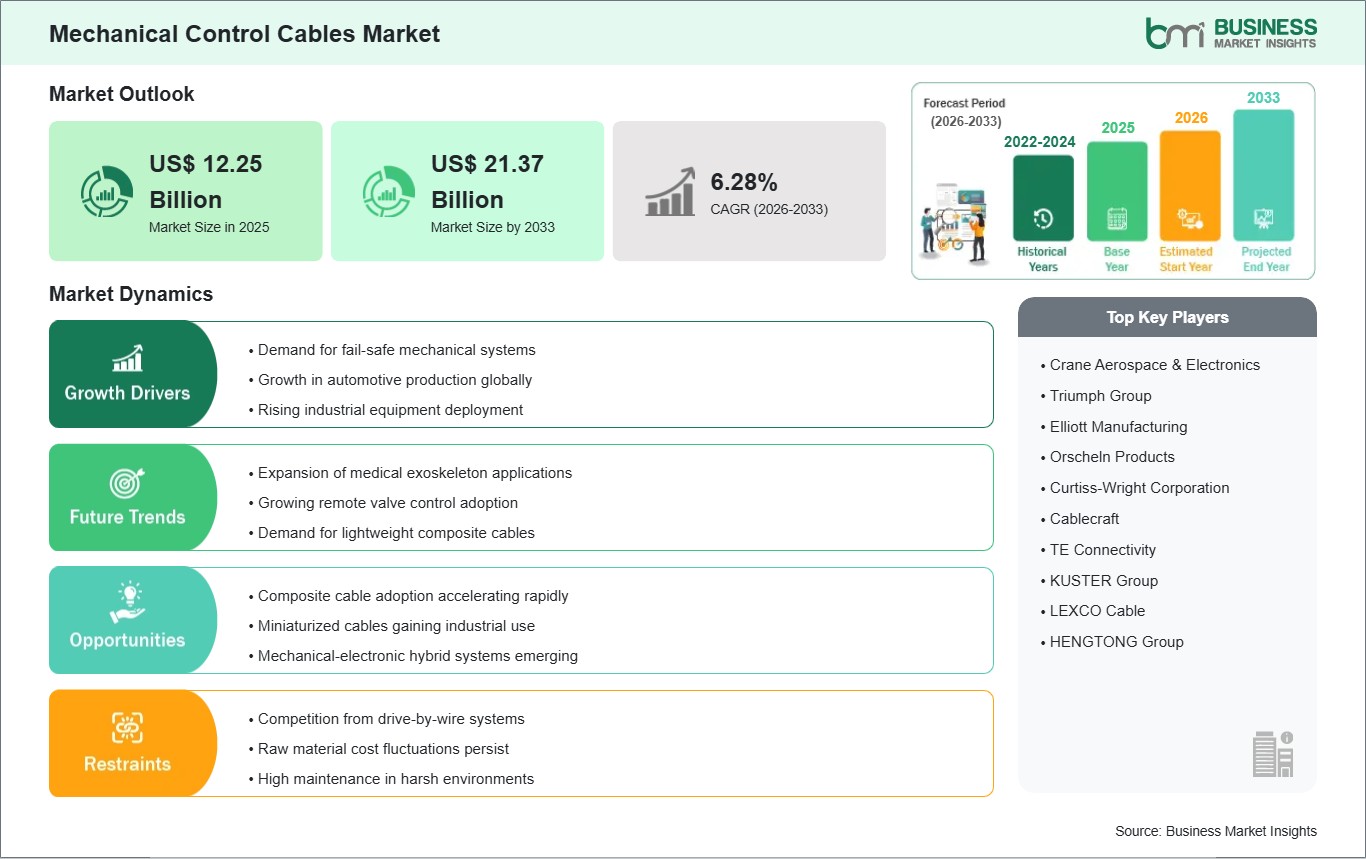

The mechanical control cable market size is expected to reach US$ 21.37 Billion by 2033 from US$ 12.25 Billion in 2025. The market is estimated to record a CAGR of 6.28% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Mechanical control cables are flexible motion-transmission assemblies that convert manual or mechanical input into precise linear or rotary actuation. They are used where dependable force transfer, routing flexibility, and compact installation are essential. These systems support throttle, braking, clutch, latch, steering, and auxiliary functions across equipment platforms that operate under vibration, load variation, and demanding environmental conditions.

Market momentum is shaped by the need for durable control architectures in automotive systems, aircraft subsystems, marine mechanisms, and industrial equipment. Manufacturers continue to prioritize reliable actuation components that simplify packaging while preserving tactile response and operational accuracy. Replacement demand also supports the industry, especially in applications where serviceability and long product life remain more practical than full electronic conversion.

Segment performance reflects varied usage conditions and control requirements. Push-Pull Cables retain broad relevance because they enable bidirectional motion in compact layouts. Pull-Only Cables remain well aligned with release and engagement functions, while Micro-Diameter Cables address constrained assemblies that require reduced mass and tighter bend capability. Across end users, automotive sustains strong volume requirements, while aerospace and marine prioritize precision, durability, and routing efficiency.

Technology development is advancing through material engineering, lower-friction liners, improved sealing, and tighter tolerance construction. Stainless steel remains important where corrosion resistance and fatigue performance are critical, while composite and hybrid constructions support weight reduction and tailored strength profiles. Design refinement is also improving installation flexibility, control smoothness, and lifecycle stability in equipment exposed to moisture, contamination, or repetitive load cycles.

Competitive conditions are defined by engineering capability, customization speed, manufacturing consistency, and long-term supply relationships. Participants differentiate through application-specific design support, regional production access, and performance validation across demanding operating environments. The market also reflects a balance between high-volume standardized programs and specialized assemblies, creating room for suppliers that can combine scale, responsiveness, and product reliability without compromising mechanical accuracy.

Mechanical Control Cables Market - Strategic Insights:

Get more information on this report

Mechanical Control Cables Market Segmentation Analysis:

The mechanical control cable market is segmented by Type, End User, and Material. The structure reflects differing motion requirements, durability needs, and platform-specific installation constraints.

By Type

Push-Pull Cables : Support bidirectional motion in compact mechanical layouts.

Pull-Only Cables : Suit release, engagement, and single-direction actuation tasks.

Micro-Diameter Cables : Fit constrained assemblies requiring reduced mass and tighter routing.

By End User

Automotive : Maintains broad deployment across throttle, brake, hood, and seat mechanisms.

Aerospace and Defense : Requires precise actuation under strict reliability conditions.

Marine : Benefits from corrosion-resistant assemblies and dependable routing flexibility.

Industrial : Serves machinery controls where rugged operation and serviceability matter.

Agriculture : Supports durable motion transfer in harsh outdoor operating environments.

Construction : Handles repetitive control inputs in heavy-duty mobile equipment.

Others : Covers specialized platforms with custom mechanical interface requirements.

By Material

Stainless Steel : Delivers fatigue strength and corrosion resistance for demanding assemblies.

Composite Materials : Reduce weight while supporting tailored flexibility characteristics.

Hybrid Materials : Balance durability, mass reduction, and application-specific performance targets.

Mechanical Control Cables Market Drivers and Opportunities:

Higher Equipment Reliability Requirements Across Mobile and Industrial Platforms

Operators across transport, industrial, and off-highway applications are prioritizing components that maintain consistent motion transfer under repeated mechanical stress. That requirement increases the need for cable systems with stable actuation, predictable response, and resistance to wear, contamination, and routing complexity. Mechanical control cables continue to gain preference where equipment designers need dependable control performance without introducing unnecessary architectural complexity or maintenance burden.

The effect is most visible in systems where uptime, operator feedback, and installation flexibility directly influence equipment usability. This context keeps mechanical control cables relevant across established vehicle and machinery categories, particularly where harsh conditions challenge electronic alternatives. Their continued relevance stems from proven field performance, straightforward replacement practices, and compatibility with platform designs that still depend on robust mechanical actuation pathways.

Material Innovation Supporting Lightweight and Application-Specific Cable Design

Material development is opening new possibilities for cable assemblies that must meet tighter packaging, corrosion resistance, and weight objectives. Composite layers, hybrid constructions, and improved liner technologies are enabling smoother motion, lower friction, and better environmental durability. These innovations are particularly useful in aerospace, marine, and compact industrial systems where conventional cable designs may limit routing efficiency or increase maintenance exposure.

Future scope for these innovations extends into broader customization, longer service life, and improved platform integration across diverse end users. As product developers refine cable architectures for specialized loads and environmental conditions, the industry can address more exact performance targets without sacrificing manufacturability. That expansion supports differentiated offerings, deeper penetration in engineered applications, and stronger value creation through application-tuned mechanical control solutions.

Mechanical Control Cables Market Size and Share Analysis:

The mechanical control cable market size is expected to reach US$ 21.37 Billion by 2033 from US$ 12.25 Billion in 2025. The market is estimated to record a CAGR of 6.28% from 2026 to 2033. This trajectory reflects continued relevance in motion-transfer applications where precision, durability, and installation flexibility remain essential. Demand is supported by established use across transportation, industrial equipment, and specialized machinery platforms that continue to rely on engineered mechanical actuation.

By segment, Push-Pull Cables hold a prominent position because they accommodate dual-direction control in compact assemblies. Stainless Steel also retains broad acceptance due to its balance of strength, corrosion resistance, and lifecycle stability. Among end users, automotive sustains leading demand through extensive integration of control cable assemblies in functional systems that require repeatable motion and cost-efficient serviceability.

Application leadership remains centered on automotive usage, where mechanical control cables support a wide range of actuation functions across internal and auxiliary systems. Aerospace and Defense, Marine, and Industrial applications also maintain strong relevance because they value routing flexibility and dependable force transmission. Agriculture and Construction further reinforce market breadth through equipment categories that continue to favor rugged mechanical control architectures.

Mechanical Control Cables Market Report Highlights:

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Crane Aerospace & Electronics

Triumph Group

Elliott Manufacturing

Orscheln Products

Curtiss-Wright Corporation

Cablecraft

TE Connectivity

KUSTER Group

LEXCO Cable

HENGTONG Group

Get more information on this report

Mechanical Control Cables Market Report Coverage and Deliverables:

The report provides a detailed analysis of the market covering the below areas:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Mechanical Control Cables Market Geographic Insights:

The mechanical control cable market shows diverse regional adoption patterns influenced by manufacturing depth, equipment mix, platform design preferences, and replacement cycles. Across the global landscape, demand reflects the continued use of cable-based actuation in transportation, machinery, and equipment systems that prioritize durable motion transfer. Regional performance therefore depends less on a single demand source and more on how each market balances industrial output, mobility production, and engineering requirements.

North America remains important because its equipment base includes mature automotive, aerospace, and industrial programs that still require dependable mechanical interfaces. The region also benefits from aftermarket activity and replacement demand tied to long operating lifecycles. Design emphasis often centers on reliability, compliance, and performance consistency, which supports suppliers capable of delivering customized assemblies for demanding applications across mobile equipment and specialized machinery.

Asia Pacific presents a broad expansion environment supported by large-scale vehicle manufacturing, rising equipment output, and an extensive supplier ecosystem. The region's role is strengthened by its combination of volume production and evolving engineering capability, allowing both standardized and application-specific cable systems to advance. Demand is particularly well positioned in automotive and industrial settings, while agriculture and construction equipment create additional space for rugged mechanical control solutions.

Europe maintains relevance through precision engineering standards, diversified mobility manufacturing, and sustained use of specialized control assemblies in automotive and industrial equipment. Emerging markets in the Middle East, Africa, and South and Central America contribute through marine activity, construction equipment demand, agricultural mechanization, and industrial modernization. Together, these regions broaden the market's application base and create opportunities for suppliers offering corrosion resistance, durability, and tailored routing performance.

Get more information on this report

Mechanical Control Cables Market Research Report Guidance:

The report includes qualitative and quantitative data in the Mechanical Control Cable market across Type, End User, Material and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Mechanical Control Cable market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Mechanical Control Cable market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Mechanical Control Cable market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Mechanical Control Cable market segments by Type, End User, Material and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Mechanical Control Cable market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Mechanical Control Cables Market News and Key Development:

Recent developments indicate continued strategic movement across the mechanical control cable industry. Market activity reflects consolidation, footprint optimization, and capability expansion aligned with global supply requirements.

In April 2026, SIKORA, a member of the MAAG Group and Dover (NYSE: DOV), has unveiled three new solutions aimed at enhancing quality control, boosting production efficiency, and minimizing material consumption in cable and wire manufacturing. The new offerings include an expanded LASER PRO diameter measurement series, the X-RAY 6000 measurement system, and the LM PRO length measurement system.

In October 2025, JAE has started sales of the MX34T variant, a through-hole reflow compatible version of its compact, high-density, non-waterproof connectors designed for automotive applications. Through-hole reflow, also known as Pin In Paste, involves inserting the connector's through-hole components into PCB through-hole openings and soldering them using the reflow process. This method enables simultaneous mounting with other SMT components, providing strong mechanical performance and high mass-production efficiency.

Key Sources Referred:

World Bank -Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Mechanical Control Cables Market

Crane Aerospace & Electronics

Triumph Group

Elliott Manufacturing

Orscheln Products

Curtiss-Wright Corporation

Cablecraft

TE Connectivity

KUSTER Group

LEXCO Cable

HENGTONG Group

About Author— Electronics and Semiconductor Research Team

Siddhika is an experienced market research professional with over five years of expertise in delivering actionable market intelligence and strategic insights to support business growth and decision-making. She has strong experience in designing and managing end-to-end research engagements, including research planning, data collection, and insight generation.

Proficient in research methodologies, Siddhika synthesizes diverse information sources to deliver accurate, high-quality insights and strategic recommendations. She excels at translating complex market information into strategic narratives that support executive decision-making..

Frequently Asked Questions

How big is the Mechanical Control Cables Market?

The Mechanical Control Cables Market is valued at US$ 12.25 Billion in 2025, it is projected to reach US$ 21.37 Billion by 2033.

What is the CAGR for Mechanical Control Cables Market by (2026 - 2033)?

As per our report Mechanical Control Cables Market, the market size is valued at US$ 12.25 Billion in 2025, projecting it to reach US$ 21.37 Billion by 2033. This translates to a CAGR of approximately 6.28% during the forecast period.

What segments are covered in this report?

The Mechanical Control Cables Market report typically cover these key segments-

Type (Push-Pull Cables, Pull-Only Cables, Micro-Diameter Cables)

End User (Automotive, Aerospace and Defense, Marine, Industrial, Agriculture, Construction)

Material (Stainless Steel, Composite Materials, Hybrid Materials)

What is the historic period, base year, and forecast period taken for Mechanical Control Cables Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Mechanical Control Cables Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Mechanical Control Cables Market?

The Mechanical Control Cables Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Crane Aerospace & Electronics

Triumph Group

Elliott Manufacturing

Orscheln Products

Curtiss-Wright Corporation

Cablecraft

TE Connectivity

KUSTER Group

LEXCO Cable

HENGTONG Group

Who should buy this report?

The Mechanical Control Cables Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Mechanical Control Cables Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Mechanical Control Cables Market

Get Free Sample For Mechanical Control Cables Market