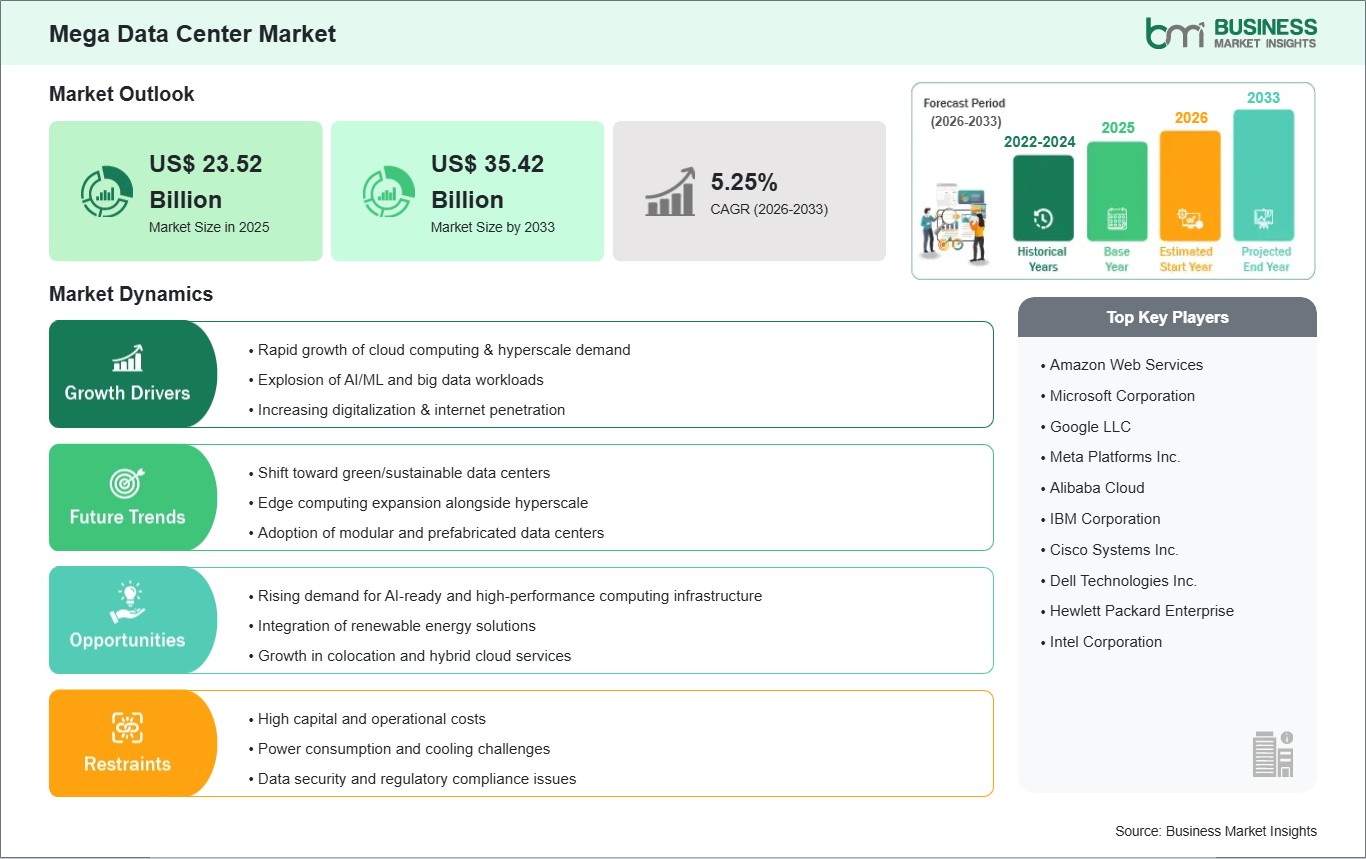

The Mega Data Center market size is expected to reach US$ 35.42 billion by 2033 from US$ 23.52 billion in 2025. The market is estimated to record a CAGR of 5.25% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Mega data centers represent massive-scale, centralized computing facilities, typically designed with a power capacity exceeding 50MW and housing hundreds of thousands of servers. Unlike traditional enterprise data centers, these facilities are purpose-built for extreme scalability and high-density workloads, serving hyperscale cloud providers such as Amazon, Google, and Microsoft, as well as large-scale internet enterprises. They leverage advanced infrastructure technologies, including liquid cooling systems, high-efficiency power distribution units (PDUs), and modular white space designs, to achieve superior Power Usage Effectiveness (PUE) ratings while managing the significant heat and energy demands generated by modern Artificial Intelligence (AI) and Machine Learning (ML) clusters. Market progression is being propelled by the ongoing infrastructure investment supercycle, with projections indicating that more than 100GW of new capacity will be deployed globally by the end of the decade.

Despite this momentum, several factors may restrain market development. Severe power grid constraints in mature hubs have extended utility connection timelines for facilities exceeding 100MW to as long as seven years in regions such as Northern Virginia. Rising construction costs, which have escalated to approximately USD 11.3 million per MW, present a substantial capital challenge for developers and investors. Furthermore, regulatory scrutiny and permitting delays are intensifying, as local governments increasingly enforce energy efficiency mandates and zoning reforms to mitigate the environmental footprint of these large-scale facilities.

Nevertheless, the market outlook remains highly favorable. Significant opportunities exist in the transition to liquid cooling and immersion technologies, which are becoming essential as rack densities approach 100kW for AI-driven workloads. Expansion into Tier 2 and secondary markets, where power availability is more favorable, is expected to accelerate growth. Additionally, the integration of on-site power generation solutions, including small modular reactors (SMRs) and large-scale battery energy storage systems (BESS), will enhance resilience and sustainability. Manufacturers are also capitalizing on modular and prefabricated construction techniques, which reduce deployment timelines and improve scalability. Collectively, these advancements position mega data centers as a cornerstone of global digital infrastructure for the coming decade.

Mega Data Center Market - Strategic Insights:

Get more information on this report

Mega Data Center Market Segmentation Analysis:

Key segments that contributed to the derivation of the Mega Data Center market analysis are resin solution, services, verticals, and end-users.

By Solutions, the market is segmented into IT Infrastructure solutions and support infrastructure solutions.

By Services, the market is divided into System integration, Monitoring services, and Professional services.

By Verticals, the market is categorized into Banking, Financial Services and Insurance (BFSI), Telecom and IT, Media and entertainment, Government and public, and Others.

By End‑Users, the market is segmented into Cloud providers, Colocation providers, and Enterprises.

Mega Data Center Market Drivers and Opportunities:

Cloud Migration, AI Workloads, and Digital Transformation

A primary driver for the mega data center market is the accelerating migration of enterprise workloads to cloud platforms, coupled with the exponential rise in artificial intelligence (AI) and machine learning applications. Mega data centers, operated by hyperscale providers, are designed to deliver massive computing power, scalability, and resilience, making them indispensable for modern digital ecosystems. Enterprises across industries are embracing cloud-first strategies to reduce costs, enhance agility, and support innovation, which directly fuels demand for large-scale facilities. The surge in AI workloads, including generative AI, predictive analytics, and advanced modeling, requires high-performance computing infrastructure that mega data centers are uniquely equipped to provide. Additionally, the proliferation of IoT devices, edge computing, and real-time applications such as autonomous vehicles and smart city platforms is intensifying the need for centralized facilities capable of processing and storing vast amounts of data. Governments and corporations investing in digital transformation programs further reinforce this trend, positioning mega data centers as the backbone of global connectivity and innovation.

Renewable Energy Integration, Edge Collaboration, and Regional Expansion

A significant opportunity in the mega data center market lies in renewable energy integration, collaboration with edge computing ecosystems, and expansion into emerging regions. Sustainability has become a strategic priority, with operators increasingly investing in renewable sources such as solar, wind, and hydro to power facilities and reduce carbon footprints. This shift not only aligns with global climate goals but also enhances operational efficiency by lowering long-term energy costs. The convergence of mega data centers with edge computing presents another transformative pathway, as centralized facilities collaborate with localized nodes to deliver low-latency services for applications like augmented reality, telemedicine, and industrial automation. Beyond technological innovation, emerging markets in Asia-Pacific, Africa, and Latin America offer lucrative prospects due to rapid urbanization, rising internet penetration, and government-led investments in digital infrastructure. Vendors who focus on building energy-efficient, scalable, and region-specific mega data centers are well-positioned to capture new market segments. The integration of renewable energy, edge collaboration, and geographic expansion underscores a transformative growth trajectory for the global mega data center market.

Mega Data Center Market Size and Share Analysis:

The Mega Data Center market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report examines subsegments categorized within solutions, services, verticals, and end users, offering insights into their contribution to overall market performance.

Based on services, the System Integration subsegment represents the highest volume of consumption within the market. These services are indispensable for Unified Architecture Deployment, ensuring that disparate hardware components function as a cohesive, high-availability fabric. By enabling seamless interoperability and reliability, system integration anchors demand and maintains its dominant influence. Its role is critical in complex environments where efficiency and uptime are paramount, positioning this subsegment as the technological backbone of service-based revenue streams. As organizations scale operations, system integration continues to drive stability and performance across multi-region facilities.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Amazon Web Services

Microsoft Corporation

Google LLC

Meta Platforms Inc.

Alibaba Cloud

IBM Corporation

Cisco Systems Inc.

Dell Technologies Inc.

Hewlett Packard Enterprise

Intel Corporation

Get more information on this report

Mega Data Center Market Report Coverage and Deliverables:

The "Mega Data Center Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all market segments covered under the scope

Market trends, as well as drivers, restraints, and opportunities

Market analysis covering key trends, global and regional framework, major players, and recent developments

Market concentration, heat map analysis, prominent players, and recent developments

Detailed company profiles, including SWOT analysis

Mega Data Center Market Geographic Insights:

The geographical scope of the Mega Data Center market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

North America currently maintains the most substantial market share, supported by the presence of primary hyperscale providers and advanced fiber connectivity. Asia Pacific is identified as the fastest-growing region, with a projected compound annual growth rate exceeding twenty-three percent, propelled by massive internet penetration and state-led digital transformation initiatives. Europe represents a sophisticated hub focused on data sovereignty and stringent environmental regulations, while the Middle East & Africa and South & Central America are emerging as strategic corridors for global data traffic and green compute investments. The Asia-Pacific Mega Data Center Market serves as a vital engine for global expansion, driven by the rapid deployment of high-capacity facilities in China, India, and Southeast Asia. These nations are prioritizing the development of AI-Ready Infrastructure, characterized by the integration of high-density liquid cooling and high-performance GPU clusters. China remains the dominant regional force, contributing significantly to the global pipeline with multi-gigawatt capacity additions aimed at supporting its national East Data, West Computing strategy. India is witnessing a notable transition, marked by aggressive investments in Mumbai and Chennai, which are evolving into primary subsea cable landing hubs that facilitate high-speed connectivity between Eastern and Western markets.

Get more information on this report

Mega Data Center Market Research Report Guidance:

The report includes qualitative and quantitative data in the Mega Data Center market across solutions, services, verticals, end users, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 11 cover market segments by solutions, services, verticals, end users, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Mega Data Center Market News and Key Development:

The Mega Data Center market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Mega Data Center market are:

In January 2026, RT-One partnered with Hitachi Energy to develop mega AI data center campuses in Uberlândia and Maringá, Brazil, with modular capacities of up to 400 MW per site. The collaboration focuses on high-voltage electrification, energy efficiency, and resilient power infrastructure to support AI, high-performance computing, and sovereign cloud initiatives. This project positions Brazil as a regional hub for mega-scale data centers and signals positive growth for the global Mega Data Center market.

In September 2025, OpenAI and NVIDIA announced a strategic partnership to deploy at least 10 gigawatts of NVIDIA systems across AI data centers, supported by up to $100 billion in investment. The collaboration will enable next-generation AI infrastructure with millions of GPUs, powering large-scale AI workloads and advancing compute capabilities. This partnership marks a significant expansion in mega data center capacity and signals strong positive growth for the AI-focused Mega Data Center market.

Key Sources Referred:

World Bank & Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Mega Data Center Market

Amazon Web Services

Microsoft Corporation

Google LLC

Meta Platforms Inc.

Alibaba Cloud

IBM Corporation

Cisco Systems Inc.

Dell Technologies Inc.

Hewlett Packard Enterprise

Intel Corporation

About Author— Electronics and Semiconductor Research Team

Siddhika is an experienced market research professional with over five years of expertise in delivering actionable market intelligence and strategic insights to support business growth and decision-making. She has strong experience in designing and managing end-to-end research engagements, including research planning, data collection, and insight generation.

Proficient in research methodologies, Siddhika synthesizes diverse information sources to deliver accurate, high-quality insights and strategic recommendations. She excels at translating complex market information into strategic narratives that support executive decision-making..

Show More

Frequently Asked Questions

How big is the Mega Data Center Market?

The Mega Data Center Market is valued at US$ 23.52 Billion in 2025, it is projected to reach US$ 35.42 Billion by 2033.

What is the CAGR for Mega Data Center Market by (2026 - 2033)?

As per our report Mega Data Center Market, the market size is valued at US$ 23.52 Billion in 2025, projecting it to reach US$ 35.42 Billion by 2033. This translates to a CAGR of approximately 5.25% during the forecast period.

What segments are covered in this report?

The Mega Data Center Market report typically cover these key segments-

Solutions (IT Infrastructure solutions, support infrastructure solutions)

Services (System integration, Monitoring services, and Professional services)

Verticals (Banking, Financial Services and Insurance (BFSI), Telecom and IT, Media and entertainment, Government and public, and Other Verticals)

End Users (Cloud providers, Colocation providers, and Enterprises)

What is the historic period, base year, and forecast period taken for Mega Data Center Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Mega Data Center Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Mega Data Center Market?

The Mega Data Center Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Amazon Web Services

Microsoft Corporation

Google LLC

Meta Platforms Inc.

Alibaba Cloud

IBM Corporation

Cisco Systems Inc.

Dell Technologies Inc.

Hewlett Packard Enterprise

Intel Corporation

Who should buy this report?

The Mega Data Center Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Mega Data Center Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Mega Data Center Market

Get Free Sample For Mega Data Center Market