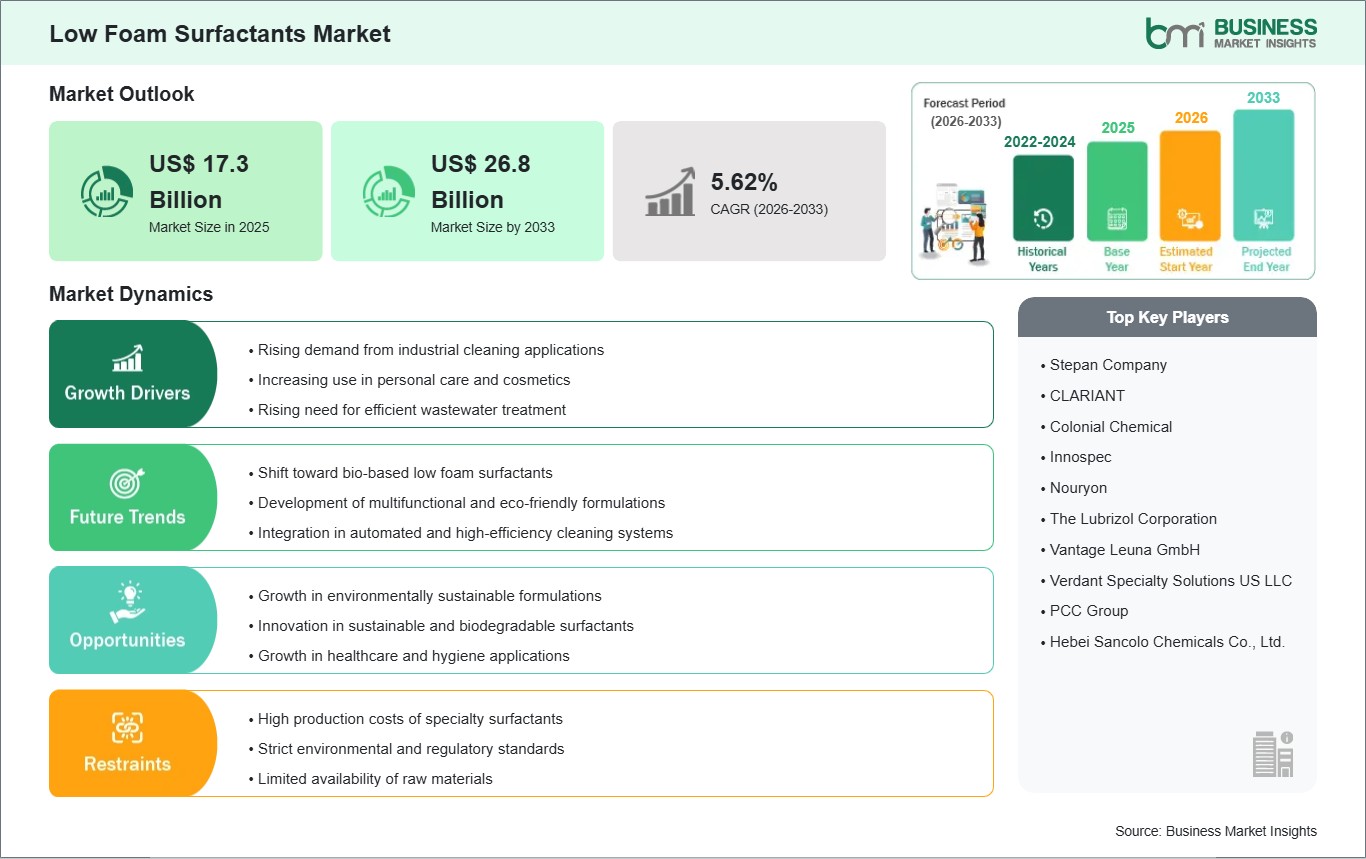

The Low Foam Surfactants Market size is expected to reach US$ 26.8 Billion by 2033 from US$ 17.3 Billion in 2025. The market is estimated to record a CAGR of 5.62% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The low-foam surfactant market is growing as companies look for formulations that provide optimal cleaning, emulsifying, and wetting performance with minimal foam. Low-foam surfactants are critical in automated systems, high-speed industrial washers, and closed-loop systems since excessive foam can hinder processes, create maintenance problems, and compromise the quality of products. Key end-use industries include metalworking, pulp and paper, textile finishing, oilfield chemicals, and institutional cleaning, which indicates the industrial nature of this market segment.

As new nonionic, anionic, and modified surfactant chemistries are developed, more tailored low-foam profiles can be created that retain high surface activity across temperature ranges, pH levels, and solvent conditions. Environmental regulations and sustainability initiatives are also affecting this market as companies continue to develop biodegradable, non-toxic, and eco-friendly products. Furthermore, the exploration of bio-based alternatives and strategic sourcing of feedstocks is increasing due to volatility in the pricing of petrochemical inputs. Companies that are focused on integrating innovation, sustainability, and operational efficiency into their product offerings are best positioned to take advantage of new growth opportunities and strengthen their position in this niche market segment.

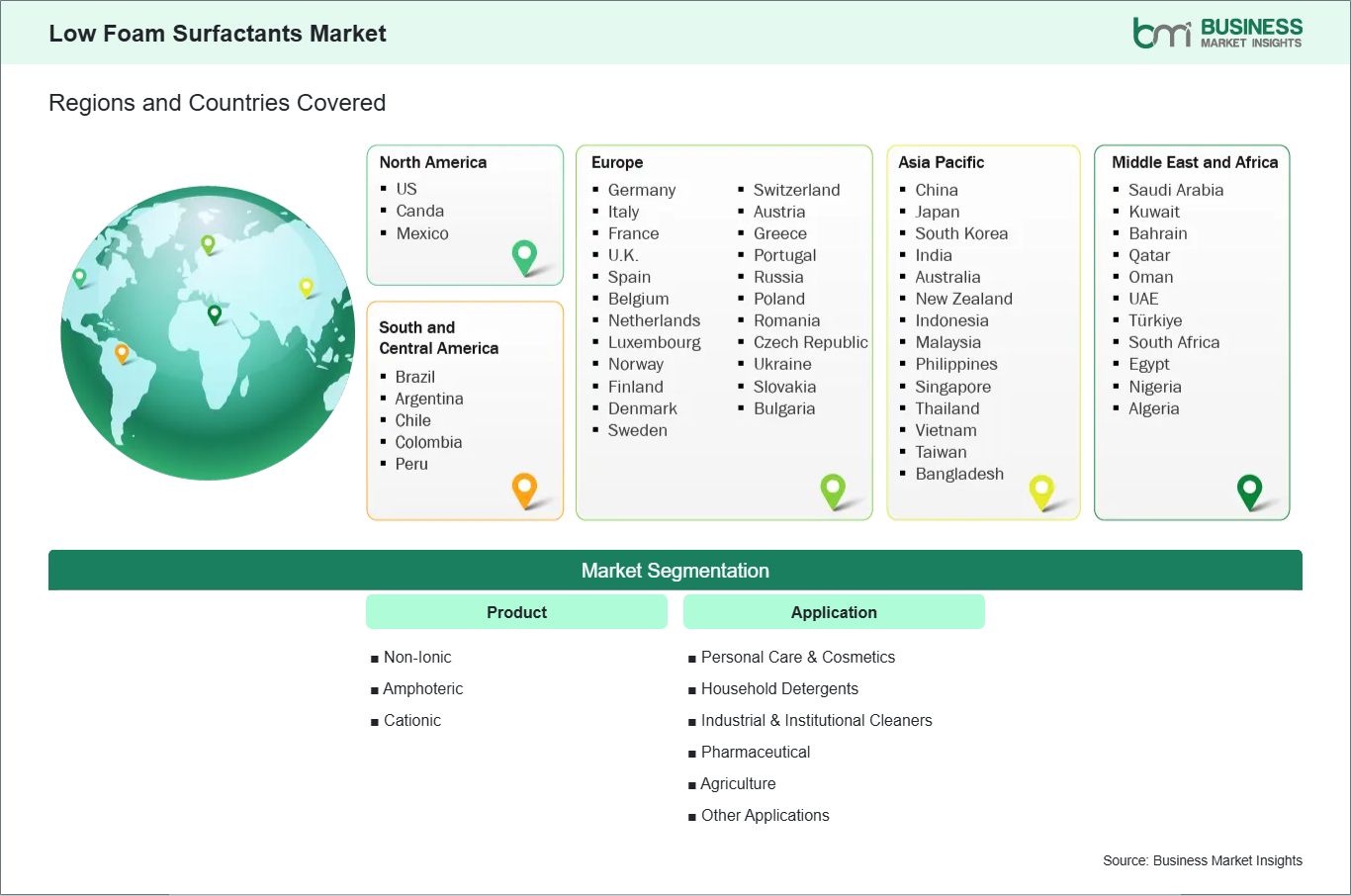

Key segments that contributed to the derivation of the low foam surfactants market analysis are product and application.

Product, the low foam surfactants market is segmented into non‑ionic, amphoteric, and cationic surfactants. The non‑ionic segment dominated the market in 2025.

Application, the low foam surfactants market is classified into personal care & cosmetics, household detergents, industrial & institutional cleaners, pharmaceutical, agriculture, and other applications. The personal care & cosmetics segment dominated the market in 2025.

Low Foam Surfactants Market Drivers and Opportunities:

Rising demand from industrial cleaning applications

As the demand for efficient and specialized cleaning products in the industry continues to rise, so too does the impetus to utilize low-foam surfactants (LFS) within the global surfactant market. Industrial applications such as textiles, paper manufacturing, metal processing and food ways are constantly under pressure to utilize surfactants that deliver optimal cleaning performance while generating minimal foam (which can hinder machinery operation and process efficiency). The desire to maximize operational efficiencies within these industries is thus prompting them to increasingly incorporate LFS into their industrial formulations as a key component. As the complexity of cleaning requirements increases in many of these industrial sectors, there is a growing trend to select formulations that possess both low-foam property characteristics along with enhanced solubility and stability. As a result of this trend, manufacturers are actively developing surfactants that can perform effectively over a wide variety of temperatures, water hardness levels and chemical environments; this allows industrial processes to continue to function smoothly without sacrificing the quality of the cleaning; this is critical in today's business environment due to increased levels of competitive pressure and costs associated with productivity. The selection of surfactants in industrial applications is also affected by regulatory and safety factors. Many companies are looking for solutions that reduce waste, minimize chemical handling risks and provide compliance with environmental standards. Furthermore, with the increasing emphasis on sustainable operation and optimization of their processes, companies are finding that low-foam surfactants are an excellent alternative to conventional surfactants in their industrial cleaning applications; thereby supporting the overall positive growth of the global low-foam surfactant market in each affected sector.

Growth in environmentally sustainable formulations

Innovation in environmentally sustainable low foam surfactants is creating significant opportunities for market expansion. Manufacturers are focusing on developing biodegradable and bio-based surfactants that offer low foaming performance without compromising cleaning efficiency. This trend is driven by growing regulatory pressure to reduce environmental impact, coupled with rising consumer and industrial preference for greener chemicals in production and maintenance processes. R&D efforts are aimed at balancing surfactant performance with sustainability, including enhancing biodegradability, reducing toxicity, and optimizing compatibility with other formulation ingredients. Companies are introducing solutions suitable for a wide variety of industrial applications, from hard surface cleaners to metalworking fluids and paper processing agents. These innovations allow industries to meet sustainability objectives while maintaining operational effectiveness, creating a clear market advantage for early adopters. Furthermore, the integration of sustainable surfactant formulations into existing processes is encouraging broader market adoption. Partnerships between chemical manufacturers and industrial end-users are facilitating the development of customized low foam solutions tailored to specific process requirements. The focus on eco-friendly innovation is positioning the low foam surfactants market for long-term growth and enabling industries to align operational efficiency with environmental responsibility.

Low Foam Surfactants Market Size and Share Analysis:

The Low Foam Surfactants Market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within product and application, offering insights into their contribution to overall market performance.

By Product, the non‑ionic surfactant subsegment dominated the market in 2025, driven by its broad compatibility, effective foam suppression, and versatility across cleaning and personal care formulations.

Based on Application, the personal care & cosmetics subsegment led the market in 2025, supported by rising consumer demand for mild, low‑foam products in shampoos, body washes, and facial cleansers.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Stepan Company

CLARIANT

Colonial Chemical

Innospec

Nouryon

The Lubrizol Corporation

Vantage Leuna GmbH

Verdant Specialty Solutions US LLC

PCC Group

Hebei Sancolo Chemicals Co., Ltd.

Get more information on this report

Low Foam Surfactants Market Report Coverage and Deliverables:

The "Low Foam Surfactants Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Low Foam Surfactants Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Low Foam Surfactants Market trends, as well as drivers, restraints, and opportunities

Low Foam Surfactants Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Low Foam Surfactants Market

Detailed company profiles, including SWOT analysis

Low Foam Surfactants Market Geographic Insights:

The geographical scope of the Low Foam Surfactants Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

Regional trends in the low foam surfactants market vary based on industrial activity, regulatory frameworks, and technical requirements. North America leads, driven by advanced manufacturing sectors in aerospace, automotive, and institutional cleaning, where precise foam control is crucial for high-speed operations and automated processes. Europe is a strong market, particularly in Germany, France, and the UK, where strict environmental regulations and REACH compliance are accelerating adoption of biodegradable, low-toxicity surfactants for pulp and paper, metal finishing, and industrial cleaning applications.

In Asia Pacific, industrialization in China, India, Japan, and South Korea is fueling demand, especially in textiles, metal fabrication, and institutional hygiene, supported by process automation and efficiency standards. Middle East & Africa is emerging, primarily in oilfield chemicals and industrial cleaning, with adoption growing alongside infrastructure modernization.

South & Central America, notably Brazil, Argentina, and Mexico, is expanding steadily, with industries integrating low foam surfactants to reduce chemical use, improve operational efficiency, and meet rising environmental expectations. Across all regions, technical customization, sustainability, and performance consistency remain key drivers shaping market leadership.

Get more information on this report

Low Foam Surfactants Market Research Report Guidance:

The report includes qualitative and quantitative data in the Low Foam Surfactants Market across product, application and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Low Foam Surfactants Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Low Foam Surfactants Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Low Foam Surfactants Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 9 cover Low Foam Surfactants Market segments across product, application, and geography across North America, Asia Pacific, Europe, the Middle East & Africa, and South & Central America. They cover the market revenue forecast and factors driving the market.

Chapter 10 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 11 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 12 provides detailed profiles of the major companies operating in the Low Foam Surfactants Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 13, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Low Foam Surfactants Market News and Key Development:

The Low Foam Surfactants Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the low foam surfactants market are:

In January 2024, Evonik Industries AG announced that it had manufactured the first product from its new industrial‑scale sustainable biosurfactants facility in Slovakia, producing rhamnolipid biosurfactants with low‑foam properties for cleaning and personal care applications marking a significant manufacturing milestone in bio‑based surfactants.

In February 2024, BASF SE expanded its presence in low‑foam and biodegradable surfactants by inaugurating the expansion of its alkyl polyglucoside (APG) production capacity at its Bangpakong site in Thailand, strengthening regional supply for sustainable surfactants used in personal care, industrial cleaning, and related applications.

Key Sources Referred:

International Organization for Standardization (ISO)American Society for Testing and Materials (ASTM International)Bureau of Indian Standards (BIS)Environmental Protection Agency (EPA), USAEuropean Chemicals Agency (ECHA)Central Pollution Control Board (CPCB), IndiaMinistry of Chemicals and Fertilizers, IndiaAmerican Chemistry Council (ACC)Indian Chemical Council (ICC)European Chemical Industry Council (Cefic)Specialty Chemical Association of India (SCAI)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Low Foam Surfactants Market

Stepan Company

CLARIANT

Colonial Chemical

Innospec

Nouryon

The Lubrizol Corporation

Vantage Leuna GmbH

Verdant Specialty Solutions US LLC

PCC Group

Hebei Sancolo Chemicals Co., Ltd.

Frequently Asked Questions

How big is the Low Foam Surfactants Market?

The Low Foam Surfactants Market is valued at US$ 17.3 Billion in 2025, it is projected to reach US$ 26.8 Billion by 2033.

What is the CAGR for Low Foam Surfactants Market by (2026 - 2033)?

As per our report Low Foam Surfactants Market, the market size is valued at US$ 17.3 Billion in 2025, projecting it to reach US$ 26.8 Billion by 2033. This translates to a CAGR of approximately 5.62% during the forecast period.

What segments are covered in this report?

The Low Foam Surfactants Market report typically cover these key segments-

Product (Non-Ionic, Amphoteric, Cationic)

Application (Personal Care & Cosmetics, Household Detergents, Industrial & Institutional Cleaners, Pharmaceutical, Agriculture, Other Applications)

What is the historic period, base year, and forecast period taken for Low Foam Surfactants Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Low Foam Surfactants Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Low Foam Surfactants Market?

The Low Foam Surfactants Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Stepan Company

CLARIANT

Colonial Chemical

Innospec

Nouryon

The Lubrizol Corporation

Vantage Leuna GmbH

Verdant Specialty Solutions US LLC

PCC Group

Hebei Sancolo Chemicals Co., Ltd.

Who should buy this report?

The Low Foam Surfactants Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Low Foam Surfactants Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Low Foam Surfactants Market

Get Free Sample For Low Foam Surfactants Market