Market?

The Military Cables Market is valued at US$ 6.10 Billion in 2025, it is projected to reach US$ 10.71 Billion by 2033.

What is the CAGR for Military Cables Market by (2026 - 2033)?

As per our report Military Cables Market, the market size is valued at US$ 6.10 Billion in 2025, projecting it to reach US$ 10.71 Billion by 2033. This translates to a CAGR of approximately 6.5% during the forecast period.

What segments are covered in this report?

The Military Cables Market report typically cover these key segments-

Product Type (Coaxial Cables, Ribbon Cables, Twisted Pair Cables)

Application (Communication Systems, Navigation Systems, Weapon Systems, Military Ground Equipment)

Conductor Material (Copper Alloys, Stainless Steel Alloys, Aluminum Alloys)

What is the historic period, base year, and forecast period taken for Military Cables Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Military Cables Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Military Cables Market?

The Military Cables Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Prysmian Group

Nexans S.A.

Sumitomo Electric Industries Ltd.

Collins Aerospace

Carlisle Interconnect Technologies

Belden Inc.

Fujikura Ltd.

LS Cable and System Ltd.

TE Connectivity

General Cable Corporation

Who should buy this report?

The Military Cables Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Military Cables Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Military Cables Market

Get Free Sample For Military Cables Market