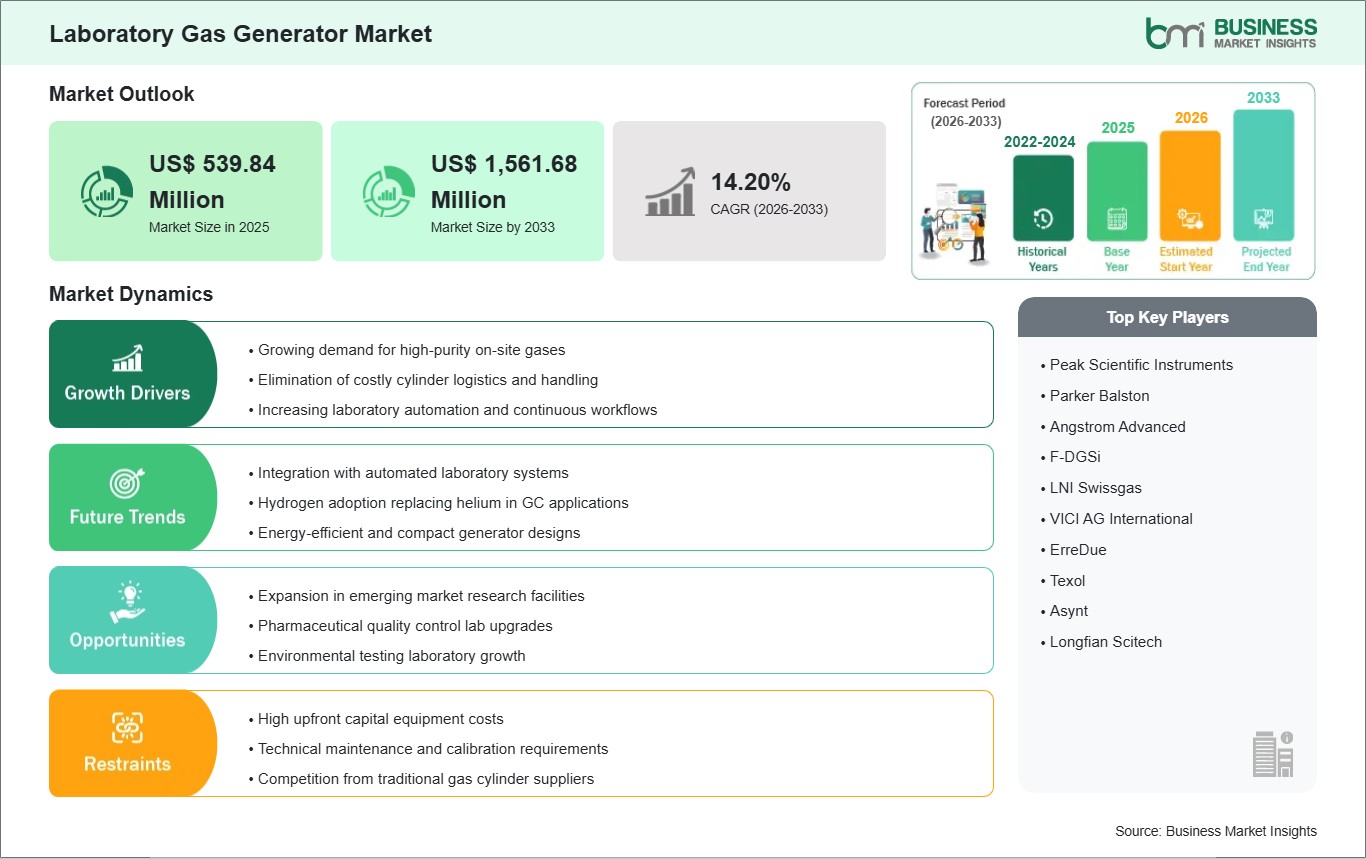

The Laboratory Gas Generator market size is expected to reach US$ 1,561.68 Million by 2033 from US$ 539.84 Million in 2025. The market is estimated to record a CAGR of 14.20% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Laboratory gas generators are compact systems that produce high-purity gases on site for analytical and research workflows. They convert compressed air or water into controlled outputs such as nitrogen, hydrogen, zero air, oxygen, and purge gas, supporting uninterrupted instrument operation without dependence on cylinder logistics. Their use has expanded as laboratories prioritize gas purity consistency, operator safety, and workflow continuity across regulated testing environments.

Adoption is advancing as laboratories seek cleaner gas delivery, lower handling risk, and improved uptime for critical analytical platforms. On-site generation reduces storage constraints, limits disruptions linked to cylinder replacement, and supports tighter control over purity and pressure stability. These advantages are especially relevant in pharmaceutical and biotech environments, where instrument reliability and traceable operating conditions directly affect productivity and compliance.

Segment patterns indicate broad demand across gas types and instrument formats. Nitrogen generators maintain wide relevance because they serve mass spectrometry and LC-MS systems requiring continuous, clean gas streams. Hydrogen units remain closely tied to gas chromatography workflows, while zero air and purge gas systems support detector performance and contamination control. End-user demand is anchored in pharmaceutical and biotech laboratories, followed by research institutions, clinical settings, and food testing operations.

Technology development is shifting the industry toward quieter, more efficient, and digitally monitored systems. Vendors are refining membrane, pressure regulation, and electrolysis designs to improve footprint, service intervals, and integration with modern analytical instruments. Product innovation increasingly emphasizes energy management, remote diagnostics, and application-specific tuning, allowing laboratories to align gas output more precisely with instrument sensitivity and throughput needs.

The competitive environment remains shaped by product reliability, installed base support, and the ability to address specialized laboratory requirements. Suppliers differentiate through application-matched platforms, service responsiveness, and lifecycle cost efficiency rather than broad commoditized offerings. As laboratories modernize infrastructure and pursue supply resilience, the market continues to favor manufacturers that combine gas purity assurance with operational simplicity.

Laboratory Gas Generator Market - Strategic Insights:

Get more information on this report

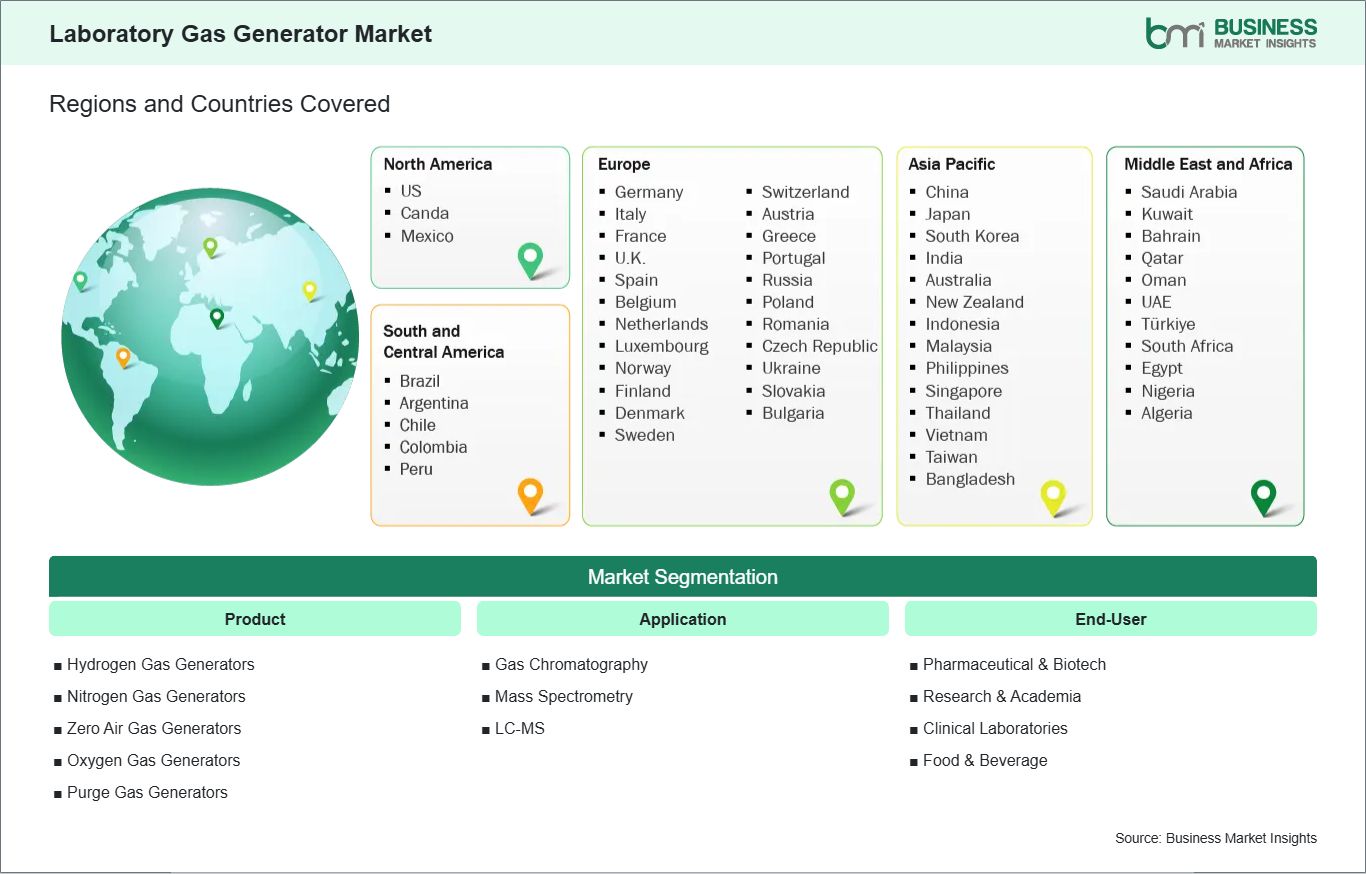

Laboratory Gas Generator Market Segmentation Analysis:

The market is segmented by product, application, and end-user, reflecting instrument-specific performance requirements and laboratory operating priorities.

By Product

Hydrogen Gas Generators: Preferred where stable carrier gas output supports chromatography continuity.

Nitrogen Gas Generators: Widely selected for LC-MS workflows requiring dependable purity control.

Zero Air Gas Generators: Used to maintain clean combustion air for detector performance.

Oxygen Gas Generators: Applied in specialized laboratory processes needing controlled oxygen supply.

Purge Gas Generators: Support contamination prevention in sensitive analytical instrument environments.

By Application

Gas Chromatography: Requires precise gas delivery for repeatable separation performance.

Mass Spectrometry: Benefits from clean, continuous gas streams for stable analytical output.

LC-MS: Relies on high-purity nitrogen for sustained instrument sensitivity and uptime.

By End-User

Pharmaceutical & Biotech: Prioritizes validated gas quality for research and production support.

Research & Academia: Uses flexible systems across diverse analytical and experimental setups.

Clinical Laboratories: Seeks reliable operation for routine testing and diagnostic workflows.

Food & Beverage: Deploys generators for quality assurance and contamination-sensitive analysis.

Laboratory Gas Generator Market Drivers and Opportunities:

Shift from Cylinder Supply to On-Site Gas Generation

Laboratories are moving away from cylinder-based supply because handling, storage, and replacement interrupt analytical continuity. This transition creates a clear need for systems that deliver gas on demand with controlled purity and pressure. On-site generators meet that requirement by simplifying operations, reducing dependence on external deliveries, and aligning gas availability with instrument runtime across chromatography and mass spectrometry environments.

The impact of this shift extends beyond convenience into laboratory safety, service efficiency, and infrastructure planning. Facilities can reduce operational interruptions while improving control over gas supply conditions. This relevance is strongest in regulated and high-throughput settings, where even minor supply inconsistency can affect instrument performance, scheduling discipline, and the quality of analytical output delivered to internal or external stakeholders.

Smarter and Application-Specific Generator Design

A clear opportunity is emerging through generator platforms designed around instrument-specific needs, digital monitoring, and lower energy use. Suppliers are introducing quieter systems, remote service capabilities, and tailored output configurations for LC-MS, gas chromatography, and detector support. This innovation strengthens the use case for replacement cycles in laboratories seeking better fit, easier maintenance, and improved alignment with modern analytical workflows.

Future scope extends into laboratory modernization programs, decentralized testing facilities, and expansion of analytical capacity across emerging research hubs. As users evaluate total operating efficiency more closely, demand can widen for systems that combine purity assurance with compact design and service visibility. This creates room for broader market expansion while reinforcing the role of laboratory gas generators as embedded infrastructure within precision testing environments.

Laboratory Gas Generator Market Size and Share Analysis:

The Laboratory Gas Generator market size is expected to reach US$ 1,561.68 Million by 2033 from US$ 539.84 Million in 2025. The market is estimated to record a CAGR of 14.20% from 2026 to 2033. This trajectory reflects stronger preference for on-site gas production, tighter expectations for instrument uptime, and broader integration of analytical platforms across research, testing, and regulated laboratory settings.

By product, nitrogen gas generators hold a leading position because they align closely with laboratories requiring consistent, high-purity supply for sensitive instrument platforms. Hydrogen gas generators retain strong relevance in chromatography-led workflows, while zero air units maintain importance where detector support is essential. Oxygen and purge gas generators occupy more specialized positions, yet they remain important in laboratories with defined process and contamination-control requirements.

By application, gas chromatography represents a central demand base due to its direct dependence on reliable carrier and support gas streams. LC-MS also accounts for substantial market relevance as laboratories require uninterrupted nitrogen delivery to preserve sensitivity and throughput. Mass spectrometry applications further reinforce adoption by prioritizing stable gas conditions that support reproducible analytical performance across complex testing environments.

Laboratory Gas Generator Market Report Highlights:

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Peak Scientific Instruments

Parker Balston

Angstrom Advanced

F-DGSi

LNI Swissgas

VICI AG International

ErreDue

Texol

Asynt

Longfian Scitech

Get more information on this report

Laboratory Gas Generator Market Report Coverage and Deliverables:

The "Laboratory Gas Generator Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering the areas below:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Laboratory Gas Generator Market Geographic Insights:

The Laboratory Gas Generator market shows diverse regional adoption patterns influenced by laboratory modernization priorities, analytical instrument density, and preferences for safer gas supply infrastructure. Across the global landscape, the industry reflects a steady movement toward on-site generation as laboratories seek continuity, cleaner operating conditions, and reduced dependence on delivered cylinders. Adoption intensity varies by installed instrument base, research activity, and the maturity of laboratory quality systems.

North America remains a key revenue center because pharmaceutical research, contract testing, and advanced analytical workflows are deeply established across the region. Laboratories in the United States and Canada place strong emphasis on uptime, safety, and standardized operating environments, which supports steady deployment of hydrogen, nitrogen, and zero air systems. The region also benefits from broad service access and a user base familiar with integrated gas management solutions.

Asia Pacific presents a dynamic expansion environment shaped by increasing laboratory capacity, rising pharmaceutical manufacturing activity, and broader investment in scientific research infrastructure. Countries such as China, Japan, South Korea, and India continue to strengthen analytical testing capabilities, which supports wider deployment of laboratory gas generators across regulated and academic settings. The region also favors compact and efficient systems suited to expanding instrument fleets and evolving laboratory footprints.

Europe maintains a solid position through established research institutions, environmental testing frameworks, and consistent attention to operational safety and quality assurance. Laboratories across the region often adopt generator systems to support cleaner workflows and tighter process control. Emerging markets in the Middle East and Africa and South and Central America are developing at a measured pace, supported by expanding diagnostic, food testing, and academic laboratory requirements that gradually strengthen demand for application-matched gas generation platforms.

Get more information on this report

Laboratory Gas Generator Market Research Report Guidance:

The report encompasses both qualitative and quantitative data pertaining to the market, categorized by product, application, and end-user, and geographical regions.

Beginning with Chapter 2, the report presents key takeaways that underscore the primary trends and market outlook.

Chapter 3 is dedicated to outlining the research methodology employed in this study.

In Chapter 4, an ecosystem analysis is provided.

Chapter 5 delves into the significant industry dynamics affecting the market, including driving factors, existing challenges, potential opportunities, and emerging trends. This section also includes an impact analysis of these drivers and constraints.

Chapter 6 reviews the market scenario, detailing historical revenue figures and forecasts extending to the year 2033.

Chapters 7 through 10 analyze market segments based on product, application, and end-user, and geography, covering regions such as North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. These chapters include market revenue data, forecasts, and driving factors.

Chapter 11 presents a competitive analysis, featuring a heat map of key players within the market.

Chapter 12 offers an industry landscape analysis, detailing business activities such as market initiatives, recent developments, mergers, and joint ventures on a global scale, alongside a competitive overview.

In Chapter 13, comprehensive profiles of major companies operating in the market are provided. These profiles include key facts, business descriptions, product and service offerings, financial overviews, SWOT analyses, and significant developments.

Finally, Chapter 14, the appendix, includes a brief company overview, a list of abbreviations, and a disclaimer.

Laboratory Gas Generator Market News and Key Development:

Recent developments reflect stronger emphasis on performance optimization, sustainability, and application-focused product refinement. The market also shows continued innovation in nitrogen and hydrogen generation for analytical laboratories.

In June 2026, PEAK Scientific, the leading manufacturer of laboratory gas generation solutions, announced the launch of Genius NEO, its most advanced generator to date. Engineered to push beyond the boundaries of what has previously been achieved by PEAK in terms of purity, sustainability and noise, Genius NEO represents a significant step forward for laboratories and instrument manufacturers who demand the very best for their gas generation equipment.

In June 2025, PEAK Scientific, the leading manufacturer of gas generation solutions, has launched their newest series of products for GC instruments, Intura, at ASMS 2025 in Baltimore, MD. The range of hydrogen, nitrogen and zero air generators are a premium, on-demand solution for labs who are looking to increase their productivity and quality of their analysis.

Key Sources Referred:

World Bank: Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Laboratory Gas Generator Market

Peak Scientific Instruments

Parker Balston

Angstrom Advanced

F-DGSi

LNI Swissgas

VICI AG International

ErreDue

Texol

Asynt

Longfian Scitech

Frequently Asked Questions

How big is the Laboratory Gas Generator Market?

The Laboratory Gas Generator Market is valued at US$ 539.84 Million in 2025, it is projected to reach US$ 1,561.68 Million by 2033.

What is the CAGR for Laboratory Gas Generator Market by (2026 - 2033)?

As per our report Laboratory Gas Generator Market, the market size is valued at US$ 539.84 Million in 2025, projecting it to reach US$ 1,561.68 Million by 2033. This translates to a CAGR of approximately 14.20% during the forecast period.

What segments are covered in this report?

The Laboratory Gas Generator Market report typically cover these key segments-

Product (Hydrogen Gas Generators, Nitrogen Gas Generators, Zero Air Gas Generators, Oxygen Gas Generators, Purge Gas Generators)

Application (Gas Chromatography, Mass Spectrometry, LC-MS)

What is the historic period, base year, and forecast period taken for Laboratory Gas Generator Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Laboratory Gas Generator Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Laboratory Gas Generator Market?

The Laboratory Gas Generator Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Peak Scientific Instruments

Parker Balston

Angstrom Advanced

F-DGSi

LNI Swissgas

VICI AG International

ErreDue

Texol

Asynt

Longfian Scitech

Who should buy this report?

The Laboratory Gas Generator Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Laboratory Gas Generator Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Laboratory Gas Generator Market

Get Free Sample For Laboratory Gas Generator Market