01

Market Summery

Executive Summary and Global Market Analysis

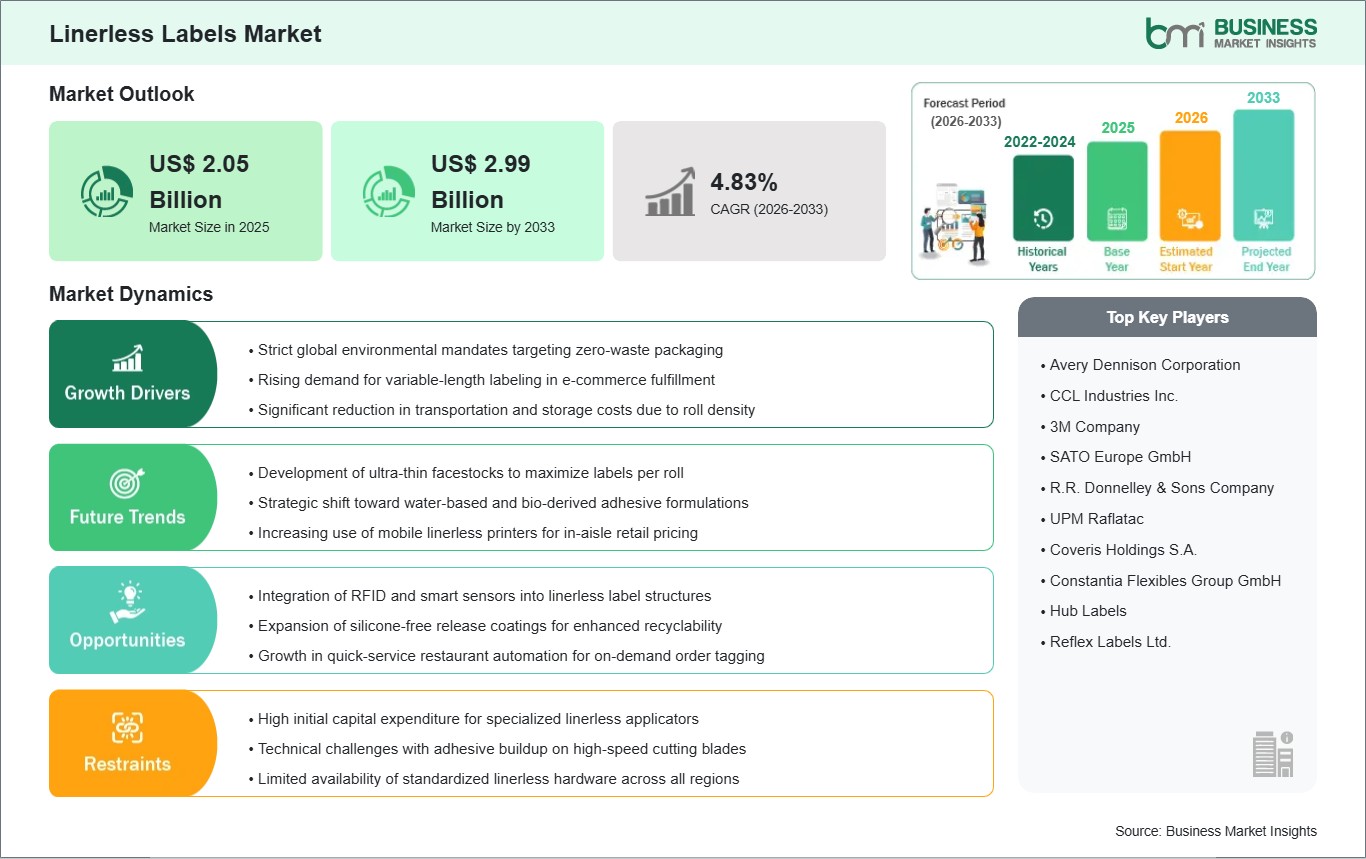

The linerless labels market is experiencing a period of rapid industrial adoption, fundamentally reshaped by the global convergence of sustainability goals and operational efficiency. By removing the release liner from the labeling equation, this market addresses one of the most persistent waste challenges in the packaging sector. The industry is currently led by the food and beverage and logistics sectors, which utilize the high-speed, variable-length printing capabilities of linerless systems to streamline complex supply chains. Direct thermal printing remains the cornerstone technology of the market, offering a ribbon-free, cost-effective method for generating labels that can be custom-cut to fit the specific data requirements of each package.

With advancements in adhesive chemistry and applicator hardware, the gap between industries that felt linerless systems were not possible for them has now been eliminated. There is a major industry trend towards the development of new high-performance silicone-free release coatings and bio-based adhesives that will increase the total recyclability of the package. Smaller companies have barriers to entry due to specialized equipment expenses, but the long-term cost savings in materials and the cost savings associated with less downtime from roll changes will yield a substantial ROI for them. The linerless labeling market is forecasted to lead the future of functional packaging because of the evolution of e-commerce, requiring faster, greener, and more flexible labeling applications.

03

Segment Analysis

Linerless Labels Market Segmentation

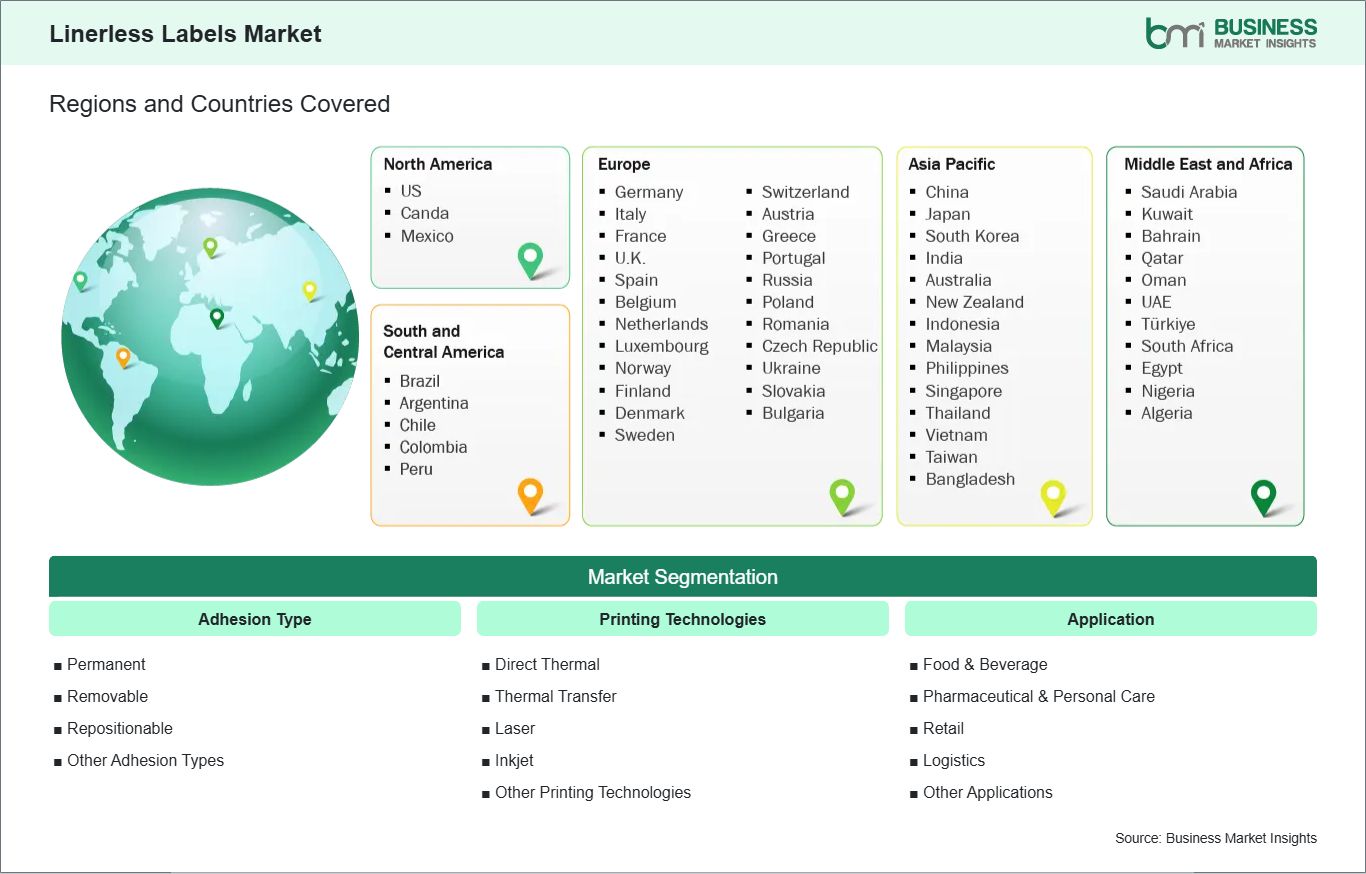

Key segments that contributed to the derivation of the Linerless Labels market analysis are adhesion type, printing technologies, and application.

- By adhesion type, the linerless labels market is segmented into Permanent, Removable, Repositionable, and Other Adhesion Types. The Permanent segment dominated the market in 2025.

- By printing technologies, the linerless labels market is segmented into Direct Thermal, Thermal Transfer, Laser, Inkjet, and Other Printing Technologies. The Direct Thermal segment dominated the market in 2025.

- By application, the linerless labels market is segmented into Food & Beverage, Pharmaceutical & Personal Care, Retail, Logistics, and Other Applications. The Food & Beverage segment dominated the market in 2025.

04

Market Forces

Linerless Labels Market Drivers and Opportunities

Strict global environmental mandates targeting zero-waste packaging

The global move towards a circular economy is one of the main drivers in the linerless labels market. One of the biggest issues facing companies that currently use traditional pressure-sensitive labels is that they generate a large amount of waste in the form of silicone-coated liner waste. This is one of the most non-recyclable forms of waste, and it is generally sent to a landfill. Environmental regulations, especially in Europe and North America, are becoming more and more punitive for companies that generate non-recyclable waste. Linerless labels provide a direct answer to this issue, as it allows companies to claim a 100 percent reduction in liner waste. This is no longer a choice for large brands that have publicly pledged to sustainability, as it significantly reduces the overall carbon footprint of the packaging process.

Beyond waste reduction, the environmental benefits extend to the entire supply chain. Because linerless rolls do not contain a bulky backing layer, they can hold up to 40 percent more labels in the same diameter compared to standard rolls. This increased density means fewer deliveries are required, leading to lower fuel consumption and reduced carbon emissions during transit. The pressure to meet "Green Packaging" standards is encouraging the food and retail sectors to overhaul their labeling lines. As businesses face carbon taxes and stricter disposal laws, the inherent eco-friendly profile of linerless systems provides a long-term strategic advantage that justifies the initial shift away from conventional linered formats.

Integration of RFID and smart sensors into linerless label structures

A major opportunity in the market is the integration of Radio Frequency Identification (RFID) and smart technologies within linerless label formats. As global retailers move toward mandatory RFID tagging for inventory accuracy and loss prevention, there is a growing need for labels that combine digital tracking with sustainable physical formats. Developing smart linerless labels involves embedding ultra-thin chips and antennas directly into the adhesive or facestock. This allows companies to enjoy the waste-reduction benefits of linerless technology while benefiting from the real-time data tracking capabilities of IoT. This hybrid approach is particularly valuable for high-value logistics and temperature-sensitive pharmaceutical shipments where traceability is paramount.

The technical challenge of protecting sensitive electronic components during the linerless printing and cutting process is a fertile ground for innovation. Manufacturers are developing specialized buffer zones and protective coatings that prevent damage to the RFID inlay when the printer cuts the label to size. This capability enables dynamic, on-demand smart labeling where the length of the label, and the data it contains, can be adjusted in real-time. As the cost of RFID components continues to fall, the adoption of intelligent linerless solutions is expected to move from niche pilot programs to mainstream industrial standards, offering a high-margin growth path for label converters and technology providers.

05

Size and Share Analysis

Linerless Labels Market Size and Share Analysis

The global Linerless Labels market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within adhesion type, printing technologies, and application, highlighting their respective contributions to overall market performance.

By adhesion type, the Permanent subsegment dominated the market in 2025 due to its critical necessity in long-term product identification and shipping. These adhesives ensure that labels remain securely attached to various substrates, including recycled corrugate and plastic films, throughout the entire supply chain and storage period.

By printing technologies, the Direct Thermal subsegment dominated the market in 2025 because it eliminates the need for ribbons, reducing both material waste and operational costs. This technology is perfectly suited for the variable-length printing capabilities of linerless systems, making it the standard for high-volume retail and logistics operations.

By application, the Food & Beverage subsegment dominated the market in 2025 due to the widespread adoption of wrap-around and top-and-side labeling for fresh produce and meat trays. The ability to increase label surface area for nutritional information while eliminating liner waste aligns with the industry's aggressive sustainability mandates.

07

Report Coverage

Linerless Labels Market Report Coverage and Deliverables

The "Linerless Labels Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

- Linerless Labels market size and forecast at the regional and country levels for segments covered under the scope

- Linerless Labels market trends, as well as drivers, restraints, and opportunities

- Linerless Labels market analysis covering key trends, regional framework, major players, regulations, and recent developments

- Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Linerless Labels market

- Detailed company profiles, including SWOT analysis

08

Geographic Insights

Linerless Labels Market Geographic Insights

The geographical scope of the Linerless Labels market report is divided into: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America holds the largest share of the linerless labels market, driven by an advanced retail infrastructure and early adoption of sustainable packaging technologies by multinational corporations. The United States, in particular, has seen a massive shift in the grocery and food service sectors, where linerless labels are used for weight-scale pricing and on-demand order tagging in quick-service restaurants. Major retail chains have integrated linerless systems into their logistics hubs to handle the immense volume of e-commerce parcels, benefiting from the reduced shipping weight and increased roll capacity. Furthermore, the region's stringent environmental regulations and corporate ESG commitments provide a robust framework that encourages the phase-out of traditional, waste-intensive labeling formats.

The dominance of North America is also supported by its role as a hub for technological innovation in the printing and adhesive sectors. Leading market players headquartered in the region are at the forefront of developing "smart" linerless solutions that integrate RFID and other digital identification technologies. The well-established supply chain for thermal paper and high-performance adhesives allows for competitive pricing and rapid deployment of new products. While the Asia-Pacific region is catching up through rapid industrialization and the growth of its own e-commerce giants, North America’s combination of high-value end-user demand and a mature regulatory environment ensures its continued leadership in market value and technological advancement.

10

Industry Activity

Recent Developments

The Linerless Labels market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Linerless Labels market are:

- In September 2025, Henkel, announced a strategic collaboration with Ravenwood Packaging to advance sustainable linerless labeling solutions, focusing on improving adhesive technologies and reducing packaging waste.

- In December 2025, DHL, announced the adoption of a linerless labeling solution developed in partnership with HERMA and cab at its Germany facility, aiming to reduce labeling waste by approximately 60%.

- In September 2023, Avery Dennison, announced the launch of its AD LinrSave decorative linerless labeling technology at Labelexpo Europe, targeting transformation of pressure-sensitive prime label applications.

11

Trust & Transparency

Research Methodology

The market analysis combines proprietary research with secondary data from government agencies, company disclosures, regulatory filings, industry databases and expert interviews. Market estimates are validated through data triangulation, cross-market benchmarking and analyst

review.

View Full Research Methodology

Key Sources Referred:

Tag & Label Manufacturers Institute (TLMI, USA)European Association for the Self-Adhesive Label IndustryLabel Manufacturers Association of India (LMAI)Japan Federation of Label Printing Industries (JFLPI)Australian Label & Tag Manufacturers Association (LATMA)Latin American Label AssociationChina Label Printing Association (CLPA)Company WebsitesCompany Annual ReportsCompany Investor Presentations