01

Market Summery

Executive Summary and Global Market Analysis

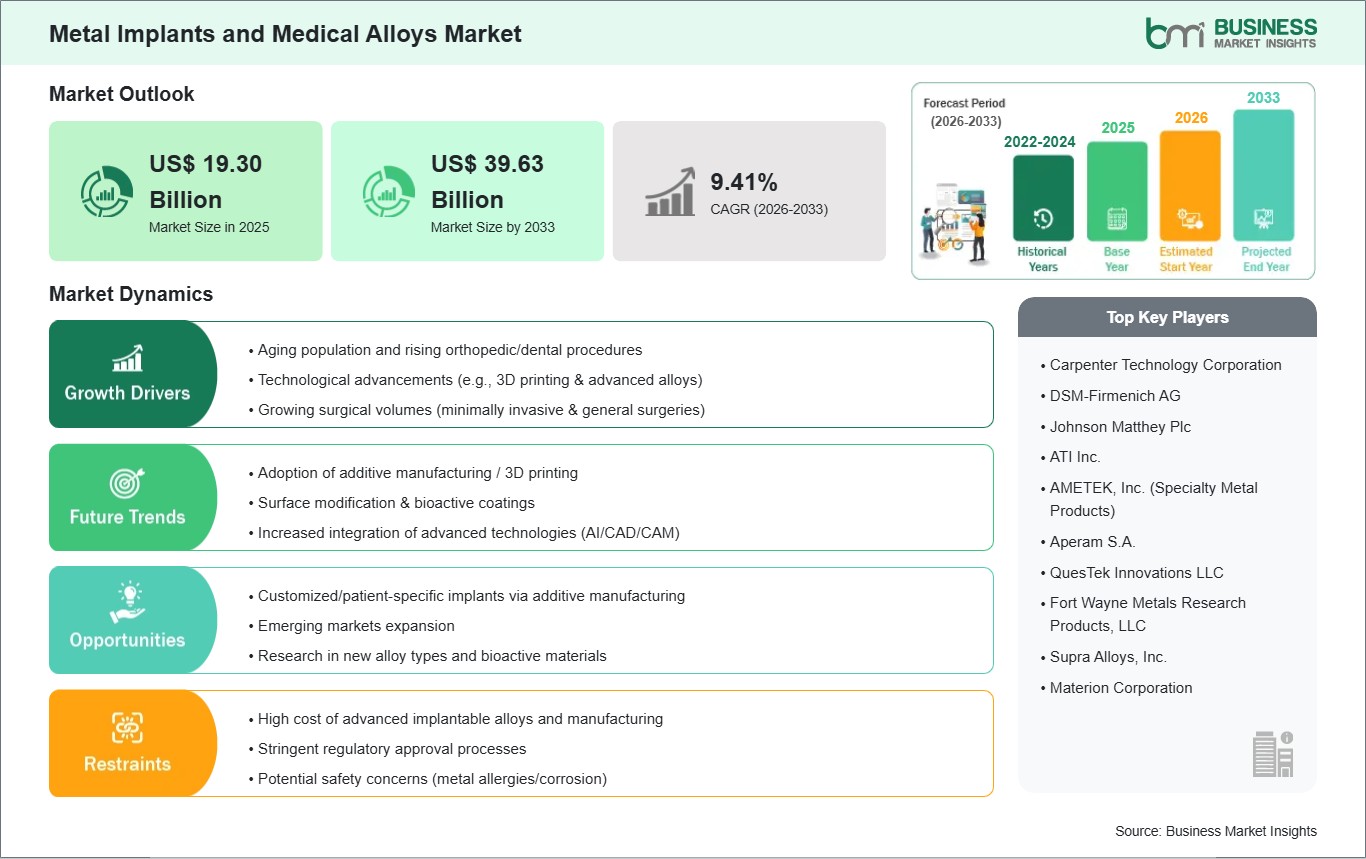

Metal implants and medical alloys refer to specialized, biocompatible materials engineered to support, replace, or enhance damaged biological structures within the human body. Market expansion is fundamentally driven by the global aging population, who exhibit an increasing need for joint reconstructions and dental restorations due to degenerative conditions such as osteoarthritis. Furthermore, the shift toward additive manufacturing (3D printing) is revolutionizing the industry by allowing for the creation of patient-specific implants that promote superior osseointegration and reduce the risk of mechanical mismatch. The rising incidence of trauma and sports-related injuries also contributes to a consistent demand for robust internal fixation devices.

However, several factors can restrain market growth. The high cost of specialized alloys and the complex post-processing required for 3D-printed components can limit their adoption in cost-sensitive healthcare environments. Stringent regulatory pathways for Class III medical devices necessitate extensive clinical evidence and long-term follow-up, which can delay the introduction of innovative material compositions. Additionally, the industry faces challenges related to metal ion release and potential allergic reactions, driving the need for advanced surface coatings and the development of highly inert or bioresorbable alternatives to mitigate long-term biological complications.

Despite these hurdles, the market holds significant opportunities in the development of bioabsorbable metal implants, particularly magnesium and zinc alloys, which gradually dissolve as bone healing progresses, eliminating the need for secondary removal surgeries. The rise of smart implants equipped with sensors for real-time monitoring of strain and infection, along with the expansion of healthcare infrastructure in emerging economies, is expected to support sustained development within the sector.

03

Segment Analysis

Metal Implants and Medical Alloys Market Segmentation

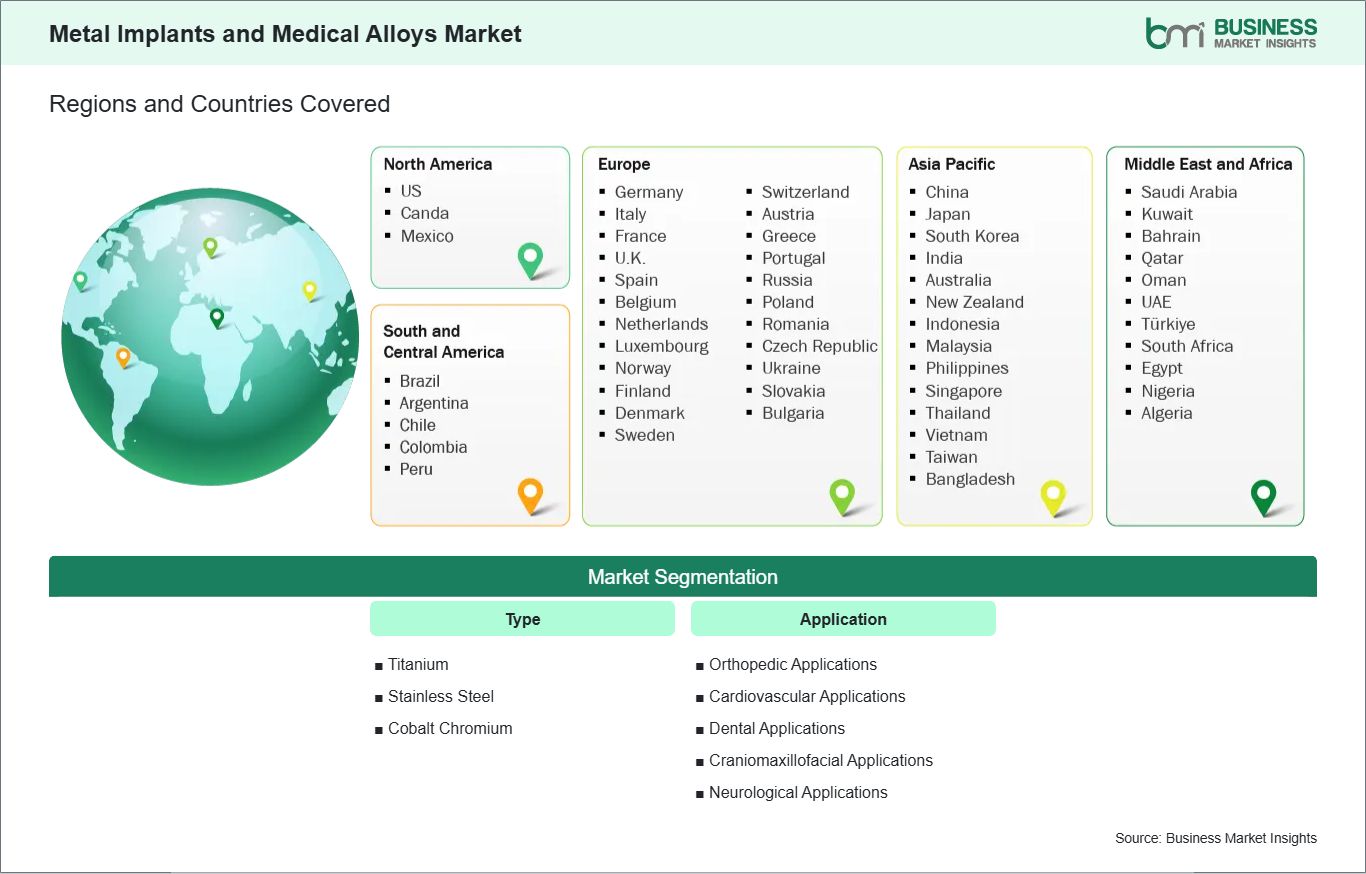

Key segments that contributed to the derivation of the Metal Implants and Medical Alloys market analysis are type and application.

- By Type, the market is segmented into Titanium, Stainless Steel, and Cobalt Chromium.

- By Application, the market is divided into Orthopedic Applications, Cardiovascular Applications, Dental Applications, Craniomaxillofacial Applications, and Neurological Applications.

04

Market Forces

Metal Implants and Medical Alloys Market Drivers and Opportunities

Aging Populations Drive Growth in Complex Orthopedic Procedures

The primary driver for the Metal Implants and Medical Alloys Market is the systemic global rise in age-related degenerative conditions and traumatic injuries. The Increasing Global Prevalence of Osteoarthritis, Osteoporosis, and Degenerative Joint Diseases acts as a foundational catalyst, as an aging population requires high-strength, durable materials for joint reconstructions and spinal fusions. This momentum is further propelled by the Rising Incidence of Road Accidents and Sports-Related Trauma, which necessitates a consistent volume of internal fixation devices, such as plates, screws, and intramedullary nails. In the technological sphere, the Rapid Adoption of Titanium Alloys for their Superior Biocompatibility and Fatigue Resistance serves as a critical driver, as these materials offer a high strength-to-weight ratio and exceptional resistance to corrosion within the physiological environment. Furthermore, the Expansion of Minimally Invasive Surgery (MIS) and Robotic-Assisted Procedures is driving the demand for miniaturized, high-precision metal components that can be deployed through smaller incisions. Together, these factors, demographic aging, trauma volumes, and material performance, ensure a robust and non-discretionary growth path for the global metallurgical healthcare landscape.

3D Printing and Biodegradable Magnesium Alloys Transform Implants

A significant high-value opportunity lies in the convergence of Metal Implants with Additive Manufacturing (3D Printing) for Personalized Care. Manufacturers are increasingly utilizing laser-based powder bed fusion to create customized implants that conform precisely to a patient`s unique anatomy, reducing surgical time and improving long-term stability. There is also a major growth frontier in the development of Next-Generation Biodegradable Metal Alloys, such as Magnesium and Zinc; these materials provide temporary mechanical support during the healing process before gradually resorbing into the body, potentially eliminating the need for secondary hardware removal surgeries, a particular advantage in pediatric and trauma care. Furthermore, the expansion of Advanced Surface Modifications and Biomimetic Coatings presents a lucrative opportunity, where implants are treated with hydroxyapatite or antimicrobial layers to accelerate bone bonding and reduce the risk of implant-associated infections. Beyond orthopedic use, the rise of Shape-Memory Alloys like Nitinol for Cardiovascular and Neurovascular Stents offers a unique frontier, as these materials can be compressed for delivery through catheters and then expand to their functional shape within the vessel. Manufacturers who focus on Low-Modulus Alloys to Prevent Stress Shielding and those pioneering AI-Driven Generative Design for Lightweight Implants are positioned to lead the most innovative and high-margin segments of the global metal implants and medical alloys market.

05

Size and Share Analysis

Metal Implants and Medical Alloys Market Size and Share Analysis

The Metal Implants and Medical Alloys market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report examines subsegments categorized within type and application, offering insights into their contribution to overall market performance.

Based on the type, Titanium subsegment holds the primary market presence, acting as the undisputed cornerstone of modern implantology. This material is indispensable for the market, maintaining a dominant influence due to its exceptional strength-to-weight ratio and its unique ability to bond directly with living bone tissue. Stainless Steel remains a significant segment due to its cost-effectiveness in temporary trauma fixation and general instrumentation. A notable trend is the surge in the Cobalt Chromium subsegment, which is registering significant traction. This alloy is becoming essential for High-Load Joint Reconstruction, as its superior wear resistance and fatigue strength make it the preferred material for the articulating surfaces of knee and hip replacements, effectively maintaining a substantial presence in the orthopedic vertical.

07

Report Coverage

Metal Implants and Medical Alloys Market Report Coverage and Deliverables

The "Metal Implants and Medical Alloys Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

- Metal Implants and Medical Alloys market size and forecast at global, regional, and country levels for all market segments covered under the scope

- Metal Implants and Medical Alloys market trends, as well as drivers, restraints, and opportunities

- Metal Implants and Medical Alloys market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Metal Implants and Medical Alloys market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Metal Implants and Medical Alloys Market Geographic Insights

The geographical scope of the Metal Implants and Medical Alloys market report is divided into five regions: North America, Asia Pacific, Europe, Middle East and Africa, and South and Central America.

North America maintains the leading market position, supported by substantial healthcare expenditure, a high volume of complex orthopedic surgeries, and a favorable reimbursement landscape that encourages the adoption of premium-grade titanium and cobalt-chromium implants. Europe represents a mature market characterized by stringent regulatory standards and a strong institutional focus on material biocompatibility and clinical safety. Asia Pacific is identified as the most rapidly advancing region, propelled by accelerating healthcare modernization, an expanding middle-class population with rising disposable income, and government initiatives in emerging economies to enhance domestic manufacturing of medical devices.

The Asia-Pacific Metal Implants and Medical Alloys Market is segmented into China, Japan, South Korea, India, Australia, and the Rest of Asia Pacific. China serves as a central hub for regional expansion, driven by extensive hospital infrastructure upgrades and a significant patient population requiring spinal and joint reconstruction. India is witnessing a notable transition as the region becomes a prominent destination for medical tourism, particularly for orthopedic and cardiovascular procedures, which increases the demand for high-quality medical alloys. Japan continues to prioritize advanced material science, focusing on the development of high-precision, 3D-printed titanium implants to address the needs of its substantial geriatric demographic.

10

Industry Activity

Recent Developments

The Metal Implants and Medical Alloys market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Metal Implants and Medical Alloys market are:

- In May 2025, Oerlikon launched two new MetcoMed™ metal powders tailored for 3D printing of dental and orthopedic implants. The Ti64 G23-C titanium alloy and CoCrMo F75-A cobalt-chromium-molybdenum alloy offer high strength, excellent ductility, and biocompatibility. The company expands global capabilities for additive manufacturing of medical implants, supporting the production of complex, patient-specific components.

- In Aug 2024, Scheftner GmbH launched a major investment at its Mainz site to expand production of high-precision alloy powders for dental and medical applications. Leveraging ISO 13485 certification, additive manufacturing technologies like PBF/SLM, and sustainable recycling processes, the company strengthens its global capabilities for medical-grade alloy powders, supporting 3D printing of complex, biocompatible components.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Bank - Global Trade Indicators World Trade Organization (WTO) International Monetary Fund (IMF) International Trade Administration (ITA) Company website Company annual reports Company investor presentations