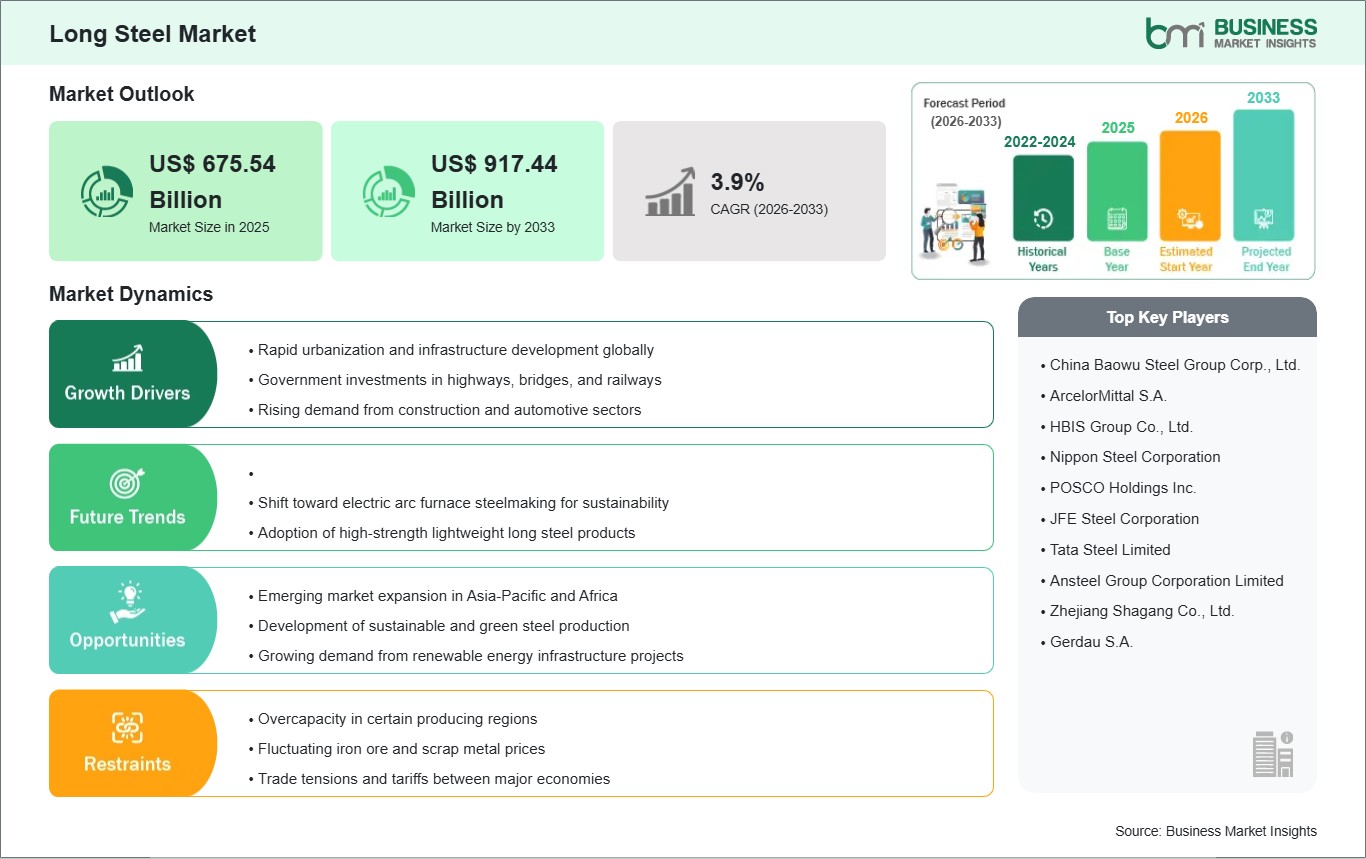

The Long Steel market size is expected to reach US$ 917.44 Billion by 2033 from US$ 675.54 Billion in 2025. The market is estimated to record a CAGR of 3.9% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Long steel products include elongated rolled steel forms such as rebar, wire rod, merchant bar, and rail used in load-bearing structures and engineered assemblies. Their mechanical strength, weldability, and processing flexibility make them central to civil works, industrial fabrication, transport systems, and reinforcement-intensive construction programs. This product group links upstream steelmaking capacity with downstream requirements for durability, formability, and structural reliability.

Market momentum is shaped by sustained project pipelines in transport corridors, urban utilities, logistics assets, and building renewal programs. Public capital spending supports baseline consumption, while private investment in industrial facilities and commercial developments sustains order visibility. Demand also reflects the need for steel grades that align with fabrication efficiency, lifecycle performance, and procurement consistency across large-volume projects.

Within segmentation, rebar holds a leading position because reinforced concrete remains the preferred construction method across many economies. Wire rod supports downstream conversion into fasteners, cables, and engineered components, while merchant bar serves fabrication-intensive uses across workshops and industrial plants. Rail remains a specialized category tied to network modernization, freight corridors, and metro expansion. Basic oxygen furnace production continues to support large integrated output, whereas electric arc furnace routes gain attention through scrap utilization and flexible melt scheduling.

Technology evolution in this sector centers on process efficiency, yield improvement, quality control, and emissions management rather than consumer-facing innovation. Producers are refining furnace operations, casting stability, and rolling precision to supply tighter tolerances and more consistent metallurgical properties. Digital monitoring, scrap optimization, and process integration are reshaping plant economics while supporting cleaner production pathways.

The competitive environment reflects a mix of integrated steelmakers, regional long-product specialists, and mills aligned with domestic construction cycles. Competitive positioning depends on capacity utilization, raw material access, product certification, distribution reach, and responsiveness to project-led demand. Producers that balance cost discipline with product consistency are better placed to navigate pricing pressure and changing trade conditions.

Long Steel Market - Strategic Insights:

Get more information on this report

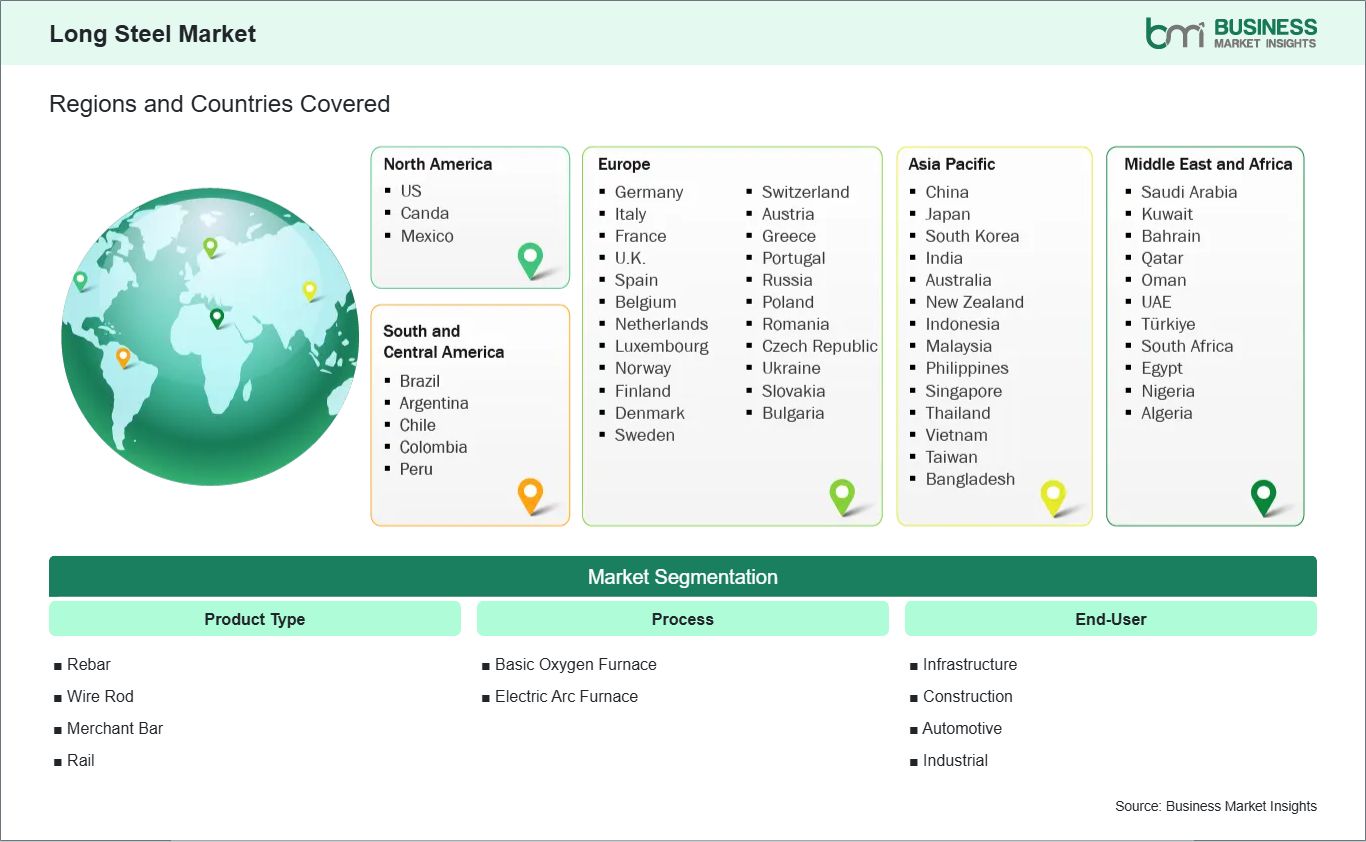

Long Steel Market Segmentation Analysis:

The market is segmented by product type, process, and end-user, reflecting distinct manufacturing economics and application needs.

By Product Type

Rebar: Reinforcement-led demand anchors its broad use across structural concrete projects.

Wire Rod: Downstream conversion supports cables, fasteners, springs, and industrial components.

Merchant Bar: Fabrication shops prefer it for frames, supports, and general engineering.

Rail: Network expansion sustains specification-driven procurement for transport infrastructure.

Electric Arc Furnace: Scrap-based melting improves flexibility and supports lower-emission pathways.

By End-User

Infrastructure: Large public works require durable steel for reinforced and linear assets.

Construction: Residential and commercial projects absorb substantial rebar and merchant bar volumes.

Automotive: Selected grades support forged parts, fasteners, suspension systems, and tire cord.

Industrial: Machinery, equipment, and fabrication demand versatile long-product formats.

Long Steel Market Drivers and Opportunities:

Infrastructure Renewal and Reinforcement-Intensive Construction

A broad pipeline of bridges, transit systems, utility corridors, and urban expansion projects continues to support long steel consumption. These assets require reinforcement materials, structural sections, and engineered bar products that can withstand repetitive loads and demanding site conditions. As project owners prioritize durability and execution speed, procurement teams increasingly favor standardized long steel formats that simplify fabrication, handling, and installation across high-volume construction programs.

The effect reaches beyond civil works because reliable long steel supply also supports industrial buildings, logistics facilities, and transport-linked development zones. In this context, the category remains relevant where project schedules depend on timely availability of rebar, wire rod, and merchant bar. Producers able to align output with contractor specifications and regional standards are positioned to capture recurring demand from institutional and private construction cycles.

Scrap-Based Steelmaking and Higher-Value Application Expansion

An important opportunity is emerging from the shift toward scrap-based melting, digital process control, and application-specific product development. Electric arc furnace configurations allow producers to adjust melt programs with greater flexibility while supporting customer interest in lower-emission material routes. This transition also encourages innovation in grades used for wire drawing, engineered reinforcement, and rail applications where consistency and traceability are becoming stronger purchasing considerations.

Future scope extends across specialized infrastructure, downstream conversion, and replacement demand in mature transport systems. Expansion in prefabricated construction, utility upgrades, and electrification-linked projects can widen the addressable base for long products with tighter performance requirements. As mills invest in cleaner operations and better finishing capabilities, the industry gains room to serve customers seeking dependable quality, shorter lead times, and more differentiated long steel solutions.

Long Steel Market Size and Share Analysis:

The Long Steel market size is expected to reach US$ 917.44 Billion by 2033 from US$ 675.54 Billion in 2025. The market is estimated to record a CAGR of 3.9% from 2026 to 2033. This trajectory indicates a large, steady industry shaped by essential material demand rather than short-cycle discretionary purchasing. Expansion remains tied to infrastructure execution, replacement cycles, and the need for structurally dependable steel inputs across construction and industrial supply chains.

By product and process, rebar commands broad volume relevance because concrete reinforcement remains fundamental across public and private building activity. Wire rod sustains downstream manufacturing needs, while merchant bar serves fabrication-intensive uses that value dimensional availability and processing ease. On the production side, basic oxygen furnace operations retain a strong position through integrated scale, although electric arc furnace routes are becoming more prominent where scrap access and decarbonization priorities shape investment choices.

By application, infrastructure represents the leading consumption base due to reinforcement demand in roads, rail systems, utilities, bridges, and civic assets. Construction also accounts for a substantial share through residential, commercial, and mixed-use projects requiring rebar and merchant bar inputs. Automotive and industrial uses provide additional depth through fasteners, spring steel, wire-based products, machinery components, and engineered applications that depend on predictable metallurgical performance.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

China Baowu Steel Group Corp., Ltd.

ArcelorMittal S.A.

HBIS Group Co., Ltd.

Nippon Steel Corporation

POSCO Holdings Inc.

JFE Steel Corporation

Tata Steel Limited

Ansteel Group Corporation Limited

Zhejiang Shagang Co., Ltd.

Gerdau S.A.

Get more information on this report

Long Steel Market Report Coverage and Deliverables:

The "Long Steel Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering the areas below:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Long Steel Market Geographic Insights:

The Long Steel market shows diverse regional adoption patterns influenced by infrastructure priorities, steelmaking capacity structures, trade exposure, and the pace of construction renewal. At a global level, consumption remains closely linked to public works execution, urban development cycles, and industrial capital formation. Regional differences emerge through scrap availability, policy support for domestic manufacturing, and the balance between integrated mills and recycling-based production routes.

North America reflects a market shaped by non-residential construction, transport maintenance, and manufacturing-linked downstream demand. Project specifications, domestic sourcing preferences, and modernization of public assets support stable usage of rebar, merchant bar, and wire rod products. Electric arc furnace production carries particular relevance in this region because scrap networks, flexible mill configurations, and shorter delivery windows align well with localized procurement requirements and evolving sustainability expectations.

Asia Pacific remains the most influential regional arena because large-scale urbanization, transport expansion, and industrial buildout continue to absorb extensive long steel volumes. The region includes both integrated steel hubs and fast-evolving electric arc furnace capacity, creating a broad manufacturing base for rebar, wire rod, and rail products. Procurement momentum is reinforced by metro systems, freight corridors, housing programs, and factory construction across several major economies.

Europe presents a more specification-driven environment where replacement demand, rail modernization, and industrial engineering applications support product movement. Market behavior is increasingly shaped by energy costs, environmental compliance, and interest in lower-emission steelmaking pathways. Beyond Europe, emerging markets in the Middle East, Africa, and South and Central America offer incremental opportunity through new urban infrastructure, logistics assets, and utility expansion, although demand patterns remain closely tied to investment timing and policy continuity.

Get more information on this report

Long Steel Market Research Report Guidance:

The report encompasses both qualitative and quantitative data pertaining to the market, categorized by product type, process, and end-user, and geographical regions.

Beginning with Chapter 2, the report presents key takeaways that underscore the primary trends and market outlook.

Chapter 3 is dedicated to outlining the research methodology employed in this study.

In Chapter 4, an ecosystem analysis is provided.

Chapter 5 delves into the significant industry dynamics affecting the market, including driving factors, existing challenges, potential opportunities, and emerging trends. This section also includes an impact analysis of these drivers and constraints.

Chapter 6 reviews the market scenario, detailing historical revenue figures and forecasts extending to the year 2033.

Chapters 7 through 10 analyze market segments based on product type, process, and end-user, and geography, covering regions such as North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. These chapters include market revenue data, forecasts, and driving factors.

Chapter 11 presents a competitive analysis, featuring a heat map of key players within the market.

Chapter 12 offers an industry landscape analysis, detailing business activities such as market initiatives, recent developments, mergers, and joint ventures on a global scale, alongside a competitive overview.

In Chapter 13, comprehensive profiles of major companies operating in the market are provided. These profiles include key facts, business descriptions, product and service offerings, financial overviews, SWOT analyses, and significant developments.

Finally, Chapter 14, the appendix, includes a brief company overview, a list of abbreviations, and a disclaimer.

Long Steel Market News and Key Development:

Recent developments highlight capacity modernization, decarbonization efforts, and product alignment with construction and industrial demand.

In April 2026, In a landmark ceremony marking a new era of Indo-Japanese industrial collaboration, JSW Steel and Japan’s JFE Steel Corporation today officially unveiled the new corporate identity for their 50:50 Joint Venture (JV): JSW JFE Steel Limited. The entity encompasses the integrated steel operations at Sambalpur, Odisha.

In December 2025, JSW Vijayanagar Metallics Ltd. (JVML), a subsidiary of JSW Steel Ltd., one of India’s leading integrated steel producers, has commissioned a new 350-ton Ruhrstahl Heraeus (RH) unit from SMS group at Vijayanagar Works Steel Plant 4 in Toranagallu, India. This installation marks the world’s first operational combination of an RH Ladle Rocker with Fast Vessel Exchange (FvE), representing a major advancement in secondary metallurgy and plant efficiency.

Key Sources Referred:

World Bank: Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Long Steel Market

China Baowu Steel Group Corp., Ltd.

ArcelorMittal S.A.

HBIS Group Co., Ltd.

Nippon Steel Corporation

POSCO Holdings Inc.

JFE Steel Corporation

Tata Steel Limited

Ansteel Group Corporation Limited

Zhejiang Shagang Co., Ltd.

Gerdau S.A.

Frequently Asked Questions

How big is the Long Steel Market?

The Long Steel Market is valued at US$ 675.54 Billion in 2025, it is projected to reach US$ 917.44 Billion by 2033.

What is the CAGR for Long Steel Market by (2026 - 2033)?

As per our report Long Steel Market, the market size is valued at US$ 675.54 Billion in 2025, projecting it to reach US$ 917.44 Billion by 2033. This translates to a CAGR of approximately 3.9% during the forecast period.

What segments are covered in this report?

The Long Steel Market report typically cover these key segments-

Product Type (Rebar, Wire Rod, Merchant Bar, Rail)

Process (Basic Oxygen Furnace, Electric Arc Furnace)

What is the historic period, base year, and forecast period taken for Long Steel Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Long Steel Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Long Steel Market?

The Long Steel Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

China Baowu Steel Group Corp., Ltd.

ArcelorMittal S.A.

HBIS Group Co., Ltd.

Nippon Steel Corporation

POSCO Holdings Inc.

JFE Steel Corporation

Tata Steel Limited

Ansteel Group Corporation Limited

Zhejiang Shagang Co., Ltd.

Gerdau S.A.

Who should buy this report?

The Long Steel Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Long Steel Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Long Steel Market

Get Free Sample For Long Steel Market