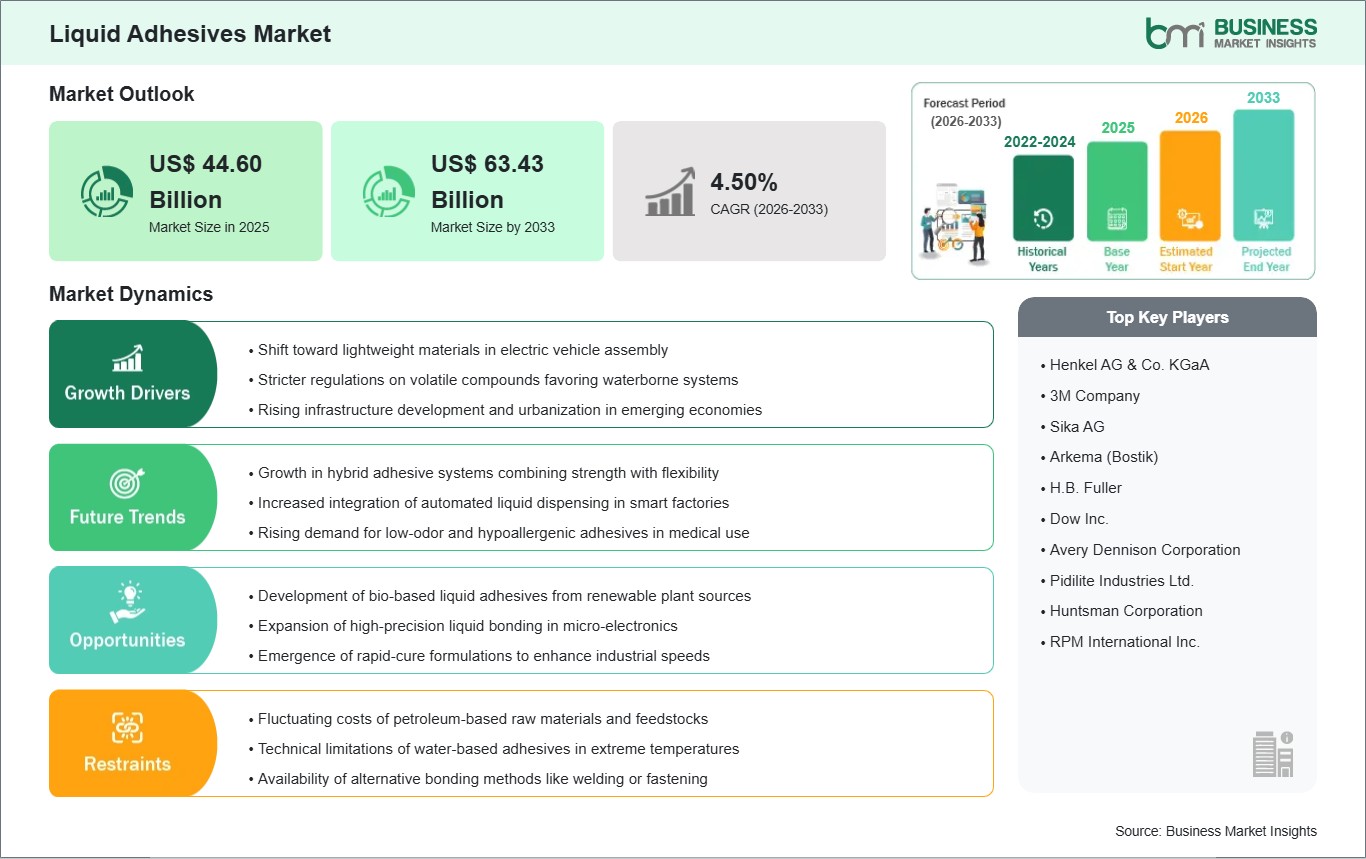

The Liquid Adhesives Market size is expected to reach US$ 63.43 Billion by 2033 from US$ 44.60 Billion in 2025. The market is estimated to record a CAGR of 4.50% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The liquid adhesive market is an essential part of the overall chemical market. The market is also considered one of the major facilitators in the development of modern manufacturing, construction, and packaging industries. Liquid adhesives are increasingly being preferred over other fastening materials such as mechanical fasteners, considering their ability to bond materials such as metal, plastic, and wood. The liquid adhesive market is in the process of undergoing a major shift in the overall formulation of products being offered in the market. The reason behind this is the overall crackdown by the government on volatile compounds and corporations' focus on sustainability.

Despite the challenges posed by volatile raw material pricing and the technical complexities of extreme-condition bonding, the market remains robust due to continuous innovation in polymer science. The rise of automation in factories has further integrated liquid adhesives into production lines, where high-speed, precision dispensing is essential. Emerging trends, such as the development of bio-based resins and the integration of smart functionalities into adhesive layers, are opening new growth avenues. As industries continue to seek materials that combine high performance with environmental responsibility, the liquid adhesives market is positioned to remain a cornerstone of industrial and consumer product development.

Liquid Adhesives Market - Strategic Insights:

Get more information on this report

Liquid Adhesives Market Segmentation Analysis:

Key segments that contributed to the derivation of the Liquid Adhesives market analysis are formulations, substrate, and end use industry.

By formulations, the liquid adhesives market is segmented into Water-based, Solvent-based, and Other Formulations. The Water-based segment dominated the market in 2025.

By substrate, the liquid adhesives market is segmented into Metal, Plastic, Glass, Wood, and Other Substrates. The Wood segment dominated the market in 2025.

By end use industry, the liquid adhesives market is segmented into Automotive & transportation, Construction, Electronics, Packaging, Healthcare, and Other End Use Industries. The Construction segment dominated the market in 2025.

Liquid Adhesives Market Drivers and Opportunities:

Shift toward lightweight materials in electric vehicle assembly

The automotive industry is undergoing a radical transformation as manufacturers prioritize vehicle range and efficiency, which directly correlates to weight reduction. Liquid adhesives are replacing traditional heavy bolts and welds because they allow for the seamless bonding of dissimilar materials such as aluminum, carbon fiber, and high-strength plastics. Unlike mechanical fasteners, liquid adhesives distribute stress evenly across the entire bonded surface, preventing material fatigue and enhancing the structural integrity of the vehicle chassis. This is particularly critical in battery pack assembly, where adhesives must provide not only structural strength but also thermal management and vibration damping to protect sensitive cells.

The transition to electric drivetrains has also changed the chemical requirements for these adhesives. There is a growing need for liquid formulations that offer electrical insulation alongside high mechanical robustness. Automakers are increasingly adopting liquid-applied sound deadeners and structural foams to improve cabin acoustics, which were previously masked by internal combustion engines. This fundamental change in vehicle architecture ensures that liquid adhesives are core components of the modern automotive assembly process. As global production of electric vehicles continues to rise, the volume of high-performance liquid adhesives required per vehicle is expected to increase significantly.

Development of bio-based liquid adhesives from renewable plant sources

The evolution of liquid adhesives derived from natural, renewable feedstocks such as soy, starch, and lignin represents a significant market shift. Traditionally, the adhesive industry has been heavily dependent on petrochemicals, making it vulnerable to oil price volatility and environmental criticism. Bio-based liquid adhesives address these concerns by offering a lower carbon footprint and reduced toxicity without sacrificing bonding performance. These green adhesives are gaining particular traction in the woodworking and indoor furniture sectors, where consumers and regulators are increasingly sensitive to formaldehyde emissions and indoor air quality.

Technological breakthroughs in cross-linking chemistry have allowed bio-based adhesives to match the moisture resistance and durability of synthetic resins. This allows them to move beyond simple paper and packaging applications into more demanding structural roles in the construction industry. As the supply chain for bio-derived monomers becomes more established, the cost competitiveness of these materials is improving. For chemical manufacturers, investing in bio-based technology is a strategic move to align with the global push for a circular economy and to differentiate their product portfolios in a highly competitive market that is increasingly scrutinized for its environmental impact.

Liquid Adhesives Market Size and Share Analysis:

The global Liquid Adhesives market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within formulations, substrate, and end use industry, highlighting their respective contributions to overall market performance.

By formulations, the Water-based subsegment dominated the market in 2025 due to its low environmental impact and minimal volatile organic compound emissions. These adhesives are the preferred choice for indoor applications and food-grade packaging where toxicity and odor must be strictly controlled to meet health and safety standards.

By substrate, the Wood subsegment dominated the market in 2025 because of the massive volume of liquid adhesives required in the global furniture and flooring industries. High-performance emulsions like polyvinyl acetate are fundamental for creating durable bonds in cabinetry, plywood manufacturing, and mass timber construction.

By end use industry, the Construction subsegment dominated the market in 2025 due to the global increase in infrastructure projects and residential building activities. Liquid adhesives are indispensable for flooring installations, roofing systems, and prefabricated wall panels, offering a faster and more uniform bonding method than traditional mechanical fasteners.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Henkel AG & Co. KGaA

3M Company

Sika AG

Arkema (Bostik)

H.B. Fuller

Dow Inc.

Avery Dennison Corporation

Pidilite Industries Ltd.

Huntsman Corporation

RPM International Inc.

Get more information on this report

Liquid Adhesives Market Report Coverage and Deliverables:

The "Liquid Adhesives Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Liquid Adhesives market size and forecast at the regional and country levels for segments covered under the scope

Liquid Adhesives market trends, as well as drivers, restraints, and opportunities

Liquid Adhesives market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Liquid Adhesives market

Detailed company profiles, including SWOT analysis

Liquid Adhesives Market Geographic Insights:

The geographical scope of the Liquid Adhesives market report is divided into: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America maintains a leading position in the liquid adhesives market, supported by a highly advanced manufacturing sector and a mature regulatory environment that fosters innovation. The region's dominance is particularly evident in the high-value specialty segments, such as aerospace and medical-grade adhesives, where North American companies lead in research and development. The United States has seen a significant boost in adhesive demand due to massive federal infrastructure investments and a resurgent automotive industry focused on electric vehicle production. Furthermore, the region's strict environmental standards have accelerated the transition to advanced water-based and solvent-free systems ahead of many other global regions.

The regional market also benefits from a well-integrated supply chain and the presence of world-leading chemical companies that provide a stable foundation for technological advancement. North American consumers have a high preference for DIY and home improvement products, sustaining a large retail market for liquid wood glues and construction adhesives. Additionally, the booming e-commerce sector in the region drives a continuous need for high-speed liquid packaging adhesives. While the Asia-Pacific region is a major volume producer, North America’s focus on high-performance, low-emission formulations and its advanced technological base provide it with a significant edge in terms of market value and industry leadership.

Get more information on this report

Liquid Adhesives Market Research Report Guidance:

The report includes qualitative and quantitative data in the Liquid Adhesives market across formulations, substrate, end use industry, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Liquid Adhesives market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Liquid Adhesives market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Liquid Adhesives market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover the Liquid Adhesives market segments by formulations, substrate, end use industry, and geography across North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Liquid Adhesives market. Companies have been profiled on the basis of their key facts, business descriptions, products, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Liquid Adhesives Market News and Key Development:

The Liquid Adhesives market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Liquid Adhesives market are:

In September 2023, Avery Dennison, announced the launch of its decorative linerless labeling solutions at Labelexpo Europe, expanding its linerless portfolio to support premium packaging and sustainability goals.

In 2024, Avery Dennison, highlighted continued expansion of its linerless labeling segment, focusing on innovation in adhesive technologies and sustainable labeling solutions to meet rising industry demand.

In 2025, HERMA, collaborated with logistics and packaging partners to deploy linerless labeling solutions aimed at reducing waste and improving efficiency in shipping and logistics operations.

Key Sources Referred:

American Chemistry Council (ACC)International Council of Chemical Associations (ICCA)European Chemical Industry Council (Cefic)China National Building Materials Group (CNBM)Indian Minerals & Granite Exporters Association (IMGEA)Japan Mining Industry Association (JMIA)Brazilian Mining Association (IBRAM)Gulf Petrochemicals and Chemicals Association (GPCA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Liquid Adhesives Market

Henkel AG & Co. KGaA

3M Company

Sika AG

Arkema (Bostik)

H.B. Fuller

Dow Inc.

Avery Dennison Corporation

Pidilite Industries Ltd.

Huntsman Corporation

RPM International Inc.

About Author— Chemicals and Materials Research Team

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Frequently Asked Questions

How big is the Liquid Adhesives Market?

The Liquid Adhesives Market is valued at US$ 44.60 Billion in 2025, it is projected to reach US$ 63.43 Billion by 2033.

What is the CAGR for Liquid Adhesives Market by (2026 - 2033)?

As per our report Liquid Adhesives Market, the market size is valued at US$ 44.60 Billion in 2025, projecting it to reach US$ 63.43 Billion by 2033. This translates to a CAGR of approximately 4.50% during the forecast period.

What segments are covered in this report?

The Liquid Adhesives Market report typically cover these key segments-

Formulations (Water-based, Solvent-based, Other Formulations)

Substrate (Metal, Plastic, Glass, Wood, Other Substrates)

End Use Industry (Automotive & transportation, Construction, Electronics, Packaging, Healthcare, Other End Use Industries)

What is the historic period, base year, and forecast period taken for Liquid Adhesives Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Liquid Adhesives Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Liquid Adhesives Market?

The Liquid Adhesives Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Henkel AG & Co. KGaA

3M Company

Sika AG

Arkema (Bostik)

H.B. Fuller

Dow Inc.

Avery Dennison Corporation

Pidilite Industries Ltd.

Huntsman Corporation

RPM International Inc.

Who should buy this report?

The Liquid Adhesives Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Liquid Adhesives Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Liquid Adhesives Market

Get Free Sample For Liquid Adhesives Market