01

Market Summery

Executive Summary and Global Market Analysis

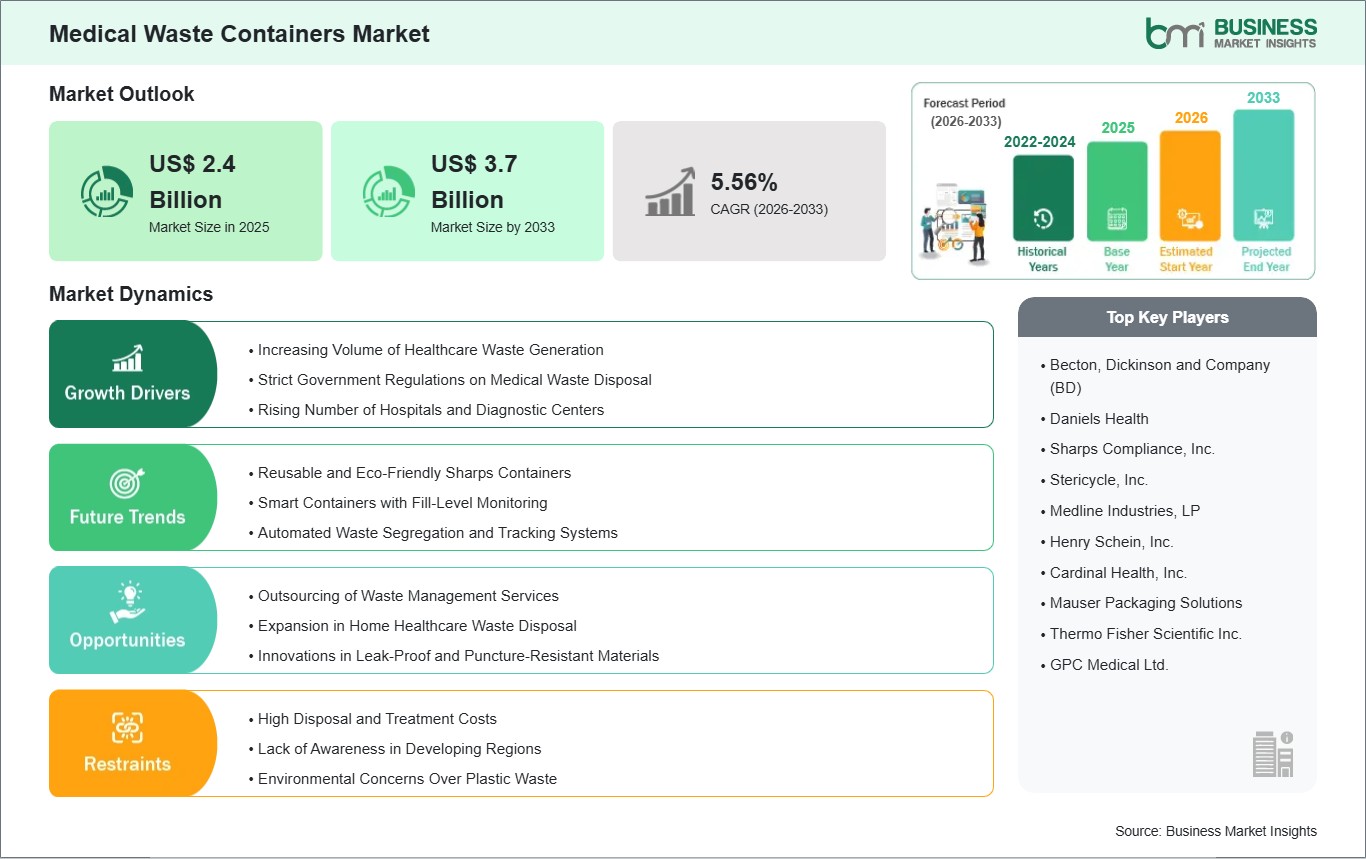

Medical waste containers are specialized, safety-engineered vessels used for the secure segregation, storage, and transport of hazardous and non-hazardous materials generated within healthcare settings. These containers are essential for preventing cross-contamination and protecting healthcare personnel, patients, and waste handlers from exposure to infectious agents, sharp injuries, or toxic substances. Market expansion is primarily driven by the rising global volume of healthcare-associated waste, which is projected to reach several million tons annually. The increasing prevalence of infectious diseases, alongside a surge in surgical interventions and diagnostic laboratory testing, necessitates a continuous supply of high-quality containment solutions. Furthermore, the global expansion of healthcare infrastructure, particularly the proliferation of hospitals, clinics, and research laboratories in developing regions, serves as a primary catalyst for sustained demand.

However, several factors may restrain market progression. The high operational costs associated with specialized waste management, including the procurement of compliant containers and the subsequent high-temperature treatment, can be prohibitive for smaller healthcare facilities. Stringent and evolving regulatory landscapes regarding the transportation of hazardous materials require manufacturers to invest heavily in rigorous testing and certification. Additionally, the industry faces challenges related to supply chain volatility for medical-grade resins and the environmental pressure to reduce the volume of single-use plastic waste generated by disposable container lines.

Despite these hurdles, the market holds significant opportunities in the development of reusable and eco-friendly containers made from sustainable or recyclable materials. The integration of smart technology, such as IoT-enabled sensors for real-time fill-level monitoring and RFID tags for procedural traceability, is expected to support long-term development. Manufacturers are also finding growth potential in the expansion of home healthcare services, which requires portable and user-friendly disposal solutions for patients managing chronic conditions outside traditional hospital settings.

03

Segment Analysis

Medical Waste Containers Market Segmentation

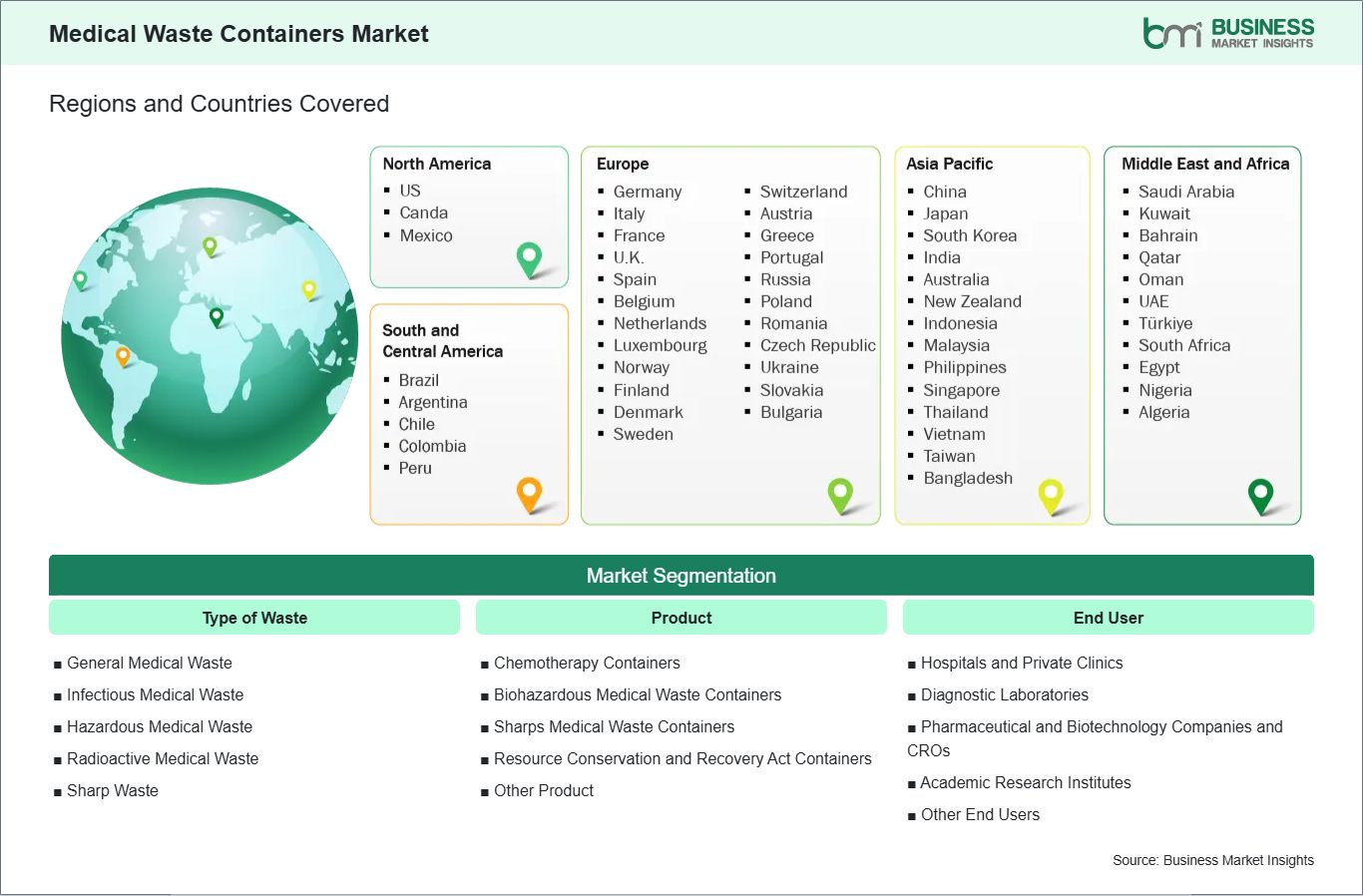

Key segments that contributed to the derivation of the Medical Waste Containers market analysis are the type of waste, product, and end user.

- By Type of waste, the market is segmented into general medical waste, infectious medical waste, hazardous medical waste, radioactive medical waste, and sharp waste.

- By Product, the market is divided into chemotherapy containers, biohazardous medical waste containers, sharps medical waste containers, Resource Conservation and Recovery Act (RCRA) containers, and others.

- By End User, the market is categorized into hospitals & private clinics, diagnostic laboratories, pharmaceutical and biotechnology companies & CROs, academic research institutes, and other end users.

04

Market Forces

Medical Waste Containers Market Drivers and Opportunities

Expanding Global Patient Throughput and Stringent Compliance Mandates

The primary driver for the Medical Waste Containers Market is the systemic global increase in healthcare utilization and the subsequent surge in biomedical waste volumes. The Escalating Number of Diagnostic Procedures and Surgical Interventions acts as a foundational catalyst, as every clinical interaction generates a non-discretionary requirement for secure waste segregation. This momentum is further propelled by Strict Government Regulations and Heavy Penalties for Non-Compliance; legislative frameworks, such as the Resource Conservation and Recovery Act (RCRA) in North America and similar biomedical waste management rules in the Asia-Pacific region, mandate the use of certified containers to prevent occupational exposure and environmental contamination. In the technological sphere, the Rapid Proliferation of Single-Use Medical Consumables serves as a critical driver, as the transition toward disposable drapes, gowns, and syringes necessitates a proportional increase in high-capacity infectious waste containment. Furthermore, Rising Awareness of Infection Control and Hospital-Acquired Infections (HAIs) is compelling healthcare facilities to invest in advanced, hands-free container designs that minimize physical contact during the disposal process. Together, these factors, demographic pressure, regulatory rigor, and procedural safety, ensure a robust and essential growth path for the global Medical Waste Containers Market.

AI-Native Tracking Systems and the Rise of Smart Reusable Ecosystems

A significant high-value opportunity lies in the convergence of Medical Waste Containers with the Internet of Things (IoT) and Real-Time Analytics. Next-generation intelligent bins are being developed to utilize built-in sensors that automatically alert facility management when containers reach capacity, thereby optimizing collection routes and preventing hazardous overflows. There is also a major growth frontier in the development of Advanced Reusable Container Programs with Automated Decanting and Sanitization; as hospital systems prioritize carbon footprint reduction, these high-durability systems offer a superior long-term economic profile by eliminating the recurring cost and environmental burden of single-use plastic incineration. Furthermore, the expansion of Specialized Chemotherapy and Radioactive Waste Solutions presents a lucrative opportunity, as the global rise in oncology treatments creates a demand for double-layered, vapor-resistant containers designed for aggressive hazardous solvents. Beyond the hardware, the rise of Digital Chain-of-Custody and Blockchain-Verified Disposal Records offers a unique frontier, providing healthcare organizations with tamper-proof documentation for regulatory audits. Manufacturers who focus on Ergonomic, Space-Saving Modular Designs and those pioneering Biodegradable and Bio-Composite Materials are positioned to lead the most innovative and high-margin segments of the global Medical Waste Containers Market.

05

Size and Share Analysis

Medical Waste Containers Market Size and Share Analysis

The Medical Waste Containers market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report examines subsegments categorized within type of waste, product, and end user, offering insights into their contribution to overall market performance.

Based on the type of waste subsegment, General Medical Waste holds the primary market presence, acting as the ubiquitous foundational stream which accounts for the vast majority of total healthcare refuse. This category is indispensable for the market, maintaining a significant position due to the constant generation of non-hazardous items such as packaging, office paper, and non-contaminated disposables. Hazardous, Radioactive, and Sharp Waste provide critical specialized requirements. A notable trend is the surge in the Infectious and Pathological Waste subsegment, which is registering the highest pace of adoption. This stream is becoming essential for Advanced Pathogen Isolation, as the move toward rigorous clinical hygiene and the management of high-consequence infectious diseases drives the requirement for specialized, leak-proof containment that prevents environmental exposure.

07

Report Coverage

Medical Waste Containers Market Report Coverage and Deliverables

The "Medical Waste Containers Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

- Medical Waste Containers market size and forecast at global, regional, and country levels for all market segments covered under the scope

- Medical Waste Containers market trends, as well as drivers, restraints, and opportunities

- Medical Waste Containers market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Medical Waste Containers market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Medical Waste Containers Market Geographic Insights

The geographical scope of the Medical Waste Containers market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America.

North America maintains the preeminent market position, supported by a highly structured healthcare industry and stringent regulatory oversight from agencies such as OSHA and the EPA. Europe represents a mature and highly regulated market where growth is sustained by a robust institutional focus on environmental sustainability and the implementation of strict biohazard waste ordinances. Asia Pacific is identified as the most rapidly advancing region, propelled by accelerating healthcare modernization, the expansion of hospital networks in emerging economies, and substantial public investments in infectious waste management infrastructure.

The Asia-Pacific Medical Waste Containers Market is segmented into China, Japan, South Korea, India, Australia, and the Rest of Asia Pacific. China serves as a central engine for regional expansion, driven by large-scale government programs to enhance hospital capacity and a growing demand for high-capacity, durable containment solutions. India is witnessing a notable transition as private healthcare providers and diagnostic chains expand their services, necessitating a wider adoption of standardized sharps and biohazard containers. Japan continues to prioritize innovation in specialized waste systems, focusing on the needs of its substantial geriatric population and the integration of automated waste tracking technologies.

10

Industry Activity

Recent Developments

The Medical Waste Containers market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Medical Waste Containers market are:

- In October 2025, Coveris partnered with SABIC, Zuyderland Medical Centre, and Artivion to pilot a closed-loop recycling initiative for non-contaminated hospital plastics, including polyethylene (PE) and polypropylene (PP) waste. Collected in dedicated hospital waste bags, the plastics were processed into certified circular PE and converted into new sterile medical packaging. This collaboration demonstrates a sustainable circular solution for hospital-generated plastic waste, reducing landfill reliance and supporting eco-friendly medical waste management practices.

In February 2024, Daniels Healthcare introduced SANIBOX®, a sustainable, fully compliant cardboard container for clinical waste, complementing its SHARPSGUARD®, WIVA™, and other container ranges. Available in multiple sizes and colors for different waste streams, SANIBOX® features visual closure indicators and FSC®-certified materials, providing healthcare facilities with safe, eco-friendly, and versatile waste containment solutions.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)(International Monetary Fund )IMFInternational Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations