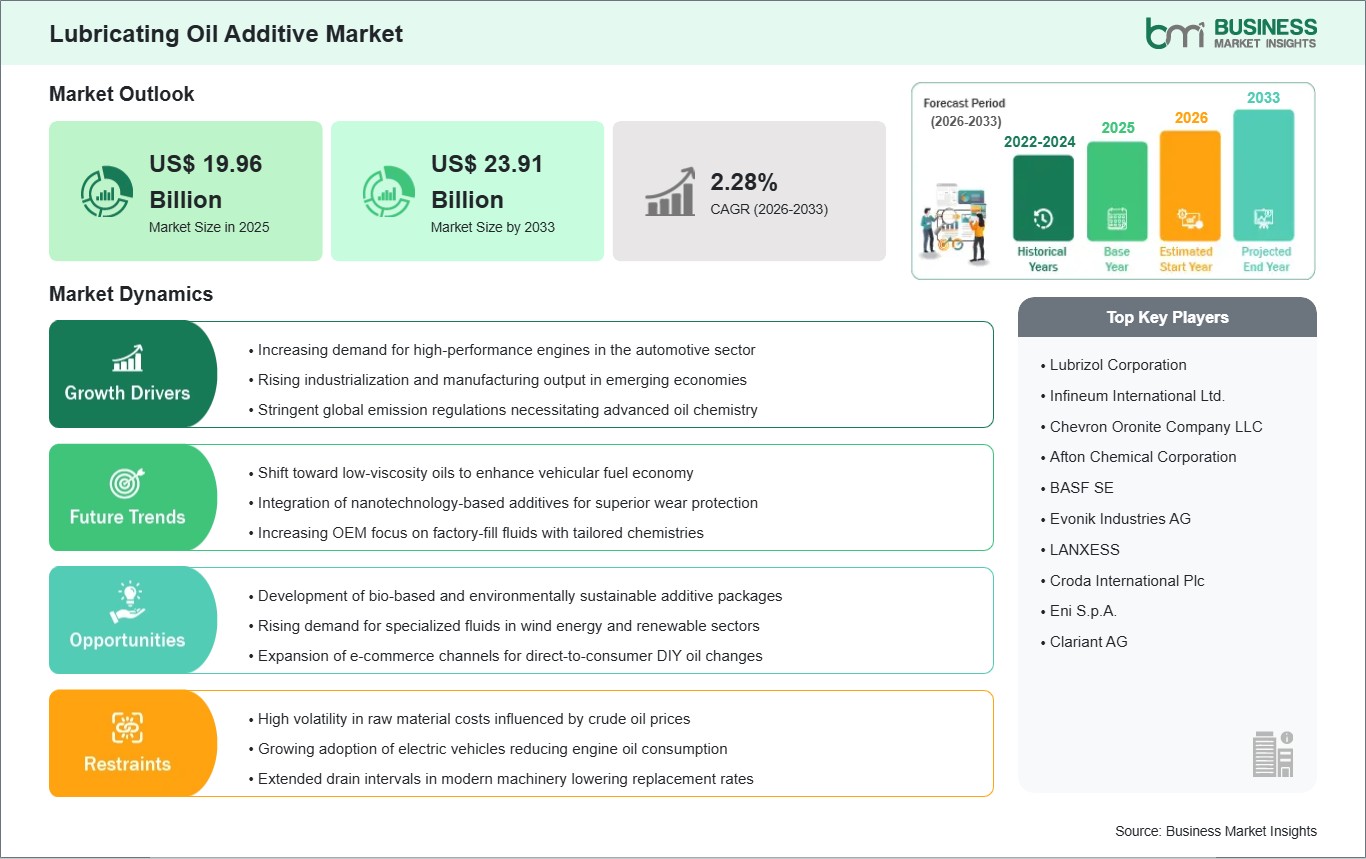

The Lubricating Oil Additive Market size is expected to reach US$ 23.91 Billion by 2033 from US$ 19.96 Billion in 2025. The market is estimated to record a CAGR of 2.28% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The lubricating oil additives market is one of the most important pillars of the global energy and industrial sectors. The lubricating oil additives industry supplies the necessary chemistry to the industrial and automotive sectors. The lubricating oil additives industry has witnessed the evolution of industrial and automotive technologies. The lubricating oil additives industry is no longer just seen as providing performance-enhancing agents but rather the necessary ingredients that enable the functioning of modern technology. The lubricating oil additives industry is at the crossroads of transitioning from volume-based commodity business to value-added and specialized products. The automotive industry is the largest consumer of lubricating oil additives, but the industrial segment is growing at a rapid rate in specialized applications.

The competitive scenario of the industry is currently led by a few global companies that have significant R&D capabilities, but regional companies are also emerging as leaders in the emerging markets of the world. The challenges that the industry faces are the shift to electric mobility and the fluctuating raw material prices, but the need for higher performance standards, as defined by the latest API and ILSAC categories, will always create a niche for premium additive chemistries. The future of the industry will depend on how well it adapts to the shift in the global energy scenario and develops products for hybrid cars and sustainable, bio-based products for industrial applications.

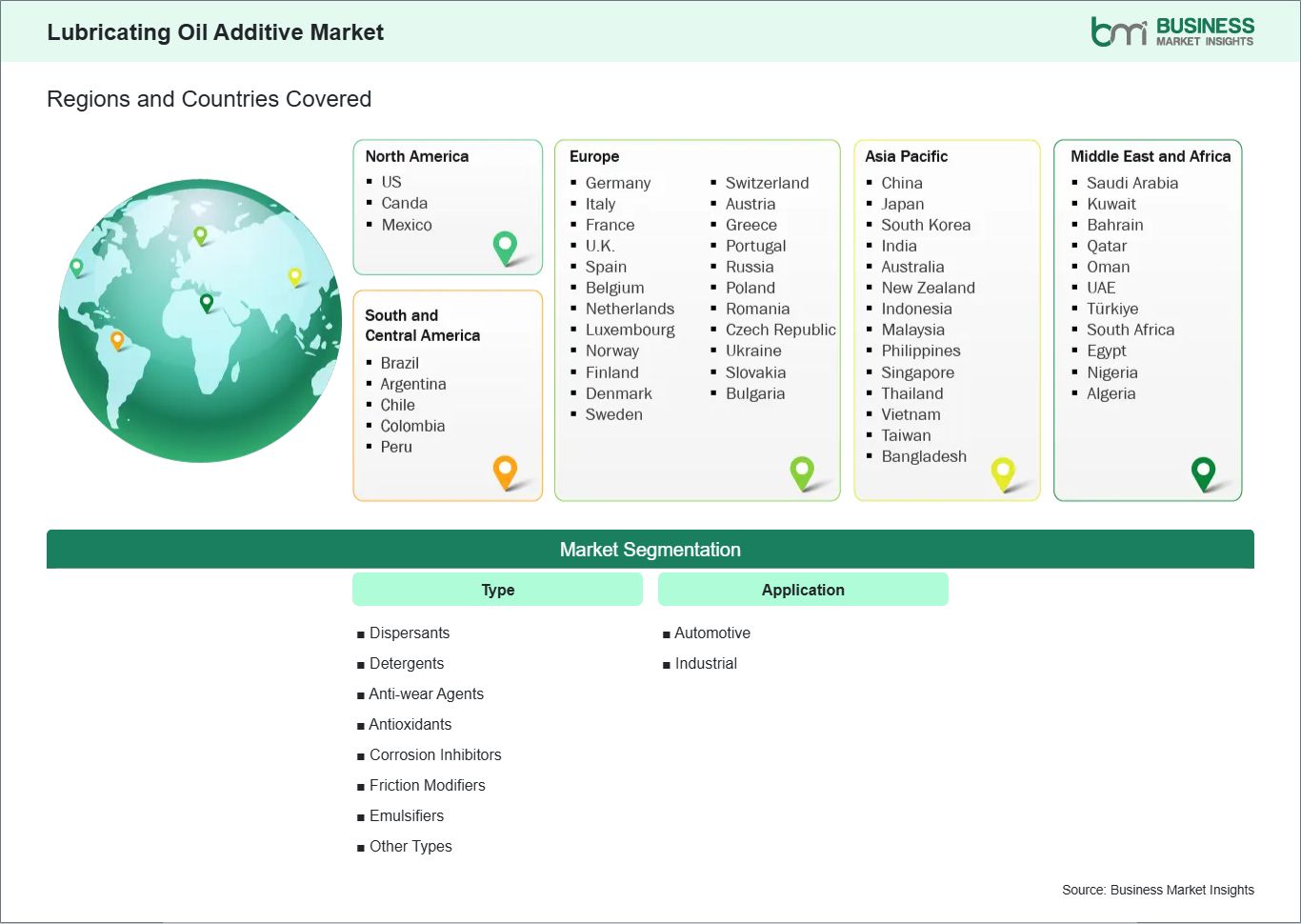

Key segments that contributed to the derivation of the Lubricating Oil Additive market analysis are type and application.

By type, the lubricating oil additive market is segmented into Dispersants, Detergents, Anti-wear Agents, Antioxidants, Corrosion Inhibitors, Friction Modifiers, Emulsifiers, and Other Types. The Dispersants segment dominated the market in 2025.

By application, the lubricating oil additive market is segmented into Automotive and Industrial. The Automotive segment dominated the market in 2025.

Lubricating Oil Additive Market Drivers and Opportunities:

Increasing demand for high-performance engines in the automotive sector

Internal combustion engines have evolved to incorporate downsizing and turbocharging, and this has led to a significant increase in the thermal and mechanical demands on lubricants. Today's high-performance engines are designed to operate in a higher temperature and pressure regime to increase the power density and fuel efficiency of the engines. Such a high-temperature environment catalyzes oil oxidation and the formation of noxious deposits. In the absence of these additives, the oil would decompose very fast, and this would result in engine failure. Therefore, today's automotive industry requires lubricants that contain complex additive combinations to guarantee long-lasting durability and performance.

Furthermore, the rise in consumer expectations for vehicle longevity and reduced maintenance costs has pushed the market toward premium synthetic and semi-synthetic oils. These formulations rely heavily on high-performance additives to maintain viscosity stability and protect critical engine components over extended periods. In developing regions, the growth of the middle class and increased vehicle ownership are providing a steady volume driver for these additives. As the automotive industry continues to innovate to meet both consumers demands and regulatory pressures, the requirement for sophisticated lubricating oil additives that can perform under extreme conditions remains a primary growth engine for the global market.

Development of bio-based and environmentally sustainable additive packages

The global push for sustainability and the reduction of petrochemical dependence is creating a significant transition within the lubricant industry. Environmental agencies are tightening regulations regarding the toxicity and biodegradability of lubricants, especially for applications in sensitive maritime, agricultural, and forestry environments. This has opened a major opportunity for the development of bio-based additives derived from renewable resources such as vegetable oils and animal fats. These green additives must match or exceed the performance of their synthetic counterparts in terms of oxidative stability and friction reduction to gain widespread commercial acceptance in mainstream automotive and industrial sectors.

Investment in sustainable chemistry is not only a regulatory necessity but also a strategic move for companies aiming to improve their Environmental, Social, and Governance (ESG) ratings. High-performance bio-lubricants often require unique additive formulations that are compatible with ester-based base oils. As the technology matures, these sustainable options are becoming more cost-competitive, attracting interest from large-scale fleet operators and industrial manufacturers. The ability to market clean lubrication solutions provides a distinct competitive advantage in a market increasingly sensitive to carbon footprints. This shift toward circular economy principles is expected to redefine the material mix of the additive industry over the coming decade.

Lubricating Oil Additive Market Size and Share Analysis:

The global Lubricating Oil Additive market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within type and application highlighting their respective contributions to overall market performance.

By type, the Dispersants subsegment dominated the market in 2025 due to their essential role in preventing sludge, varnish, and soot agglomeration in high-heat internal combustion engines, making up nearly 70% to 80% of total additive loading in heavy-duty diesel engine oil formulations.

By application, the Automotive subsegment dominated the market in 2025 because of the massive global vehicle parc and the high frequency of oil changes required for passenger cars and commercial fleets to maintain fuel efficiency and comply with stringent international emission standards.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Lubrizol Corporation

Infineum International Ltd.

Chevron Oronite Company LLC

Afton Chemical Corporation

BASF SE

Evonik Industries AG

LANXESS

Croda International Plc

Eni S.p.A.

Clariant AG

Get more information on this report

Lubricating Oil Additive Market Report Coverage and Deliverables:

The "Lubricating Oil Additive Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Lubricating Oil Additive market size and forecast at the regional and country levels for segments covered under the scope

Lubricating Oil Additive market trends, as well as drivers, restraints, and opportunities

Lubricating Oil Additive market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Lubricating Oil Additive market

Detailed company profiles, including SWOT analysis

The geographical scope of the Lubricating Oil Additive market report is divided into: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America remains the dominant region in the lubricating oil additive market, primarily due to its massive and mature automotive sector and its role as a global leader in high-tech industrial manufacturing. The United States possesses one of the largest vehicles parcs in the world, characterized by a high proportion of heavy-duty trucks and high-performance passenger vehicles that require advanced, high-additive-load engine oils. Furthermore, North American regulatory bodies, such as the EPA and various state-level agencies, have some of the world's strictest fuel economy and emission standards. These regulations force a continuous cycle of innovation in lubricant chemistry, maintaining the region's status as a hub for advanced additive research and development.

The region's dominance is further solidified by the presence of major global additive manufacturers and oil majors who have established integrated supply chains across the continent. This infrastructure allows for the rapid deployment of new technologies, such as low-viscosity oils and long-drain formulations, which are increasingly favored by North American fleet operators to reduce total cost of ownership. Additionally, the rebounding industrial sector, particularly in the oil and gas, construction, and aerospace industries, provides a stable secondary demand for high-performance industrial additives. With a strong focus on premiumization and a growing shift toward synthetic and sustainable formulations, North America continues to set the global benchmark for lubricant additive consumption and technological evolution.

Get more information on this report

Lubricating Oil Additive Market Research Report Guidance:

The report includes qualitative and quantitative data in the Lubricating Oil Additive market across type, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Lubricating Oil Additive market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Lubricating Oil Additive market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Lubricating Oil Additive market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 9 cover the Lubricating Oil Additive market segments by type, application, and geography across North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 10 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 11 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 12 provides detailed profiles of the major companies operating in the Lubricating Oil Additive market. Companies have been profiled on the basis of their key facts, business descriptions, types, financial overview, SWOT analysis, and key developments.

Chapter 13, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Lubricating Oil Additive Market News and Key Development:

The Lubricating Oil Additive market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Lubricating Oil Additive market are:

In December 2025, Lubrizol Corporation, announced its 2025 innovation highlights, including advancements in lubricant additive technologies focused on sustainability, improved fuel efficiency, and extended equipment life.

In December 2024, Lubrizol Corporation, announced the launch of new lubricant additive products along with portfolio expansions to enhance performance across automotive and industrial lubricant applications.

In 2024, Afton Chemical Corporation, announced continued development of advanced additive packages designed to meet evolving engine requirements, including lower emissions and improved durability for modern engines.

Key Sources Referred:

American Chemistry Council (ACC)International Council of Chemical Associations (ICCA)European Chemical Industry Council (Cefic)China National Building Materials Group (CNBM)Indian Minerals & Granite Exporters Association (IMGEA)Japan Mining Industry Association (JMIA)Brazilian Mining Association (IBRAM)Gulf Petrochemicals and Chemicals Association (GPCA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Lubricating Oil Additive Market

Lubrizol Corporation

Infineum International Ltd.

Chevron Oronite Company LLC

Afton Chemical Corporation

BASF SE

Evonik Industries AG

LANXESS

Croda International Plc

Eni S.p.A.

Clariant AG

About Author— Chemicals and Materials Research Team

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Show More

Frequently Asked Questions

How big is the Lubricating Oil Additive Market?

The Lubricating Oil Additive Market is valued at US$ 19.96 Billion in 2025, it is projected to reach US$ 23.91 Billion by 2033.

What is the CAGR for Lubricating Oil Additive Market by (2026 - 2033)?

As per our report Lubricating Oil Additive Market, the market size is valued at US$ 19.96 Billion in 2025, projecting it to reach US$ 23.91 Billion by 2033. This translates to a CAGR of approximately 2.28% during the forecast period.

What segments are covered in this report?

The Lubricating Oil Additive Market report typically cover these key segments-

Type (Dispersants, Detergents, Anti-wear Agents, Antioxidants, Corrosion Inhibitors, Friction Modifiers, Emulsifiers, Other Types)

Application (Automotive, Industrial)

What is the historic period, base year, and forecast period taken for Lubricating Oil Additive Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Lubricating Oil Additive Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Lubricating Oil Additive Market?

The Lubricating Oil Additive Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Lubrizol Corporation

Infineum International Ltd.

Chevron Oronite Company LLC

Afton Chemical Corporation

BASF SE

Evonik Industries AG

LANXESS

Croda International Plc

Eni S.p.A.

Clariant AG

Who should buy this report?

The Lubricating Oil Additive Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Lubricating Oil Additive Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Lubricating Oil Additive Market

Get Free Sample For Lubricating Oil Additive Market