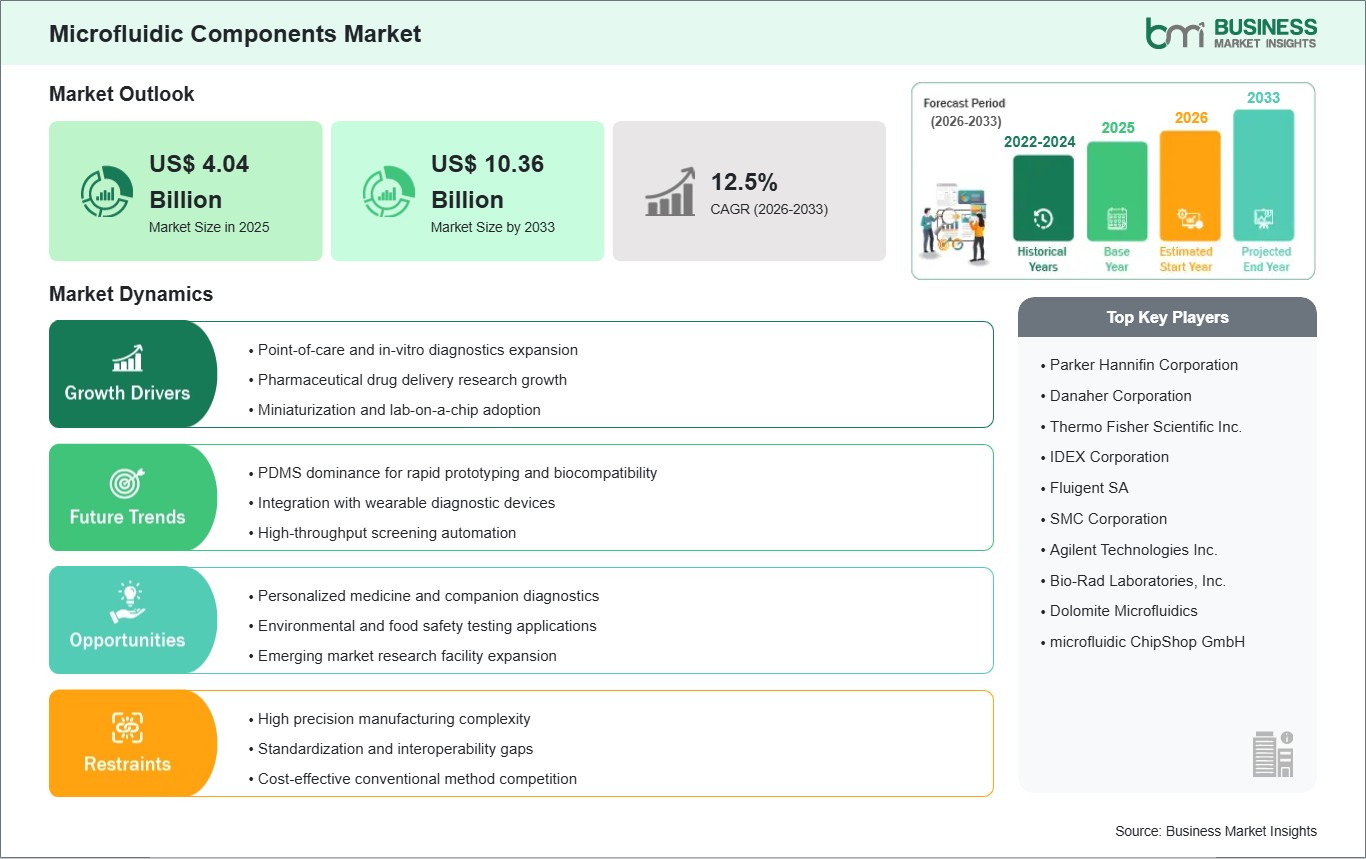

The Microfluidic Components market size is expected to reach US$ 10.36 billion by 2033 from US$ 4.04 billion in 2025. The market is estimated to record a CAGR of 12.5% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Microfluidic components are miniaturized fluid control elements designed to direct, regulate, sense, and transfer very small liquid volumes within compact analytical systems. These components include chips, micropumps, valves, controllers, sensors, and microneedles that support precise handling of samples and reagents across diagnostic and research workflows. Their engineering value lies in improving analytical consistency while reducing reagent consumption, device footprint, and processing time.

Market expansion reflects broader use of decentralized testing formats, automation in laboratory processes, and tighter performance requirements in pharmaceutical research. Point-of-care platforms increasingly rely on compact fluid pathways and accurate control modules to deliver stable results outside centralized laboratories. At the same time, hospitals and diagnostic centers are prioritizing systems that shorten handling steps and improve reproducibility in routine analysis.

Segmentation patterns indicate broad relevance across component design, material selection, application setting, and end-user requirements. Microfluidic chips remain central because they define channel architecture and system integration, while polymers and PDMS support flexible prototyping and scalable fabrication routes. In application terms, in vitro diagnostics and point-of-care testing maintain strong commercial relevance due to their dependence on controlled fluid movement and compact analytical performance.

Technology development is shifting component design toward tighter integration, material compatibility, and application-specific functionality. Sensor-controller combinations are becoming more sophisticated as users demand stable pressure regulation and accurate feedback in compact instruments. Microneedles are also extending system utility by supporting minimally invasive sampling and targeted delivery concepts, widening the addressable scope of microfluidic platforms beyond conventional bench workflows.

Competitive conditions remain shaped by product differentiation, component interoperability, and manufacturing know-how rather than simple scale alone. Suppliers that align precision engineering with application fit are better positioned to address evolving demand from diagnostics, life sciences, and advanced drug delivery programs. As buyers seek dependable subsystem performance, the market continues to reward vendors capable of balancing customization, quality consistency, and production efficiency.

The Microfluidic Components market is segmented by component type, material, application, and end-user to reflect design priorities and deployment needs.

By Component Type

Microfluidic Chips: Define channel architecture and support integrated assay execution.

Micropumps: Enable controlled fluid transfer within compact analytical systems.

Microfluidic Valves: Regulate flow paths and improve switching precision.

Flow/Pressure Sensors and Controllers: Maintain operational stability through continuous measurement and adjustment.

Microneedles: Extend functionality into sampling and localized delivery formats.

By Material

PDMS: Supports rapid prototyping with optical clarity and design flexibility.

Polymer: Favors scalable production and broad commercial manufacturability.

Glass: Provides chemical resistance and stable analytical surfaces.

Silicon: Offers precise microfabrication and compatibility with sensor integration.

By Application

IVD: Requires precise fluid handling for standardized diagnostic performance.

Point-of-Care Testing: Benefits from miniaturized architectures and reduced processing steps.

Pharmaceutical Research: Uses components for screening, modeling, and assay control.

Lab Analytics: Relies on repeatable flow management across compact instruments.

Drug Delivery: Incorporates controlled microfluidic pathways for targeted administration.

Hospitals & Diagnostic Centers: Prioritize dependable components for clinical workflows.

Academic & Research Institutes: Advance prototyping and experimental platform development.

Pharmaceutical & Biotech Companies: Integrate components into research and translational pipelines.

By End-User

Hospitals & Diagnostic Centers: Emphasize workflow reliability and assay consistency.

Academic & Research Institutes: Explore new designs, materials, and device concepts.

Pharmaceutical & Biotech Companies: Adopt specialized components for discovery and development programs.

Microfluidic Components Market Drivers and Opportunities:

Broader Use of Decentralized Diagnostics and Compact Analytical Platforms

Healthcare systems are adopting compact analytical formats that reduce sample handling, shorten turnaround pathways, and support testing beyond centralized laboratories. This operating shift creates a direct need for chips, pumps, valves, and sensing elements that manage fluids with accuracy inside constrained device footprints. As point-of-care instruments move into broader clinical and near-patient settings, component reliability becomes central to stable analytical performance and easier workflow integration.

The market benefits because decentralized platforms depend on tightly coordinated fluid movement, measurement, and control across multiple operating steps. This requirement increases the relevance of specialized components in diagnostic cartridges, lab analytics tools, and portable systems used in routine testing environments. The driver remains significant because end users are evaluating not only instrument outcomes but also component-level consistency, manufacturability, and compatibility with expanding assay menus.

Component Innovation for Advanced Drug Delivery and Research Platforms

Innovation opportunities are widening as microfluidic systems move beyond analysis into therapeutic delivery, biological modeling, and minimally invasive sampling formats. Microneedles, integrated controllers, and material-specific chip designs are enabling more specialized use cases in pharmaceutical research and targeted administration concepts. This transition supports higher-value component development where performance depends on precise dosing, localized transport, and compatibility with sensitive biological environments.

Future scope extends across translational research, wearable formats, and application-tailored subsystems designed for specific assay or delivery objectives. As component suppliers refine material selection, miniaturization, and integration strategies, the market can expand into more differentiated commercial pathways. This opportunity matters because it links engineering advances with end-use relevance, allowing the industry to serve emerging needs in drug development, personalized care, and next-generation testing architectures.

Microfluidic Components Market Size and Share Analysis:

The Microfluidic Components market size is expected to reach US$ 10.36 billion by 2033 from US$ 4.04 billion in 2025. The market is estimated to record a CAGR of 12.5% from 2026 to 2033. This trajectory indicates sustained commercial expansion supported by wider integration of compact fluid handling systems across diagnostics, research platforms, and delivery-oriented applications.

By component type, microfluidic chips hold a leading position because they serve as the structural and functional base of most system designs. Polymers and PDMS retain strong relevance within material selection due to their fabrication flexibility, while sensors, controllers, valves, and micropumps strengthen overall platform precision and operational control.

By application, IVD represents a prominent share of market activity because diagnostic workflows depend on repeatable fluid routing and compact assay integration. Point-of-care testing also commands strong attention as healthcare delivery shifts toward decentralized formats, while pharmaceutical research and drug delivery continue to broaden the commercial relevance of specialized microfluidic components.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Parker Hannifin Corporation

Danaher Corporation

Thermo Fisher Scientific Inc.

IDEX Corporation

Fluigent SA

SMC Corporation

Agilent Technologies Inc.

Bio-Rad Laboratories, Inc.

Dolomite Microfluidics

microfluidic ChipShop GmbHÂ

Get more information on this report

Microfluidic Components Market Report Coverage and Deliverables:

The "Microfluidic Components Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering the areas below:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

The Microfluidic Components market shows diverse regional adoption patterns influenced by healthcare infrastructure maturity, research intensity, manufacturing capabilities, and the pace of diagnostic decentralization. Global demand is shaped by the need for compact, reliable fluid handling architectures across testing, analytical, and therapeutic platforms. Regional performance therefore reflects not only end-user demand, but also the strength of fabrication ecosystems and integration expertise.

North America maintains a strong position because the region combines established diagnostic markets with advanced life sciences research and mature commercialization pathways. Demand is reinforced by sustained use of microfluidic subsystems in clinical testing, pharmaceutical development, and lab automation environments. Buyers in this region generally emphasize performance validation, interoperability, and dependable supply for specialized analytical instruments.

Asia Pacific presents a dynamic growth environment supported by expanding healthcare access, strong electronics and polymer processing capabilities, and increasing research activity across biotechnology and diagnostics. The region benefits from manufacturing depth that supports component scaling as well as cost-sensitive product development. Adoption is also supported by rising interest in portable testing formats and compact laboratory systems suited to high-throughput and distributed settings.

Europe contributes through strong analytical science capabilities, material engineering expertise, and a structured approach to precision healthcare applications. Emerging markets in the Middle East and Africa, as well as South and Central America, are developing more gradually, with adoption linked to laboratory modernization, targeted diagnostic deployment, and institutional investment in applied research. Together, these regions broaden the market’s expansion profile by adding differentiated demand conditions and application priorities.

Get more information on this report

Microfluidic Components Market Research Report Guidance:

The report encompasses both qualitative and quantitative data pertaining to the market, categorized by component type, material, application, end-user, and geographical regions.

Beginning with Chapter 2, the report presents key takeaways that underscore the primary trends and market outlook.

Chapter 3 is dedicated to outlining the research methodology employed in this study.

In Chapter 4, an ecosystem analysis is provided.

Chapter 5 delves into the significant industry dynamics affecting the market, including driving factors, existing challenges, potential opportunities, and emerging trends. This section also includes an impact analysis of these drivers and constraints.

Chapter 6 reviews the market scenario, detailing historical revenue figures and forecasts extending to the year 2033.

Chapters 7 through 10 analyze market segments based on component type, material, application, end-user, and geography, covering regions such as North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. These chapters include market revenue data, forecasts, and driving factors.

Chapter 11 presents a competitive analysis, featuring a heat map of key players within the market.

Chapter 12 offers an industry landscape analysis, detailing business activities such as market initiatives, recent developments, mergers, and joint ventures on a global scale, alongside a competitive overview.

In Chapter 13, comprehensive profiles of major companies operating in the market are provided. These profiles include key facts, business descriptions, product and service offerings, financial overviews, SWOT analyses, and significant developments.

Finally, Chapter 14, the appendix, includes a brief company overview, a list of abbreviations, and a disclaimer.

Microfluidic Components Market News and Key Development:

The Microfluidic Components Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

In February 2026, Tsubaki Nakashima has launched manufacturing capabilities for microfluidic plates, enabling customers to expand their microfluidics-related businesses. Through a strategic partner, our Engineered Plastic Components business has already established initial manufacturing capabilities in the UK. This includes equipment that supports customer collaboration on design and prototyping, enabling the development of application-specific solutions.

In January 2026, Intrepid Automation, provider of industrial additive manufacturing (AM) solutions, and Rapid Fluidics, market leader in design and rapid-production services to microfluidic systems customers, today announced a strategic partnership to advance development and U.S.-based manufacturing of microfluidic technologies. The collaboration combines Rapid Fluidics' design and prototyping expertise with Intrepid Automation's scalable, production-grade additive manufacturing capabilities, enabling more cost-effective development and production of high-precision microfluidic components.

Key Sources Referred:

World Bank: Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Microfluidic Components Market

Parker Hannifin Corporation

Danaher Corporation

Thermo Fisher Scientific Inc.

IDEX Corporation

Fluigent SA

SMC Corporation

Agilent Technologies Inc.

Bio-Rad Laboratories, Inc.

Dolomite Microfluidics

microfluidic ChipShop GmbH

Frequently Asked Questions

How big is the Microfluidic Components Market?

The Microfluidic Components Market is valued at US$ 4.04 Billion in 2025, it is projected to reach US$ 10.36 Billion by 2033.

What is the CAGR for Microfluidic Components Market by (2026 - 2033)?

As per our report Microfluidic Components Market, the market size is valued at US$ 4.04 Billion in 2025, projecting it to reach US$ 10.36 Billion by 2033. This translates to a CAGR of approximately 12.5% during the forecast period.

What segments are covered in this report?

The Microfluidic Components Market report typically cover these key segments-

Component Type (Microfluidic Chips, Micropumps, Microfluidic Valves, Flow/Pressure Sensors and Controllers, Microneedles)

Material (PDMS, Polymer, Glass, Silicon)

Application (IVD, Point-of-Care Testing, Pharmaceutical Research, Lab Analytics, Drug Delivery)

What is the historic period, base year, and forecast period taken for Microfluidic Components Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Microfluidic Components Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Microfluidic Components Market?

The Microfluidic Components Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Parker Hannifin Corporation

Danaher Corporation

Thermo Fisher Scientific Inc.

IDEX Corporation

Fluigent SA

SMC Corporation

Agilent Technologies Inc.

Bio-Rad Laboratories, Inc.

Dolomite Microfluidics

microfluidic ChipShop GmbHÃÂ

Who should buy this report?

The Microfluidic Components Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Microfluidic Components Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Microfluidic Components Market

Get Free Sample For Microfluidic Components Market