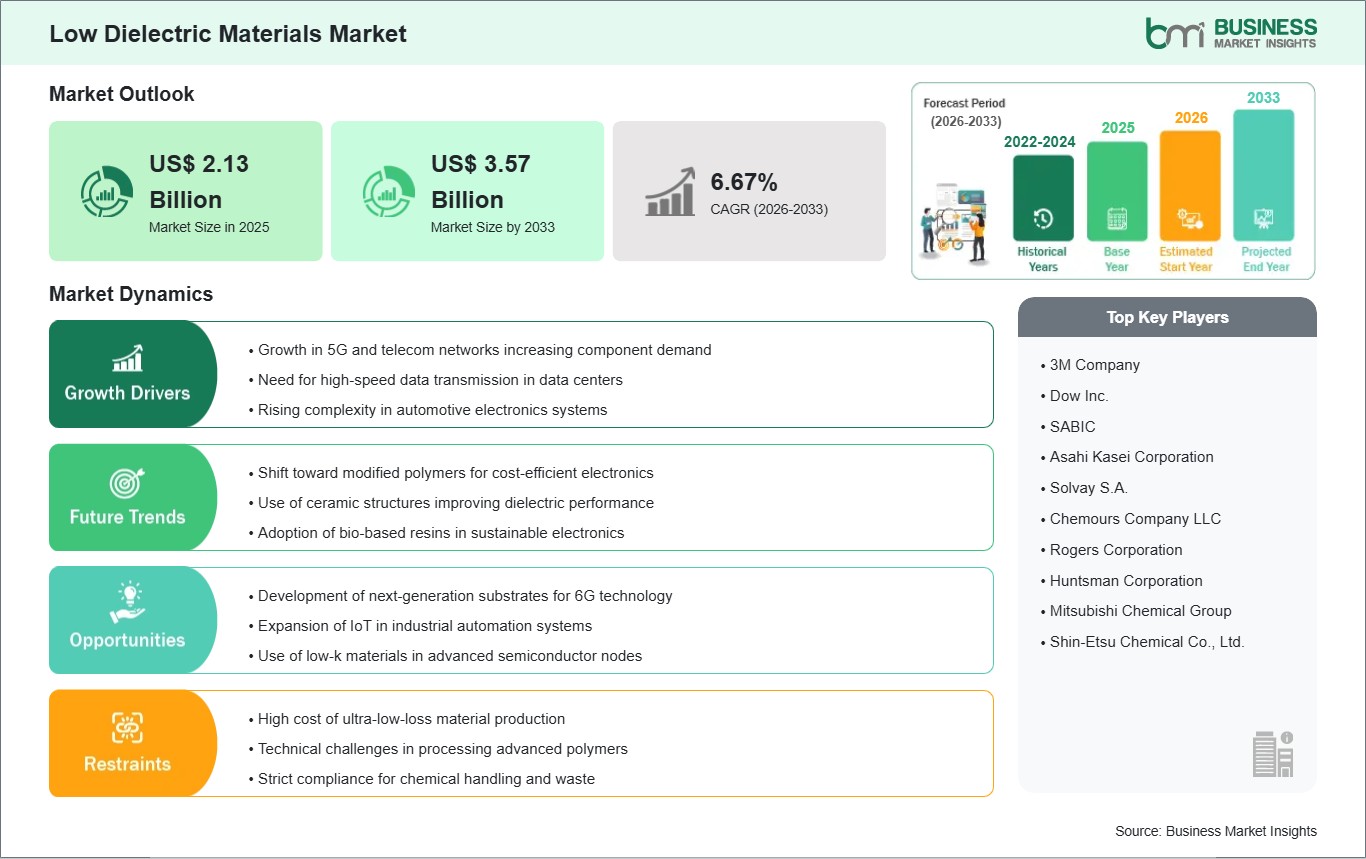

The Low Dielectric Materials Market size is expected to reach US$ 3.57 Billion by 2033 from US$ 2.13 Billion in 2025. The market is estimated to record a CAGR of 6.67% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The world market for low dielectric materials is in an era of intense technological development, mainly driven by the growing demands of high-frequency electronic devices. With the telecommunications and data processing industries moving towards higher speeds and bandwidths in information transmission, it is imperative that insulating materials also develop to ensure that there is no degradation in signals and loss in transmitted energy. These materials, with their low dielectric constant and dissipation factor, have been the unsung heroes in our journey towards modern-day technology and computing. The world market for low dielectric materials is presently dominated by high-performance polymers and ceramics.

This market growth is also fueled by the general trend in the world towards the miniaturization of electronic devices, which demands materials with consistent electrical properties, even in extremely thin layers or complex three-dimensional structures. Although the telecommunication industry is the main driver of market volume, the automobile and aerospace industries are gaining importance as key high-value segments. Despite the challenges of high material costs and complex manufacturing processes, the industry's focus on innovation, coupled with the trend towards sustainable, recyclable materials, promises a bright future. The market is highly competitive, with a strong focus on research and development to meet the requirements of future 6G and AI technologies.

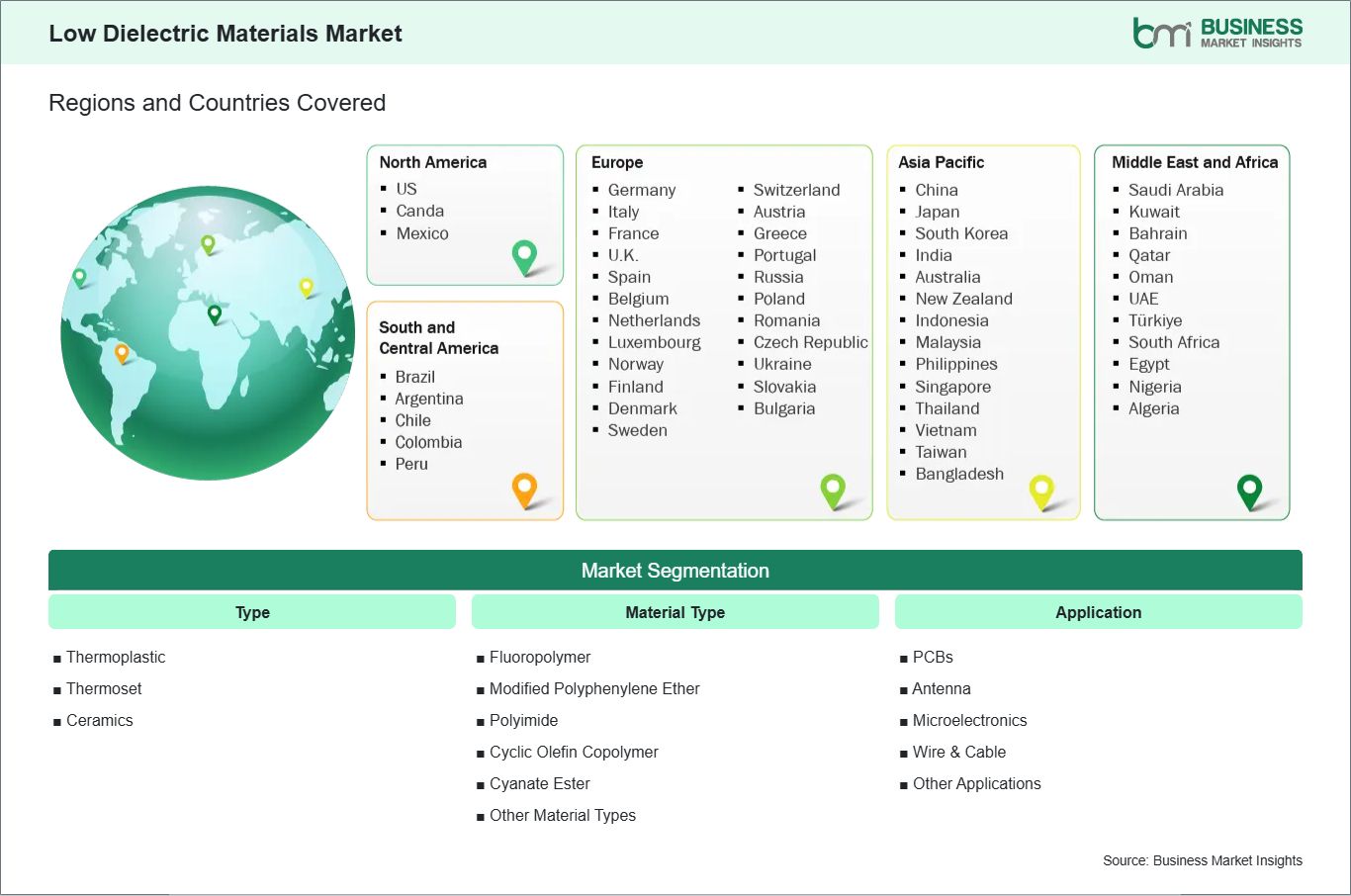

Key segments that contributed to the derivation of the Low Dielectric Materials market analysis are type, material type, and application.

By type, the low dielectric materials market is segmented into Thermoplastic, Thermoset, and Ceramics. The Thermoset segment dominated the market in 2025.

By material type, the low dielectric materials market is segmented into Fluoropolymer, Modified Polyphenylene Ether, Polyimide, Cyclic Olefin Copolymer, Cyanate Ester, and Other Material Types. The Fluoropolymer segment dominated the market in 2025.

By application, the low dielectric materials market is segmented into PCBs, Antenna, Microelectronics, Wire & Cable, and Other Applications. The PCBs segment dominated the market in 2025.

Low Dielectric Materials Market Drivers and Opportunities:

Surging global deployment of 5G and mmWave telecommunications networks

The move to fifth-generation wireless technology is a big change for the electronics materials industry. 5G networks work at much higher frequencies than older networks, so they need hardware that can handle millimeter-wave signals without losing much energy. At these frequencies, traditional insulating materials often have a lot of signal loss, which can cause overheating and a shorter network range. Because of this, there is a specific need for advanced polymers and ceramics that have a very low dielectric constant and loss tangent. These materials keep the signal clear and prevent the base stations from using too much power.

The rise of 5G-enabled consumer devices, such as smartphones and wearables, has made it necessary to redesign the internal parts of the infrastructure itself. To keep high data rates in hardware environments that are getting more crowded, antennas and internal circuit substrates need to be more efficient. To meet these strict standards, manufacturers are aggressively looking for high-purity polyimides and liquid crystal polymers. This demand isn't just about performance; it's also about making sure the network can do what it's supposed to do. As global coverage grows, the need for high-frequency hardware keeps growing. This creates a steady and recession-proof engine for the materials market.

Development of next-generation 6G compatible dielectric substrates

While 5G is being rolled out, the research and development community is already focusing on 6G, which is expected to use the terahertz frequency spectrum. Operating at these extreme levels brings a new set of challenges that current materials cannot completely solve. This gap has created a big opportunity for companies to innovate ultra-low-k dielectric substrates that provide near-zero signal interference. These materials are being designed with controlled porosity and precise molecular structures to ensure the necessary electrical insulation while meeting the massive bandwidth needs of the future. The first movers in this area are likely to secure high-margin contracts for pilot infrastructure and advanced research equipment.

This opportunity involves satellite communications and deep-space exploration, where high-frequency data links are essential. As the world shifts toward a more connected global satellite network, the hardware on these orbital platforms needs to be durable and energy-efficient. There is a high demand for low dielectric materials that can endure the vacuum of space and solar radiation while keeping their electrical properties. Creating these specialized materials requires teamwork between chemical manufacturers and aerospace designers. By establishing a presence in 6G development now, material providers are placing themselves at the leading edge of a technological cycle that will reshape global connectivity for decades to come.

Low Dielectric Materials Market Size and Share Analysis:

The global Low Dielectric Materials market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within type, material type, and application, highlighting their respective contributions to overall market performance.

By type, the Thermoset subsegment dominated the market in 2025 due to its superior dimensional stability and high resistance to deformation under extreme thermal stress, making it the industry standard for high-density interconnects and structural electronics that require long-term reliability.

By material type, the Fluoropolymer subsegment dominated the market in 2025 because it offers an unrivaled combination of ultra-low dielectric constant and chemical inertness, which is essential for maintaining signal integrity in high-frequency 5G infrastructure and specialized aerospace communication systems.

By application, the PCBs subsegment dominated the market in 2025 as the rapid expansion of high-speed computing and advanced telecommunications increased the demand for multi-layered circuit boards that rely on low-loss substrates to minimize signal attenuation and crosstalk.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

3M Company

Dow Inc.

SABIC

Asahi Kasei Corporation

Solvay S.A.

Chemours Company LLC

Rogers Corporation

Huntsman Corporation

Mitsubishi Chemical Group

Shin-Etsu Chemical Co., Ltd.

Get more information on this report

Low Dielectric Materials Market Report Coverage and Deliverables:

The "Low Dielectric Materials Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Low Dielectric Materials market size and forecast at the regional and country levels for segments covered under the scope

Low Dielectric Materials market trends, as well as drivers, restraints, and opportunities

Low Dielectric Materials market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Low Dielectric Materials market

Detailed company profiles, including SWOT analysis

The geographical scope of the Low Dielectric Materials market report is divided into: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America dominates the low dielectric materials market because it is the world center for semiconductors and the design of advanced telecommunications. The region also hosts some of the world’s greatest technology companies and defense firms responsible for setting the guidelines for next-generation communication standards. Such leadership enables low dielectric material suppliers to be located near end-users for quick prototyping and quick uptake of advanced dielectric solutions. Focus on the U.S. has been evident in domestic chip production, 5G building efforts, and stabilizing demand for top-tier PCBs and antenna components.

The region’s dominance is also reinforced by a strong regulatory framework and institutional support for technological innovation in the defense and aerospace sectors. Low dielectric materials are critical for stealth technology, radar systems, and secure satellite communications, all of which are priority areas for North American national security. Additionally, the presence of a mature venture capital ecosystem allows for the continuous funding of startups focused on material science and nanotechnology, keeping the region at the cutting edge of the industry. As North America continues to push the boundaries of high-speed computing and artificial intelligence, the demand for superior insulating materials that can support these energy-intensive and high-frequency environments is expected to remain the highest in the world.

Get more information on this report

Low Dielectric Materials Market Research Report Guidance:

The report includes qualitative and quantitative data in the Low Dielectric Materials market across type, material type, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Low Dielectric Materials market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Low Dielectric Materials market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Low Dielectric Materials market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover the Low Dielectric Materials market segments by type, material type, application, and geography across North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Low Dielectric Materials market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Low Dielectric Materials Market News and Key Development:

The Low Dielectric Materials market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Low Dielectric Materials market are:

In February 2024, SABIC, announced new damp heat performance data for its Elcres™ HTV150A dielectric films at APEC 2024, demonstrating enhanced reliability for high-temperature electronic applications such as capacitors.

In October 2024, DIC Corporation, in collaboration with Unitika, announced the development of a low-dielectric PPS film designed for millimeter-wave PCB and radar applications, supporting high-frequency communication systems.

In 2023, DuPont, announced continued advancements in low dielectric constant materials for semiconductor and advanced packaging applications, focusing on reducing signal loss and improving performance in high-speed computing environments.

Key Sources Referred:

American Chemistry Council (ACC)International Council of Chemical Associations (ICCA)European Chemical Industry Council (Cefic)China National Building Materials Group (CNBM)Indian Minerals & Granite Exporters Association (IMGEA)Japan Mining Industry Association (JMIA)Brazilian Mining Association (IBRAM)Gulf Petrochemicals and Chemicals Association (GPCA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Low Dielectric Materials Market

3M Company

Dow Inc.

SABIC

Asahi Kasei Corporation

Solvay S.A.

Chemours Company LLC

Rogers Corporation

Huntsman Corporation

Mitsubishi Chemical Group

Shin-Etsu Chemical Co., Ltd.

About Author— Chemicals and Materials Research Team

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Show More

Frequently Asked Questions

How big is the Low Dielectric Materials Market?

The Low Dielectric Materials Market is valued at US$ 2.13 Billion in 2025, it is projected to reach US$ 3.57 Billion by 2033.

What is the CAGR for Low Dielectric Materials Market by (2026 - 2033)?

As per our report Low Dielectric Materials Market, the market size is valued at US$ 2.13 Billion in 2025, projecting it to reach US$ 3.57 Billion by 2033. This translates to a CAGR of approximately 6.67% during the forecast period.

What segments are covered in this report?

The Low Dielectric Materials Market report typically cover these key segments-

Type (Thermoplastic, Thermoset, Ceramics)

Material Type (Fluoropolymer, Modified Polyphenylene Ether, Polyimide, Cyclic Olefin Copolymer, Cyanate Ester, Other Material Types)

Application (PCBs, Antenna, Microelectronics, Wire & Cable, Other Applications)

What is the historic period, base year, and forecast period taken for Low Dielectric Materials Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Low Dielectric Materials Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Low Dielectric Materials Market?

The Low Dielectric Materials Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

3M Company

Dow Inc.

SABIC

Asahi Kasei Corporation

Solvay S.A.

Chemours Company LLC

Rogers Corporation

Huntsman Corporation

Mitsubishi Chemical Group

Shin-Etsu Chemical Co., Ltd.

Who should buy this report?

The Low Dielectric Materials Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Low Dielectric Materials Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Low Dielectric Materials Market

Get Free Sample For Low Dielectric Materials Market