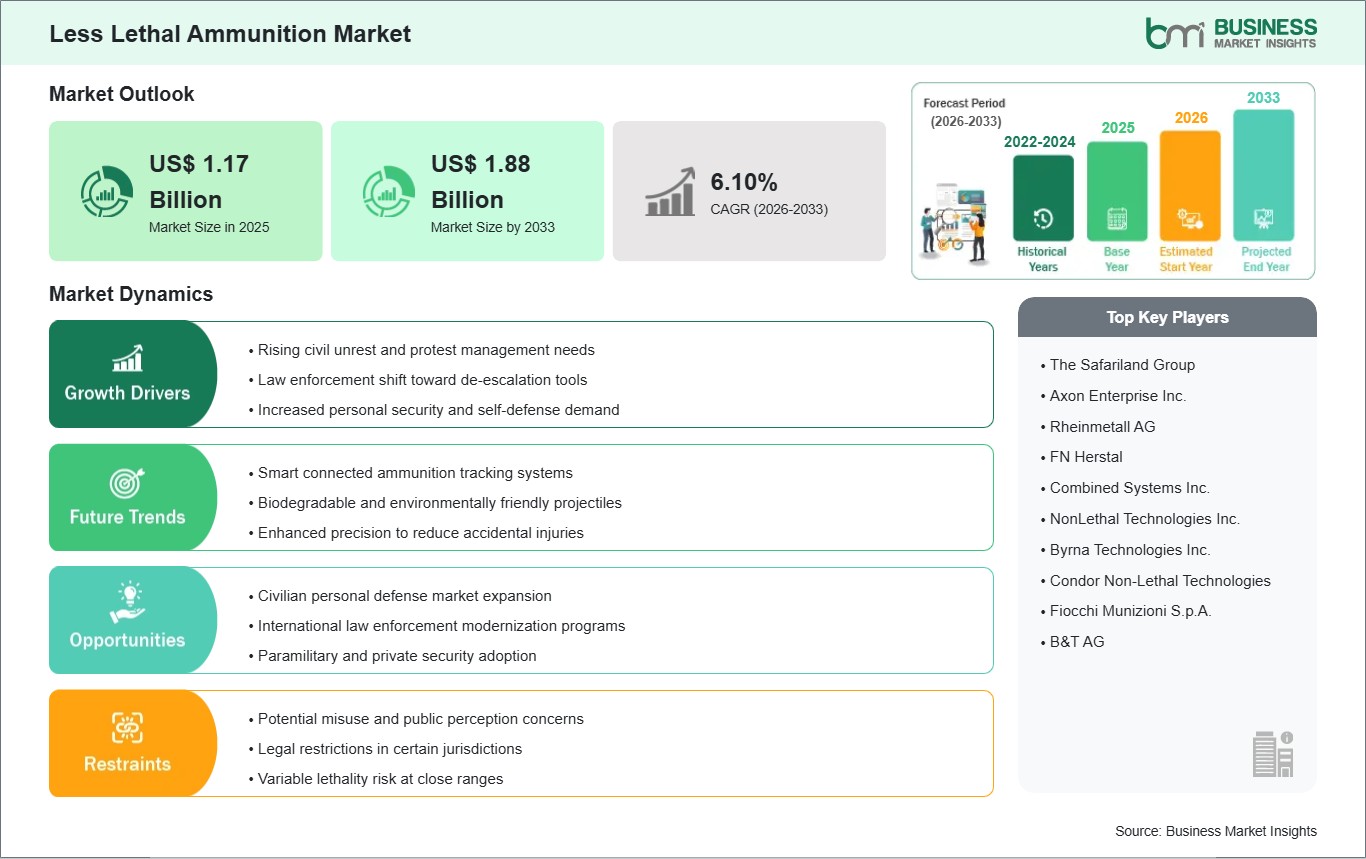

The Less Lethal Ammunition market size is expected to reach US$ 1.88 Billion by 2033 from US$ 1.17 Billion in 2025. The market is estimated to record a CAGR of 6.10% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Less lethal ammunition comprises specialized projectiles formulated to incapacitate, deter, or disperse targets while limiting fatal outcomes. These munitions include impact rounds and chemical payloads used when force calibration matters more than maximum terminal effect. Their role sits between verbal intervention and live ammunition, giving operators additional response options during crowd management, tactical containment, and controlled compliance scenarios.

Procurement momentum reflects policy emphasis on de-escalation, accountability, and selective force application across security environments. Agencies are aligning inventories with operating standards that prioritize stand-off capability, response flexibility, and lower injury exposure during volatile encounters. Civilian interest also contributes to sector depth in jurisdictions where nonlethal self-protection tools occupy a defined legal and practical niche.

Across segmentation, rubber bullets and pepper balls remain visible categories because they address distinct control requirements, while bean bag rounds and sponge grenades fit precision-oriented deployments. Kinetic impact systems retain broad operational relevance where measured physical interruption is required. Chemical irritants extend utility in dispersal settings, and electroshock technologies represent a narrower but technically differentiated path within this sector.

Product development is shifting toward tighter performance consistency, improved launcher compatibility, and better control of range effects. Engineering attention increasingly centers on dispersion accuracy, payload stability, and operational documentation to support training and review requirements. This evolution favors suppliers that can pair ammunition performance with structured deployment protocols rather than relying on product breadth alone.

Competitive conditions remain shaped by qualification standards, legal scrutiny, and platform interoperability. Suppliers differentiate through ammunition portfolios, agency support models, and the ability to serve law enforcement, military, and civilian demand without diluting product specificity. As end users refine doctrine around controlled engagement, the industry is moving toward performance credibility and deployment accountability as core decision factors.

Less Lethal Ammunition Market - Strategic Insights:

Get more information on this report

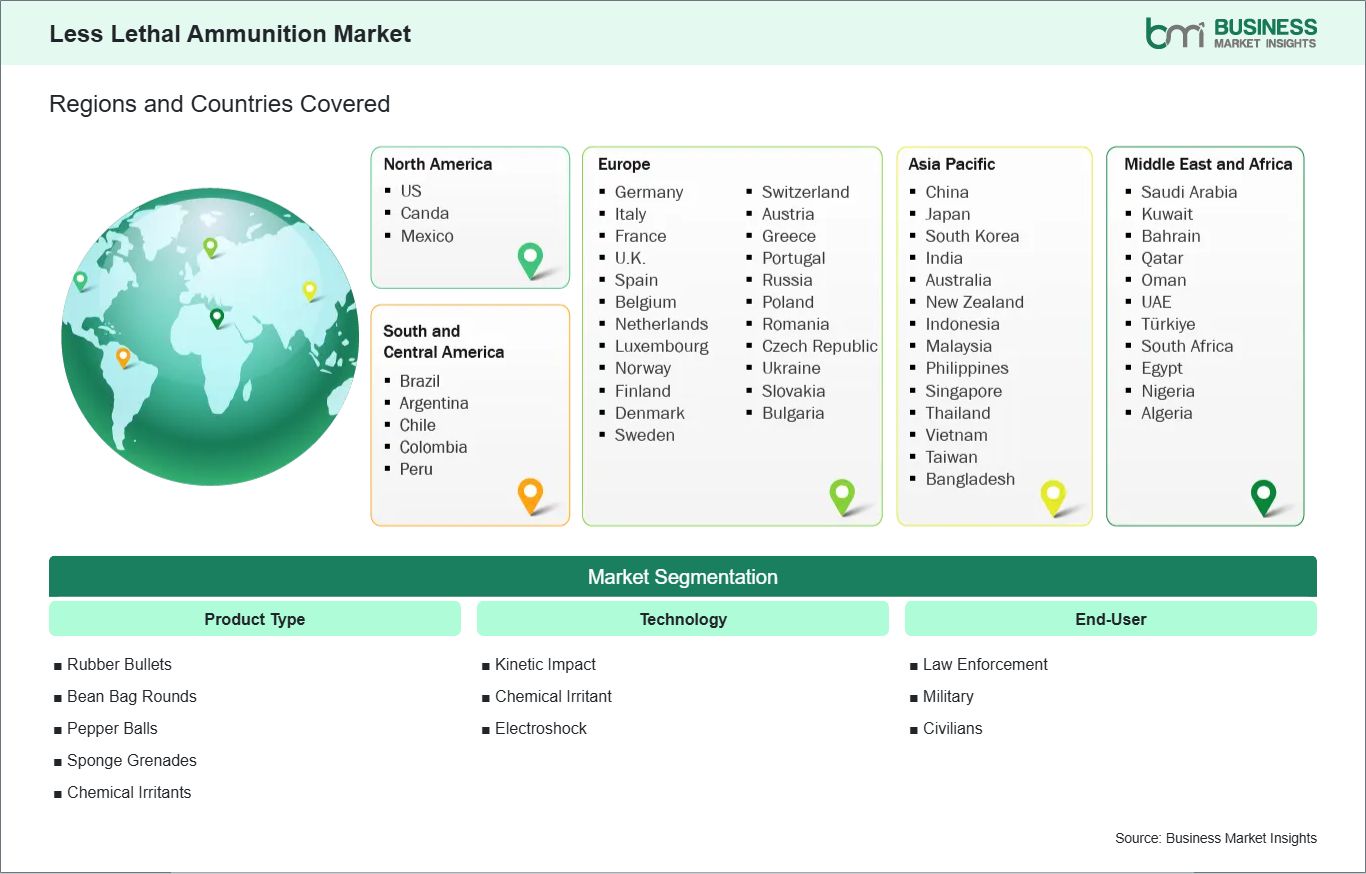

Less Lethal Ammunition Market Segmentation Analysis:

The market is segmented by product type, technology, and end-user to reflect deployment context and operational intent.

By Product Type

Rubber Bullets: Preferred for perimeter control where visible deterrence and impact response are required.

Bean Bag Rounds: Selected for close-range subject intervention with moderated kinetic transfer.

Pepper Balls: Enable area denial and targeted irritant delivery through launcher-based deployment.

Chemical Irritants: Serve dispersal operations through sensory disruption and tactical space control.

By Technology

Kinetic Impact: Maintains broad utility where measured physical incapacitation is operationally necessary.

Chemical Irritant: Supports distance-based crowd management with scalable dispersal effects.

Electroshock: Addresses controlled neuromuscular interruption in specialized enforcement scenarios.

By End-User

Law Enforcement: Accounts for sustained procurement tied to crowd control and apprehension protocols.

Military: Uses these munitions for escalation control in security and peace-support operations.

Civilians: Expands through personal protection products in regulated self-defense channels.

Less Lethal Ammunition Market Drivers and Opportunities:

Expansion of De-escalation-Centered Force Protocols

Security agencies are operating under tighter expectations around proportional response, public accountability, and documented force selection. That shift increases the need for munitions that create distance, preserve control, and reduce reliance on live ammunition during unstable encounters. Less lethal ammunition fits this requirement by expanding tactical choices across arrest operations, crowd dispersal, and perimeter enforcement where outcome management carries legal and operational weight.

Its market effect is visible in purchasing frameworks that emphasize deployment thresholds, injury mitigation, and compatibility with established launcher systems. This environment strengthens demand for certified rounds, structured training support, and consistent performance under field conditions. The driver remains highly relevant because procurement is no longer based only on inventory replacement, but on aligning equipment choices with revised engagement doctrine and post-incident review practices.

Innovation in Specialized Payloads and Civilian-Facing Platforms

Opportunity creation is increasingly linked to payload engineering, platform versatility, and scenario-specific ammunition design. Manufacturers are introducing rounds tailored for marking, sensor disruption, irritant dispersal, and controlled entry support, widening the practical use range beyond conventional riot response. At the same time, regulated civilian products are broadening the addressable base by translating professional operating concepts into personal protection formats with simpler deployment requirements.

Future scope extends through modular launcher ecosystems, more application-specific rounds, and stronger integration of training-led product adoption. Expansion can emerge in corrections, border security, private security, and civilian preparedness channels where escalation control remains a central concern. The opportunity matters because suppliers that combine innovation with usability and policy alignment can broaden market reach while improving acceptance across multiple end-user groups.

Less Lethal Ammunition Market Size and Share Analysis:

The Less Lethal Ammunition market size is expected to reach US$ 1.88 Billion by 2033 from US$ 1.17 Billion in 2025. The market is estimated to record a CAGR of 6.10% from 2026 to 2033. The projected expansion reflects sustained procurement across controlled-force applications, where end users seek tools that balance operational effectiveness with lower fatality risk. Market progression also indicates that product qualification, deployment standards, and training compatibility are becoming central to purchasing decisions.

By product and technology, kinetic impact categories hold a prominent position because they support direct intervention with predictable operational handling. Rubber bullets and bean bag rounds remain closely associated with established use cases, while pepper balls and chemical irritants broaden tactical utility in dispersal scenarios. Electroshock technologies occupy a more specialized position, shaped by platform specificity and deployment doctrine.

By application and end-user orientation, law enforcement represents the leading area of use due to routine requirements in crowd management, suspect control, and distance-based intervention. Military demand remains relevant where controlled escalation tools are required during security missions and peace-support activities. Civilian participation adds another layer of market breadth, particularly where self-defense products are positioned as alternatives to lethal personal protection methods.

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

The Safariland Group

Axon Enterprise Inc.

Rheinmetall AG

FN Herstal

Combined Systems Inc.

NonLethal Technologies Inc.

Byrna Technologies Inc.

Condor Non-Lethal Technologies

Fiocchi Munizioni S.p.A.

B&T AG

Get more information on this report

Less Lethal Ammunition Market Report Coverage and Deliverables:

The "Less Lethal Ammunition Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering the areas below:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Less Lethal Ammunition Market Geographic Insights:

The Less Lethal Ammunition market shows diverse regional adoption patterns influenced by policing frameworks, public-order requirements, procurement standards, and legal scrutiny surrounding force application. Across the global landscape, demand is shaped less by volume deployment and more by doctrine, accountability, and the ability of suppliers to meet qualification expectations. Markets with formalized escalation protocols typically create steadier pathways for category penetration and product standardization.

North America remains a mature arena for this sector because agencies place significant emphasis on approved equipment lists, training requirements, and operational documentation. Product selection often reflects a balance between field effectiveness and reviewability, which benefits suppliers offering established launcher ecosystems and differentiated ammunition types. Civilian self-defense channels also carry relevance in this region, adding a parallel route for market participation outside institutional procurement cycles.

Asia Pacific presents a different growth profile, supported by internal security modernization, expanding urban control requirements, and broader investment in tactical readiness. End users across the region are increasingly focused on versatile systems that can address both containment and dispersal scenarios without shifting to lethal force. As procurement processes evolve, suppliers able to provide adaptable ammunition formats and operational support are likely to gain stronger positioning in regional tenders.

Europe continues to reflect demand shaped by regulatory oversight, human-rights sensitivity, and measured public-order strategies, which encourages preference for controlled performance and documented use conditions. Emerging markets in the Middle East, Africa, and South and Central America are building adoption around security readiness, border control, and crowd-management capability, although procurement pacing varies by institutional capacity. Together, these regions broaden the industry footprint through differing but complementary use-of-force requirements.

Get more information on this report

Less Lethal Ammunition Market Research Report Guidance:

The report encompasses both qualitative and quantitative data pertaining to the market, categorized by product type, technology, and end-user, and geographical regions.

Beginning with Chapter 2, the report presents key takeaways that underscore the primary trends and market outlook.

Chapter 3 is dedicated to outlining the research methodology employed in this study.

In Chapter 4, an ecosystem analysis is provided.

Chapter 5 delves into the significant industry dynamics affecting the market, including driving factors, existing challenges, potential opportunities, and emerging trends. This section also includes an impact analysis of these drivers and constraints.

Chapter 6 reviews the market scenario, detailing historical revenue figures and forecasts extending to the year 2033.

Chapters 7 through 10 analyze market segments based on product type, technology, and end-user, and geography, covering regions such as North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. These chapters include market revenue data, forecasts, and driving factors.

Chapter 11 presents a competitive analysis, featuring a heat map of key players within the market.

Chapter 12 offers an industry landscape analysis, detailing business activities such as market initiatives, recent developments, mergers, and joint ventures on a global scale, alongside a competitive overview.

In Chapter 13, comprehensive profiles of major companies operating in the market are provided. These profiles include key facts, business descriptions, product and service offerings, financial overviews, SWOT analyses, and significant developments.

Finally, Chapter 14, the appendix, includes a brief company overview, a list of abbreviations, and a disclaimer.

Less Lethal Ammunition Market News and Key Development:

Recent developments indicate continued product innovation and procurement activity across the less lethal ammunition landscape.

In November 2025, Byrna Technologies Inc., a personal defense technology company specializing in the development, manufacture, and sale of innovative less-lethal personal security solutions, today announced that it is experiencing traction with houses of worship and schools as growing national attention shifts towards less-lethal protection options.

In April 2024, Cymat Technologies Ltd. announced its first commercial order for SmartMetal Stabilized Aluminum Foam (“SAF”) cylinders, to be used in non-lethal bullets, from their customer Nobel Sport. Nobel Sport is a French-based law enforcement specialty manufacturer of a wide range of ammunition and ancillary products for sport, law enforcement and military customers. This first order, destined for the French Armed Forces, is for 21,000 cylinders with a contract value of approximately $200,000.

Key Sources Referred:

Government procurement records and public safety equipment award noticesLaw enforcement policy documents and approved equipment listsCompany annual reports and investor materialsIndustry reports on nonlethal systems and tactical equipmentPeer-reviewed journals covering injury risk, policing, and public-order methodsAcademic studies on force escalation, crowd management, and compliance toolsRegulatory guidance and public-sector operational frameworks

The List of Companies - Less Lethal Ammunition Market

The Safariland Group

Axon Enterprise Inc.

Rheinmetall AG

FN Herstal

Combined Systems Inc.

NonLethal Technologies Inc.

Byrna Technologies Inc.

Condor Non-Lethal Technologies

Fiocchi Munizioni S.p.A.

B&T AG

Frequently Asked Questions

How big is the Less Lethal Ammunition Market?

The Less Lethal Ammunition Market is valued at US$ 1.17 Billion in 2025, it is projected to reach US$ 1.88 Billion by 2033.

What is the CAGR for Less Lethal Ammunition Market by (2026 - 2033)?

As per our report Less Lethal Ammunition Market, the market size is valued at US$ 1.17 Billion in 2025, projecting it to reach US$ 1.88 Billion by 2033. This translates to a CAGR of approximately 6.10% during the forecast period.

What segments are covered in this report?

The Less Lethal Ammunition Market report typically cover these key segments-

Product Type (Rubber Bullets, Bean Bag Rounds, Pepper Balls, Sponge Grenades, Chemical Irritants)

Technology (Kinetic Impact, Chemical Irritant, Electroshock)

End-User (Law Enforcement, Military, Civilians)

What is the historic period, base year, and forecast period taken for Less Lethal Ammunition Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Less Lethal Ammunition Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Less Lethal Ammunition Market?

The Less Lethal Ammunition Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

The Safariland Group

Axon Enterprise Inc.

Rheinmetall AG

FN Herstal

Combined Systems Inc.

NonLethal Technologies Inc.

Byrna Technologies Inc.

Condor Non-Lethal Technologies

Fiocchi Munizioni S.p.A.

B&T AG

Who should buy this report?

The Less Lethal Ammunition Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Less Lethal Ammunition Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Less Lethal Ammunition Market

Get Free Sample For Less Lethal Ammunition Market