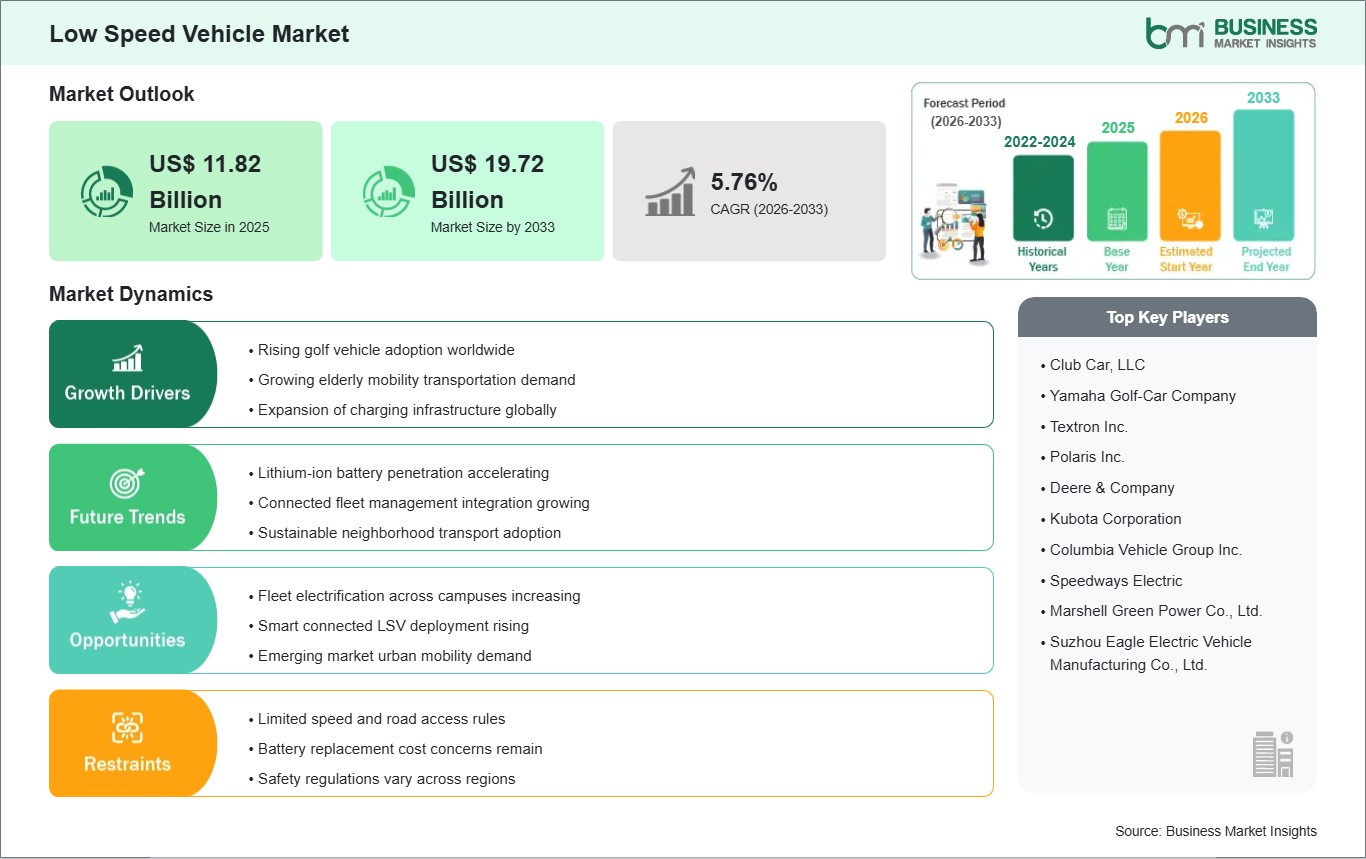

The Low Speed Vehicle market size is expected to reach US$ 19.72 Billion by 2033 from US$ 11.82 Billion in 2025. The market is estimated to record a CAGR of 5.76% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Low speed vehicles are compact transport platforms designed for short-distance movement within controlled or semi-controlled environments. Their operating profile prioritizes maneuverability, simplified handling, and low operating intensity over highway performance. These vehicles support passenger transfer, equipment movement, and site-level mobility across enclosed campuses, hospitality properties, and industrial premises.

Adoption is advancing as site operators seek quieter transport options, lower maintenance requirements, and better suitability for repetitive short-route operations. Electrified models align well with facilities aiming to reduce localized emissions and simplify fleet servicing. At the same time, established ICE platforms remain relevant where refueling convenience and extended operating cycles are priorities.

Segmentation reveals a market shaped by functional diversity. Golf carts maintain strong visibility through course operations and leisure mobility, while commercial turf utility and industrial utility vehicles address maintenance, logistics, and workforce transport. Personal mobility vehicles serve properties that require compact, user-friendly movement across resorts, airports, and mixed-use campuses.

Technology evolution is centered on battery management, charging efficiency, durable lightweight components, and connected fleet oversight. Manufacturers are refining vehicle architecture to improve route consistency, usability, and operational uptime. Design progress also reflects application-specific requirements, such as cargo flexibility, passenger comfort, and reliable performance across landscaped, paved, and indoor service areas.

Competitive conditions remain shaped by product customization, dealer reach, fleet service capability, and application-focused engineering. Suppliers differentiate through configurable platforms that match hospitality, airport, golf, and industrial use cases. The market also reflects a gradual tilt toward integrated fleet solutions, where durability, operating economics, and support responsiveness influence procurement decisions.

Low Speed Vehicle Market - Strategic Insights:

Get more information on this report

Low Speed Vehicle Market Segmentation Analysis:

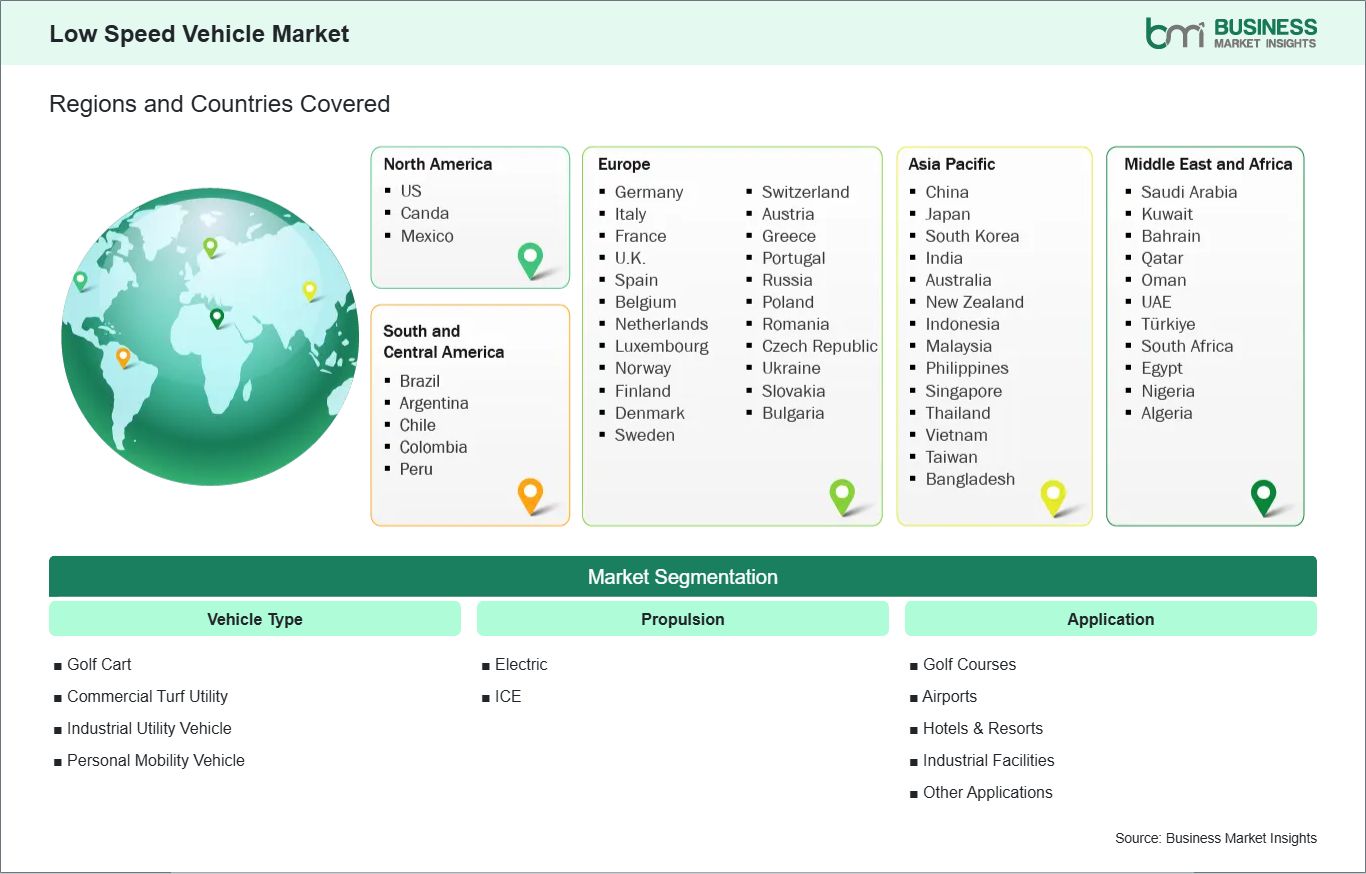

The Low Speed Vehicle market is segmented by vehicle type, propulsion, and application. Each category reflects distinct operating priorities and end-user purchase behavior.

By Vehicle Type

Golf Cart - Remains central to passenger movement across leisure-focused and managed property environments.

Commercial Turf Utility - Supports groundskeeping tasks with practical cargo handling and route flexibility.

Industrial Utility Vehicle - Addresses internal transport needs within warehouses, plants, and service complexes.

Personal Mobility Vehicle - Serves convenient short-range transport where compact footprint and comfort matter.

By Propulsion

Electric - Gains preference through quieter operation, simplified maintenance, and site-level sustainability goals.

ICE - Retains utility where refueling speed and extended duty cycles remain operational priorities.

By Application

Golf Courses - Anchors fleet demand through routine player transport and course operations.

Airports - Improves controlled-area mobility for personnel, luggage support, and passenger assistance.

Hotels & Resorts - Enhances guest movement and back-of-house transport across expansive properties.

Other Applications - Extends into campuses, residential communities, and institutional sites.

Low Speed Vehicle Market Drivers and Opportunities:

Rising Need for Efficient On-Site Mobility

Large properties require transport systems that handle short, repetitive routes without the cost profile of full-sized vehicles. That need is strengthening interest in low speed vehicles across golf courses, resorts, airports, and industrial sites. Operators favor platforms that move people, tools, or light cargo efficiently while fitting narrow pathways, service corridors, and managed traffic environments.

The impact is visible in fleet planning, where procurement decisions increasingly emphasize utilization, route suitability, and operating convenience. Low speed vehicles align with sites that value quiet movement, compact parking, and simplified driver training. Their relevance continues to widen as facilities seek transport assets that support daily operations without introducing unnecessary vehicle complexity.

Electrification and Connected Fleet Management

A clear opportunity is emerging from the combination of electric propulsion and digital fleet tools. Operators are showing interest in vehicles equipped with better charging control, battery monitoring, and basic telematics visibility. These capabilities improve dispatching, reduce avoidable downtime, and support use cases where predictable route cycles and property-wide coordination matter.

Future scope lies in broader deployment across mixed-use campuses, hospitality clusters, and industrial estates seeking cleaner internal mobility systems. As product configurations become more specialized, suppliers can address guest transport, maintenance support, and utility tasks with greater precision. This expansion can strengthen operational efficiency while widening the market’s application footprint over time.

Low Speed Vehicle Market Size and Share Analysis:

The Low Speed Vehicle market size is expected to reach US$ 19.72 Billion by 2033 from US$ 11.82 Billion in 2025. The market is estimated to record a CAGR of 5.76% from 2026 to 2033. This trajectory reflects broader use of compact mobility fleets in environments where short-distance transport efficiency, operational convenience, and lower site-level emissions are becoming more important procurement considerations.

By segment, golf carts hold a prominent position because they remain deeply embedded in established course fleets and adjacent leisure properties. Electric propulsion is strengthening its standing as buyers prioritize quieter operation and easier upkeep. Commercial turf utility and industrial utility vehicles also contribute meaningfully, particularly where properties require dependable movement of personnel, supplies, and maintenance equipment.

Across applications, golf courses remain the most visible demand center because fleet replacement cycles and daily usability sustain consistent purchasing interest. Hotels and resorts follow through guest mobility requirements and property services, while airports and industrial facilities strengthen demand through controlled-area transport needs. The application mix highlights the marke's dependence on localized, repetitive, and operationally focused movement patterns.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Club Car, LLC

Yamaha Golf-Car Company

Textron Inc.

Polaris Inc.

Deere & Company

Kubota Corporation

Columbia Vehicle Group Inc.

Speedways Electric

Marshell Green Power Co., Ltd.

Suzhou Eagle Electric Vehicle Manufacturing Co., Ltd.

Get more information on this report

Low Speed Vehicle Market Report Coverage and Deliverables:

The " Low Speed Vehicle Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Low Speed Vehicle Market Geographic Insights:

The Low Speed Vehicle market shows diverse regional adoption patterns influenced by infrastructure design, fleet operating practices, and end-use concentration across managed environments. Globally, the market reflects a balance between leisure mobility, utility transport, and internal site logistics. Demand strengthens where operators value compact vehicles that can circulate efficiently through campuses, hospitality properties, and controlled-access facilities.

North America remains a mature regional landscape shaped by established golf infrastructure, resort mobility usage, and broad familiarity with property-scale transport fleets. Procurement trends favor configurable vehicles that support passenger movement, utility work, and neighborhood-style applications. The region also benefits from strong aftermarket networks, which influence replacement decisions and support continued deployment across commercial and recreational settings.

Asia Pacific presents a different expansion profile, with adoption linked to tourism infrastructure, industrial site development, and localized mobility needs within large properties. Buyers increasingly evaluate operating cost, maneuverability, and suitability for multi-use facilities. As hospitality projects and organized campus environments broaden across the region, the market gains support from practical transport requirements rather than recreational use alone.

Europe contributes through demand for efficient internal transport in resorts, institutional campuses, and service-oriented commercial sites, while emerging markets add momentum through new property developments and industrial modernization. In these regions, vehicle selection often reflects terrain, maintenance capability, and energy preference. This combination creates a regionally varied but steadily broadening market base for low speed vehicle deployment.

Get more information on this report

Low Speed Vehicle Market Research Report Guidance:

The report includes qualitative and quantitative data in the market across Vehicle Type, Propulsion, Application and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover market segments by Vehicle Type, Propulsion, Application and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Low Speed Vehicle Market News and Key Development:

Recent developments reflect continued product refinement and stronger emphasis on electric and utility-focused fleet applications. The following updates highlight notable activity relevant to the Low Speed Vehicle market.

In November 2025, Zelio E-Mobility has expanded its Eeva product portfolio with the introduction of three electric scooters targeting the low-speed EV segment. On November 6, 2025, the company launched two new models, the Eeva Eco LX and Eeva Eco ZX, along with an updated version of the Eeva ZX Plus.

In March 2026, Club Car proudly introduces the all-new Onward LSV (Low-Speed Vehicle), the company's most advanced personal vehicle yet. Designed for street-legal driving, the Onward LSV blends luxury, performance, and safety making it the ideal choice for everyday neighborhood use and beyond. The Onward LSV is built for life on the move. From dropping kids off at school, heading out for date night, or running weekend errands, this vehicle brings automotive-style engineering and must-have features to create a seamless mix of fun and function..

Key Sources Referred:

World Bank -Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Low Speed Vehicle Market

Club Car, LLC

Yamaha Golf-Car Company

Textron Inc.

Polaris Inc.

Deere & Company

Kubota Corporation

Columbia Vehicle Group Inc.

Speedways Electric

Marshell Green Power Co., Ltd.

Suzhou Eagle Electric Vehicle Manufacturing Co., Ltd.

Frequently Asked Questions

How big is the Low Speed Vehicle Market?

The Low Speed Vehicle Market is valued at US$ 11.82 Billion in 2025, it is projected to reach US$ 19.72 Billion by 2033.

What is the CAGR for Low Speed Vehicle Market by (2026 - 2033)?

As per our report Low Speed Vehicle Market, the market size is valued at US$ 11.82 Billion in 2025, projecting it to reach US$ 19.72 Billion by 2033. This translates to a CAGR of approximately 5.76% during the forecast period.

What segments are covered in this report?

The Low Speed Vehicle Market report typically cover these key segments-

Vehicle Type (Golf Cart, Commercial Turf Utility, Industrial Utility Vehicle, Personal Mobility Vehicle)

What is the historic period, base year, and forecast period taken for Low Speed Vehicle Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Low Speed Vehicle Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Low Speed Vehicle Market?

The Low Speed Vehicle Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Club Car, LLC

Yamaha Golf-Car Company

Textron Inc.

Polaris Inc.

Deere & Company

Kubota Corporation

Columbia Vehicle Group Inc.

Speedways Electric

Marshell Green Power Co., Ltd.

Suzhou Eagle Electric Vehicle Manufacturing Co., Ltd.

Who should buy this report?

The Low Speed Vehicle Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Low Speed Vehicle Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Low Speed Vehicle Market

Get Free Sample For Low Speed Vehicle Market