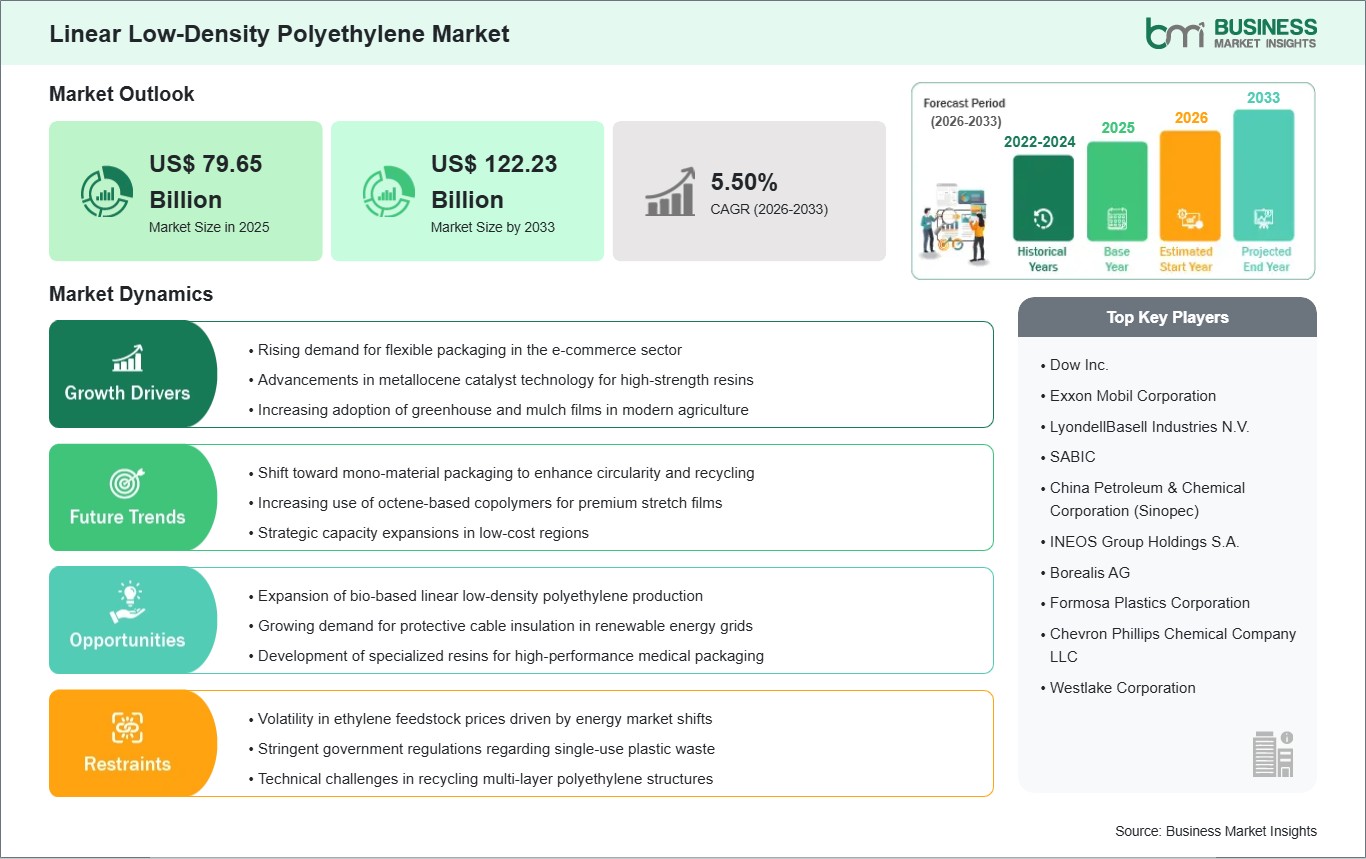

The Linear Low-Density Polyethylene Market size is expected to reach US$ 122.23 Billion by 2033 from US$ 79.65 Billion in 2025. The market is estimated to record a CAGR of 5.50% from 2026 to 2033.

Executive Summary and Global Market Analysis:

The linear low-density polyethylene market is currently dominated by its role in enabling international trade and food security. The material, being highly versatile in nature, acts as the backbone for the flexible packaging industry, which is expanding in response to urbanization and the growth of the e-commerce world. The linear low-density polyethylene market is dominated by gas-phase production processes, which have the scale and flexibility required to meet various industrial needs. Though films dominate the linear low-density polyethylene market, its unique balance of flexibility and resistance to environmental stress cracking has helped it penetrate the construction, automotive, and agricultural industries.

This has allowed for the development of high-performance resins that offer greater strength at reduced thicknesses, and it has been the primary driver in response to cost pressures and environmental sustainability concerns. Despite the challenges that the market has faced in the form of cost variability in feedstocks and increasing levels of regulatory pressure regarding waste, the market has remained buoyant due to the lack of alternatives that are capable of offering a similar price/performance equation. Moving forward, the market will likely continue to develop the recyclability of the structures that the resin takes, as well as the ability to utilize bio-based feedstocks, to ensure that linear low-density polyethylene continues to be a major player in the world of modern material science.

Linear Low-Density Polyethylene Market - Strategic Insights:

Get more information on this report

Linear Low-Density Polyethylene Market Segmentation Analysis:

Key segments that contributed to the derivation of the Linear Low-Density Polyethylene market analysis are process type and application.

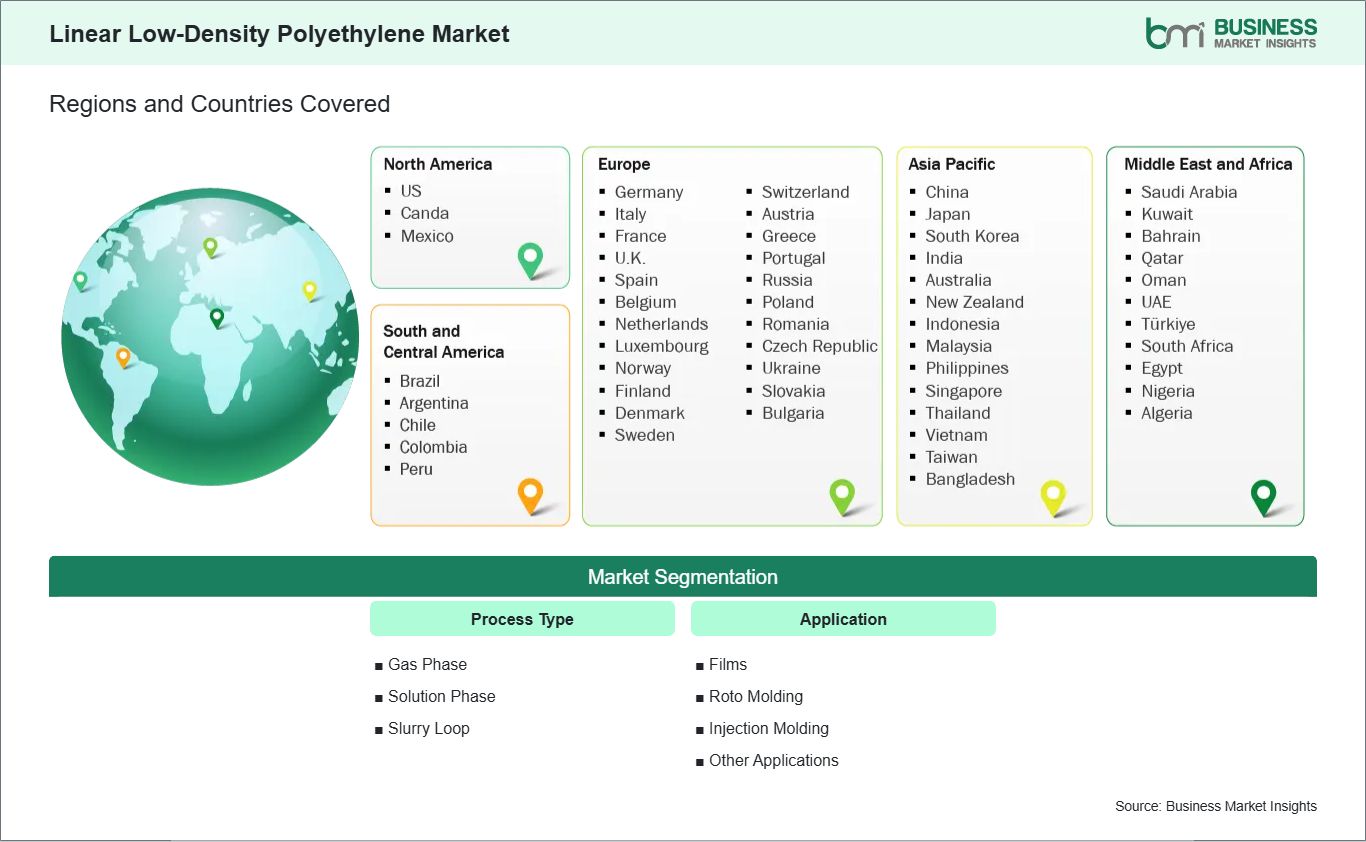

By process type, the linear low-density polyethylene market is segmented into Gas Phase, Solution Phase, and Slurry Loop. The Gas Phase segment dominated the market in 2025.

By application, the linear low-density polyethylene market is segmented into Films, Roto Molding, Injection Molding, and Other Applications. The Films segment dominated the market in 2025.

Linear Low-Density Polyethylene Market Drivers and Opportunities:

Rising demand for flexible packaging in the e-commerce sector

The recent rise in the popularity of online shopping worldwide has redefined the need for shipping services, making linear low-density polyethylene an essential packaging material. The packaging required for electronic commerce needs to be resistant to high mechanical stress during the entire shipping process. This material possesses the required puncture resistance and tear strength to ensure mailing bags, air pillows, or bubble wrap do not compromise the quality of the items during shipping. The capacity to make very thin yet strong films enables shipping companies to reduce the weight of the packaging, which directly results in reduced emissions and shipping costs.

Furthermore, the retail sector is increasingly moving away from rigid formats toward flexible pouches and stand-up bags. These formats rely on the excellent sealability and hot-tack properties of specialized resins to maintain package integrity and extend the shelf life of perishable goods. As consumer behavior continues to favor convenience and home delivery, the volume of protective and primary packaging required remains on a steep upward trajectory. This sustained demand is forcing manufacturers to innovate in film clarity and gloss, allowing brands to maintain premium aesthetic appeal while benefiting from the superior mechanical protection of advanced polyethylene grades.

Expansion of bio-based linear low-density polyethylene production

The shift toward a circular economy has created a massive opportunity for the integration of renewable feedstocks into the polyethylene supply chain. Bio-based resins, derived from resources such as sugar cane or used cooking oils, offer an identical molecular structure to their petroleum-based counterparts, allowing them to be processed on existing machinery without modification. This "drop-in" compatibility is highly attractive to multinational brand owners who have made public commitments to reduce their reliance on fossil fuels. By utilizing bio-derived monomers, companies can significantly lower the carbon footprint of their packaging while maintaining the high performance and recyclability that industrial users expect.

This opportunity is particularly relevant in the high-end consumer goods and organic food markets, where the packaging's environmental profile is a key part of the product's value proposition. As production technology for bio-ethylene matures, the economies of scale are beginning to improve, making these sustainable alternatives more accessible to a broader range of applications. Governments in several regions are also providing incentives or tax breaks for the use of renewable content, further accelerating the commercial viability of these resins. Investing in bio-based technology not only mitigates the risks associated with volatile crude oil prices but also positions producers as leaders in the transition toward a more sustainable and carbon-neutral chemical industry.

Linear Low-Density Polyethylene Market Size and Share Analysis:

The global Linear Low-Density Polyethylene market is experiencing steady growth, with market size and share analysis reflecting evolving treatment preferences and competitive dynamics among key players. The report evaluates important subsegments categorized within process type and application highlighting their respective contributions to overall market performance.

By process type, the Gas Phase subsegment dominated the market in 2025 due to its superior operational flexibility and cost-efficiency for large-scale production. This process allows for the creation of a wide range of molecular weight distributions, making it ideal for high-volume commodity resin manufacturing.

By application, the Films subsegment dominated the market in 2025 because of the massive global demand for flexible packaging and agricultural protection. The material’s high puncture resistance and tensile strength allow for significant downgauging, providing a more sustainable and cost-effective alternative to traditional thicker plastics.

Linear Low-Density Polyethylene Market Report Highlights:

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Dow Inc.

Exxon Mobil Corporation

LyondellBasell Industries N.V.

SABIC

China Petroleum & Chemical Corporation (Sinopec)

INEOS Group Holdings S.A.

Borealis AG

Formosa Plastics Corporation

Chevron Phillips Chemical Company LLC

Westlake Corporation

Get more information on this report

Linear Low-Density Polyethylene Market Report Coverage and Deliverables:

The "Linear Low-Density Polyethylene Market Size and Forecast (2022 - 2033)" report provides a detailed analysis of the market covering below areas:

Linear Low-Density Polyethylene market size and forecast at the regional and country levels for segments covered under the scope

Linear Low-Density Polyethylene market trends, as well as drivers, restraints, and opportunities

Linear Low-Density Polyethylene market analysis covering key trends, regional framework, major players, regulations, and recent developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Linear Low-Density Polyethylene market

Detailed company profiles, including SWOT analysis

Linear Low-Density Polyethylene Market Geographic Insights:

The geographical scope of the Linear Low-Density Polyethylene market report is divided into: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. North America held the largest share in 2025.

North America maintains a dominant position in the linear low-density polyethylene market, largely due to its significant cost advantage in raw material procurement. The region benefits from an abundance of low-cost ethane derived from shale gas, which provides a stable and inexpensive feedstock for ethylene production. This has led to massive capital investments in integrated petrochemical complexes along the Gulf Coast, making the United States a global hub for polyethylene manufacturing and export. The presence of a highly developed infrastructure and a mature plastics processing industry allows North American producers to maintain high operating rates and serve both domestic and international markets with high-performance resins.

The dominance of the region is further supported by the advanced state of its packaging and e-commerce sectors. North American consumers have a high per-capita consumption of packaged goods, and the region’s retail giants are at the forefront of adopting thin-gauge, high-strength films for load stability and protection. Additionally, the region is a leader in technological innovation, with major industry players headquartered here focusing on the development of specialized grades for medical and industrial applications. While the Asia-Pacific region is growing rapidly in terms of total volume, North America’s combination of feedstock security, technical expertise, and a high-value end-user base ensures its continued leadership in the global market landscape.

Get more information on this report

Linear Low-Density Polyethylene Market Research Report Guidance:

The report includes qualitative and quantitative data in the Linear Low-Density Polyethylene market across process type, application, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Linear Low-Density Polyethylene market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Linear Low-Density Polyethylene market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Linear Low-Density Polyethylene market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 9 cover the Linear Low-Density Polyethylene market segments by process type, application, and geography across North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 10 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 11 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 12 provides detailed profiles of the major companies operating in the Linear Low-Density Polyethylene market. Companies have been profiled on the basis of their key facts, business descriptions, process types, financial overview, SWOT analysis, and key developments.

Chapter 13, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Linear Low-Density Polyethylene Market News and Key Development:

The Linear Low-Density Polyethylene market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Linear Low-Density Polyethylene market are:

In March 2025, ExxonMobil, announced the start-up of a new linear low-density polyethylene (LLDPE) unit in Huizhou, China, aimed at strengthening supply of advanced metallocene polyethylene grades.

In mid-2025, Dow, announced the startup of a new 600,000 tons per year LLDPE and HDPE swing unit in Freeport, Texas, expanding its polyethylene production capacity in North America.

In May 2025, LyondellBasell Industries, announced the launch of Plexar PX3990, a high-performance LLDPE-based tie-layer resin designed for advanced flexible packaging applications.

Key Sources Referred:

American Chemistry Council (ACC)International Council of Chemical Associations (ICCA)European Chemical Industry Council (Cefic)China National Building Materials Group (CNBM)Indian Minerals & Granite Exporters Association (IMGEA)Japan Mining Industry Association (JMIA)Brazilian Mining Association (IBRAM)Gulf Petrochemicals and Chemicals Association (GPCA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Linear Low-Density Polyethylene Market

Dow Inc.

Exxon Mobil Corporation

LyondellBasell Industries N.V.

SABIC

China Petroleum & Chemical Corporation (Sinopec)

INEOS Group Holdings S.A.

Borealis AG

Formosa Plastics Corporation

Chevron Phillips Chemical Company LLC

Westlake Corporation

About Author— Chemicals and Materials Research Team

Suraj Sajeev is a market research and consulting professional with nearly 10 years of experience across Life Sciences, Consumer Goods, Food & Beverages, Materials & Chemicals, and Automotive industries. Throughout his career, he has successfully managed and delivered custom market research and consulting engagements, enabling clients to make informed strategic decisions through actionable market intelligence.

Suraj has extensive expertise in end-to-end project management, including proposal development, market assessment, competitive intelligence, opportunity analysis, market sizing and forecasting, strategic recommendation..

Frequently Asked Questions

How big is the Linear Low-Density Polyethylene Market?

The Linear Low-Density Polyethylene Market is valued at US$ 79.65 Billion in 2025, it is projected to reach US$ 122.23 Billion by 2033.

What is the CAGR for Linear Low-Density Polyethylene Market by (2026 - 2033)?

As per our report Linear Low-Density Polyethylene Market, the market size is valued at US$ 79.65 Billion in 2025, projecting it to reach US$ 122.23 Billion by 2033. This translates to a CAGR of approximately 5.50% during the forecast period.

What segments are covered in this report?

The Linear Low-Density Polyethylene Market report typically cover these key segments-

Process Type (Gas Phase, Solution Phase, Slurry Loop)

Application (Films, Roto Molding, Injection Molding, Other Applications)

What is the historic period, base year, and forecast period taken for Linear Low-Density Polyethylene Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Linear Low-Density Polyethylene Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Linear Low-Density Polyethylene Market?

The Linear Low-Density Polyethylene Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Dow Inc.

Exxon Mobil Corporation

LyondellBasell Industries N.V.

SABIC

China Petroleum & Chemical Corporation (Sinopec)

INEOS Group Holdings S.A.

Borealis AG

Formosa Plastics Corporation

Chevron Phillips Chemical Company LLC

Westlake Corporation

Who should buy this report?

The Linear Low-Density Polyethylene Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Linear Low-Density Polyethylene Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Linear Low-Density Polyethylene Market

Get Free Sample For Linear Low-Density Polyethylene Market