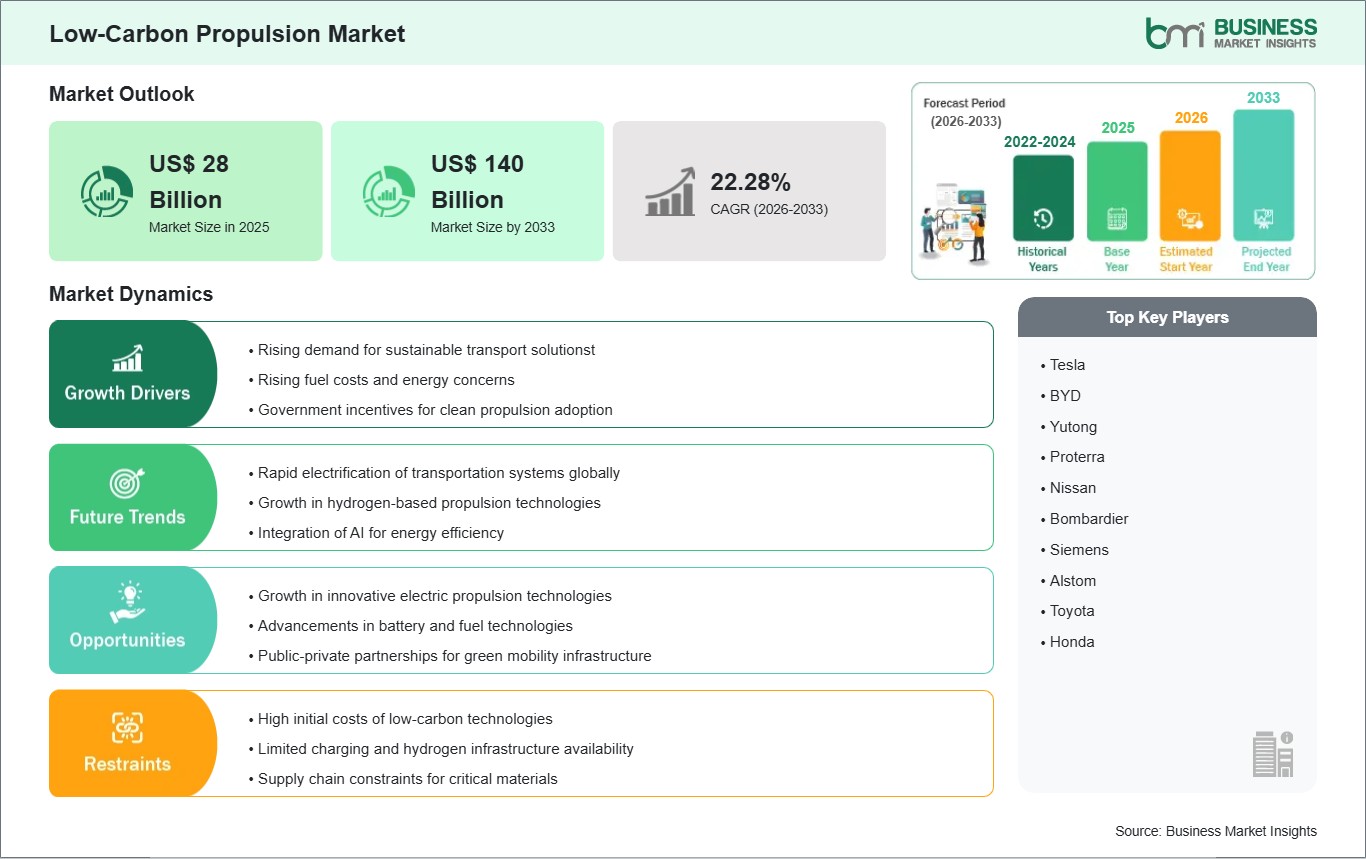

The Low-Carbon Propulsion Market size is expected to reach US$ 140 Billion by 2033 from US$ 28 Billion in 2025. The market is estimated to record a CAGR of 22.28% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The low‑carbon propulsion market is expanding rapidly as industries worldwide adopt sustainable mobility solutions and energy-efficient transportation methods. The automotive industry, the aerospace industry, the marine industry and the heavy-duty vehicle industry prioritize electric and hydrogen fuel-cell and biofuel and hybrid propulsion technologies. Regulatory mandates, which include strict emissions limits and zero-emission vehicle (ZEV) targets and sustainability frameworks, force OEMs and suppliers to fast-track their research and development efforts while expanding their propulsion system options. The passenger vehicle market and the commercial vehicle market show increasing demand for battery electric vehicles (BEVs) and modular hybrid systems, while hydrogen fuel cells and synthetic fuels gain popularity in heavy-duty transport and maritime applications.

Technological advancements in energy storage systems, power electronic devices and high-efficiency electric motors enable better performance and lower emissions throughout their lifecycle while making electric propulsion systems more affordable than traditional systems. Automotive companies, energy providers and component manufacturers are forming strategic partnerships to solve infrastructure problems, enhance supply chain efficiency and reduce total ownership costs. Market participants use financial tools like green bonds and carbon credits, and government incentives to speed up their market entry process. The global low-carbon propulsion market will benefit from technological innovation, which companies use with operational resilience and sustainability initiatives despite the challenges created by supply chain instability, their reliance on scarce materials and their insufficient charging and fueling infrastructure.

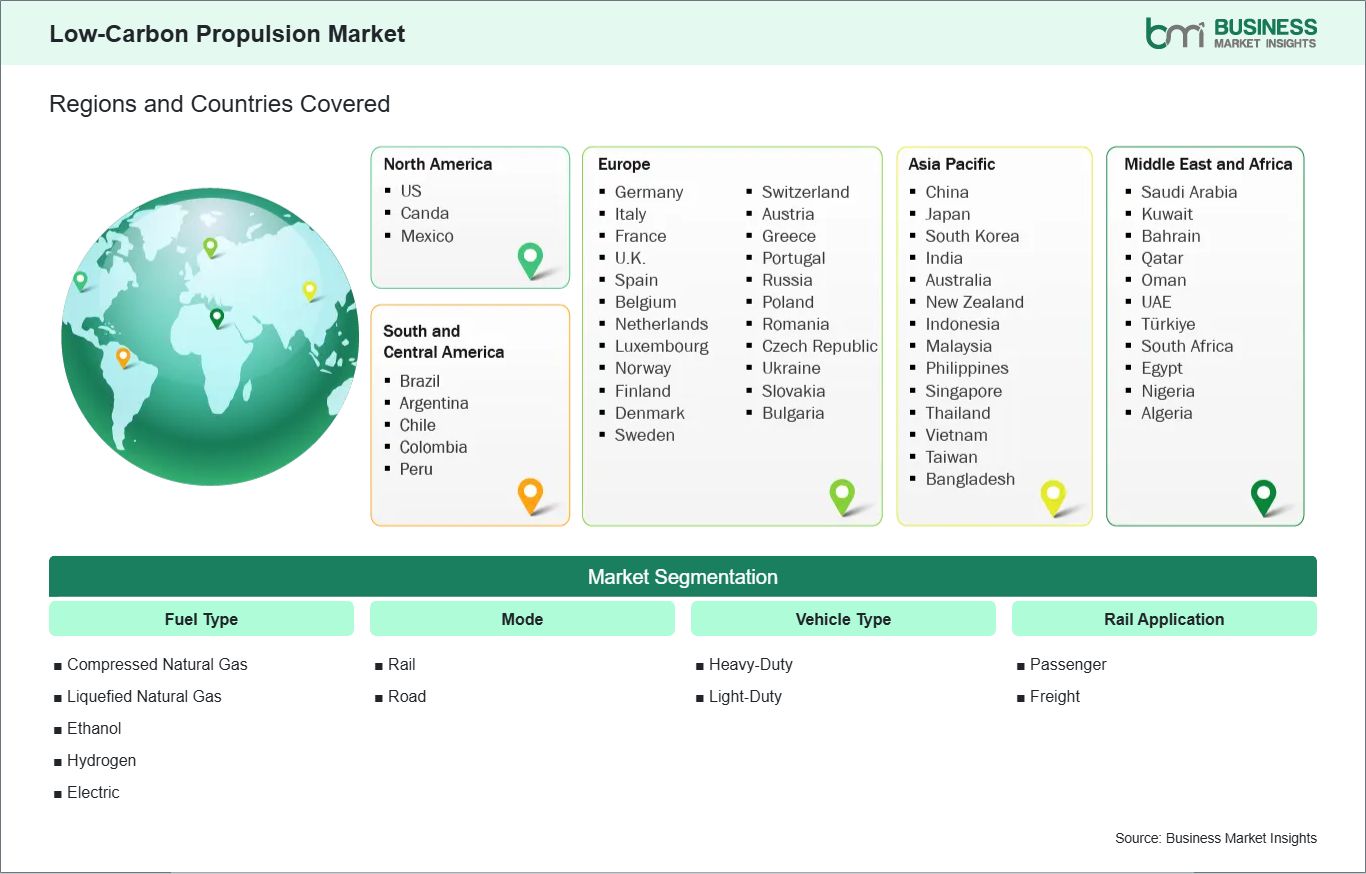

Key segments that contributed to the derivation of the low‑carbon propulsion market analysis are fuel type, mode, vehicle type, rail application, and electric vehicle type.

Fuel Type, the low‑carbon propulsion market is segmented into compressed natural gas (CNG), liquefied natural gas (LNG), ethanol, hydrogen, and electric. The electric segment dominated the market in 2025.

Mode, the low‑carbon propulsion market is categorized into rail and road. The road segment dominated the market in 2025.

Vehicle Type, the low‑carbon propulsion market is classified into heavy‑duty and light‑duty vehicles. The light‑duty segment dominated the market in 2025.

Rail Application, the low‑carbon propulsion market is segmented into passenger and freight. The passenger segment dominated in 2025.

Electric Vehicle Type, the low‑carbon propulsion market is further broken down into electric passenger car, electric bus, electric two‑wheeler, and electric off‑highway vehicle. The electric passenger car segment dominated in 2025.

Low‑Carbon Propulsion Market Drivers and Opportunities:

Rising demand for sustainable transport solutions

The global low-carbon propulsion market is experiencing a transformation because multiple regions are now adopting environmentally friendly transportation methods. The need for cleaner propulsion alternatives stems from established markets that already have emissions reduction regulations because they must decrease their emissions. The current transport planning process combines electrical system development with alternative fuel solutions to achieve decarbonization goals and better air quality results. The ongoing demand for low-carbon propulsion solutions has become a key focus area for both industrial and city transportation planners. The combined effect of strong manufacturing development and transportation policy incentives has resulted in rapid changes to fleet operations.

The shift from internal combustion engines to hybrid and electric drivetrains by urban bus networks and commercial vehicle segments creates a fundamental transformation in mobility service delivery. The market area is growing because investments in charging and refueling infrastructure, plus low emission vehicle procurement preferences, are expanding operations. Emerging economies are participating in market growth, but they adopt new technologies at different speeds. Public and private stakeholders are balancing infrastructure development with cost considerations, leading to phased deployment of low-carbon propulsion solutions. The example of electric bus rollouts and alternative fuel commercial fleet deployments shows how organizations now include eco-friendly transport solutions into their overall mobility plans, which increases regional demand and helps market development.

Growth in innovative electric propulsion technologies

The global low-carbon propulsion market experiences its biggest growth through innovations that create new electric propulsion technologies. The development of new battery systems, powertrain designs and propulsion control systems leads to better performance, energy efficiency and dependable operation of multiple vehicle types. The advanced R&D ecosystems in various markets have made it easier for electric and hybrid propulsion systems to gain acceptance in both light and heavy transport vehicles. The main manufacturers, together with the technology developers, are optimizing their electric propulsion systems through their efforts to enhance system integration, energy storage capabilities and operational effectiveness throughout the system's entire lifespan. Solid-state batteries, modular drive systems and hybrid engine systems create new competitive advantages that make these technologies suitable for both fleet operators and individual customers.

The partnership between original equipment manufacturers and technology companies drives the development of new solutions, which leads to the creation of additional market alternatives. Electric propulsion technologies expand their applications from passenger vehicles to public transportation and freight operations and business use in areas where electrification infrastructure experiences fast growth. The establishment of charging networks and their associated support systems enables a system to operate at its full capacity while maintaining dependable performance. The system's economic performance and resilience improvements result from developments in power electronics, smart energy management and grid resource integration, which establish electric propulsion as a fundamental element for worldwide low-carbon transportation solutions.

Low‑Carbon Propulsion Market Size and Share Analysis:

The Low‑Carbon Propulsion Market demonstrates steady growth, with size and share analysis highlighting evolving trends and competitive dynamics among key players. The report examines subsegments categorized within fuel type, mode, vehicle type, rail application, and electric vehicle type, offering insights into their contribution to overall market performance.

By Fuel Type, the electric subsegment dominated the market in 2025, driven by increasing demand for battery‑electric powertrains and stringent emission regulations incentivizing zero‑emission vehicles.

Based on Mode, the road subsegment dominated in 2025, owing to widespread adoption of low‑carbon propulsion solutions across passenger and commercial road vehicles.

On the Basis of Vehicle Type, the light‑duty vehicle subsegment led the market in 2025, supported by growth in last‑mile delivery vehicles and personal transport electrification.

From the Rail Application perspective, the passenger segment dominated in 2025 thanks to increasing deployment of eco‑friendly rail transport options.

Within Electric Vehicle Types, electric passenger cars held the largest share in 2025, reflecting strong consumer demand and policy support for electrified passenger mobility.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Tesla

BYD

Yutong

Proterra

Nissan

Bombardier

Siemens

Alstom

Toyota

Honda

Get more information on this report

Low‑Carbon Propulsion Market Report Coverage and Deliverables:

The "Low‑Carbon Propulsion Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Low‑Carbon Propulsion Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Low‑Carbon Propulsion Market trends, as well as drivers, restraints, and opportunities

Low‑Carbon Propulsion Market analysis covering key trends, global and regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Low‑Carbon Propulsion Market

Detailed company profiles, including SWOT analysis

Low‑Carbon Propulsion Market Geographic Insights:

The geographical scope of the Low‑Carbon Propulsion Market report is divided into North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

Regional trends in the low‑carbon propulsion market highlight differences in policy, infrastructure, and technology adoption across North America, Europe, Asia Pacific, the Middle East & Africa, and South & Central America. North America leads due to federal incentives, strict emissions regulations, and advanced R&D ecosystems supporting electrification, hydrogen corridors, and public transit electrification. The United States and Canada are prioritizing domestic manufacturing and supply chain localization to meet growing EV and fuel-cell demand. Europe is driven by aggressive climate goals, carbon pricing, and ZEV mandates, with Germany, France, and the Nordic countries pioneering hydrogen adoption for heavy transport, electrified rail, and industrial mobility.

In the Asia Pacific, China dominates electrified vehicle production and battery manufacturing, while Japan and South Korea focus on hydrogen propulsion and industrial electrification.

Middle East & Africa are emerging markets, investing in hydrogen hubs, renewable-powered transportation pilots, and low-carbon energy strategies despite infrastructure constraints.

South & Central America, particularly Brazil and Chile, is gradually adopting electric and hybrid mobility in urban transport and light commercial fleets, supported by renewable energy and sustainability initiatives. Across all regions, collaboration between policymakers, manufacturers, and technology providers remains critical to achieving scalable, low-carbon mobility solutions and meeting global decarbonization targets.

Get more information on this report

Low‑Carbon Propulsion Market Research Report Guidance:

The report includes qualitative and quantitative data in the Low‑Carbon Propulsion Market across fuel type, mode, vehicle type, rail application, electric vehicle type and geography.

The report starts with the key takeaways (chapter 2), highlighting key trends and outlook of the Low‑Carbon Propulsion Market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Low‑Carbon Propulsion Market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Low‑Carbon Propulsion Market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 12 cover Low‑Carbon Propulsion Market segments across fuel type, mode, vehicle type, rail application, electric vehicle type and geography across North America, Asia Pacific, Europe, the Middle East & Africa, and South & Central America. They cover the market revenue forecast and factors driving the market.

Chapter 13 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 14 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 15 provides detailed profiles of the major companies operating in the Low‑Carbon Propulsion Market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 16, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Low‑Carbon Propulsion Market News and Key Development:

The Low‑Carbon Propulsion Market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the low‑carbon propulsion market are:

In March 2025, GE Aerospace showcased advances in hybrid‑electric propulsion technologies, including multiple demonstrator programs (e.g., Sikorsky hybrid systems and MW‑class electrified powertrains) designed to accelerate integration of hybrid‑electric propulsion architectures in future aviation platforms.

In September 2025, GE Aerospace and BETA Technologies, Inc. announced a strategic partnership and equity investment, with GE committing approximately US$ 300 million to co‑develop hybrid‑electric turbogenerators aimed at enabling longer‑range, more efficient hybrid‑electric propulsion systems for advanced air mobility and regional aircraft applications.

Key Sources Referred:

International Organization for Standardization (ISO)American Society for Testing and Materials (ASTM International)Bureau of Indian Standards (BIS)Environmental Protection Agency (EPA), USAEuropean Chemicals Agency (ECHA)Central Pollution Control Board (CPCB), IndiaMinistry of Chemicals and Fertilizers, IndiaAmerican Chemistry Council (ACC)Indian Chemical Council (ICC)European Chemical Industry Council (Cefic)Specialty Chemical Association of India (SCAI)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Low‑Carbon Propulsion Market

Tesla

BYD

Yutong

Proterra

Nissan

Bombardier

Siemens

Alstom

Toyota

Honda

Frequently Asked Questions

How big is the Low‑Carbon Propulsion Market?

The Low‑Carbon Propulsion Market is valued at US$ 28 Billion in 2025, it is projected to reach US$ 140 Billion by 2033.

What is the CAGR for Low‑Carbon Propulsion Market by (2026 - 2033)?

As per our report Low‑Carbon Propulsion Market, the market size is valued at US$ 28 Billion in 2025, projecting it to reach US$ 140 Billion by 2033. This translates to a CAGR of approximately 22.28% during the forecast period.

What segments are covered in this report?

The Low‑Carbon Propulsion Market report typically cover these key segments-

Fuel Type (Compressed Natural Gas (CNG), Liquefied Natural Gas (LNG), Ethanol, Hydrogen, Electric)

Mode (Rail, Road)

Vehicle Type (Heavy-Duty, Light-Duty)

Rail Application (Passenger, Freight)

What is the historic period, base year, and forecast period taken for Low‑Carbon Propulsion Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Low‑Carbon Propulsion Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Low‑Carbon Propulsion Market?

The Low‑Carbon Propulsion Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Tesla

BYD

Yutong

Proterra

Nissan

Bombardier

Siemens

Alstom

Toyota

Honda

Who should buy this report?

The Low‑Carbon Propulsion Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Low‑Carbon Propulsion Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Low‑Carbon Propulsion Market

Get Free Sample For Low‑Carbon Propulsion Market