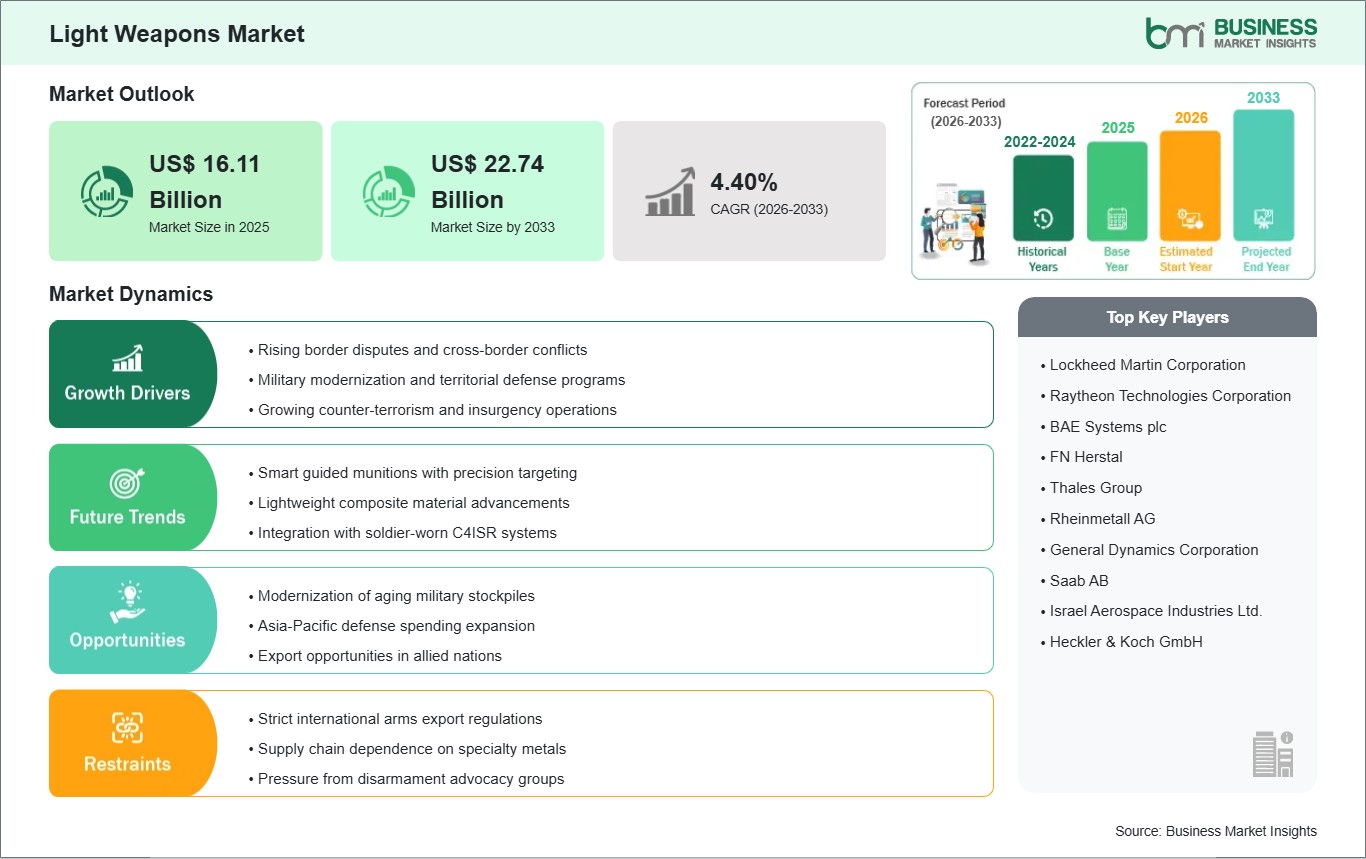

The Light Weapons market size is expected to reach US$ 22.74 billion by 2033 from US$ 16.11 billion in 2025. The market is estimated to record a CAGR of 4.40% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Light weapons comprise portable or crew-served combat systems designed for mobility, rapid deployment, and tactical flexibility across contested environments. This category includes heavy machine guns, grenade launchers, mortars, man-portable anti-tank systems, and man-portable air defense systems used by armed forces and security agencies. Their operational value lies in combining transportability with direct-fire or short-range support capabilities. Procurement priorities increasingly emphasize modularity, handling efficiency, and mission-specific effectiveness across conventional and asymmetric scenarios.

Demand momentum is closely linked to infantry modernization, border readiness requirements, and the need for responsive weapon systems in distributed operations. Defense establishments are refining force structures around portable firepower that can support maneuver units without heavy logistical burdens. Law enforcement agencies also assess selected platforms for specialized response roles where mobility, controlled engagement, and operational reliability matter. These conditions sustain procurement interest across both replacement cycles and capability expansion programs.

Segment distribution reflects different mission profiles within the market. Heavy machine guns and grenade launchers retain relevance in suppressive and support roles, while mortars continue to serve indirect-fire requirements with field adaptability. MANPATS and MANPADS address distinct battlefield threats by extending anti-armor and low-altitude air defense capability at the tactical edge. From an end-user perspective, military demand remains broader in scope, while law enforcement procurement tends to remain selective and role dependent.

Technology choices are shaping performance differentiation across the industry. Guided configurations are gaining strategic attention where strike accuracy, target discrimination, and engagement efficiency are prioritized. Unguided systems remain important in missions that require ruggedness, lower integration complexity, and established field use. This technology split is influencing product development, procurement planning, and upgrade pathways throughout the market.

The competitive environment is defined by long procurement cycles, compliance-intensive manufacturing, and sustained emphasis on platform reliability. Suppliers differentiate through system integration, portability improvements, and alignment with evolving operational doctrines. Market positioning also depends on the ability to support modernization programs with adaptable product portfolios and lifecycle service capabilities. As procurement agencies sharpen performance requirements, competitive intensity continues to center on mission fit rather than volume expansion alone.

Light Weapons Market - Strategic Insights:

Get more information on this report

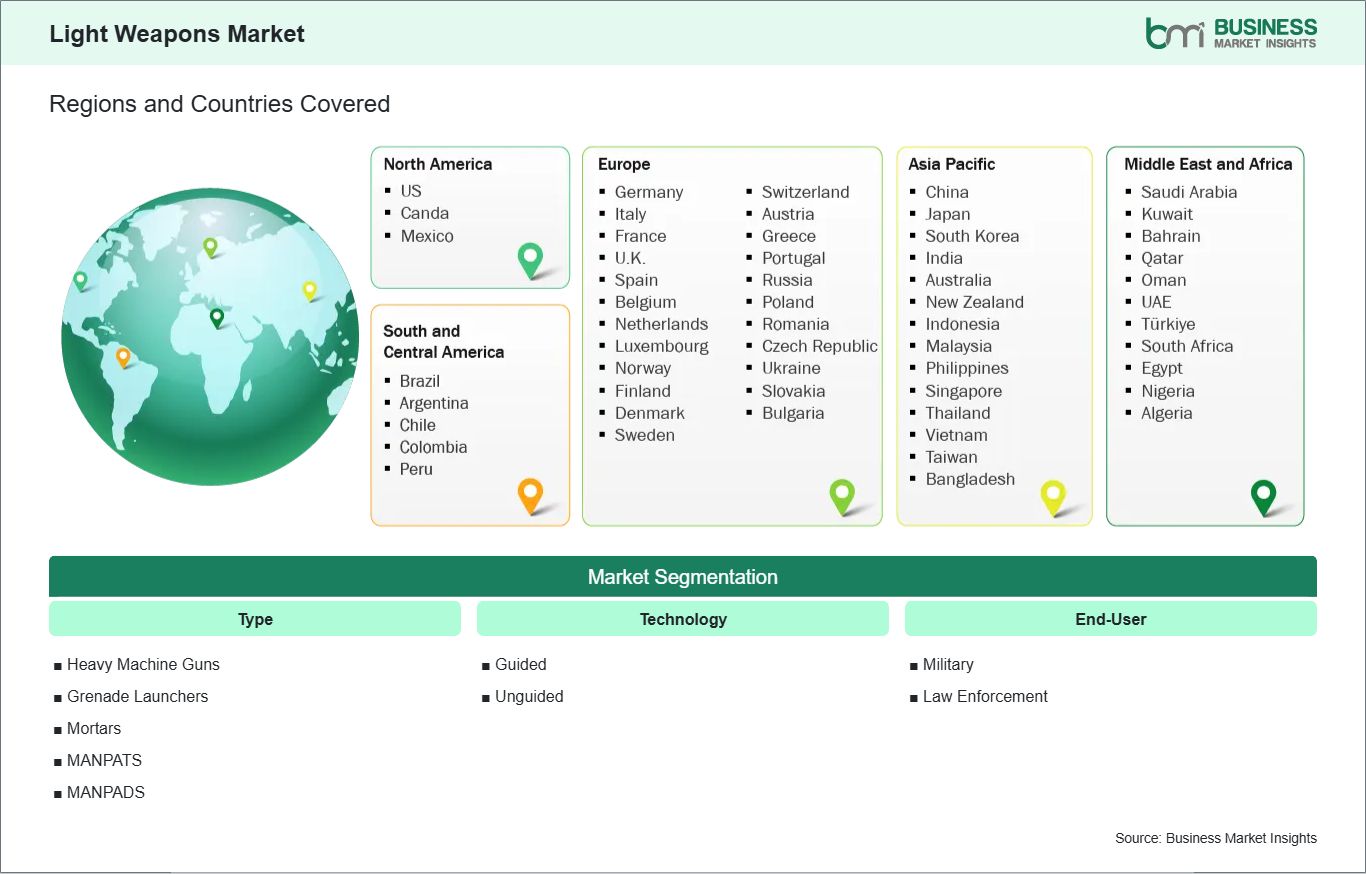

Light Weapons Market Segmentation Analysis:

The market is segmented by type, technology, and end-user, reflecting distinct tactical roles and procurement priorities.

By Type

Heavy Machine Guns: Sustained suppressive fire supports fixed defense and vehicle-mounted combat roles.

Mortars: Indirect fire capability enables rapid area coverage and adaptable field deployment.

MANPATS: Portable anti-armor systems strengthen frontline engagement against armored threats.

MANPADS: Short-range air defense extends protection against low-flying aerial targets.

By Technology

Guided: Precision engagement supports target discrimination and improved operational efficiency.

Unguided: Proven simplicity favors field durability and lower integration requirements.

By End-User

Military: Broad mission requirements sustain procurement across offensive and defensive weapon categories.

Law Enforcement: Specialized deployments emphasize controlled use, portability, and mission-specific readiness.

Light Weapons Market Drivers and Opportunities:

Infantry Modernization and Tactical Mobility Requirements

Force restructuring programs are increasing attention on mobile weapon systems that can strengthen squad-level lethality without imposing heavy support burdens. Military planners are prioritizing platforms that improve maneuver flexibility, rapid emplacement, and operational responsiveness across varied terrain. This requirement supports procurement of light weapons that align with dispersed formations, border security tasks, and tactical support missions where portability and field effectiveness remain central decision criteria.

The market impact extends beyond replacement demand because modernization programs often incorporate training compatibility, modular accessories, and evolving engagement doctrines. As armed forces refine readiness models, suppliers that address durability, handling, and mission adaptation gain stronger relevance. This context keeps the market commercially active, particularly where procurement agencies seek systems that can support both current operational needs and longer-term capability transitions.

Guided Weapon Integration and Precision Engagement Pathways

A clear opportunity is emerging through the integration of guidance technologies into portable and semi-portable weapon platforms. Procurement authorities are evaluating solutions that improve engagement accuracy, reduce ammunition inefficiency, and support use in complex operational settings. This trend is encouraging innovation in fire-control compatibility, seeker integration, and mission-oriented targeting support, creating a stronger value proposition for advanced systems across tactical applications.

Future scope is widening as defense organizations consider precision-enabled portfolios for border defense, infrastructure protection, and mobile combat support. Expansion potential is especially notable where procurement priorities shift toward controlled engagement and enhanced interoperability. For suppliers, this creates room to develop differentiated offerings that pair portability with upgraded targeting performance, reinforcing the market’s longer-term transition toward more technically sophisticated light weapon systems.

Light Weapons Market Size and Share Analysis:

The Light Weapons market size is expected to reach US$ 22.74 billion by 2033 from US$ 16.11 billion in 2025. The market is estimated to record a CAGR of 4.40% from 2026 to 2033. This trajectory indicates measured expansion shaped by modernization demand, replacement cycles, and procurement emphasis on mobile firepower across defense and security operations.

By type, heavy machine guns and grenade launchers maintain strong market relevance because they address recurring support and engagement requirements across diverse operational settings. Mortars remain important where indirect-fire flexibility is necessary, while MANPATS and MANPADS attract attention in procurement programs focused on tactical anti-armor and short-range air defense capability.

Military applications account for the leading share of demand due to broad deployment requirements, structured acquisition programs, and sustained battlefield readiness priorities. Law enforcement use remains more selective, centered on specialized operations that require portable systems with controlled deployment characteristics, operational dependability, and alignment with mission-specific response frameworks.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Lockheed Martin Corporation

Raytheon Technologies Corporation

BAE Systems plc

FN Herstal

Thales Group

Rheinmetall AG

General Dynamics Corporation

Saab AB

Israel Aerospace Industries Ltd.

Heckler & Koch GmbH

Get more information on this report

Light Weapons Market Report Coverage and Deliverables:

The "Light Weapons Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering the areas below:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Light Weapons Market Geographic Insights:

The Light Weapons market shows diverse regional adoption patterns influenced by defense posture shifts, tactical modernization priorities, procurement governance, and operational threat perceptions. Across the global landscape, acquisition strategies are increasingly shaped by the need for portable systems that can support flexible force deployment. Demand patterns vary according to military doctrine, domestic manufacturing depth, export regulations, and the extent to which security agencies prioritize mobile fire support and short-range protection capabilities.

North America retains a strong position due to mature defense procurement institutions, continuing capability refinement, and emphasis on infantry effectiveness across evolving mission profiles. Acquisition activity in this region often reflects a balance between modernization and interoperability, with attention directed toward reliable field performance and integration into broader combat systems. Law enforcement demand remains narrower, concentrated in specialized units and controlled operational scenarios rather than broad-based deployment.

Asia Pacific presents a dynamic growth environment as regional security considerations, border management priorities, and industrial upgrading efforts shape procurement planning. Several countries in the region are aligning acquisitions with mobility, responsiveness, and localized production capability. This creates a market setting where portable anti-armor systems, support weapons, and selective precision-enabled platforms gain traction as defense organizations seek adaptable solutions suited to varied terrain and rapidly changing tactical requirements.

Europe remains important through sustained rearmament discussions, stock renewal efforts, and doctrine adjustments linked to regional security planning. Emerging markets in the Middle East, Africa, and South and Central America show more selective procurement behavior, often shaped by budget discipline, operational urgency, and platform suitability. Together, these regions contribute to a geographically varied industry structure in which procurement timing and mission alignment matter as much as absolute demand volume.

Get more information on this report

Light Weapons Market Research Report Guidance:

The report encompasses both qualitative and quantitative data pertaining to the market, categorized by type, technology, and end-user, and geographical regions.

Beginning with Chapter 2, the report presents key takeaways that underscore the primary trends and market outlook.

Chapter 3 is dedicated to outlining the research methodology employed in this study.

In Chapter 4, an ecosystem analysis is provided.

Chapter 5 delves into the significant industry dynamics affecting the market, including driving factors, existing challenges, potential opportunities, and emerging trends. This section also includes an impact analysis of these drivers and constraints.

Chapter 6 reviews the market scenario, detailing historical revenue figures and forecasts extending to the year 2033.

Chapters 7 through 10 analyze market segments based on type, technology, and end-user, and geography, covering regions such as North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. These chapters include market revenue data, forecasts, and driving factors.

Chapter 11 presents a competitive analysis, featuring a heat map of key players within the market.

Chapter 12 offers an industry landscape analysis, detailing business activities such as market initiatives, recent developments, mergers, and joint ventures on a global scale, alongside a competitive overview.

In Chapter 13, comprehensive profiles of major companies operating in the market are provided. These profiles include key facts, business descriptions, product and service offerings, financial overviews, SWOT analyses, and significant developments.

Finally, Chapter 14, the appendix, includes a brief company overview, a list of abbreviations, and a disclaimer.

Light Weapons Market News and Key Development:

Recent developments highlight continued product advancement and procurement activity across portable and tactical weapon platforms.

In March 2026, AeroVironment, Inc., a global defense technology leader, announced the release of LOCUST X3, the third generation of AV’s high-energy laser weapon system that delivers precise, speed-of-light engagement for rapid defeat of unmanned aerial threats. LOCUST X3 builds on lessons learned from widely deployed systems to set a new standard in modular, AI-enabled drone defense—delivering unprecedented precision, scalability, and operational flexibility to defeat current and emerging aerial threats, including Group 1-3 unmanned aircraft systems and unmanned surface vehicles.

In March 2026, Moog Inc. (NYSE: MOG.A and MOG.B), a worldwide designer, manufacturer and systems integrator of high-performance precision motion and fluid controls and control systems, announced it has priced its offering of $500 million in aggregate principal amount of its 5.500% senior notes due 2034 (the “Notes”). Moog intends to use the net proceeds from the offering, together with cash on hand, to redeem all $500 million aggregate principal amount outstanding of its 4.250% Senior Notes due 2027 (the “2027 Notes”), including any accrued and unpaid interest thereon. This press release does not form part of or constitute a notice of redemption with respect to the 2027 Notes. The offering is expected to close on March 24th, 2026, subject to the satisfaction of customary closing conditions.

Key Sources Referred:

World Bank: Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Light Weapons Market

Lockheed Martin Corporation

Raytheon Technologies Corporation

BAE Systems plc

FN Herstal

Thales Group

Rheinmetall AG

General Dynamics Corporation

Saab AB

Israel Aerospace Industries Ltd.

Heckler & Koch GmbH

Frequently Asked Questions

How big is the Light Weapons Market?

The Light Weapons Market is valued at US$ 16.11 Billion in 2025, it is projected to reach US$ 22.74 Billion by 2033.

What is the CAGR for Light Weapons Market by (2026 - 2033)?

As per our report Light Weapons Market, the market size is valued at US$ 16.11 Billion in 2025, projecting it to reach US$ 22.74 Billion by 2033. This translates to a CAGR of approximately 4.40% during the forecast period.

What segments are covered in this report?

The Light Weapons Market report typically cover these key segments-

Type (Heavy Machine Guns, Grenade Launchers, Mortars, MANPATS, MANPADS)

Technology (Guided, Unguided)

End-User (Military, Law Enforcement)

What is the historic period, base year, and forecast period taken for Light Weapons Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Light Weapons Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Light Weapons Market?

The Light Weapons Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Lockheed Martin Corporation

Raytheon Technologies Corporation

BAE Systems plc

FN Herstal

Thales Group

Rheinmetall AG

General Dynamics Corporation

Saab AB

Israel Aerospace Industries Ltd.

Heckler & Koch GmbH

Who should buy this report?

The Light Weapons Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Light Weapons Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Light Weapons Market

Get Free Sample For Light Weapons Market