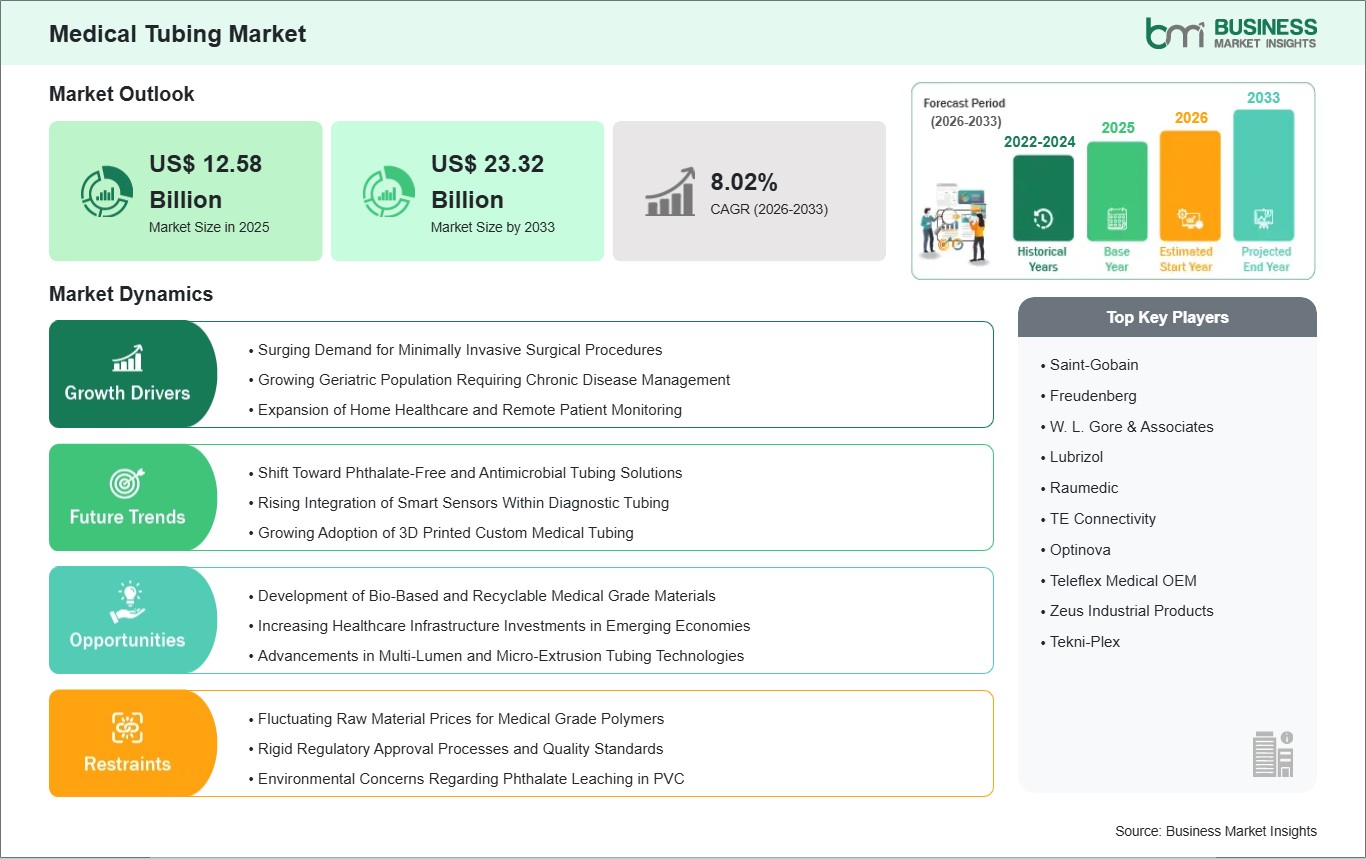

The Medical Tubing Market size is expected to reach US$ 23.32 Billion by 2033 from US$ 12.58 Billion in 2025. The market is estimated to record a CAGR of 8.02% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global Medical Tubing market is an integral part of the healthcare supply chain, as it is used as an essential medium for the management of fluids, gases, and surgical procedures. The market is presently witnessing a strong growth phase, driven by the increasing incidence rates of chronic diseases such as cardiovascular disorders and diabetes, which demand the frequent use of catheters and infusion devices. Advances in extrusion technologies have also made it possible to manufacture tubes with multiple lumens as well as micro-diameter tubes, meeting the precise needs of medical devices. While PVC-based materials dominate the market in terms of volume, there is an obvious move towards high-performance materials such as polymers and elastomers with superior biocompatibility.

The competitive landscape is characterized by a focus on material innovation and strategic partnerships between tubing manufacturers and medical device OEMs. As there is a shift in the way healthcare is delivered towards a more decentralized approach, including home care and ambulatory surgical centers, there is a growing need for user-friendly and portable tubing systems. Despite challenges in the industry, including a difficult regulatory environment as governed by the FDA and MDR regulations, as well as environmental concerns related to disposable plastic materials, the industry has shown resilience. The focus on digital innovation and material innovation is expected to continue as the main driver of industry evolution in the future.

Medical Tubing Market - Strategic Insights:

Get more information on this report

Medical Tubing Market Segmentation Analysis:

Key segments that contributed to the derivation of the Medical Tubing market analysis are material and application.

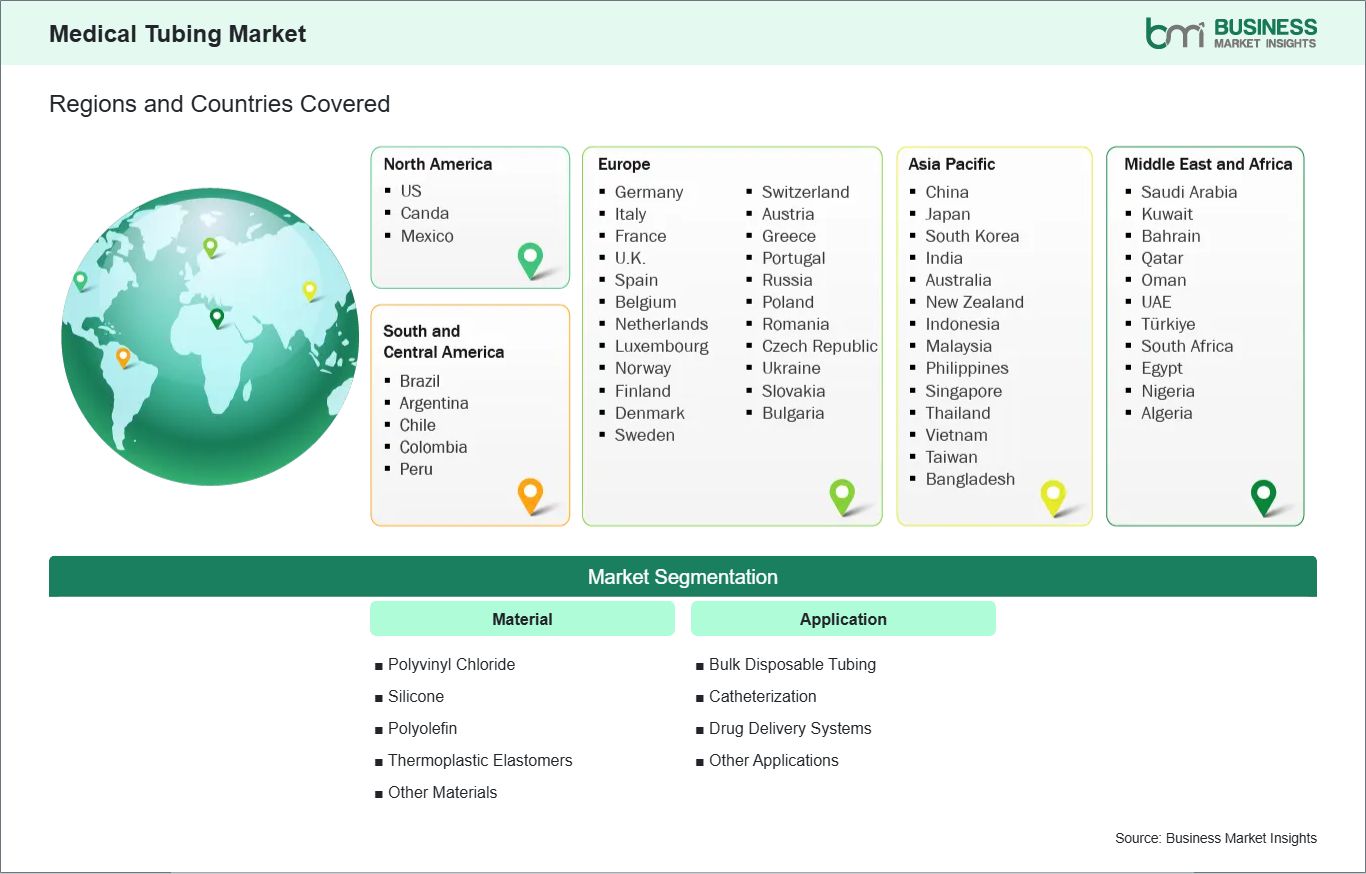

By material, the Medical Tubing market is segmented into Polyvinyl Chloride, Silicone, Polyolefin, Thermoplastic Elastomers, and Other Materials. The Polyvinyl Chloride segment dominated the market in 2025.

By application, the Medical Tubing market is segmented into Bulk Disposable Tubing, Catheterization, Drug Delivery Systems, and Other Applications. The Bulk Disposable Tubing segment dominated the market in 2025.

Medical Tubing Market Drivers and Opportunities:

Surging Demand for Minimally Invasive Surgical Procedures

The medical tubing market is experiencing significant growth driven by the global shift toward minimally invasive surgical (MIS) techniques. Modern healthcare providers and patients increasingly prefer these procedures over traditional open surgeries because they involve smaller incisions, reduced physical trauma, and significantly shorter recovery periods. This clinical transition relies heavily on the development of specialized, high-performance tubing that can navigate the complex vascular and internal pathways of the human body. As surgeons utilize more advanced endoscopic, laparoscopic, and catheter-based interventions, the demand for precision-engineered tubing with specific mechanical properties—such as kink resistance, high torqueability, and ultra-thin walls—has reached unprecedented levels.

Additionally, with the increase in MIS, there is a drive for innovation in micro-extrusions. Small-diameter tubing is now a necessity in neurovascular and cardiovascular surgery, where space is extremely limited. There is a constant demand for new technologies in this area, where there is a requirement for flexibility in tubing while still having to provide strength in the material. The constant evolution in robotic-assisted surgery is another driver in this category, as this type of surgery always needs integrated tubing for fluid management, suction, and fiber-optic sensors, etc. This trend will keep the demand for value-added, technical tubing products high, moving beyond basic fluid management.

Development of Bio-Based and Recyclable Medical Grade Materials

The medical device industry is also facing greater pressure to reduce the impact on the environment, especially with regards to the large amounts of plastic waste generated from the use of disposable products. This is an enormous opportunity for the development and commercialization of bio-based and recyclable medical-grade materials. In the past, the medical device industry has been driven by the need for sterility and performance, but with the advancements in polymer science, it is now possible to create bio-based materials that are used to create tubing while meeting the high standards required for biocompatibility and safety. The ability to create tubing that is easily identifiable, sortible, and recyclable within the medical waste stream is an important way for companies to contribute to the global sustainability agenda.

Beyond traditional recycling, there is a growing interest in chemically recyclable polymers that can be broken down into their original monomers. This allows for a closed-loop system where used medical tubing can be transformed back into high-quality medical-grade resin, bypassing the degradation typically associated with mechanical recycling. Companies that invest in green material chemistry are likely to find a receptive market among hospital systems looking to reduce their carbon footprint and comply with emerging environmental regulations. This opportunity also extends to the replacement of controversial additives, such as certain phthalates, with safer, plant-derived plasticizers, further driving the appeal of sustainable tubing solutions.

Medical Tubing Market Size and Share Analysis:

The global Medical Tubing market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within material and application highlighting their respective contributions to overall market performance.

By material, the Polyvinyl Chloride subsegment dominated the market in 2025 due to its superior balance of cost-efficiency, flexibility, and high compatibility with common sterilization methods like gamma radiation and ethylene oxide, making it the industry standard for high-volume disposable medical products.

By application, the Bulk Disposable Tubing subsegment dominated the market in 2025 because of the massive global demand for single-use consumables in hospitals, including IV sets and blood administration lines, which are essential for maintaining hygiene standards and preventing cross-contamination during routine patient care.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Saint-Gobain

Freudenberg

W. L. Gore & Associates

Lubrizol

Raumedic

TE Connectivity

Optinova

Teleflex Medical OEM

Zeus Industrial Products

Tekni-Plex

Get more information on this report

Medical Tubing Market Report Coverage and Deliverables:

The "Medical Tubing Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Medical Tubing market size and forecast at the regional and country levels for segments covered under the scope

Medical Tubing market trends, as well as drivers, restraints, and opportunities

Medical Tubing market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Medical Tubing market

Detailed company profiles, including SWOT analysis

Medical Tubing Market Geographic Insights:

The geographical scope of the Medical Tubing market report is divided into: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America maintains a dominant position in the medical tubing market, primarily due to its sophisticated healthcare infrastructure and the presence of a large number of global medical device manufacturers. The United States, in particular, serves as a hub for research and development, where significant investments are made into advanced catheter technologies and drug delivery systems. The region's high healthcare expenditure and the early adoption of minimally invasive surgical techniques further drive the demand for specialized tubing products. Furthermore, well-established regulatory pathways provided by the FDA ensure that high-quality and safe products are consistently introduced to the market, instilling confidence in both clinicians and patients.

The dominance is also reinforced by an aging population that requires frequent medical interventions and long-term care. This demographic trend sustains a high volume of demand for bulk disposable tubing and specialized home-use medical kits. While manufacturing costs in the region can be higher than in emerging markets, the focus on high-value, technical tubing such as those used in neurology and cardiology, ensures that North America remains the revenue leader. Additionally, the region is at the forefront of the shift toward PVC-free and phthalate-free alternatives, as healthcare providers increasingly prioritize patient safety and environmental sustainability in their procurement processes.

Get more information on this report

Medical Tubing Market Research Report Guidance:

The report includes qualitative and quantitative data in the Medical Tubing market across material, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Medical Tubing market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Medical Tubing market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Medical Tubing market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 9 cover the Medical Tubing market segments by material, application, and geography across North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 10 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 11 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 12 provides detailed profiles of the major companies operating in the Medical Tubing market. Companies have been profiled on the basis of their key facts, business descriptions, process types, financial overview, SWOT analysis, and key developments.

Chapter 13, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Medical Tubing Market News and Key Development:

The Medical Tubing market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Medical Tubing market are:

In October 2025, Medical Extrusion Technologies Inc., announced the launch of an online shop offering FEP heat shrink tubing and precision extrusion products, aimed at improving accessibility and traceability for medical device manufacturers.

In June 2025, Medical Extrusion Technologies Inc., highlighted advancements in extractables and leachables testing for medical tubing materials, supporting improved safety and compliance in medical device manufacturing.

In 2025, Junkosha Inc., announced that it significantly expanded its medical tubing production capacity, including doubling capacity for peelable heat shrink tubing and liner products to meet rising demand in medical devices.

Key Sources Referred:

American Chemistry Council (ACC)International Council of Chemical Associations (ICCA)European Chemical Industry Council (Cefic)China National Building Materials Group (CNBM)Indian Minerals & Granite Exporters Association (IMGEA)Japan Mining Industry Association (JMIA)Brazilian Mining Association (IBRAM)Gulf Petrochemicals and Chemicals Association (GPCA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the Medical Tubing Market?

The Medical Tubing Market is valued at US$ 12.58 Billion in 2025, it is projected to reach US$ 23.32 Billion by 2033.

What is the CAGR for Medical Tubing Market by (2026 - 2033)?

As per our report Medical Tubing Market, the market size is valued at US$ 12.58 Billion in 2025, projecting it to reach US$ 23.32 Billion by 2033. This translates to a CAGR of approximately 8.02% during the forecast period.

What segments are covered in this report?

The Medical Tubing Market report typically cover these key segments-

Material (Polyvinyl Chloride, Silicone, Polyolefin, Thermoplastic Elastomers, Other Materials)

Application (Bulk Disposable Tubing, Catheterization, Drug Delivery Systems, Other Applications)

What is the historic period, base year, and forecast period taken for Medical Tubing Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Medical Tubing Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Medical Tubing Market?

The Medical Tubing Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Saint-Gobain

Freudenberg

W. L. Gore & Associates

Lubrizol

Raumedic

TE Connectivity

Optinova

Teleflex Medical OEM

Zeus Industrial Products

Tekni-Plex

Who should buy this report?

The Medical Tubing Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Medical Tubing Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Medical Tubing Market

Get Free Sample For Medical Tubing Market