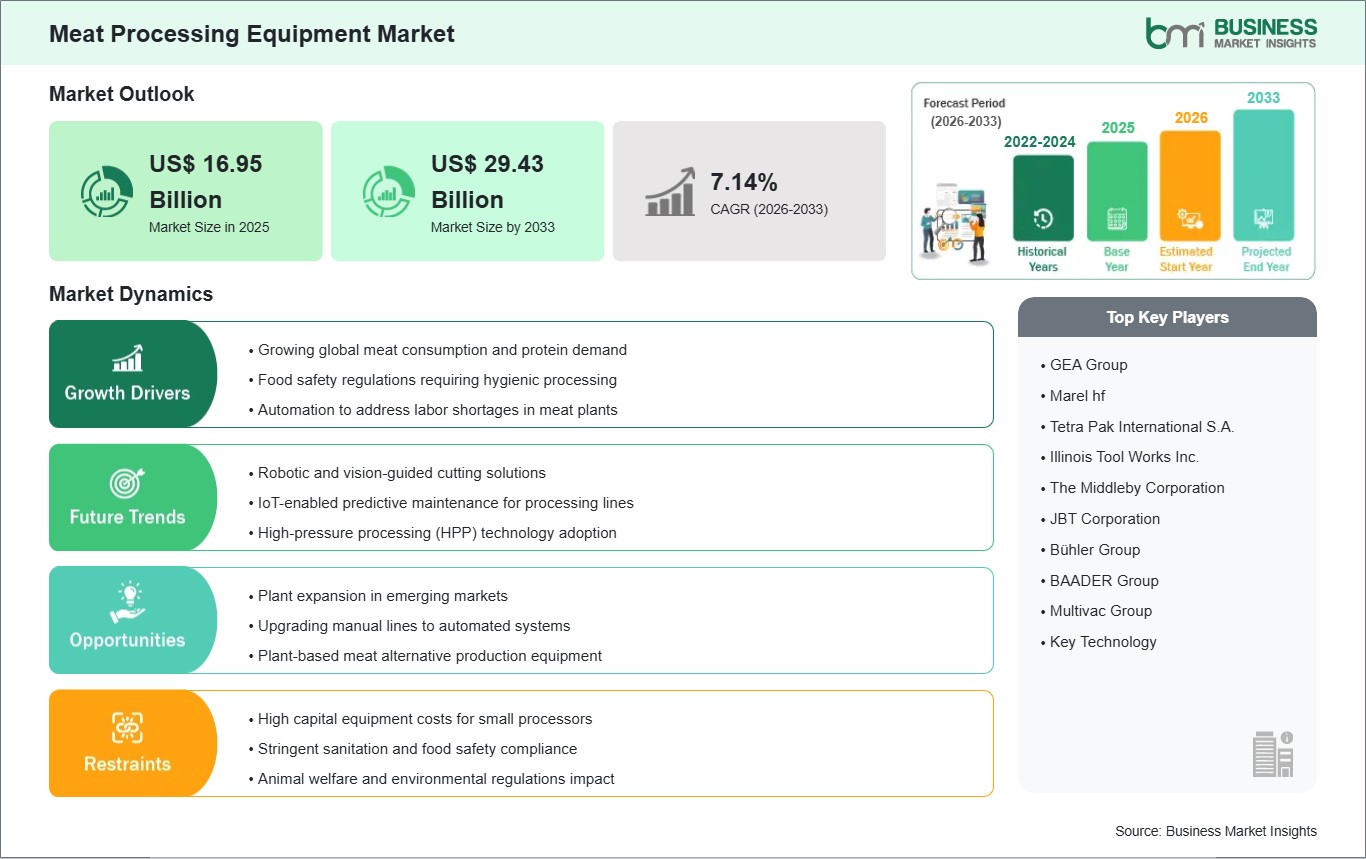

The Meat Processing Equipment market size is expected to reach US$ 29.43 Billion by 2033 from US$ 16.95 Billion in 2025. The market is estimated to record a CAGR of 7.14% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Meat processing equipment comprises engineered systems that cut, grind, blend, fill, tenderize, smoke, and cook animal protein under controlled production conditions. These machines support throughput consistency, hygiene control, and recipe precision across primary and secondary processing lines. Their role extends beyond mechanical handling, as processors rely on them to maintain texture, portion uniformity, and thermal performance across high-volume operations.

Market momentum reflects the need for efficient protein handling, tighter food safety execution, and greater line reliability in labor-constrained environments. Processors are modernizing plant layouts to reduce manual intervention, standardize yields, and improve sanitation outcomes. As product portfolios widen across chilled, cooked, marinated, and value-added formats, equipment selection increasingly centers on flexibility, uptime, and process control.

Segment positioning highlights broad demand across product type, automation level, meat type, and end-user environments. Cutting and grinding systems remain foundational because they shape upstream material preparation for downstream forming and cooking stages. Automatic configurations attract large processors seeking repeatable performance, while semi-automatic and manual formats remain relevant where batch diversity, plant scale, or capital priorities differ.

Technology development is shifting equipment design toward integrated controls, washdown-ready construction, and smarter monitoring across critical processing stages. Manufacturers are refining servo-driven filling, programmable mixing, and thermal systems that support recipe accuracy with reduced giveaway. This evolution is improving changeover efficiency and reinforcing traceable production workflows in facilities balancing output targets with compliance requirements.

Competitive conditions remain centered on equipment breadth, application expertise, aftermarket support, and system integration capabilities. Vendors are differentiating through modular line design, processor-specific engineering, and lifecycle services that help customers sustain utilization. The market therefore reflects not only machinery demand, but also the strategic importance of adaptable platforms aligned with evolving processing requirements.

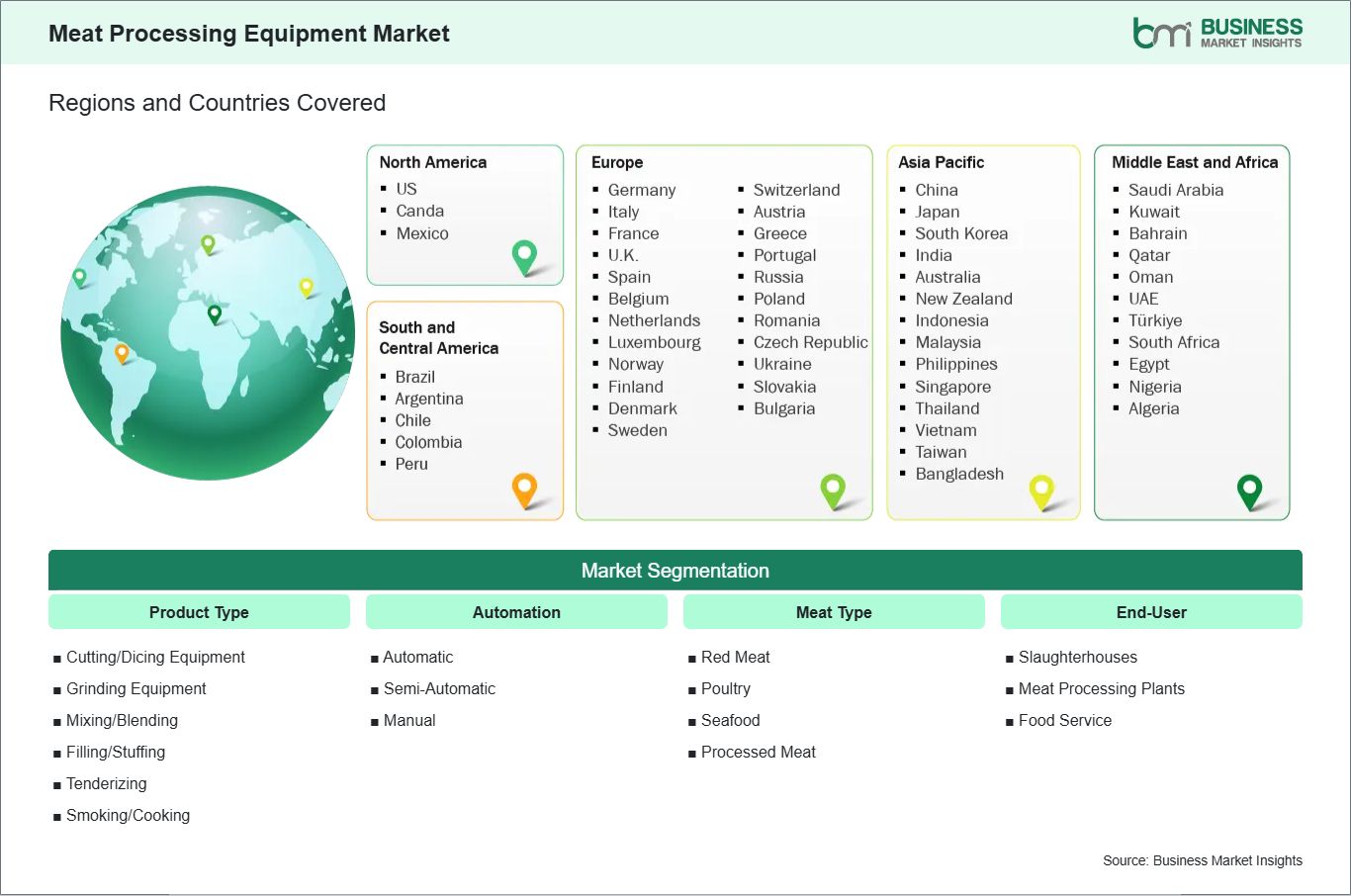

The Meat Processing Equipment market is segmented by product type, automation, meat type, and end-user, reflecting plant configuration needs and processing complexity across operating environments.

By Product Type

Cutting/Dicing Equipment: Shapes portion size and improves downstream uniformity.

Grinding Equipment: Supports texture control for minced and formed products.

Mixing/Blending: Enables even ingredient distribution across batch formulations.

Filling/Stuffing: Advances portion accuracy for sausages and prepared items.

Tenderizing: Enhances bite consistency in structured muscle products.

Smoking/Cooking: Delivers thermal treatment and flavor development in one stage.

By Automation

Automatic: Prioritizes throughput stability and repeatable line performance.

Semi-Automatic: Balances operator control with process efficiency.

Manual: Fits smaller facilities with flexible batch handling needs.

By Meat Type

Red Meat: Requires robust systems for dense muscle processing tasks.

Poultry: Favors hygienic, high-speed equipment for volume-oriented lines.

Seafood: Demands gentle handling and corrosion-conscious equipment design.

Processed Meat: Relies on integrated steps for mixing, filling, and cooking.

By End-User

Slaughterhouses: Use heavy-duty equipment for initial preparation and conversion.

Meat Processing Plants: Operate integrated lines for scaled product transformation.

Food Service: Prefers compact systems for controlled batch preparation.

Meat Processing Equipment Market Drivers and Opportunities:

Automation Upgrades Across Protein Processing Facilities

Processors are reconfiguring production lines to handle tighter hygiene demands, higher throughput expectations, and more standardized product specifications. That shift creates a clear need for equipment that reduces manual contact, improves cut precision, and stabilizes batch execution. As facilities pursue greater operational discipline, investment is moving toward automated cutting, grinding, mixing, and thermal systems that align daily output with quality targets.

The effect is visible in plant modernization programs focused on sanitation efficiency, yield management, and consistent finished-product attributes. In this context, advanced machinery becomes relevant not only for speed, but also for repeatable process control across demanding production schedules. The market benefits as processors prioritize equipment platforms that support reliable execution in multi-shift environments and increasingly complex product mixes.

Smart Processing Systems for Flexible Product Portfolios

A notable opportunity is emerging from the shift toward flexible production architectures that can accommodate diverse protein formats and recipe changes. Equipment suppliers are introducing smarter controls, modular assemblies, and programmable functions that simplify transitions between product runs. These innovations are particularly useful in filling, blending, and cooking operations where formulation integrity and process timing directly influence product consistency.

Future scope extends across processors seeking adaptable lines that can support premium, convenience-oriented, and prepared meat categories without prolonged changeovers. This creates room for broader deployment of digitally assisted equipment in both established plants and expanding processing networks. As operational flexibility becomes a stronger purchasing criterion, suppliers with scalable and application-specific solutions can strengthen their position across this sector.

Meat Processing Equipment Market Size and Share Analysis:

The Meat Processing Equipment market size is expected to reach US$ 29.43 Billion by 2033 from US$ 16.95 Billion in 2025. The market is estimated to record a CAGR of 7.14% from 2026 to 2033. This trajectory reflects steady capital allocation toward line modernization, sanitation-focused design, and higher process consistency across protein handling operations.

By product type, cutting/dicing equipment and grinding equipment hold a central position because they anchor upstream material preparation and influence downstream efficiency. Automatic systems command stronger interest among larger processors due to their repeatable performance, while semi-automatic and manual formats remain relevant where production scale and workflow flexibility shape equipment choices.

By application context, meat processing plants represent the dominant end-user environment as they require integrated equipment across multiple transformation stages. Demand is also sustained in slaughterhouses for primary conversion tasks, while food service settings support more compact equipment needs tied to controlled-volume preparation and menu standardization.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

GEA Group

Marel hf

Tetra Pak International S.A.

Illinois Tool Works Inc.

The Middleby Corporation

JBT Corporation

Bühler Group

BAADER Group

Multivac Group

Key Technology

Get more information on this report

Meat Processing Equipment Market Report Coverage and Deliverables:

The "Meat Processing Equipment Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering the areas below:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

The Meat Processing Equipment market shows diverse regional adoption patterns influenced by protein consumption structures, plant modernization priorities, regulatory expectations, and processing intensity across supply chains. Global demand reflects the need for equipment that can improve hygiene execution, yield consistency, and throughput across both established processors and expanding production networks.

North America maintains a mature procurement environment supported by large-scale processing infrastructure, replacement demand, and a strong focus on labor efficiency. Equipment selection in the region increasingly emphasizes automation depth, sanitation-oriented engineering, and dependable aftermarket support. Processors are attentive to line resilience, especially where product uniformity and uptime influence operating economics.

Asia Pacific presents a different growth profile, shaped by expanding processing capacity, shifting food distribution models, and the formalization of protein value chains. Manufacturers and processors across the region are increasing equipment deployment to improve handling efficiency and support broader product portfolios. Demand is particularly aligned with scalable systems that can serve both volume expansion and operational standardization.

Europe continues to emphasize precision engineering, process reliability, and compliance-led equipment design, which sustains demand for advanced integrated systems. Emerging markets in the Middle East, Africa, and South and Central America are progressing through selective investments tied to cold-chain development, domestic processing expansion, and food service supply needs. Together, these regions broaden the market’s long-term equipment replacement and installation base.

Get more information on this report

Meat Processing Equipment Market Research Report Guidance:

The report encompasses both qualitative and quantitative data pertaining to the market, categorized by product type, automation, meat type, and end-user, and geographical regions.

Beginning with Chapter 2, the report presents key takeaways that underscore the primary trends and market outlook.

Chapter 3 is dedicated to outlining the research methodology employed in this study.

In Chapter 4, an ecosystem analysis is provided.

Chapter 5 delves into the significant industry dynamics affecting the market, including driving factors, existing challenges, potential opportunities, and emerging trends. This section also includes an impact analysis of these drivers and constraints.

Chapter 6 reviews the market scenario, detailing historical revenue figures and forecasts extending to the year 2033.

Chapters 7 through 10 analyze market segments based on product type, automation, meat type, and end-user, and geography, covering regions such as North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. These chapters include market revenue data, forecasts, and driving factors.

Chapter 11 presents a competitive analysis, featuring a heat map of key players within the market.

Chapter 12 offers an industry landscape analysis, detailing business activities such as market initiatives, recent developments, mergers, and joint ventures on a global scale, alongside a competitive overview.

In Chapter 13, comprehensive profiles of major companies operating in the market are provided. These profiles include key facts, business descriptions, product and service offerings, financial overviews, SWOT analyses, and significant developments.

Finally, Chapter 14, the appendix, includes a brief company overview, a list of abbreviations, and a disclaimer.

Meat Processing Equipment Market News and Key Development:

The Meat Processing Equipment Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

In January 2026, Henco Machinery manufacturer announced the launch of its newly developed Meat Equal-Weight Cutting Line. This cutting-edge solution is set to redefine efficiency, precision, and safety standards in the meat processing sector, addressing the industry's pressing needs for cost optimization, waste reduction, and consistent product quality.

In April 2024, JBT Corporation (NYSE: JBT), a leading global technology solutions provider to high-value segments of the food & beverage industry, announced that JBT and Marel hf. (ICL: Marel) have executed a definitive transaction agreement related to JBT’s previously announced intention to make a voluntary takeover offer for all of the issued and outstanding shares of Marel. The transaction agreement includes the terms of the offer and other important governance, social, and operating items relating to the proposed business combination of JBT and Marel. The transaction agreement was approved by the Boards of Directors of both companies.

Key Sources Referred:

World Bank: Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Meat Processing Equipment Market

GEA Group

Marel hf

Tetra Pak International S.A.

Illinois Tool Works Inc.

The Middleby Corporation

JBT Corporation

Bühler Group

BAADER Group

Multivac Group

Key Technology

Frequently Asked Questions

How big is the Meat Processing Equipment Market?

The Meat Processing Equipment Market is valued at US$ 16.95 Billion in 2025, it is projected to reach US$ 29.43 Billion by 2033.

What is the CAGR for Meat Processing Equipment Market by (2026 - 2033)?

As per our report Meat Processing Equipment Market, the market size is valued at US$ 16.95 Billion in 2025, projecting it to reach US$ 29.43 Billion by 2033. This translates to a CAGR of approximately 7.14% during the forecast period.

What segments are covered in this report?

The Meat Processing Equipment Market report typically cover these key segments-

Product Type (Cutting/Dicing Equipment, Grinding Equipment, Mixing/Blending, Filling/Stuffing, Tenderizing, Smoking/Cooking)

Automation (Automatic, Semi-Automatic, Manual)

Meat Type (Red Meat, Poultry, Seafood, Processed Meat)

What is the historic period, base year, and forecast period taken for Meat Processing Equipment Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Meat Processing Equipment Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Meat Processing Equipment Market?

The Meat Processing Equipment Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

GEA Group

Marel hf

Tetra Pak International S.A.

Illinois Tool Works Inc.

The Middleby Corporation

JBT Corporation

Bühler Group

BAADER Group

Multivac Group

Key Technology

Who should buy this report?

The Meat Processing Equipment Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Meat Processing Equipment Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Meat Processing Equipment Market

Get Free Sample For Meat Processing Equipment Market