01

Market Summery

Executive Summary and Global Market Analysis

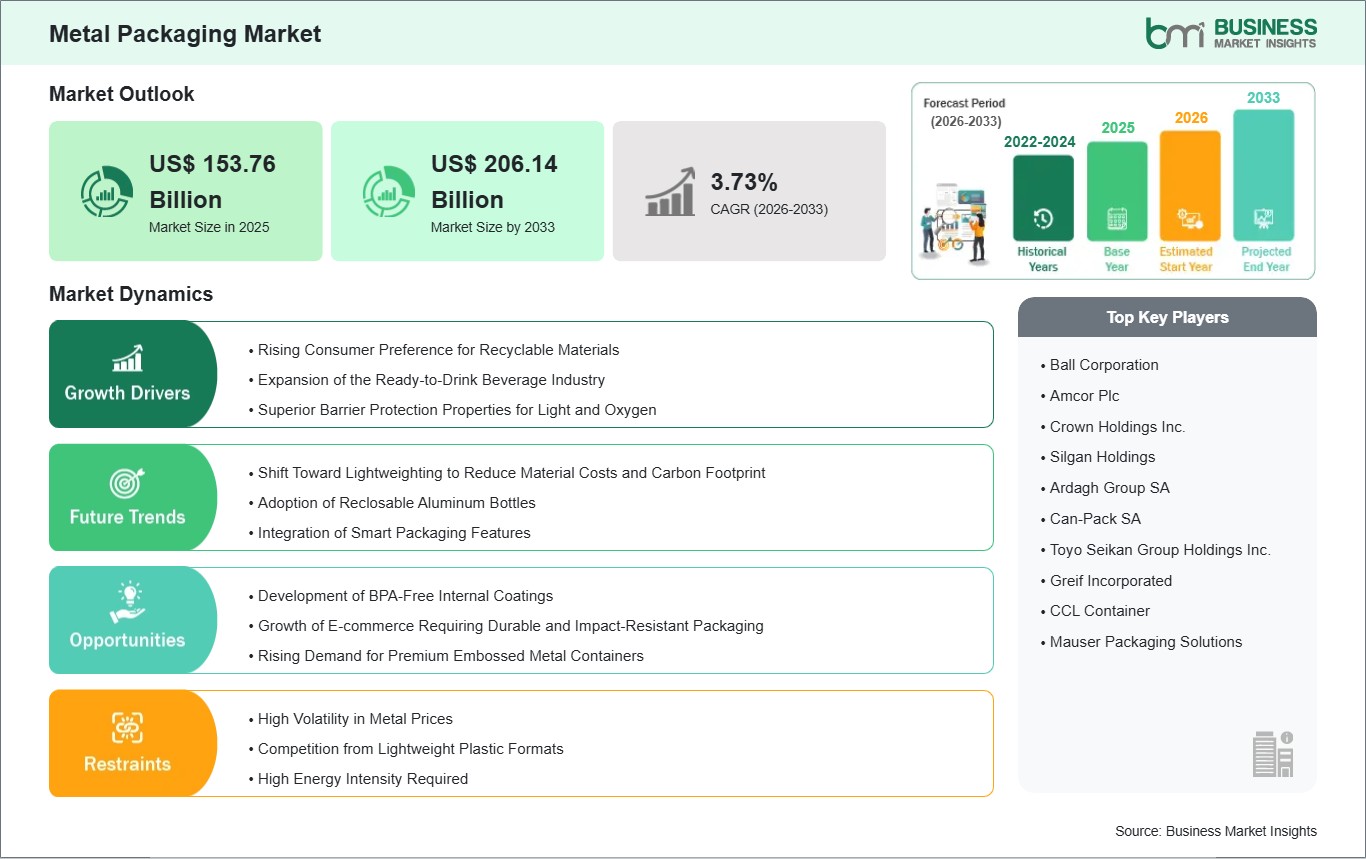

The Metal Packaging market, globally, is an important pillar of the Packaging industry, which has traditionally been valued for its strength, safety, and exceptional sustainability credentials. The market, based on materials like aluminum and steel, offers essential solutions to ensure the security and integrity of food, beverage, and industrial chemical packages. The market, however, is undergoing a paradigm shift with the ongoing revolution in the market, driven by the move from plastic to metal, as brands across the world look to exploit the infinite recyclability of metals to meet ever-increasing environmental requirements. Although the beverage market remains the largest volume market, driven by aluminum cans, other markets like aerosol containers and industrial drums continue to benefit from the exceptional strength and impact resistance offered only by metals.

Innovation within the market is occurring on two primary fronts: lightweighting and material safety. By reducing the gauge of the metal used in cans and closures, the cost of producing the cans is reduced, as is the amount of carbon used during transport. At the same time, the market is quickly moving away from traditional coatings in favor of advanced, health-conscious alternatives. Despite the difficulties posed by the volatility of raw material costs and the high cost of energy, the market is aided by the existing infrastructure for recycling the material and the growing demand for premium sustainable products. The growth of the middle class in emerging countries will continue to fuel the demand for packaged consumer products.

03

Segment Analysis

Metal Packaging Market Segmentation

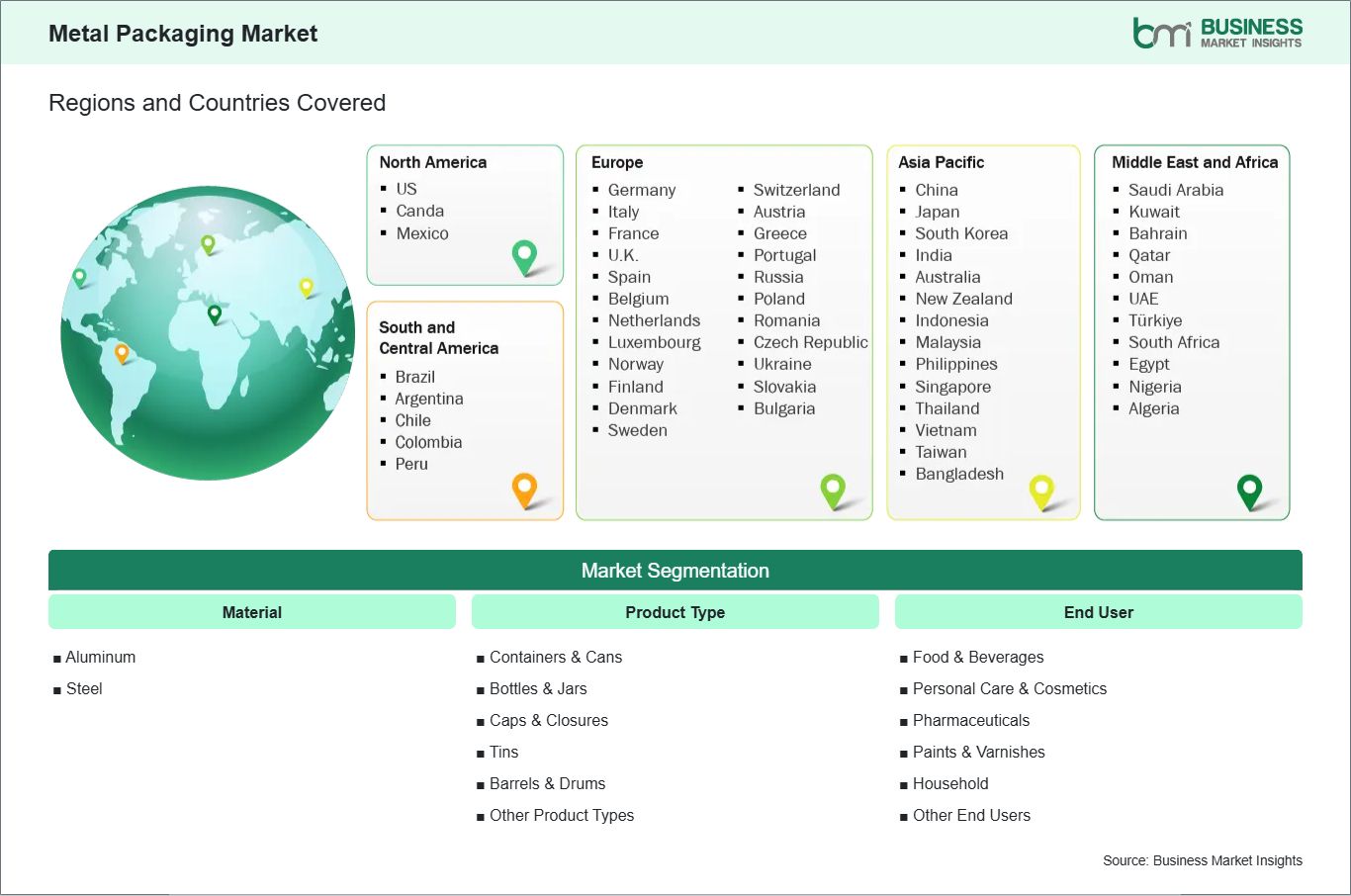

Key segments that contributed to the derivation of the Metal Packaging market analysis are material, product type, and end user.

- By material, the Metal Packaging market is segmented into Aluminum and Steel. The Aluminum segment dominated the market in 2025.

- By product type, the Metal Packaging market is segmented into Containers & Cans, Bottles & Jars, Caps & Closures, Tins, Barrels & Drums, and Other Product Types. The Containers & Cans segment dominated the market in 2025.

- By end user, the Metal Packaging market is segmented into Food & Beverages, Personal Care & Cosmetics, Pharmaceuticals, Paints & Varnishes, Household, and Other End Users. The Food & Beverages segment dominated the market in 2025.

04

Market Forces

Metal Packaging Market Drivers and Opportunities

Rising Consumer Preference for Recyclable Materials

The main driver for the metal packaging industry is the accelerated move toward a circular economy at a global level, which is largely being driven by increased consumer awareness of plastic pollution. Unlike other materials, metals such as aluminum and steel possess the advantage of being permanent materials, meaning they can be recycled indefinitely without compromising their physical properties. This has led to metal packaging being considered the pinnacle for brands looking to achieve a zero-waste strategy. Additionally, regulatory factors are also driving a move toward increased recycling within packaging, and metals possess a well-established infrastructure to meet these demands.

Moreover, there has been an increasing trend among retailers and large multinational CG companies to make public pledges to remove non-recyclable plastics from their supply chain. This shift has been most evident in the beverage industry, which has moved from plastic to aluminum cans. The secondary value of metals can provide an economic driver to ensure successful curbside and recycling programs, which can provide a steady feedstock for recycling. The increasing importance of sustainability as a primary buying criterion among younger demographics means that the natural recyclability of metals can provide a powerful marketing tool to build brand loyalty and market share.

Development of BPA-Free Internal Coatings

One of the significant opportunities in the metal packaging industry is related to the widespread commercialization of advanced internal coatings, which are not based on epoxies. Metal cans have traditionally been lined with Bisphenol A-based materials in order to prevent the food from reacting with the metal and causing corrosive problems as well as undesirable flavors. However, due to growing concerns from health organizations and food safety regulations, there is a growing need for alternative materials. Companies that are successful in developing cost-effective internal coatings that offer similar performance in terms of shelf-life as epoxies will have a greater share in the premium food and beverage industry. This is particularly important in terms of acidic foodstuffs.

This trend towards safer chemistry also provides an opportunity for metal packaging to be utilized in sensitive segments such as infant formula and organic specialty foods, where chemical migration is a key concern for consumers. Another advantage of these new technologies is the ability to preserve flavors, ensuring that the product's organoleptic properties remain intact throughout its shelf life. This technological evolution not only addresses regulatory challenges, but also reinforces the image of metal as a clean, premium, and safe packaging solution for long-term consumption. As food safety regulations continue to move towards a higher level of harmony, being able to certify safe, high-barrier metal containers will be a competitive advantage.

05

Size and Share Analysis

Metal Packaging Market Size and Share Analysis

The global Metal Packaging market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within material, product type, and end user, highlighting their respective contributions to overall market performance.

By material, the Aluminum subsegment dominated the market in 2025 due to its lightweight nature, exceptional corrosion resistance, and high recyclability rates, making it the preferred choice for beverage brands seeking to reduce transportation costs and meet aggressive corporate sustainability targets.

By product type, the Containers & Cans subsegment dominated the market in 2025 because of the massive global consumption of carbonated soft drinks, energy drinks, and canned preserved foods, which rely on the hermetic seal and structural integrity provided by metal cans for long-term shelf stability.

By end user, the Food & Beverages subsegment dominated the market in 2025 driven by the rising demand for convenient, ready-to-drink options and the industry-wide shift away from single-use plastics toward infinitely recyclable metal formats that align with modern consumer environmental preferences.

07

Report Coverage

Metal Packaging Market Report Coverage and Deliverables

The "Metal Packaging Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

- Metal Packaging market size and forecast at the regional and country levels for segments covered under the scope

- Metal Packaging market trends, as well as drivers, restraints, and opportunities

- Metal Packaging market analysis covering key trends, regional framework, major players, regulations, and recent developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Metal Packaging market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Metal Packaging Market Geographic Insights

The geographical scope of the Metal Packaging market report is divided into: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America stands as the dominant force in the metal packaging market, a position rooted in the region's massive per capita consumption of canned beverages and a highly consolidated manufacturing landscape. The United States market is characterized by a sophisticated supply chain where major players drive continuous innovation in can design and recycling technology. The high prevalence of on-the-go lifestyles in North America has historically fueled the demand for convenient, single-serve aluminum cans for everything from craft beer to sparkling water. Additionally, the region benefits from some of the most advanced recycling programs in the world, which sustain the circular flow of aluminum and steel required for high-volume production.

The dominance of the North American region is further supported by a strong industrial sector that utilizes steel barrels and drums for the transport of chemicals, oils, and paints. Regulatory frameworks are also increasingly focused on eliminating single-use plastics, providing a legislative tailwind for metal packaging adoption. While the Asia-Pacific region is catching up in terms of production volume due to rapid industrialization, North America remains the leader in market value and technological leadership, particularly in the development of specialty and premium metal containers. The regional market is also seeing a surge in the craft movement, where small-scale food and beverage producers utilize the branding potential of metal to differentiate their products on retail shelves.

10

Industry Activity

Recent Developments

The Metal Packaging market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Metal Packaging market are:

- In February 2025, Ball Corporation announced a long-term agreement with Açaí Motion to supply aluminum cans for its beverage products, supporting expansion in sustainable packaging adoption.

- In November 2024, Crown Holdings, Inc. announced the construction of a new beverage can manufacturing plant in Virginia, USA, to increase production capacity and meet growing demand.

- In August 2024, Ardagh Metal Packaging announced the launch of its next-generation lightweight beverage can ends, designed to reduce material usage while maintaining performance.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

American Chemistry Council (ACC)International Council of Chemical Associations (ICCA)European Chemical Industry Council (Cefic)China National Building Materials Group (CNBM)Indian Minerals & Granite Exporters Association (IMGEA)Japan Mining Industry Association (JMIA)Brazilian Mining Association (IBRAM)Gulf Petrochemicals and Chemicals Association (GPCA)Company WebsitesCompany Annual ReportsCompany Investor Presentations