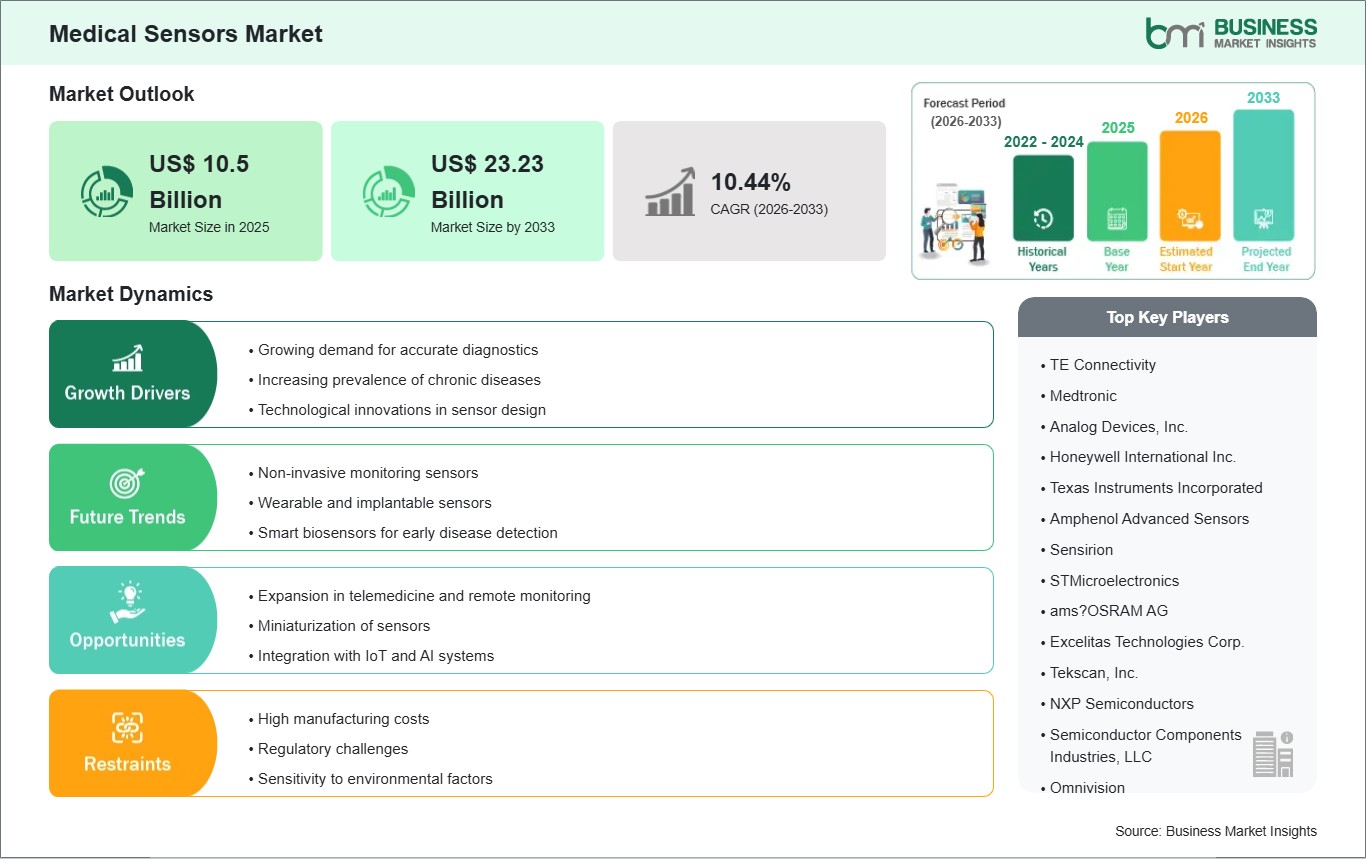

The Medical Sensors Market size is expected to reach US$ 23.23 Billion by 2033 from US$ 10.5 Billion in 2025. The market is estimated to record a CAGR of 10.44% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Medical sensors play a critical role in modern healthcare, enabling precise monitoring, diagnostics, and therapeutic interventions across a wide range of medical applications. They are essential for sectors such as hospitals, clinics, home healthcare, diagnostics, chronic disease management, and remote patient monitoring. Medical sensors offer several advantages, including accurate and real-time data collection, early disease detection, improved patient outcomes, and seamless integration with digital health platforms. Increasing prevalence of chronic diseases, growing adoption of telemedicine, and rising demand for personalized healthcare solutions are fueling the market. Additionally, innovations in sensor technology, miniaturization, wireless connectivity, and artificial intelligence are enhancing device functionality, reliability, and data analytics capabilities.

However, several challenges can restrain market growth, such as high manufacturing costs, strict regulatory compliance requirements, integration complexities with existing healthcare IT systems, and concerns over data privacy and cybersecurity. The industry is also sensitive to technological limitations, accuracy issues, and disparities in healthcare infrastructure across regions. Despite these hurdles, the market holds significant opportunities driven by rising demand for remote patient monitoring, expansion of digital health initiatives in emerging economies, and increasing adoption of wearable and connected medical devices. Investment in advanced AI-enabled sensors, continuous monitoring solutions, and smart healthcare platforms is also expected to open new avenues for market expansion, further positioning medical sensors as a cornerstone of the global digital healthcare ecosystem.

Medical Sensors Market - Strategic Insights:

Get more information on this report

Medical Sensors Market Segmentation Analysis:

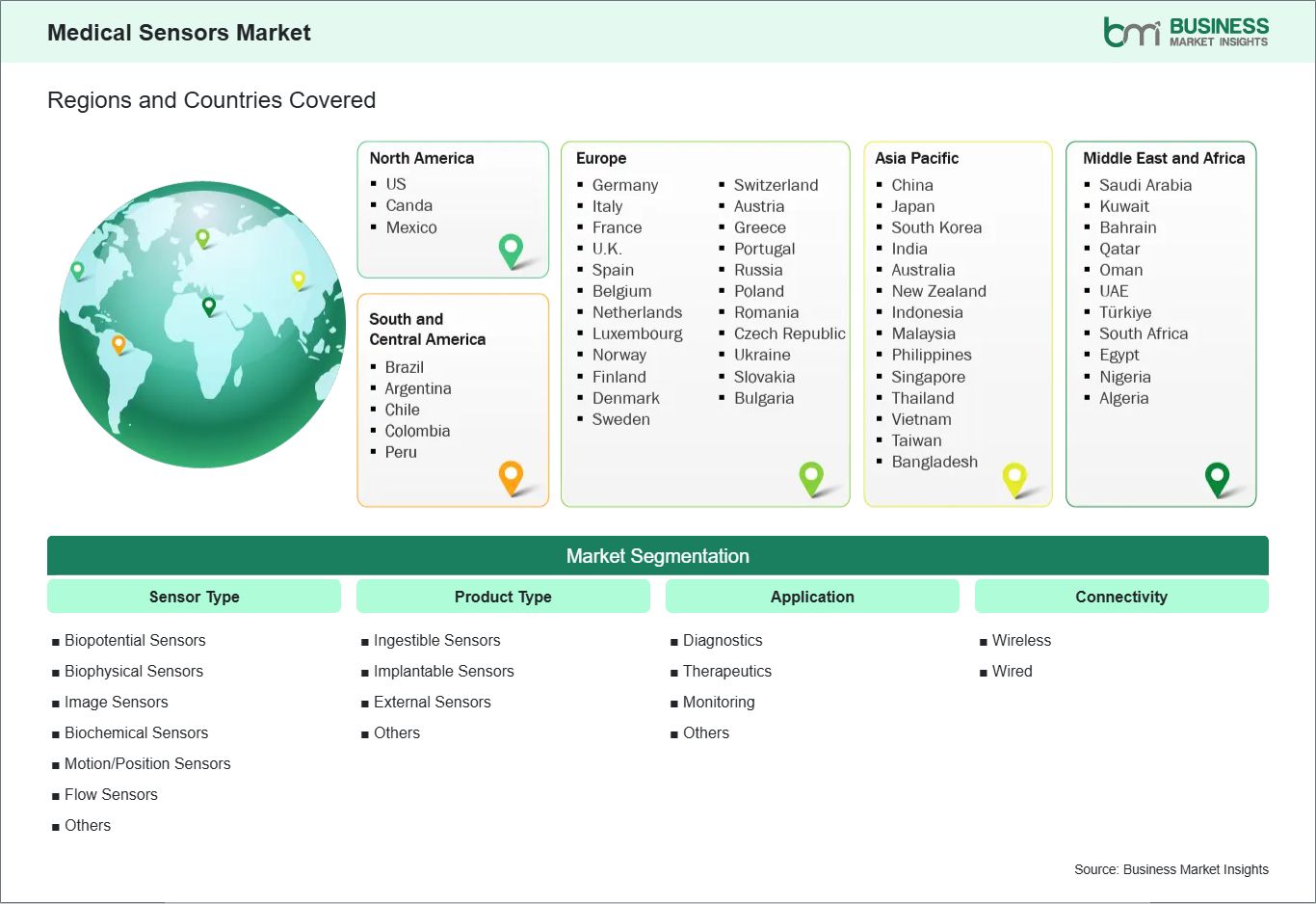

Key segments that contributed to the derivation of the Medical Sensors market analysis are Sensor Type, Product Type, Application, Connectivity, Technology, End User.

By Sensor Type, the Medical Sensors market is segmented into Biopotential Sensors, Biophysical Sensors, Image Sensors, Biochemical Sensors, Motion/Position Sensors, Flow Sensors, Others.

By product type, the market is segmented into Ingestible Sensors, Implantable Sensors, External Sensors (Non-Invasive), Others. The External Sensors (Non-Invasive) segment held the largest share of the market in 2025.

By application, the market is segmented into Diagnostics, Therapeutics, Monitoring, Others. The Diagnostics segment held the largest share of the market in 2025.

By connectivity, the market is segmented into Wired and Wireless. The Wireless segment held the largest share of the market in 2025.

By technology, the market is segmented into Micro-Electro-Mechanical Systems (MEMS), Complementary Metal-Oxide-Semiconductor (CMOS), Nano/Graphene-Based Sensors, Fiber-Optic Sensors, Piezoelectric Sensors, Others. The MEMS segment held the largest share of the market in 2025.

By end user, the market is segmented into Hospitals & Clinics, Nursing Homes, Assisted Living Facilities, Long-Term Care Centers, Home Care Settings, Others. The Hospitals & Clinics segment held the largest share of the market in 2025

Medical Sensors Market Drivers and Opportunities:

Escalating Burden of Chronic Diseases and Aging Populations

The market for Medical Sensors is driven by the never-ending increase of chronic diseases and the fast aging of population all over the world that hotly demand medical monitoring with the help of these devices continuously, in real-time to get the most out of this monitoring through early detection, personalized management, and a less strained healthcare system. The U.S. Centers for Disease Control and Prevention (CDC, 2024) reports that chronic diseases affect 194 million adults in the U.S. which is 76.4% of the adult population, diabetes alone being the cause of 37 million people affected and heart-related conditions causing 695,000 annual deaths. This is the case globally, as the World Health Organization (WHO, 2024) has stated that the number of people dying from non-communicable diseases is 41 million a year, which is 74% of total global mortality, and these deaths are mainly due to cardiovascular diseases, diabetes, cancers, and respiratory diseases.

The aging population puts even more pressure on the situation. The U.S. Census Bureau (2024) stated that there were 61.2 million people who were aged 65 and above, which is a 3.1% rise compared to 2023, while the World Health Organization (2024) predicts that by 2050, one in every six people in the world will be above 65 years, which is an increase from one in eleven in 2019. In America, 93% of the elderly have at least one chronic disease (CDC, 2024), consequently, it is the case that there are a lot of sensors for monitoring glucose, blood pressure, heart rate, oxygen saturation, and activity levels that need to be placed in such people for comprehensive monitoring continuously.

The latest regulatory steps taken signify this fast-paced development. In January 2025, the U.S. Food and Drug Administration (FDA, 2025), approved the new version of the Dexcom G7 continuous glucose monitoring system containing electrochemical sensors that are smaller, accurate, and are intended for the 7.3 million U.S. diabetes patients (CDC, 2024). Likewise, the European Medicines Agency (EMA, 2024) allowed Abbott’s FreeStyle Libre 3 sensor for real-time glucose monitoring to be upgraded to the latest, thereby covering the 60 million diabetes patients in Europe. The National Institutes of Health (NIH, 2025) has also provided grants amounting to more than 20 projects for implantable cardiac sensors, including bioresorbable pressure monitors, which are aimed at reducing heart failure readmissions that affect 6.7 million adults in the U.S. every year (CDC, 2024).

These overlapping factors i.e. chronic disease epidemic, population aging, and regulation approval of advanced monitoring technologies, have set medical sensors as the main element of the healthcare transformation that is already pro-active and data-driven.

Advancements in Wearable and Implantable Sensor Technologies

The Medical Sensors market is very attractive and is supported by the quick adoption of sophisticated wearable and implantable sensor technologies that make it possible to monitor vital physiological parameters in real-time and continuously, thus changing the landscape of chronic disease management and preventive healthcare. The Statistics of the U.S. Centers for Disease Control and Prevention (CDC, 2024) show that almost 76.4% of the adult population is affected by chronic diseases in the US., which means 194 million adults are in the group. Diabetes, in particular, is the underlying cause for 37 million persons and is also responsible for a large part of the healthcare expenses due to complications resulting from diabetes. This situation is replicated on a global scale. The World Health Organization (WHO, 2024) reports that non-communicable diseases account for 41 million deaths annually, among which are cardiovascular diseases and diabetes, which lead to an increased need for sensors that perform non-invasive monitoring of glucose, heart rate, oxygen saturation, and blood pressure.

Amongst the several scenarios, one of the most prominent ones is the U.S. Food and Drug Administration (FDA, 2025) sanctioning of the Dexcom G7 Continuous Glucose Monitoring (CGM) system's expansion in January 2025. The new system uses electronic sensors that are very small and very accurate and it is expected to serve over 7.3 million U.S. diabetes patients as per CDC data. Along with this, the European Medicines Agency (EMA, 2024) in Europe granted approval for Abbott's FreeStyle Libre 3 sensor upgrades which offer real-time interstitial glucose monitoring and are now available for the whole of Europe with its 60 million diabetes cases. More than that, the National Institutes of Health (NIH, 2025) has provided funds for more than 20 projects for implantable cardiac sensors that will include bioresorbable pressure monitors that would help in reducing heart failure readmissions—a problem that affects 6.7 million U.S. adults every year according to CDC (2024) reports.

The combination of these advancements along with the factors like miniaturization, AI-powered analytics, and wireless connectivity, the creation of personalized, remote patient monitoring is facilitated hence hospital visits are minimized and the outcome is better in the case of the elderly people. The partnership of regulatory support, technological advancement, and rising chronic diseases puts medical sensors atop as a major enabler of the next-generation healthcaredelivery system

Medical Sensors Market Size and Share Analysis:

By Sensor Type, the Medical Sensors market is segmented into Biopotential Sensors, Biochemical Sensors, Motion/Position Sensors, Flow Sensors, Biophysical Sensors, Image Sensors, Others. The Biopotential Sensors segment dominated the market in 2025. Biopotential sensors dominate due to widespread clinical applications in ECG, EEG, and EMG monitoring, essential for diagnosing cardiovascular, neurological, and muscular disorders globally.

By product type, the market is segmented into Ingestible Sensors, Implantable Sensors, External Sensors (Non-Invasive), Others. The External Sensors (Non-Invasive) segment held the largest share of the market in 2025. Non-invasive sensors lead because they are safer, easy to use, widely adopted for continuous monitoring, and compatible with wearable and home healthcare devices.

By application, the market is segmented into Diagnostics, Therapeutics, Monitoring, Others. The Diagnostics segment held the largest share of the market in 2025. Diagnostics dominate as early detection and disease monitoring are critical, driving high adoption of sensors for accurate testing and patient health assessment across hospitals and labs.

By connectivity, the market is segmented into Wired and Wireless. The Wireless segment held the largest share of the market in 2025. Wireless sensors lead due to convenience, remote monitoring capabilities, integration with telehealth platforms, and rising demand for real-time patient data without physical connectivity constraints.

By technology, the market is segmented into Micro-Electro-Mechanical Systems (MEMS), Complementary Metal-Oxide-Semiconductor (CMOS), Nano/Graphene-Based Sensors, Fiber-Optic Sensors, Piezoelectric Sensors, Others. The MEMS segment held the largest share of the market in 2025. MEMS technology dominates because of miniaturization, high sensitivity, low power consumption, cost-effectiveness, and wide applications in wearable, implantable, and diagnostic healthcare devices.

By end user, the market is segmented into Hospitals & Clinics, Nursing Homes, Assisted Living Facilities, Long-Term Care Centers, Home Care Settings, Others. The Hospitals & Clinics segment held the largest share of the market in 2025. Hospitals and clinics dominate as primary end users due to high patient volumes, need for continuous monitoring, clinical validation requirements, and investment in advanced medical sensor technologies.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

TE Connectivity

Medtronic

Analog Devices, Inc.

Honeywell International Inc.

Texas Instruments Incorporated

Amphenol Advanced Sensors

Sensirion

STMicroelectronics

ams?OSRAM AG

Excelitas Technologies Corp.

Tekscan, Inc.

NXP Semiconductors

Semiconductor Components Industries, LLC

Omnivision

Nihon Kohden Corporation

Get more information on this report

Medical Sensors Market Report Coverage and Deliverables:

The "Medical Sensors Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Medical Sensors market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Medical Sensors market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Medical Sensors market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Medical Sensors market

Detailed company profiles, including SWOT analysis

Medical Sensors Market Geographic Insights:

The geographical scope of the Medical Sensors market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The Medical Sensors market in Asia Pacific is expected to grow significantly during the forecast period.

The Asia-Pacific Medical Sensors market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. The market in the Asia-Pacific region is experiencing strong growth, which is largely due to the increase in the number of chronic diseases, the rise of the elderly population, and the growing use of wearable and remote monitoring devices. The largest and the most populous countries in Asia, China and India, are the main drivers of this market growth. They are investing in the healthcare sector, modernizing hospitals, and making people more aware of the importance of preventive care.

The area is also increasing the use of modern sensor technologies such as health monitoring through AI, IoMT integration, wireless biosensors plus smart diagnostic devices—in particular, these are appropriate for diabetes management, cardiovascular monitoring, and critical care. The healthcare facility expansion coupled with a hospital and diagnostic center modernization is improving both operational efficiency and patient output. Furthermore, the booming telehealth adoption, the provision of home healthcare, and the digital health platforms are giving Asia-Pacific an impressive position as a major player in the global medical sensors ecosystem. The government initiatives, pro-healthcare policies, and the growing healthcare budget are the factors that further reinforce the region’s stronghold in the market

Get more information on this report

Medical Sensors Market Research Report Guidance:

The report includes qualitative and quantitative data in the Medical Sensors market across Sensor Type, Product Type, Application, Connectivity, Technology, End User, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Medical Sensors market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Medical Sensors market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Medical Sensors market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Medical Sensors market segments by Sensor Type, Product Type, Application, Connectivity, Technology, End User, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market volume revenue forecast and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Medical Sensors market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix is inclusive of a brief overview of the company, list of abbreviations, and disclaimer

Medical Sensors Market News and Key Development:

The Medical Sensors market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Medical Sensors market are:

In December 2025, JSA Advocates & Solicitors advised MO Alternates in its acquisition of a ‘significant minority stake’ in the medical diagnostic equipment manufacturer, Sensa Core Medical Instrumentation Private Limited (“Sensa Core”), through a combination of primary infusion and secondary purchase of shares.

In December 2025, Royal Philips, a global leader in health technology announced it has entered into an agreement to acquire SpectraWAVE, Inc., an innovator in Enhanced Vascular Imaging (EVI) of coronary arteries, angiography-based physiology assessments, and the use of AI in medical imaging.

In December 2025, Medtronic, a global leader in healthcare technology, announced the broad U.S. commercial launch of the MiniMed™ 780G system integrated with the Instinct sensor, made by Abbott and designed exclusively for MiniMed™ systems. Following U.S. FDA clearance of the system earlier this year to enable integration with the Instinct sensor, the system is now shipping to customers across the U.S., marking a major milestone in diabetes technology and delivering a smart, seamless way to manage diabetes

Key Sources Referred:

World Bank – Global Trade IndicatorsAmerican Medical Association (AMA)National Center for Biotechnology Information (NCBI)National Library of Medicine (NLM)Centers for Disease Control and Prevention (CDC)Company websiteNational Institutes of Health (NIH)International Hospital Federation (IHF)Company annual reportsCompany investor presentations

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the Medical Sensors Market?

The Medical Sensors Market is valued at US$ 10.5 Billion in 2025, it is projected to reach US$ 23.23 Billion by 2033.

What is the CAGR for Medical Sensors Market by (2026 - 2033)?

As per our report Medical Sensors Market, the market size is valued at US$ 10.5 Billion in 2025, projecting it to reach US$ 23.23 Billion by 2033. This translates to a CAGR of approximately 10.44% during the forecast period.

What segments are covered in this report?

The Medical Sensors Market report typically cover these key segments-

What is the historic period, base year, and forecast period taken for Medical Sensors Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Medical Sensors Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Medical Sensors Market?

The Medical Sensors Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

TE Connectivity

Medtronic

Analog Devices, Inc.

Honeywell International Inc.

Texas Instruments Incorporated

Amphenol Advanced Sensors

Sensirion

STMicroelectronics

ams?OSRAM AG

Excelitas Technologies Corp.

Tekscan, Inc.

NXP Semiconductors

Semiconductor Components Industries, LLC

Omnivision

Nihon Kohden Corporation

Innovative Sensor Technology IST AG

CTS Corporation

ROHM Co., Ltd.

Who should buy this report?

The Medical Sensors Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Medical Sensors Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Medical Sensors Market

Get Free Sample For Medical Sensors Market