Analysis By Product (Concrete Admixtures, Asphalt Additives, Waterproofing Chemicals, Adhesives and Sealants, Flame Retardants, and Others) and Application (Residential, Commercial, Industrial, Institutional, and Infrastructure)

No. of Pages:125

Report Code:

BMIRE00027528

Category:

Chemicals and Materials

Middle East & Africa Construction Chemicals Market

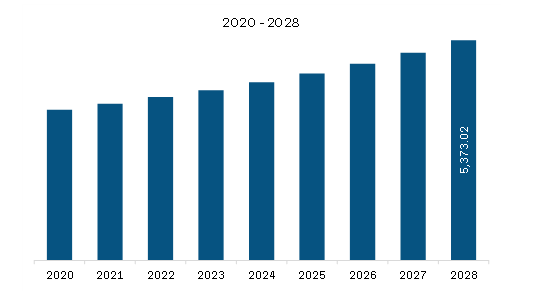

The construction chemicals market in Middle East & Africa is expected to grow from US$ 3,989.61 million in 2022 to US$ 5,373.02 million by 2028. It is estimated to grow at a CAGR of 5.1% from 2022 to 2028.

Development and Adoption of Innovative Products such as Ready-Mix Concrete

Ready-mix concrete is a concrete that is batched for delivery from a central plant instead of being mixed on the job site. It is ideal for many jobs. Ready-mix concrete is particularly beneficial when small quantities of concrete or intermittent placing of concrete are required. It is also ideal for large jobs where space is limited and there is little room for a mixing plant and aggregate stockpiles. There are several advantages of ready-mix concrete, making it a more viable and efficient alternative to site-mix concrete. Ready-mix concrete circumvents the messy and long-drawn task of producing the concrete onsite. With the better handling practices and proper mixing, the consumption of cement can be reduced by nearly 10% to 12%. Ready-mix concrete helps save on capital investments by not having to invest in plants and machinery for cement. All these benefits contribute to the increasing use of ready-mix concrete in various construction activities. Various cities are increasingly changing the traditional dynamics with growing ready-mix concrete penetration. Therefore, the development and adoption of innovative products such as ready-mix-concrete is predicted to offer lucrative opportunities for the Middle East & Africa construction chemicals market growth during the forecast period. Market Overview

South Africa, Saudi Arabia, UAE, and rest of Middle East & Africa are the key contributors to the construction chemicals market in the Middle East & Africa. The growing demand among real estate developers and the surge in infrastructural projects owing to industrialization and urbanization in the region are the key factors anticipated to drive the construction chemicals market. The rising urban population has improved the construction of private residential buildings in semi-urban and urban cities. The government looks forward to investing copious amounts in the building and construction industry. According to World Bank Data, the total value of infrastructure and construction projects in the Middle East & Africa reached $3.2 trillion in mid-2021. The increasing need for residential and non-residential buildings in the region has created lucrative opportunities for the Middle East & Africa construction chemicals market. The increasing adoption of innovative eco-friendly materials in construction and the presence of government standards and initiatives for developing the smart building in the region will drive market revenue growth during the forecast period—rapid urbanization and construction growth, with increasing government spending on infrastructure development through programs in the Middle East & Africa. The leading players in the region are in strategic collaborations that are likely to create growth opportunities for the regional market. In addition, rapid technological advancements in infrastructure development with improving economic conditions, thus resulting in rising disposable income among consumers, have created market opportunities for the Middle East & Africa construction chemicals market. Increasing investment in offices, malls, colleges, schools, universities, and hospitals in the region, with the global expansion of the hospitality business, is expected to support regional revenue growth during the forecast period.

Middle East & Africa Construction Chemicals Market Revenue and Forecast to 2028 (US$ Million)

Middle East & Africa Construction Chemicals Market Segmentation

Based on product, the market is segmented into concrete admixtures, asphalt additives, waterproofing chemicals, adhesives and sealants, flame retardants, and others. The concrete admixtures segment registered the largest market share in 2022.

Based on application, the market is segmented into residential, commercial, industrial, institutional, and infrastructure. The residential segment held a largest market share in 2022.

Based on country, the market is segmented into South Africa, Saudi Arabia, UAE, and rest of Middle East & Africa. Rest of Middle East & Africa dominated the market share in 2022.

Ashland Global Holdings Inc; BASF SE; MAPEI S.p.A; Sika AG; Compagnie de Saint-Gobain S.A.; Pidilite Industries Limited; Forcing; RPM International Inc; and Dow Chemicals Company are the leading companies operating in the construction chemicals market in the Middle East & Africa region.

Middle East & Africa Construction Chemicals Market Strategic Insights

Get more information on this report

Middle East & Africa Construction Chemicals Market Segmentation Analysis

Middle East & Africa Construction Chemicals Market Report Highlights

Middle East & Africa Construction Chemicals Report Scope

Report Attribute

Details

Market size in 2022

US$ 3,989.61 Million

Market Size by 2028

US$ 5,373.02 Million

CAGR (2022 - 2028)

5.1%

Historical Data

2020-2021

Forecast period

2023-2028

Segments Covered

By Product

Concrete Admixtures

Asphalt Additives

Waterproofing Chemicals

Adhesives and Sealants

Flame Retardants

By Application

Residential

Commercial

Industrial

Institutional

Infrastructure

Regions and Countries Covered

Middle East and Africa

South Africa, Saudi Arabia, UAE, Rest of Middle East and Africa

Market leaders and key company profiles

BASE SE.

MAPEI S p.A.

Sika AG.

Fosroc,Inc.

Compagnie de Saint – Gobain S.A.

Pidilite Industries Limited.

RPM International Inc.

Dow Chemicals Company.

Get more information on this report

Middle East & Africa Construction Chemicals Market Country and Regional Insights

Get more information on this report

Identical Market Reports with other Region/Countries

The List of Companies - Middle East & Africa Construction Chemicals Market

BASE SE.MAPEI S p.A.Sika AG.Fosroc,Inc.Compagnie de Saint – Gobain S.A.Pidilite Industries Limited.RPM International Inc.Dow Chemicals Company.

Frequently Asked Questions

How big is the Middle East & Africa Construction Chemicals Market?

The Middle East & Africa Construction Chemicals Market is valued at US$ 3,989.61 Million in 2022, it is projected to reach US$ 5,373.02 Million by 2028.

What is the CAGR for Middle East & Africa Construction Chemicals Market by (2022 - 2028)?

As per our report Middle East & Africa Construction Chemicals Market, the market size is valued at US$ 3,989.61 Million in 2022, projecting it to reach US$ 5,373.02 Million by 2028. This translates to a CAGR of approximately 5.1% during the forecast period.

What segments are covered in this report?

The Middle East & Africa Construction Chemicals Market report typically cover these key segments-

What is the historic period, base year, and forecast period taken for Middle East & Africa Construction Chemicals Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Middle East & Africa Construction Chemicals Market report:

Historic Period : 2020-2021

Base Year : 2022

Forecast Period : 2023-2028

Who are the major players in Middle East & Africa Construction Chemicals Market?

The Middle East & Africa Construction Chemicals Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

BASE SE.

MAPEI S p.A.

Sika AG.

Fosroc,Inc.

Compagnie de Saint – Gobain S.A.

Pidilite Industries Limited.

RPM International Inc.

Dow Chemicals Company.

Who should buy this report?

The Middle East & Africa Construction Chemicals Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Middle East & Africa Construction Chemicals Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Middle East & Africa Construction Chemicals Market

Get Free Sample For Middle East & Africa Construction Chemicals Market