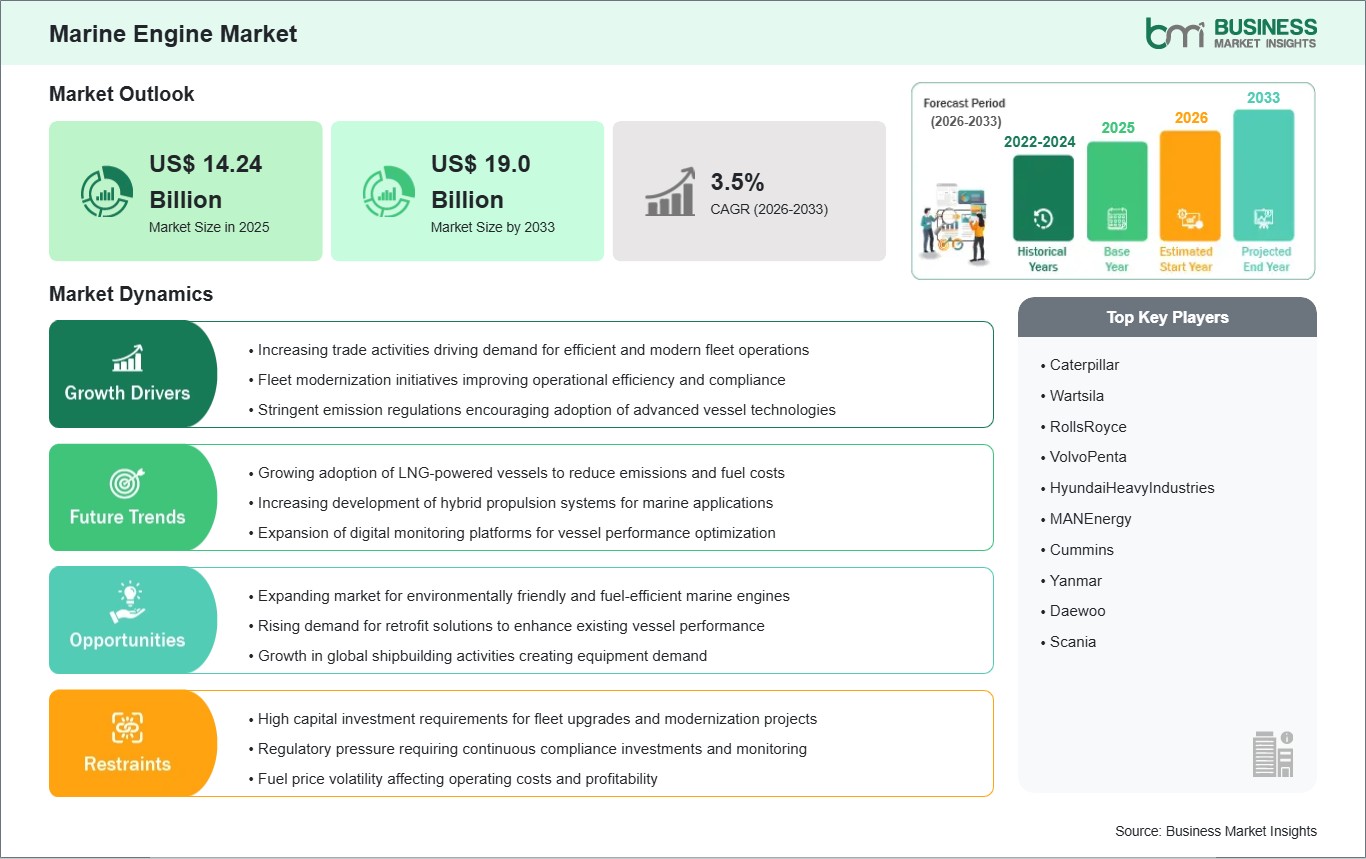

The Marine Engine market size is expected to reach US$ 19.0 billion by 2033 from US$ 14.24 billion in 2025. The market is estimated to record a CAGR of 3.5% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Marine propulsion and auxiliary power systems encompass mechanical technologies that convert fuel energy into thrust and onboard electricity for maritime vessels. These systems integrate combustion mechanisms, fuel conditioning units, and emission control technologies to support navigation across commercial and defense fleets. Their configuration varies depending on vessel size, operational range, and fuel type requirements, reflecting advancements in energy efficiency and environmental compliance.

Expansion in seaborne trade and sustained vessel replacement cycles have intensified the need for reliable and fuel-efficient engine systems. Regulatory frameworks targeting emission intensity have further compelled fleet operators to adopt cleaner propulsion solutions. This shift aligns with rising utilization of alternative fuels and energy-efficient engineering configurations, reinforcing steady procurement patterns across shipping industries.

Segment-wise differentiation highlights propulsion engines as the principal revenue contributors due to their direct role in vessel movement. Auxiliary engines maintain operational demand in power generation for onboard systems. Among engine types, two-stroke systems dominate long-haul shipping, while four-stroke engines remain favorable in medium-range applications. Diesel continues to lead fuel usage, although liquefied natural gas and hybrid configurations are gaining operational acceptance.

Technological development centers on emission reduction systems, digital monitoring integration, and fuel flexibility solutions. Innovations in combustion efficiency and hybrid power integration are reshaping product design strategies. Enhanced automation capabilities enable predictive maintenance, minimizing operational downtime while improving fuel optimization outcomes.

Marine Engine Market - Strategic Insights:

Get more information on this report

Marine Engine Market Segmentation Analysis:

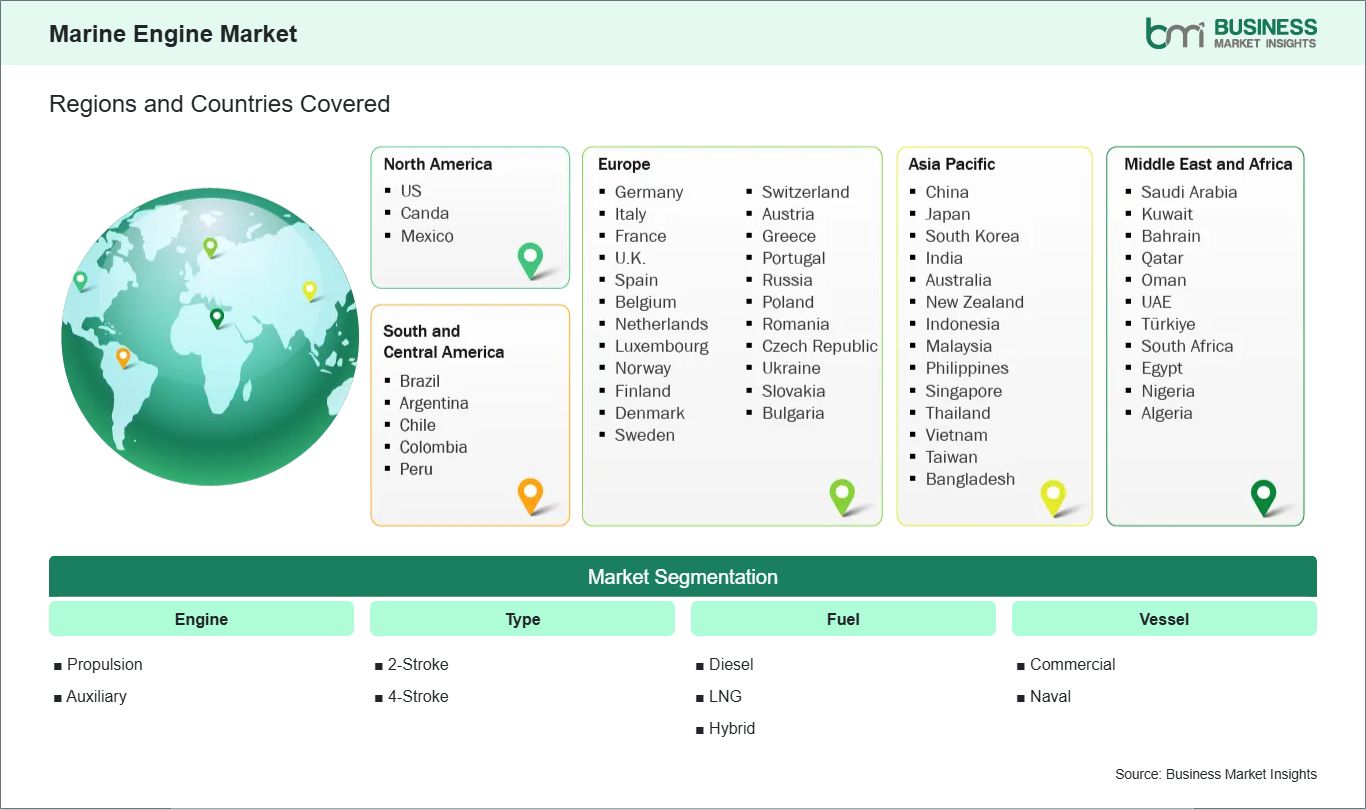

The market is segmented based on engine, type, fuel, and vessel categories.

By Engine

Propulsion - Core power source enabling vessel movement across long-distance maritime operations

Auxiliary - Supplies onboard electricity and supports operational functionality of vessel systems.

By Type

2-Stroke - Preferred for high-efficiency, long-haul maritime transportation applications

4-Stroke - Utilized in medium-speed vessels requiring operational flexibility.

By Fuel

Diesel - Established fuel choice due to infrastructure compatibility and operational consistency

LNG - Selected for reduced emissions and regulatory compliance advantages

Hybrid - Combines fuel efficiency with electric assistance for optimized energy usage

By Vessel

Commercial - Dominates demand through cargo transport, shipping logistics, and bulk operations

Naval - Focuses on reliability, durability, and mission-specific propulsion requirements

Global enforcement of emission control policies has reshaped procurement strategies within maritime fleets. Regulatory bodies continue to impose stricter compliance requirements, compelling operators to reassess engine configurations. This has accelerated the transition toward low-emission fuel technologies, particularly LNG-based propulsion systems, alongside retrofitting existing vessels with advanced emission control units to meet regulatory standards.

Adoption trends highlight measurable operational shifts as fleet owners prioritize regulatory alignment alongside fuel cost optimization. This transition has enhanced relevance of advanced engine systems capable of dual-fuel operation. Additionally, compliance-driven investments are fostering technology upgrades, strengthening overall market expansion while maintaining adherence to sustainability frameworks.

Hybrid propulsion systems unlocking operational efficiency gains

Emerging hybrid propulsion technologies are redefining energy consumption patterns in maritime operations. Integration of electric propulsion components with conventional engines allows flexible energy usage during varying operational phases. This approach reduces fuel consumption while maintaining engine performance stability, particularly in port operations and short-distance navigation.

Future deployment of hybrid systems is expected to expand across diverse vessel categories, driven by advancements in energy storage and control systems. Increasing investments in hybrid-compatible vessels will support broader integration, enabling cost-effective energy management solutions while simultaneously aligning with environmental objectives and efficiency enhancement priorities.

Marine Engine Market Size and Share Analysis:

The Marine Engine Market was valued at US$ 14.24 Billion in 2025 to reach US$ 19.0 Billion by 2033, at a CAGR of 3.5% from 2026 to 2033. This trajectory reflects consistent expansion supported by stable maritime trade volumes and gradual technological upgrades. Market growth remains moderate due to high capital intensity and cyclical demand patterns within shipbuilding and fleet modernization activities.

Segment-level analysis shows propulsion engines maintaining a leading position due to their critical role in vessel performance. Auxiliary engines demonstrate steady adoption across multiple vessel categories, supported by essential onboard power requirements and operational reliability standards.

From an application perspective, commercial vessels account for dominant demand patterns driven by global trade logistics. Naval applications maintain specialized growth, emphasizing durability, mission readiness, and engineering precision. The balance between these segments reinforces sustained demand across both civilian and defense maritime operations.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Caterpillar

Wartsila

RollsRoyce

VolvoPenta

HyundaiHeavyIndustries

MANEnergy

Cummins

Yanmar

Daewoo

Scania

Get more information on this report

Marine Engine Market Report Coverage and Deliverables:

The "Marine Engine Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all market segments covered under the scope

Market trends, as well as drivers, restraints, and opportunities

Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Marine Engine Market Geographic Insights:

The Marine Engine market shows diverse regional adoption patterns influenced by trade intensity, regulatory enforcement, and shipbuilding activity distribution. Mature shipping corridors prioritize compliance-driven upgrades, while emerging maritime economies focus on capacity expansion and fleet development. The interplay between environmental standards and operational efficiency drives regional investment strategies across engine technologies.

North America reflects steady demand supported by naval modernization programs and inland waterway transportation. Regulatory emphasis on emission reduction policies has encouraged adoption of cleaner propulsion alternatives. Industrial capabilities and maintenance infrastructure further support sustained utilization of upgraded engine systems within the region.

Asia Pacific demonstrates strong expansion momentum due to its dominance in shipbuilding and global trade flows. Countries with extensive maritime infrastructure continue investing in fleet expansion and replacement cycles. Adoption of LNG-based engines and hybrid technologies is strengthening as regional authorities emphasize emission control and fuel efficiency improvements.

Europe maintains a technology-focused market driven by stringent environmental regulations and innovation in fuel alternatives. Manufacturers in this region continue advancing hybrid propulsion and digital monitoring capabilities. Meanwhile, regions such as the Middle East, Africa, and South America are gradually expanding maritime operations, creating opportunities for engine deployment aligned with infrastructure growth and trade development.

Get more information on this report

Marine Engine Market Research Report Guidance:

The report includes qualitative and quantitative data in the market across engine, type, fuel, vessel, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover market segments by engine, type, fuel, vessel, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Marine Engine Market News and Key Development:

The Marine Engine market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. Recent developments and news in the market include:

In September 2025, Swiss marine power company WinGD offered the first ethanol-fuelled two-stroke marine engine next year, with deliveries for newbuild and retrofit applications starting in 2027. The announcement follows a decade of investigation into ethanol fuel—including full-scale engine tests in 2018—and the successful launch of a methanol-fuelled engine that uses the same combustion concept and is subject to the same safety regulations as the new ethanol engine.

In October 2025, Rolls-Royce successfully tested the world’s first high-speed marine engine powered exclusively by methanol on its test bench in Friedrichshafen. Together with their partners in the meOHmare research project, Rolls-Royce engineers have thus reached an important milestone on the road to climate-neutral and environmentally friendly propulsion solutions for shipping.

Key Sources Referred:

Industry technical publications on marine propulsion systemsGovernment maritime regulatory frameworks and emission standardsShipping and shipbuilding industry reportsEngineering and combustion system journalsCompany WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Marine Engine Market

Caterpillar

Wartsila

RollsRoyce

VolvoPenta

HyundaiHeavyIndustries

MANEnergy

Cummins

Yanmar

Daewoo

Scania

Frequently Asked Questions

How big is the Marine Engine Market?

The Marine Engine Market is valued at US$ 14.24 Billion in 2025, it is projected to reach US$ 19.0 Billion by 2033.

What is the CAGR for Marine Engine Market by (2026 - 2033)?

As per our report Marine Engine Market, the market size is valued at US$ 14.24 Billion in 2025, projecting it to reach US$ 19.0 Billion by 2033. This translates to a CAGR of approximately 3.5% during the forecast period.

What segments are covered in this report?

The Marine Engine Market report typically cover these key segments-

Engine (Propulsion, Auxiliary)

Type (2-Stroke, 4-Stroke)

Fuel (Diesel, LNG, Hybrid)

Vessel (Commercial, Naval)

What is the historic period, base year, and forecast period taken for Marine Engine Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Marine Engine Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Marine Engine Market?

The Marine Engine Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Caterpillar

Wartsila

RollsRoyce

VolvoPenta

HyundaiHeavyIndustries

MANEnergy

Cummins

Yanmar

Daewoo

Scania

Who should buy this report?

The Marine Engine Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Marine Engine Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Marine Engine Market

Get Free Sample For Marine Engine Market