Analysis - by Type (Corn Cob, Corn Kernels/Sweet Corn, Green Peas, Baby Corn, Carrot, Cauliflower, Green Beans, Spinach, Broccoli, Onions, Brussel Sprouts, Mixed Vegetables, and Others), Category (Organic and Conventional), and End User (Food Processing, Food Retail, and Foodservice)

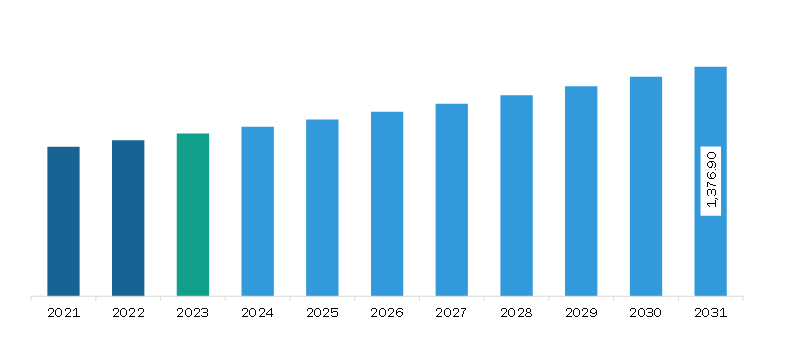

The Middle East & Africa frozen vegetables market was valued at US$ 974.57 million in 2023 and is expected to reach US$ 1,376.90 million by 2031; it is estimated to register a CAGR of 4.4% from 2023 to 2031.

Sustainability in the Frozen Vegetable Industry Bolsters Middle East & Africa Frozen Vegetables Market

Sustainability is becoming a core focus in the frozen vegetable market, driven by both consumer demand and environmental responsibility. One major advantage of frozen vegetables is reduced food waste—thanks to their long shelf life, they help limit spoilage at both retail and household levels. Additionally, many producers are transitioning to eco-friendly packaging, such as recyclable or compostable materials, to minimize plastic waste.

Sustainable farming practices are also gaining traction, including reduced pesticide use, crop rotation, and organic certification. Locally sourced produce is being prioritized to lower carbon emissions from transportation. Energy-efficient freezing and storage technologies are being adopted to further reduce environmental impact.

Moreover, companies are increasingly transparent about their sustainability efforts, using labeling and certifications to inform eco-conscious consumers. As sustainability becomes a key differentiator, brands that invest in green innovations are better positioned to lead the market in the coming years.

Middle East & Africa Frozen Vegetables Market Overview

In the Middle East and Africa, the middle-class population is increasing, along with rising disposable income. With improved purchasing power, consumers are more inclined to explore a variety of frozen vegetables, including premium and exotic options. The presence of supermarket chains and the development of cold chain infrastructure in countries across the Middle East further facilitate the availability and accessibility of frozen vegetables. The market also witnesses growing production and consumption of organic produce in a few countries, such as Saudi Arabia, Kuwait, and the UAE. According to Business Start Up Saudi Arabia, the number of organic farms increased by 28% in 2021 owing to Saudi Arabia's US$ 200 million strategy for innovation plan. The plan aims to increase the capacity of organic farming by 300% in the coming years. The rising urbanization, increasing disposable income, and advancement in supply chain infrastructure are a few factors that drive the market for frozen vegetables.

Middle East & Africa Frozen Vegetables Market Revenue and Forecast to 2031 (US$ Million)

Middle East & Africa Frozen Vegetables Market Segmentation

By type, the Middle East & Africa frozen vegetables market is segmented into corn cob, corn kernels/sweet corn, green peas, baby corn, carrot, cauliflower, green beans, spinach, broccoli, onions, brussel sprouts, mixed vegetables, and others. The others segment held the largest share of the Middle East & Africa frozen vegetables market share in 2023.

In terms of category, the Middle East & Africa frozen vegetables market is bifurcated into organic and conventional. The conventional segment held a larger share of the Middle East & Africa frozen vegetables market share in 2023.

Based on end user, the Middle East & Africa frozen vegetables market is segmented into food processing, food retail, and foodservice. The food retail segment held the largest share of the Middle East & Africa frozen vegetables market share in 2023.

Based on country, the Middle East & Africa frozen vegetables market is segmented into South Africa, Saudi Arabia, the UAE, and the Rest of Middle East and Africa. The Rest of Middle East and Africa segment held the largest share of Middle East & Africa frozen vegetables market in 2023.

Alasko Food Inc.; Ardo Foods NV; B&G Foods; Bonduelle SA; Dawtona Frozen; General Mills Inc; Goya Foods Inc; Grupo Virto; Hanover Foods; La Fe Foods; McCain Foods Ltd; Mondial Foods BV; Mother Dairy Fruit & Vegetable Pvt. Ltd; Seneca Foods Corp; and Simplot Global Food are some of the leading companies operating in the Middle East & Africa frozen vegetables market.

Middle East & Africa Frozen Vegetables Market Strategic Insights

Get more information on this report

Middle East & Africa Frozen Vegetables Market Segmentation Analysis

Middle East & Africa Frozen Vegetables Market Report Highlights

Middle East & Africa Frozen Vegetables Report Scope

Report Attribute

Details

Market size in 2023

US$ 974.57 Million

Market Size by 2031

US$ 1,376.90 Million

CAGR (2023 - 2031)

4.4%

Historical Data

2021-2023

Forecast period

2025-2031

Segments Covered

By Type

Corn Cob

Corn Kernels/Sweet Corn

Green Peas

Baby Corn

Carrot

Cauliflower

Green Beans

Spinach

Broccoli

Onions

Brussel Sprouts

Mixed Vegetables

By Category

Organic

Conventional

By End User

Food Processing

Food Retail

Foodservice

Regions and Countries Covered

Middle East & Africa

Saudi Arabia, the UAE, South Africa, Rest of Middle East & Africa

Market leaders and key company profiles

Alasko Food Inc.

Ardo Foods NV

B&G Foods

Bonduelle SA

Dawtona Frozen

General Mills Inc

Goya Foods Inc

Grupo Virto

Hanover Foods

La Fe Foods

McCain Foods Ltd

Mondial Foods BV

Mother Dairy Fruit & Vegetable Pvt. Ltd

Seneca Foods Corp

Simplot Global Food

Get more information on this report

Middle East & Africa Frozen Vegetables Market Country and Regional Insights

Get more information on this report

Identical Market Reports with other Region/Countries

Shruti Bankar is a market research professional with experience in secondary research, industry analysis, and business intelligence. She is currently associated with The Insight Partners, where she supports the development of market intelligence and actionable insights across a range of industries.

A management graduate from Sinhgad Institute of Management, she combines strong academic foundations with practical research expertise. Her core strengths include analytical thinking, data interpretation, and effective communication, enabling her to deliver accurate, structured, and insight-driven research that supports informed business..

Show More

Frequently Asked Questions

How big is the Middle East & Africa Frozen Vegetables Market?

The Middle East & Africa Frozen Vegetables Market is valued at US$ 974.57 Million in 2023, it is projected to reach US$ 1,376.90 Million by 2031.

What is the CAGR for Middle East & Africa Frozen Vegetables Market by (2023 - 2031)?

As per our report Middle East & Africa Frozen Vegetables Market, the market size is valued at US$ 974.57 Million in 2023, projecting it to reach US$ 1,376.90 Million by 2031. This translates to a CAGR of approximately 4.4% during the forecast period.

What segments are covered in this report?

The Middle East & Africa Frozen Vegetables Market report typically cover these key segments-

Type (Corn Cob, Corn Kernels/Sweet Corn, Green Peas, Baby Corn, Carrot, Cauliflower, Green Beans, Spinach, Broccoli, Onions, Brussel Sprouts, Mixed Vegetables)

Category (Organic, Conventional)

End User (Food Processing, Food Retail, Foodservice)

What is the historic period, base year, and forecast period taken for Middle East & Africa Frozen Vegetables Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Middle East & Africa Frozen Vegetables Market report:

Historic Period : 2021-2023

Base Year : 2023

Forecast Period : 2025-2031

Who are the major players in Middle East & Africa Frozen Vegetables Market?

The Middle East & Africa Frozen Vegetables Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Alasko Food Inc.

Ardo Foods NV

B&G Foods

Bonduelle SA

Dawtona Frozen

General Mills Inc

Goya Foods Inc

Grupo Virto

Hanover Foods

La Fe Foods

McCain Foods Ltd

Mondial Foods BV

Mother Dairy Fruit & Vegetable Pvt. Ltd

Seneca Foods Corp

Simplot Global Food

Who should buy this report?

The Middle East & Africa Frozen Vegetables Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Middle East & Africa Frozen Vegetables Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Middle East & Africa Frozen Vegetables Market

Get Free Sample For Middle East & Africa Frozen Vegetables Market