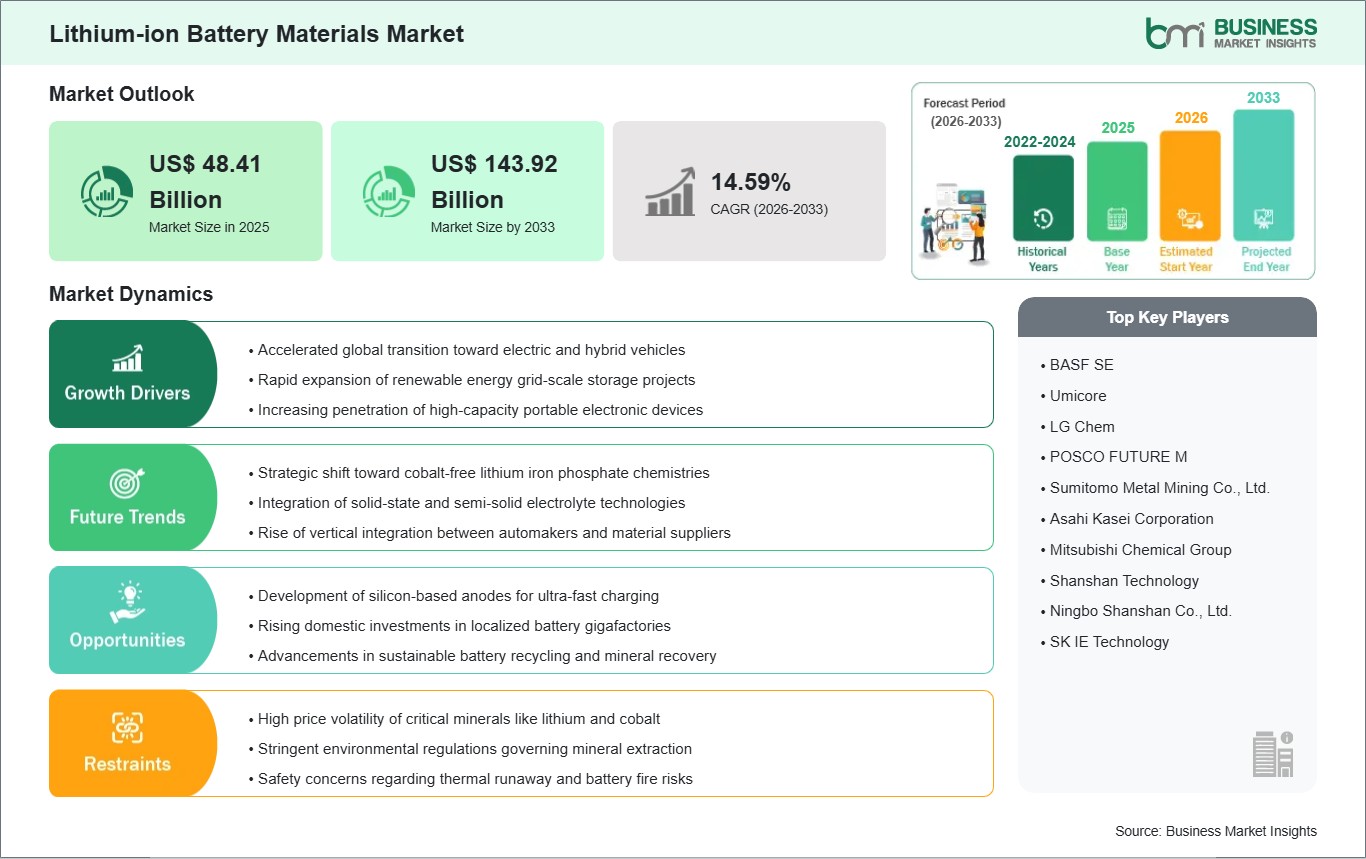

The Lithium-ion Battery Materials Market size is expected to reach US$ 143.92 Billion by 2033 from US$ 48.41 Billion in 2025. The market is estimated to record a CAGR of 14.59% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The global lithium-ion battery materials market is currently at the center of the world's energy and industrial transformation. It is growing rapidly due to a high demand for decarbonization and the electrification of transportation. The largest portion of the lithium-ion battery materials market is in cathode materials because the chemical composition of the cathode determines the overall performance of the battery. There is an ongoing transition in the materials market toward regionalized supply chains as countries look for ways to reduce dependence on international imports with domestic gigafactories, so there is significant competition and innovation from material scientists to develop chemistries that are more stable, efficient, and cost-effective.

Beyond the automotive sector, energy storage systems are providing a powerful secondary engine for growth. High-capacity lithium-ion batteries are essential in load balancing and grid stabilization as renewable energy accounts for a larger proportion of power supply. The market also faces issues over ethical sourcing of raw minerals and the impact of large-scale mining on the environment. To address this, the industry is investing heavily in recycling technologies that are able to recover metals from end-of-life batteries. The future for lithium-ion technology, in fact, is extremely bright.

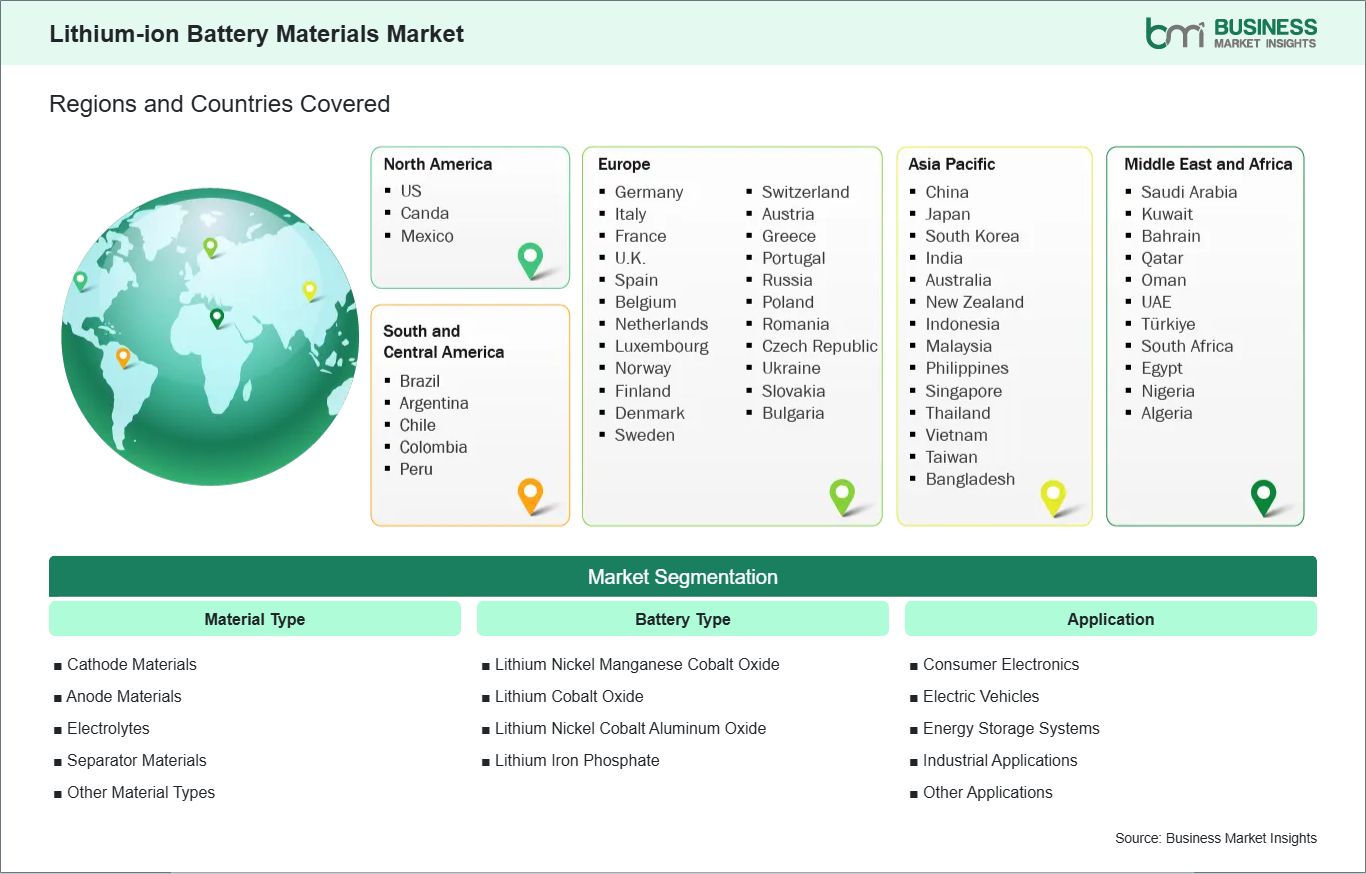

Key segments that contributed to the derivation of the Lithium-ion Battery Materials market analysis are material type, battery type, and application.

By material type, the lithium-ion battery materials market is segmented into Cathode Materials, Anode Materials, Electrolytes, Separator Materials, and Other Material Types. The Cathode Materials segment dominated the market in 2025.

By battery type, the lithium-ion battery materials market is segmented into Lithium Nickel Manganese Cobalt Oxide, Lithium Cobalt Oxide, Lithium Nickel Cobalt Aluminum Oxide, and Lithium Iron Phosphate. The Lithium Nickel Manganese Cobalt Oxide segment dominated the market in 2025.

By application, the lithium-ion battery materials market is segmented into Consumer Electronics, Electric Vehicles, Energy Storage Systems, Industrial Applications, and Other Applications. The Electric Vehicles segment dominated the market in 2025.

Lithium-ion Battery Materials Market Drivers and Opportunities:

Accelerated global transition toward electric and hybrid vehicles

The most significant factor that catalyzes the lithium-ion battery materials industry is the monumental shift that the global automotive industry is witnessing. The governments of all countries around the world have launched aggressive decarbonization strategies, and as a result, there is a need for a shift from internal combustion engines to electric propulsion. This shift has resulted in a monumental shift in the demand for chemical precursors, as automotive manufacturers need high-purity cathode and anode materials on a larger-than-ever scale. The need for long driving ranges has resulted in the need for high-nickel-based battery types, as this type of configuration results in a higher range than traditional types.

Furthermore, the automotive sector is no longer just a consumer but a primary driver of material innovation. To maintain a competitive edge, manufacturers are increasingly looking for materials that can withstand rigorous duty cycles and provide long-term durability. This has led to heavy investments in the research and development of specialized coatings and high-performance separators that enhance the stability of battery cells under extreme stress. As electric vehicle adoption reaches mass-market status, the sheer volume of material required to satisfy production targets continues to underpin the growth of the entire supply chain, from raw mineral processing to advanced chemical synthesis.

Integration of RFID and smart sensors into linerless label structures

The drive to attain faster rates of charge and energy capacity has led to the identification of the growth potential of silicon-based anodes in the market. The graphite-based anodes have already reached their theoretical capacity and are not capable of delivering the rapid energy transfer that is now expected in the market. The addition of silicon to the anode structure is expected to greatly improve the capacity of the battery, as it is capable of carrying far more lithium ions compared to graphite. This is the technological leap that is required to deliver the next generation of premium electric vehicles and other high-end devices that do not come with a proportional physical size increase.

While the historical difficulty of silicon’s physical expansion has been well-documented in the course of charging cycles, recent breakthroughs in material science related to nano-structuring and binder materials make commercialization of the technology viable. This represents a tremendous opportunity for material suppliers to provide high-value carbon-silicon composites. As the technology moves out of the high-performance niche and into the mainstream, the material is expected to redefine the standard. This represents an opportunity for battery manufacturers to provide solutions that charge in a fraction of the time required today, eliminating range anxiety and providing a greatly enhanced user experience for billions of people worldwide.

Lithium-ion Battery Materials Market Size and Share Analysis:

The global Lithium-ion Battery Materials market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within material type, battery type, and application, highlighting their respective contributions to overall market performance.

By material type, the Cathode Materials subsegment dominated the market in 2025 due to its critical role in determining the energy density and safety of battery cells, while also representing the most expensive component in the overall cell bill of materials.

By battery type, the Lithium Nickel Manganese Cobalt Oxide subsegment dominated the market in 2025 because it provides a superior balance of high energy density, stability, and cost-effectiveness, making it the preferred choice for long-range electric vehicle platforms globally.

By application, the Electric Vehicles subsegment dominated the market in 2025 as major automotive manufacturers accelerated their transition to electrified fleets, requiring massive volumes of high-performance materials to meet strict carbon emission targets and rising consumer demand.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

BASF SE

Umicore

LG Chem

POSCO FUTURE M

Sumitomo Metal Mining Co., Ltd.

Asahi Kasei Corporation

Mitsubishi Chemical Group

Shanshan Technology

Ningbo Shanshan Co., Ltd.

SK IE Technology

Get more information on this report

Lithium-ion Battery Materials Market Report Coverage and Deliverables:

The "Lithium-ion Battery Materials Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Lithium-ion Battery Materials market size and forecast at the regional and country levels for segments covered under the scope

Lithium-ion Battery Materials market trends, as well as drivers, restraints, and opportunities

Lithium-ion Battery Materials market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Lithium-ion Battery Materials market

Detailed company profiles, including SWOT analysis

The geographical scope of the Lithium-ion Battery Materials market report is divided into: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America has managed to carve its niche in the lithium-ion battery materials market, driven largely by the massive industrial incentives available in the region and the strategic bid to achieve energy independence. The US has put in place robust federal policies that offer tax credits and grants to the domestic production of materials and components related to the manufacturing of lithium-ion batteries. This has encouraged the establishment of both regional startups and global players, leading to the swift development of clusters of battery manufacturing facilities in the region. This has enabled the region to effectively address the risks of supply chain disruptions and the volatility of shipping costs.

The region’s leadership is also underpinned by the presence of a world-class research and development landscape that is at the vanguard of developing new-generation battery technologies. The major automotive groups in North America are aggressively pursuing vertical integration strategies with raw material suppliers to guarantee long-term access to critical raw materials. This guarantees that the region will continue to be at the vanguard of innovation in areas such as new-generation battery materials such as solid-state electrolytes and high-capacity silicon anodes. The strong demand for electric vehicle and energy storage products in the North American region also provides a high-value and stable market for the region’s producers.

Get more information on this report

Lithium-ion Battery Materials Market Research Report Guidance:

The report includes qualitative and quantitative data in the Lithium-ion Battery Materials market across material type, battery type, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Lithium-ion Battery Materials market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Lithium-ion Battery Materials market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Lithium-ion Battery Materials market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover the Lithium-ion Battery Materials market segments by material type, battery type, application, and geography across North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Lithium-ion Battery Materials market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Lithium-ion Battery Materials Market News and Key Development:

The Lithium-ion Battery Materials market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Lithium-ion Battery Materials market are:

In April 2025, Lyten, announced that it began U.S. production of battery-grade lithium-metal foils and alloys, marking a major step toward establishing a fully localized supply chain for next-generation battery materials.

In May 2025, Ascend Elements, announced that it received a government subsidy commitment of up to US$ 320 million to support construction of a lithium-ion battery materials plant in Poland, strengthening its European cathode materials production footprint.

In September 2024, Ascend Elements, announced the opening of a new lithium-ion battery recycling facility in Poland in collaboration with Elemental Strategic Metals, aimed at producing sustainable battery materials for EV supply chains.

Key Sources Referred:

American Chemistry Council (ACC)International Council of Chemical Associations (ICCA)European Chemical Industry Council (Cefic)China National Building Materials Group (CNBM)Indian Minerals & Granite Exporters Association (IMGEA)Japan Mining Industry Association (JMIA)Brazilian Mining Association (IBRAM)Gulf Petrochemicals and Chemicals Association (GPCA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Lithium-ion Battery Materials Market

BASF SE

Umicore

LG Chem

POSCO FUTURE M

Sumitomo Metal Mining Co., Ltd.

Asahi Kasei Corporation

Mitsubishi Chemical Group

Shanshan Technology

Ningbo Shanshan Co., Ltd.

SK IE Technology

About Author— Chemicals and Materials Research Team

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Show More

Frequently Asked Questions

How big is the Lithium-ion Battery Materials Market?

The Lithium-ion Battery Materials Market is valued at US$ 48.41 Billion in 2025, it is projected to reach US$ 143.92 Billion by 2033.

What is the CAGR for Lithium-ion Battery Materials Market by (2026 - 2033)?

As per our report Lithium-ion Battery Materials Market, the market size is valued at US$ 48.41 Billion in 2025, projecting it to reach US$ 143.92 Billion by 2033. This translates to a CAGR of approximately 14.59% during the forecast period.

What segments are covered in this report?

The Lithium-ion Battery Materials Market report typically cover these key segments-

Material Type (Cathode Materials, Anode Materials, Electrolytes, Separator Materials, Other Material Types)

Battery Type (Lithium Nickel Manganese Cobalt Oxide, Lithium Cobalt Oxide, Lithium Nickel Cobalt Aluminum Oxide, Lithium Iron Phosphate)

Application (Consumer Electronics, Electric Vehicles, Energy Storage Systems, Industrial Applications, Other Applications)

What is the historic period, base year, and forecast period taken for Lithium-ion Battery Materials Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Lithium-ion Battery Materials Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Lithium-ion Battery Materials Market?

The Lithium-ion Battery Materials Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

BASF SE

Umicore

LG Chem

POSCO FUTURE M

Sumitomo Metal Mining Co., Ltd.

Asahi Kasei Corporation

Mitsubishi Chemical Group

Shanshan Technology

Ningbo Shanshan Co., Ltd.

SK IE Technology

Who should buy this report?

The Lithium-ion Battery Materials Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Lithium-ion Battery Materials Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Lithium-ion Battery Materials Market

Get Free Sample For Lithium-ion Battery Materials Market