01

Market Summery

Executive Summary and Global Market Analysis

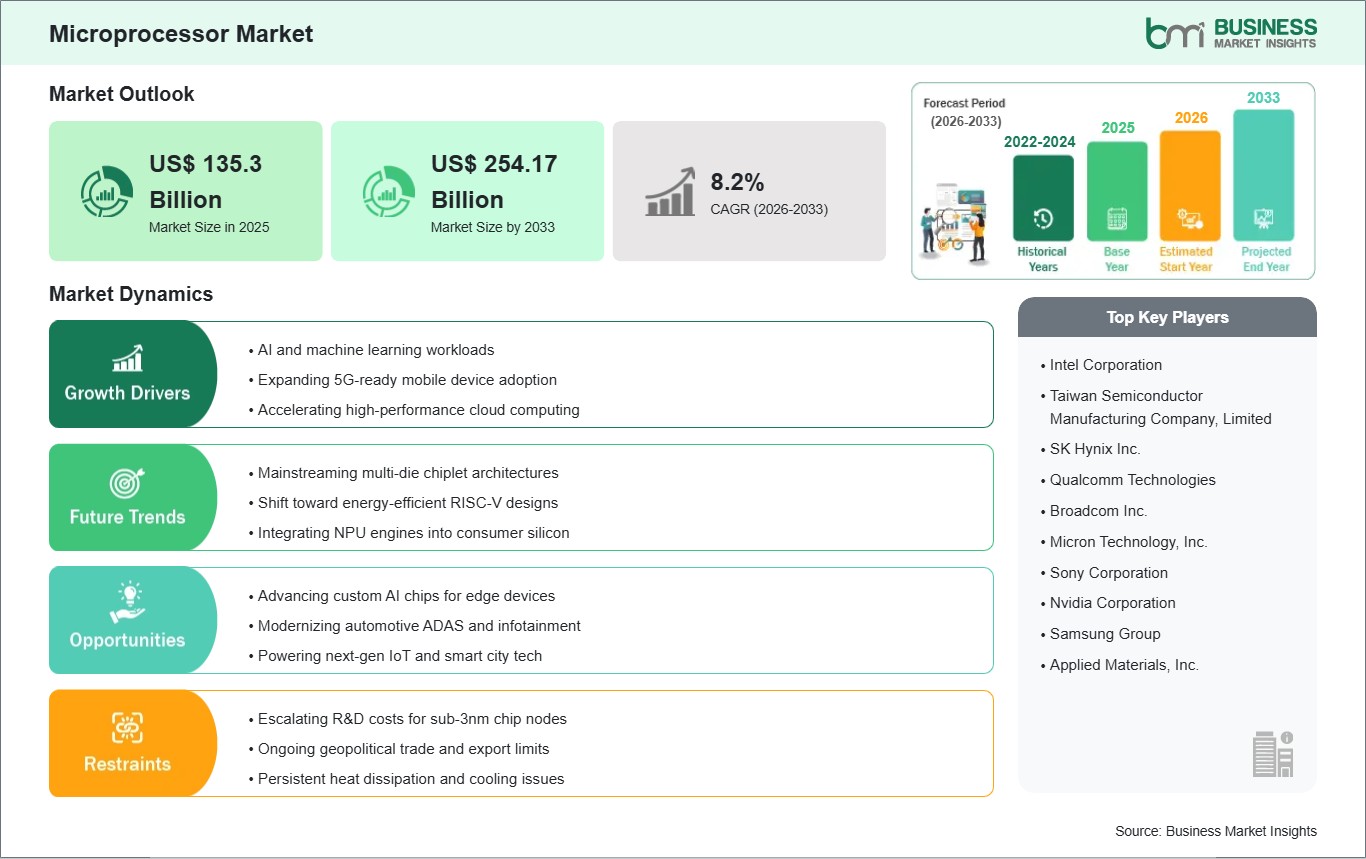

The microprocessor (MPU) serves as the central processing unit and computational brain for many digital devices. It manages system operations and executes complex instructions. MPUs are essential for core applications such as personal computers and laptops, high-performance computing (HPC), enterprise servers, and embedded control systems. MPUs offer advantages including unparalleled computational power, backward compatibility across software ecosystems, and high-level integration of diverse functions (e.g., graphics). The market is being fueled by the accelerating global demand for Artificial Intelligence (AI) and Machine Learning (ML) inference and training, the continued need for cloud computing infrastructure upgrades (servers), and the post-pandemic resurgence of the PC and notebook market. Additionally, the architectural shift toward heterogeneous computing and specialized chipsets (accelerators) is driving market innovation.

However, several challenges can restrain market growth: the increasing complexity and rising costs associated with manufacturing chips at smaller process nodes (e.g., 3nm and 2nm) necessitate enormous capital investment and significantly raise barriers to entry. Intense competition from custom-designed chipsets (e.g., Apple Silicon, Google Tensor) and specialized Accelerated Processing Units (APUs) is fragmenting the traditional MPU market share. Furthermore, the industry faces structural constraints due to the global semiconductor supply chain volatility and the need for continuous, rapid design innovation (following Moore's Law) to maintain performance leadership. Despite these hurdles, the market holds immense opportunities due to exponential growth in edge computing and IoT devices, which require low-power, high-performance MPUs, strategic national investments in domestic semiconductor manufacturing (e.g., CHIPS Act), and the increasing convergence of MPU and GPU architectures for AI workloads.

03

Segment Analysis

Microprocessor Market Segmentation

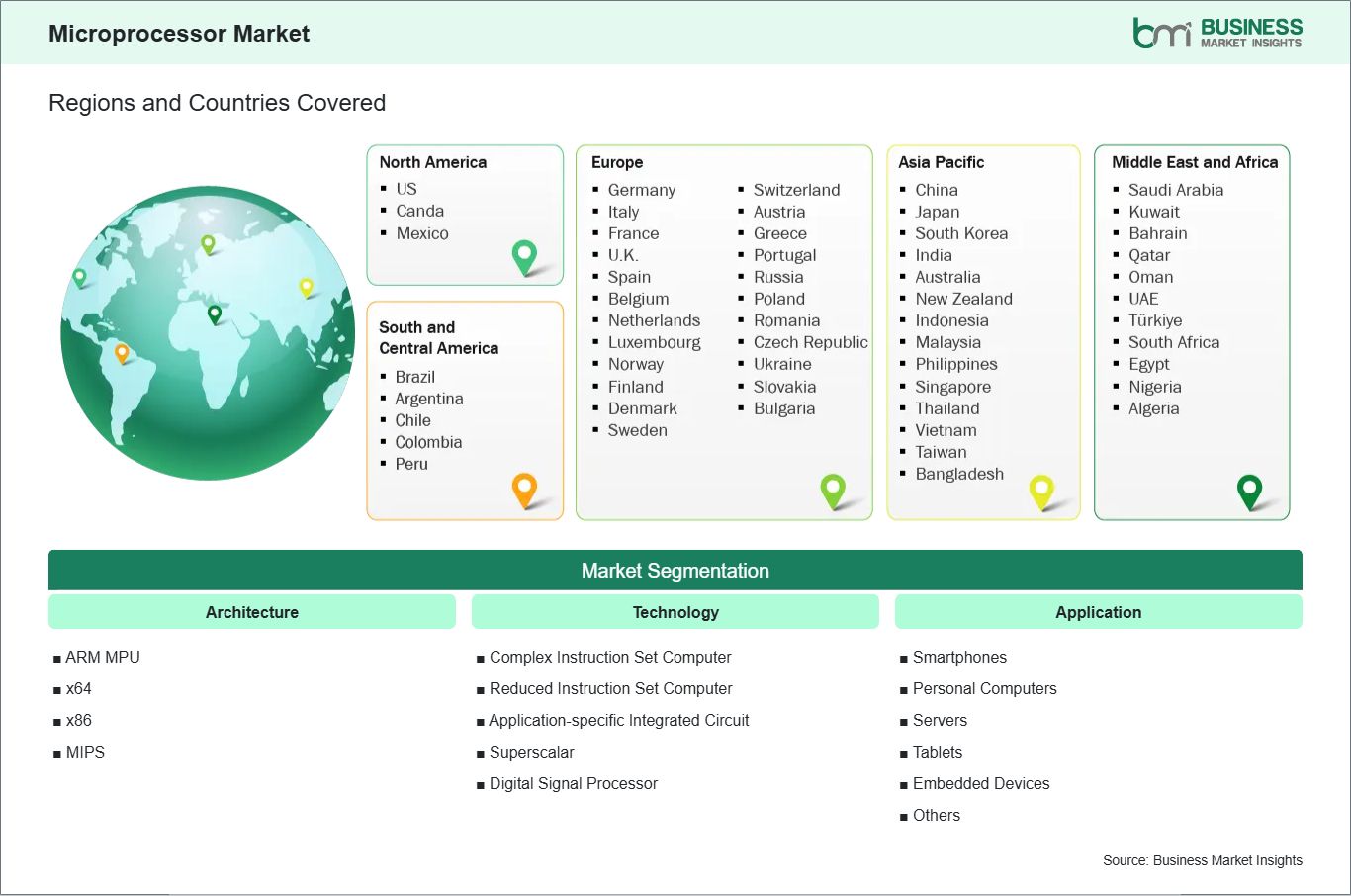

Key segments that contributed to the derivation of the Microprocessor market analysis are architecture, technology, and application.

- By Architecture, the market is segmented into ARM MPU (ARM 32-Bit, ARM 64-Bit), x64, x86, and MIPS.

- By Technology, the market is segmented into Complex Instruction Set Computer (CISC), Reduced Instruction Set Computer (RISC), Application-specific Integrated Circuit (ASIC), Superscalar, and Digital Signal Processor (DSP).

- By Application, the market is segmented into Smartphones, Personal Computers, Servers, Tablets, Embedded Devices, and Others.

04

Market Forces

Microprocessor Market Drivers and Opportunities

Rising Need for Unified AI, HPC, and IoT Solutions

The chief catalyst propelling the Microprocessor Market is the exploding demand for computational power driven by the convergence of Artificial Intelligence (AI), high-performance computing (HPC) for data centers, and the vast proliferation of Internet of Things (IoT) devices. Every modern technological trend requires more processing capability than the last. AI and Machine Learning workloads demand specialized chips, including advanced CPUs, GPUs, and custom AI accelerators, that can handle massive datasets and parallel processing efficiently for training and inference. Concurrently, the proliferation of billions of IoT devices requires microprocessors that are optimized for compact size, ultra-low power consumption, and real-time processing at the network edge. This constant, insatiable need for greater speed and energy efficiency in computing, from the smallest sensor to the largest data center, serves as the fundamental engine for continuous investment and innovation in microprocessor design and manufacturing.

Accelerating Trend of Custom Silico

Major technology companies (hyperscalers, automotive manufacturers, and large consumer electronics brands) are increasingly designing their own custom microprocessors and specialized accelerators. This is done to precisely optimize performance-per-watt for their unique workloads (e.g., custom AI training chips or mobile SoCs), achieve greater competitive differentiation, and secure their supply chains. This movement toward application-specific processors, often utilizing modular chiplet designs, opens the market for specialized manufacturing and design service providers. Furthermore, the rising adoption of open-standard architectures like RISC-V presents an opportunity to challenge the dominance of established ISAs, providing greater flexibility and lower licensing costs for developers targeting embedded systems, industrial automation, and custom chips.

05

Size and Share Analysis

Microprocessor Market Size and Share Analysis

The Microprocessor market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within architecture, technology, and application, offering insights into their contribution to overall market performance.

The ARM 64-bit architecture, built on the Reduced Instruction Set Computer (RISC) framework, represents the dominant configuration within the smartphone and tablet segment. Its widespread adoption is driven by the architecture’s strong balance of power efficiency and high performance-per-watt, enabling mobile devices to support advanced multitasking workloads and AI-driven capabilities while preserving long battery life.

As demand for high-performance mobile computing continues to rise, ARM-based solutions are increasingly expanding beyond traditional mobile devices into embedded systems, IoT hardware, and lightweight laptops. This diversification highlights ARM’s growing relevance across multiple device categories, underscoring its role as a key enabler of efficient, scalable computing across emerging application areas.

07

Report Coverage

Microprocessor Market Report Coverage and Deliverables

The "Microprocessor Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

- Microprocessor market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

- Microprocessor market trends, as well as market dynamics such as drivers, restraints, and key opportunities

- Microprocessor market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Microprocessor market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Microprocessor Market Geographic Insights

The geographical scope of the Microprocessor market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

The Asia-Pacific Microprocessor Market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. The market is primarily driven by the region's dominance in consumer electronics and the rapid expansion of AI-centric high-performance computing.

Growth is further bolstered by the surging demand for AI accelerators and the integration of advanced microprocessors in the automotive sector for autonomous driving and ADAS. Government initiatives, such as India's PLI scheme and China's "Made in China 2025," alongside the rollout of 5G networks, solidify Asia-Pacific as the primary global hub for microprocessor manufacturing and technological deployment.

10

Industry Activity

Recent Developments

The Microprocessor market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Microprocessor market are:

- In September 2025, Qualcomm Technologies, Inc., announced the Snapdragon 8 Elite Gen 5 Mobile Platform, the world's fastest mobile system-on-a-chip. Snapdragon 8 Elite Gen 5 has upgraded the experiences that users today expect from their mobile devices, including Lightning-fast multitasking and seamless app switching and Long game play with incredible performance and power efficiency.

- In March 2025, MediaTek and TSMC announced that they had jointly demonstrated the first silicon-proven power management unit (PMU) and integrated power amplifier (iPA) on TSMC’s N6RF+ process. This achievement makes it possible to integrate these two essential components into a system-on-chip (SoC) on an advanced RF process for wireless connectivity products, enabling a significantly smaller form factor while enjoying performance competitive with stand-alone modules.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Bank - Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations