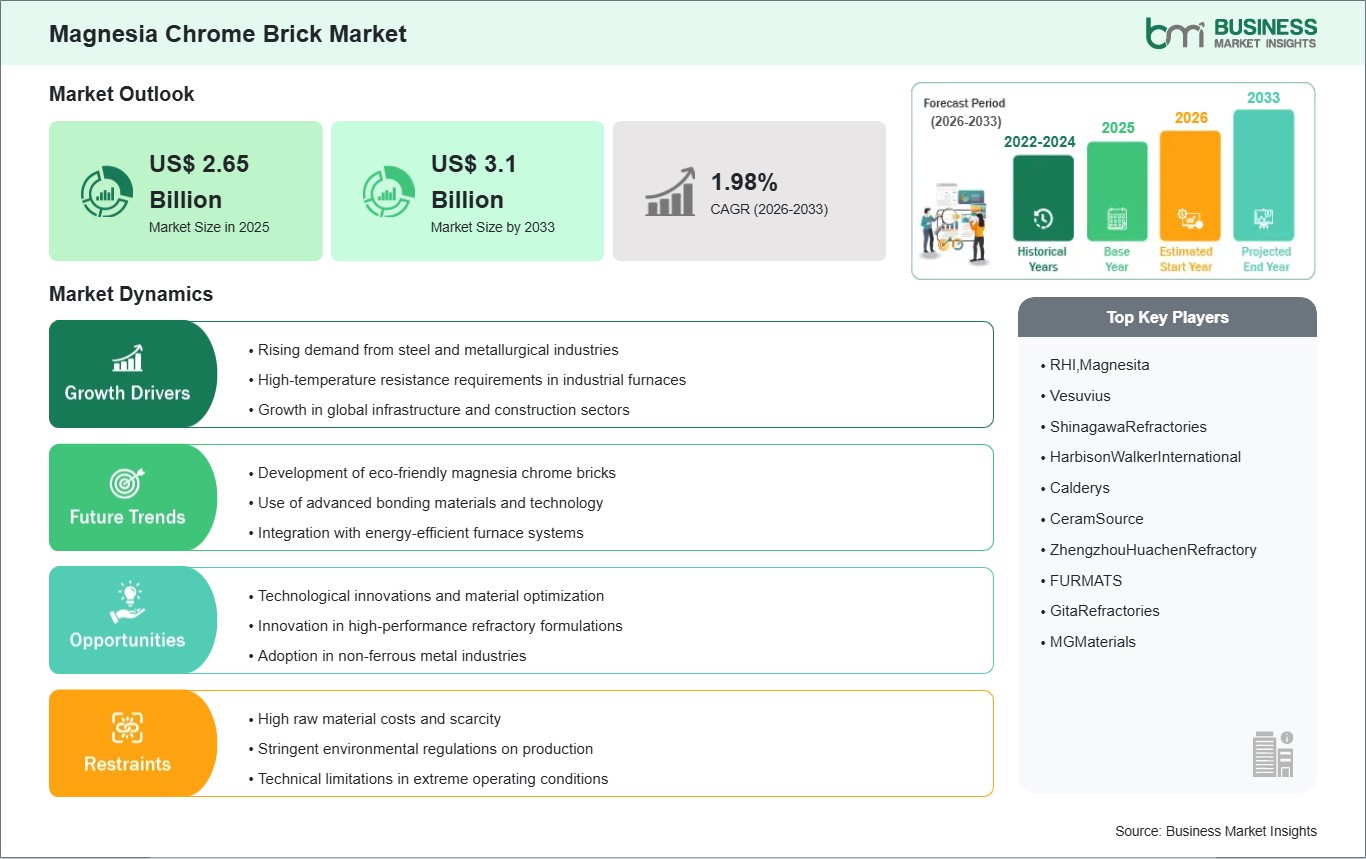

The Magnesia Chrome Brick Market size is expected to reach US$ 3.1 Billion by 2033 from US$ 2.65 Billion in 2025. The market is estimated to record a CAGR of 1.98% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global magnesia chrome brick market continues to grow as demand for refractory materials used in high-temperature industrial processes increases, mainly in steel, cement, and non-ferrous production. Magnesia chrome bricks are excellent in terms of thermal stability, corrosion resistant, and the mechanical strength of magnesia chrome bricks has made them widely used as refractory linings in furnaces, kilns, and other types of equipment required to withstand high-temperature operations. Increasing steel production and modernization of industrial furnaces for the purpose of improving energy efficiency and operational life expectancy are driving the growth of this market. Some of the latest developments in the technology regarding magnesia chrome bricks include increasing chemical purity, improving firing techniques, and creating bricks that are more resistant to slag and thermal shock. Refractory manufacturers are also focusing on lightweight, energy-efficient refractories, resulting in innovative formulations and manufacturing techniques.

Manufacturers can create a competitive advantage through strategic initiatives such as establishing local production facilities in proximity to industrial centers, developing partnerships with steel and cement manufacturers, and providing customized refractory solutions to customers. In addition, manufacturers are beginning to take notice of sustainability-related issues associated with the magnesia chrome brick market and are developing new strategies to reduce energy consumption during manufacturing and exploring the use of recycled raw materials. Companies that implement product innovation and technical support systems while developing strategic supply chain management capabilities will be best positioned to capitalize on the growing magnesia chrome brick market.

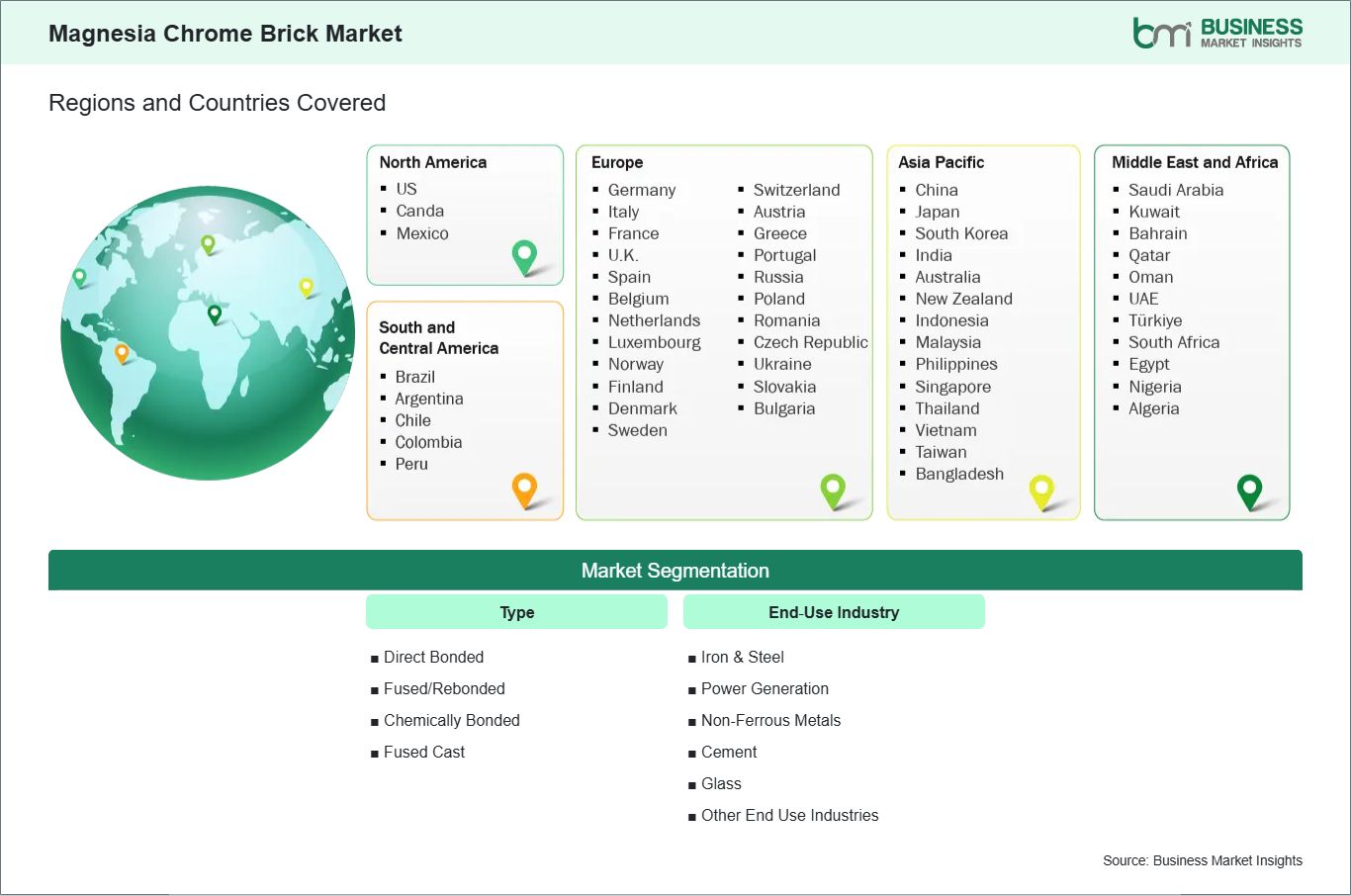

Key segments that contributed to the derivation of the magnesia chrome brick market analysis are type and end‑use industry.

Type, the magnesia chrome brick market is segmented into direct bonded, fused/rebonded, chemically bonded, and fused cast. The direct bonded segment dominated the market in 2025.

End‑Use Industry, the magnesia chrome brick market is classified into iron & steel, power generation, non‑ferrous metals, cement, glass, and others. The iron & steel segment dominated the market in 2025.

Magnesia Chrome Brick Market Drivers and Opportunities:

Rising demand from steel and metallurgical industries

Rising steel and metallurgical requirements are driving the global magnesia chrome brick market. These industries require high-temperature refractory materials that can withstand chemical corrosion, thermal shock, and mechanical wear during operations in kilns and furnaces. Due to excellent resistance to basic slags, high refractoriness, and structural stability in extremely harsh conditions, magnesia chrome bricks are the preferred choice for steelmaking and metallurgical applications. Magnesia chrome bricks are critical industrial products that support operational efficiency in applications such as electric arc furnaces, ladle linings, and rotary kilns, while also increasing the longevity of furnaces or kilns.

Manufacturers are focused on the quality, uniformity, and dimensional accuracy of magnesia chrome bricks in order to meet the demanding requirements of modern high-temperature operations. Therefore, advanced refractory solutions that can withstand an extended period of exposure to thermal heating and chemical attack have seen consistent demand in recent years. Furthermore, because the steel industry continues to expand and modernize, magnesia chrome bricks are being adopted globally in increasing volumes. End-users are looking for materials that will minimize maintenance, maximize furnace life, and promote process stability. As a result, the magnesia chrome brick market is positioned for steady growth through the prediction of steel and metallurgical applications globally.

Technological innovations and material optimization

The emergence of new magnesia chrome brick technologies presents an exciting opportunity for growth in the market. There are now more manufacturers creating bricks with optimized compositions, advanced sintering methods, and superior microstructural controls that will result in improved performance under extreme thermal and mechanical stress. Innovations in these bricks will provide superior resistance to slag penetration, thermal spalling, and dimensional change, thereby improving furnace efficiency and reliability. In addition, research is focused on modifying brick properties to suit each specific furnace environment, such as improving slag resistance, increasing thermal conductivity, and increasing strength. By being able to customize bricks, end-users will maximize operational efficiency and decrease energy use while minimizing downtime due to maintenance.

Lastly, collaboration between refractory manufacturers and their industrial customers will drive the development of environmentally-friendly, high-performance brick solutions. By utilizing advanced manufacturing techniques, including using synthetic raw materials and precise chemical control, the quality and consistency of final products is being greatly enhanced. These technological advancements, combined with the increase in steel production and modernization in metallurgy, will ensure that the magnesia chrome brick industry continues to grow globally over the long term.

Magnesia Chrome Brick Market Size and Share Analysis:

The magnesia chrome brick market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within type and end‑use industry, offering insights into their contribution to overall market performance.

By Type, the direct bonded subsegment dominated the market in 2025, driven by its widespread use in high‑temperature furnace linings and cost‑effective installation in steel and cement applications.

Based on End‑Use Industry, the iron & steel subsegment dominated the market in 2025, supported by increasing demand for high‑performance refractory solutions in blast furnaces, ladles, and converter linings.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

RHIÂ Magnesita

Vesuvius

ShinagawaRefractories

HarbisonWalkerInternational

Calderys

CeramSource

ZhengzhouHuachenRefractory

FURMATS

GitaRefractories

MGMaterials

Get more information on this report

Magnesia Chrome Brick Market Report Coverage and Deliverables:

The "Magnesia Chrome Brick Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Magnesia Chrome Brick Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Magnesia Chrome Brick Market trends, as well as drivers, restraints, and opportunities

Magnesia Chrome Brick Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Magnesia Chrome Brick Market

Detailed company profiles, including SWOT analysis

Magnesia Chrome Brick Market Geographic Insights:

The geographical scope of the Magnesia Chrome Brick Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

Regional adoption of magnesia chrome bricks is closely linked to industrial production capacity, infrastructure development, and metallurgical activity. North America is a leading market, supported by a mature steel industry, advanced cement production, and ongoing furnace modernization programs in the U.S. and Canada. Europe demonstrates strong demand in Germany, Italy, and France, driven by sustainable steel and cement production, high-quality refractory requirements, and strict environmental and operational standards.

Asia Pacific is the fastest-growing region, led by China, India, Japan, and South Korea, where rising steel production, infrastructure expansion, and industrialization drive substantial consumption of high-performance refractory bricks. Middle East & Africa is an emerging market, with growth tied to cement manufacturing, metal processing, and construction projects in countries like Saudi Arabia, UAE, and South Africa.

South & Central America, led by Brazil and Mexico, is gradually increasing demand due to growing metallurgical and cement industries and modernization of existing furnaces. Across all regions, key drivers include material quality, thermal efficiency, chemical resistance, and supplier technical support, which determine competitive positioning in the magnesia chrome brick market.

Get more information on this report

Magnesia Chrome Brick Market Research Report Guidance:

The report includes qualitative and quantitative data in the Magnesia Chrome Brick Market across type, end‑use industry and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Magnesia Chrome Brick Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Magnesia Chrome Brick Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Magnesia Chrome Brick Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 9 cover Magnesia Chrome Brick Market segments across type, end‑use industry, and geography across North America, Asia Pacific, Europe, the Middle East & Africa, and South & Central America. They cover the market revenue forecast and factors driving the market.

Chapter 10 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 11 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 12 provides detailed profiles of the major companies operating in the Magnesia Chrome Brick Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 13, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Magnesia Chrome Brick Market News and Key Development:

The Magnesia Chrome Brick Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the magnesia chrome brick market are:

In January 2023, RHI Magnesita completed the acquisition of a midsize Indian refractory company, expanding its local manufacturing and distribution capacity for magnesia chrome bricks to better serve regional steel and cement industries.

In January 2025, RHI Magnesita completed its acquisition of the Resco Group to strengthen its North American refractory brick footprint, enhancing local production of magnesia chrome bricks and improving supply chain responsiveness in steel and cement end markets.

Key Sources Referred:

International Organization for Standardization (ISO)American Society for Testing and Materials (ASTM International)Bureau of Indian Standards (BIS)Environmental Protection Agency (EPA), USAEuropean Chemicals Agency (ECHA)Central Pollution Control Board (CPCB), IndiaMinistry of Chemicals and Fertilizers, IndiaAmerican Chemistry Council (ACC)Indian Chemical Council (ICC)European Chemical Industry Council (Cefic)Specialty Chemical Association of India (SCAI)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Magnesia Chrome Brick Market

RHI Magnesita

Vesuvius

ShinagawaRefractories

HarbisonWalkerInternational

Calderys

CeramSource

ZhengzhouHuachenRefractory

FURMATS

GitaRefractories

MGMaterials

About Author— Chemicals and Materials Research Team

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Show More

Frequently Asked Questions

How big is the Magnesia Chrome Brick Market?

The Magnesia Chrome Brick Market is valued at US$ 2.65 Billion in 2025, it is projected to reach US$ 3.1 Billion by 2033.

What is the CAGR for Magnesia Chrome Brick Market by (2026 - 2033)?

As per our report Magnesia Chrome Brick Market, the market size is valued at US$ 2.65 Billion in 2025, projecting it to reach US$ 3.1 Billion by 2033. This translates to a CAGR of approximately 1.98% during the forecast period.

What segments are covered in this report?

The Magnesia Chrome Brick Market report typically cover these key segments-

Type (Direct Bonded, Fused/Rebonded, Chemically Bonded, Fused Cast)

End-Use Industry (Iron & Steel, Power Generation, Non-Ferrous Metals, Cement, Glass, Other End Use Industries)

What is the historic period, base year, and forecast period taken for Magnesia Chrome Brick Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Magnesia Chrome Brick Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Magnesia Chrome Brick Market?

The Magnesia Chrome Brick Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

RHIÃÂ Magnesita

Vesuvius

ShinagawaRefractories

HarbisonWalkerInternational

Calderys

CeramSource

ZhengzhouHuachenRefractory

FURMATS

GitaRefractories

MGMaterials

Who should buy this report?

The Magnesia Chrome Brick Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Magnesia Chrome Brick Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Magnesia Chrome Brick Market

Get Free Sample For Magnesia Chrome Brick Market