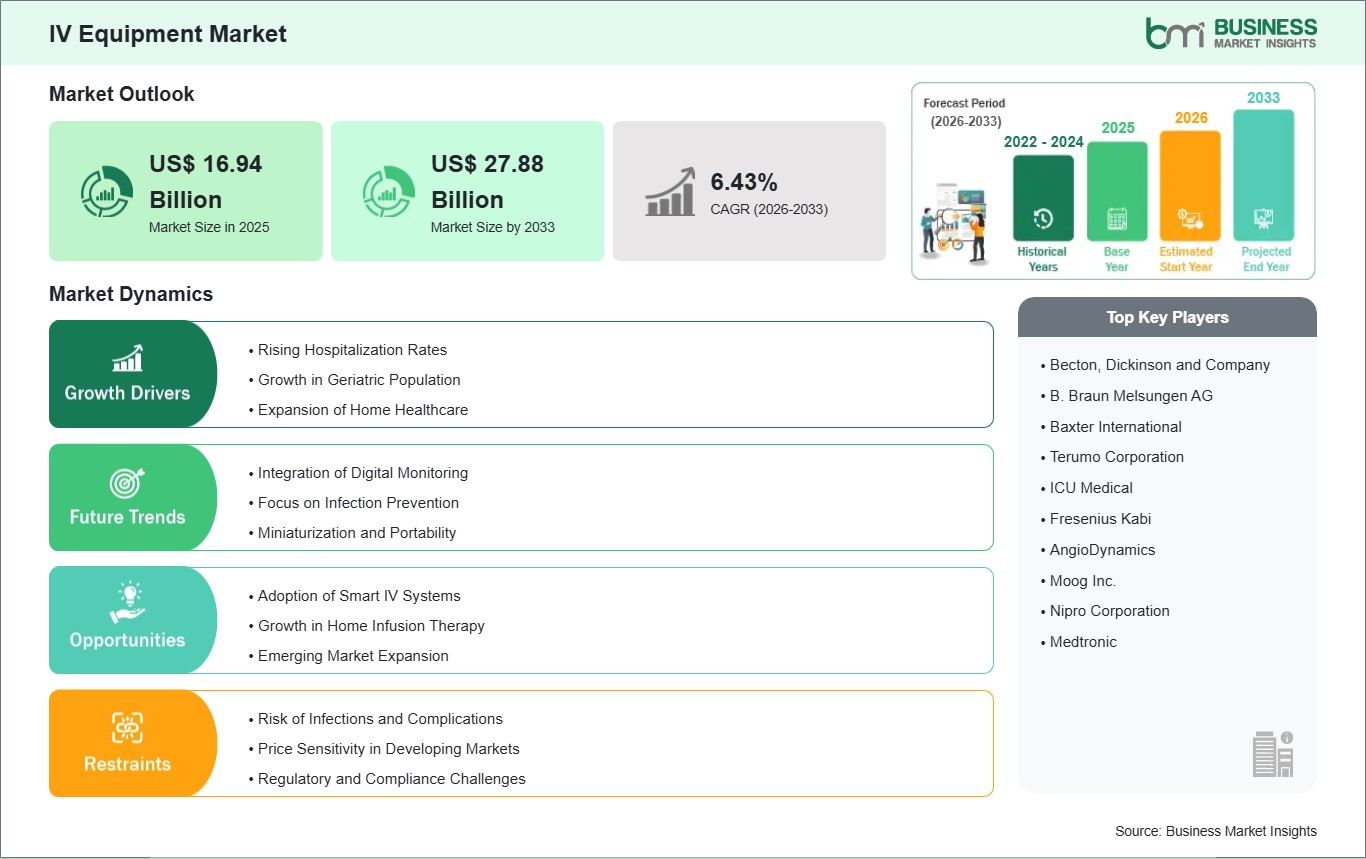

The IV Equipment Market size is expected to reach US$ 27.88 Billion by 2033 from US$ 16.94 Billion in 2025. The market is estimated to record a CAGR of 6.43% from 2026 to 2033.

Executive Summary and Global Market Analysis:

IV (Intravenous) equipment is basically medical equipment used for the infusion of fluids, medications, nutrients, and blood products directly into a patient's bloodstream, ensuring rapid and controlled therapy. This equipment generally includes IV catheters, infusion pumps, IV sets, cannulas, drip chambers, and their accessories.

The global IV equipment market is a very significant area of the medical devices industry, and this is because of the crucial role of intravenous therapy in acute care, surgery, chronic disease management, and emergency services. The steadily rising hospitalization rates, growth of the global geriatric population, and rising incidence of various types of chronic conditions, namely, cancer, diabetes, and cardiovascular diseases, leading to the need for prolonged infusion therapy, are further fueling this growth in the global market. Technological innovation, namely smart infusion pumps with dose error reduction systems and safety catheters, is further improving clinical efficiencies and safety, and this is expected to trigger further growth and adoption of this technology. As far as the analysis of the global market is concerned, North America currently leads this market due to its well-advanced medical infrastructure and significant per capita spending on healthcare, and this is followed closely by Europe due to its robust medical regulations and predominant hospital adoption. As far as growth is concerned, the current leader is expected to be the Asian Pacific Market, and this is due to its rapidly rising acceptance of medical care, backing of significant investments in medical infrastructure, and rising awareness of modern infusion therapies.

IV Equipment Market - Strategic Insights:

Get more information on this report

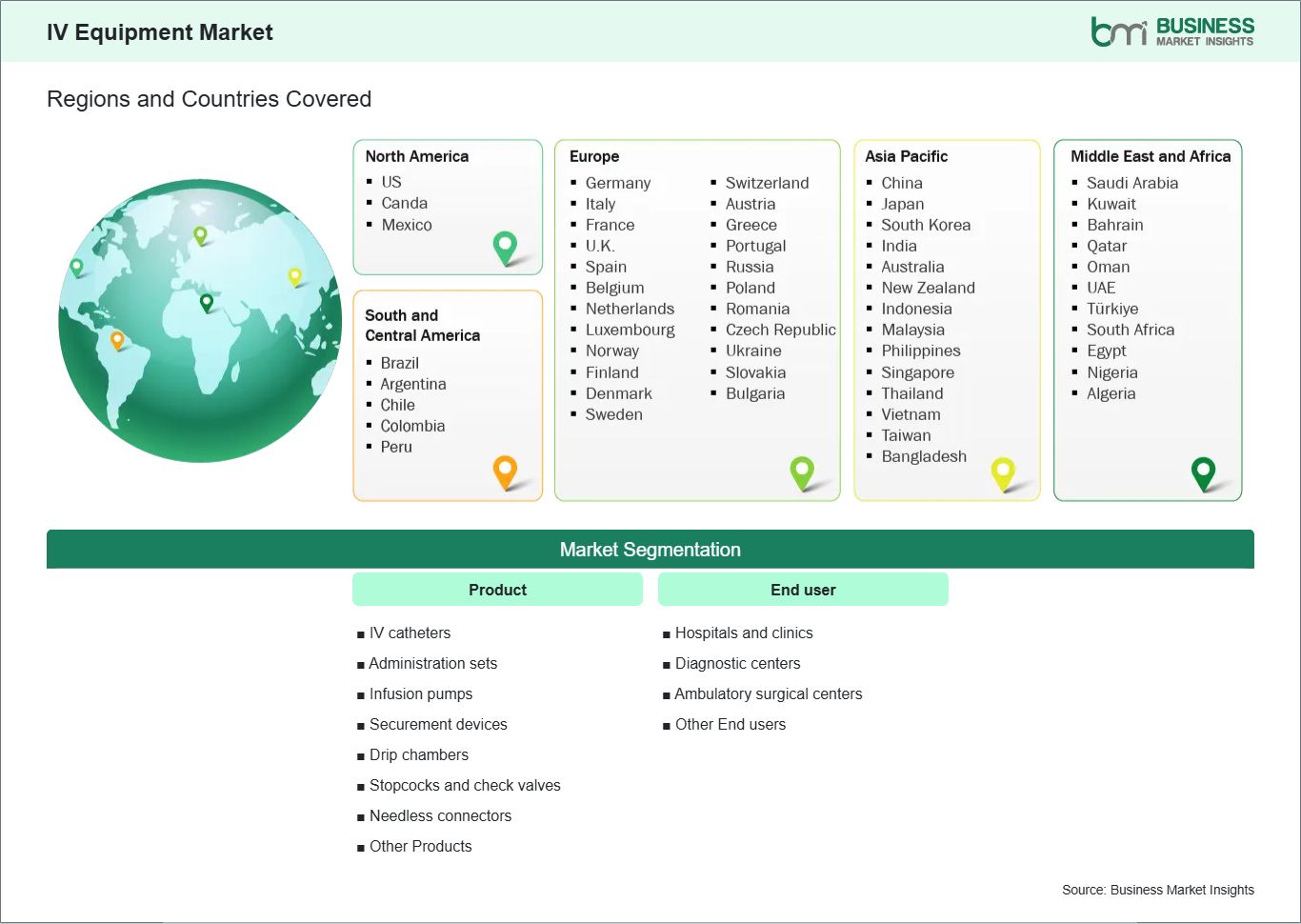

IV Equipment Market Segmentation Analysis:

Key segments that contributed to the derivation of the IV equipment market analysis are product and end user.

By product, the market is categorized into IV catheters, administration sets, infusion pumps, securement devices, drip chambers, stopcocks and check valves, needless connectors, other products. The IV catheters segment held the largest share of the market in 2024.

By end user, the IV equipment market is segmented into hospitals and clinics, diagnostic centers, ambulatory surgical centers, other end users. The hospitals and clinics segment dominated the market in 2024.

IV Equipment Market Drivers and Opportunities:

Increasing Prevalence of Chronic Diseases

Increasing burden of chronic diseases, significantly increases the demand for intravenous therapies relying on specialized equipment such as infusion pumps, IV catheters, and administration sets. Chronic diseases, including cardiovascular diseases, diabetes, and cancer, often require repeated or long-term fluid, medication, and nutritional infusions as part of a regimen of treatment protocols. Because intravenous therapy remains a mainstay of patient care globally, many industry analyses demonstrate that as the incidence of these non-communicative diseases increases, so too does healthcare utilization and the need for reliable IV delivery systems; for instance, it is demonstrated that 71% of global deaths are due to chronic diseases, indicating an ever-expanding population reliant on such therapies. Moreover, with an aging population, the prevalence of age-related chronic conditions further amplifies this effect, resulting in continued demand for IV equipment within both hospitals, clinics, and home healthcare settings. It is expected that new or enhanced IV technologies will fuel demand, hence underlining the leading role of chronic disease as a factor in market growth.

Rapid Expansion of Home-Based Healthcare Services and Smart Infusion Technologies

Home-based healthcare service and smart infusion technology activation is the result of changing the care delivery models and technology innovation. Portable and easy-to-use IV devices are becoming a necessity with hospitals in demand for smart infusion pumps that not only connect with the digital platforms but also with electronic health records (EHRs) and remote monitoring systems. For instance, almost half of the hospitals, i.e., 46%, are going for the adoption of smart infusion pumps worldwide; thus, these connected devices that are lowering medication errors and improving safety are becoming a trend more and more prevalent. To date, AI-powered smart pumps from the likes of B. Braun whose main feature is real-time monitoring and improved safety have been the latest technological rollouts; this is vividly showing how innovation is not only bringing about new product categories but also new revenue streams. Expansion of home infusion therapy options partnered with telehealth and remote patient management is resulting in higher usage of small IV systems outside hospitals. All these trends open a strong window for the makers to grow by innovating and developing sophisticated, connected IV equipment that is suited for home care and digital healthcare systems simultaneously.

IV Equipment Market Size and Share Analysis:

By product, the IV equipment market is categorized into IV catheters, administration sets, infusion pumps, securement devices, drip chambers, stopcocks and check valves, needless connectors, other products. The IV catheters segment held the largest share of the market in 2024. IV catheters dominance is driven by their universal use across almost all intravenous procedures, high procedural volumes, and frequent replacement needs due to single-use and short dwell times. IV catheters are essential in emergency care, surgeries, inpatient treatments, and outpatient therapies, giving them a consistently large market share. While infusion pumps contribute significant revenue due to higher unit costs and technological sophistication, and administration sets are widely used, IV catheters remain the most extensively utilized product globally.

By end user, the IV equipment market is segmented into hospitals and clinics, diagnostic centers, ambulatory surgical centers, other end users. The hospitals and clinics segment dominated the market in 2024. Hospitals and clinics segment accounts for the largest share due to high patient inflow, the wide range of medical procedures requiring IV therapy, and the availability of advanced healthcare infrastructure. Hospitals and clinics routinely use multiple types of IV equipment for surgeries, critical care, chronic disease management, and emergency services. Although ambulatory surgical centers are growing rapidly due to minimally invasive procedures and shorter hospital stays, they currently trail hospitals and clinics in overall market share.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Becton, Dickinson and Company

B. Braun Melsungen AG

Baxter International

Terumo Corporation

ICU Medical

Fresenius Kabi

AngioDynamics

Moog Inc.

Nipro Corporation

Medtronic

Get more information on this report

IV Equipment Market Report Coverage and Deliverables:

The " IV Equipment Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

IV equipment market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

IV equipment market trends, as well as market dynamics such as drivers, restraints, and key opportunities

IV equipment market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the IV equipment market

Detailed company profiles, including SWOT analysis

IV Equipment Market Geographic Insights:

The geographical scope of the IV equipment market report is divided into five regions: North America, Asia Pacific, Europe, Middle East & Africa, and South & Central America. The IV equipment market in Asia Pacific is expected to grow significantly during the forecast period.

The Asia-Pacific IV equipment market is segmented into China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh, and the Rest of Asia. The Asia-Pacific IV equipment market is experiencing robust growth, due to a number of connected factors based on the development of healthcare and demographic trends. One main reason for this is the healthcare infrastructure and investment in countries like China, India, Japan, and South Korea, which has led to a rise in hospital capacity and surgical volumes that require IV equipment like infusion pumps, catheters, and administration sets to a large extent. The governments of these countries are consistently providing support to healthcare in terms of access and quality, thus modernizing the facilities and leading to higher adoption of advanced IV technologies.

Another factor is the huge and increasing patient population suffering from chronic diseases like cancer, cardiovascular conditions, and diabetes who have become the mainstay of the IV therapy demand in both the inpatient and outpatient environments. The rising burden of patients with chronic diseases is proportionate to the increase in hospital admissions and thus the need for long-term IV treatment. Furthermore, the rapid pace of urbanization and the rising health consciousness among the people are aiding the utilization of IV therapy for three primary purposes: hydration, nutrition support, and drug delivery. The region's geriatric population has also contributed to the demand, as the elderlies usually need more frequent and complex medical care that involves intravenous interventions.

In combination with the increasing adoption of home healthcare and the demand for smart, portable infusion systems, these trends build a good environment for a strong IV equipment market growth in Asia-Pacific.

Get more information on this report

IV Equipment Market Research Report Guidance:

The report includes qualitative and quantitative data in the IV Equipment Market across product, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the IV equipment market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the IV equipment market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the IV equipment market scenario, in terms of historical market revenues, and forecast till the year 2031.

Chapters 7 to 9 cover IV Equipment Market segments by product, end user, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue forecast and factors driving the market.

Chapter 10 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 11 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 12 provides detailed profiles of the major companies operating in the IV equipment market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 13, i.e., the appendix is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

IV Equipment Market News and Key Development:

The IV equipment market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the IV equipment market are:

In July 2022, B. Braun Medical Inc. launched the Introcan Safety 2 IV catheter, which consists of a single-time blood control mechanism. The new IV catheter provides higher safety for medical personnel by reducing the risk of needle-stick injuries and limiting their contact with blood during the catheter insertion process.

In May 2023, Terumo revealed the establishment of an ultramodern production plant at its renowned Kofu Factory. The Medical Care Solutions company and its US$360 million investment made the next step in the sector.

Key Sources Referred:

World Health Organization (WHO)Centers for Disease Control and Prevention (CDC)Institute for Health Metrics and EvaluationOECD Health StatisticsOur World in DataCompany websitesCompany annual reportsCompany investor presentations

Krishna is a Market Research Analyst with over 4 years of experience across Life Sciences and Materials & Chemicals industries. He holds a Bachelor's degree in Pharmacy (B.Pharm.) and a Master's degree in Pharmaceutical Medicinal Chemistry (M.Pharm.). His expertise spans market intelligence, competitive benchmarking, market sizing and forecasting, primary and secondary research, and strategic consulting.

Krishna has successfully contributed to numerous syndicated and custom research engagements, delivering industry reports, market assessments, competitive analyses, and business proposals for clients across diverse sectors. With ..

Show More

Frequently Asked Questions

How big is the IV Equipment Market?

The IV Equipment Market is valued at US$ 16.94 Billion in 2025, it is projected to reach US$ 27.88 Billion by 2033.

What is the CAGR for IV Equipment Market by (2026 - 2033)?

As per our report IV Equipment Market, the market size is valued at US$ 16.94 Billion in 2025, projecting it to reach US$ 27.88 Billion by 2033. This translates to a CAGR of approximately 6.43% during the forecast period.

What segments are covered in this report?

The IV Equipment Market report typically cover these key segments-

Product (IV catheters, Administration sets, Infusion pumps, Securement devices, Drip chambers, Stopcocks and check valves, Needless connectors, Other Products)

End user (Hospitals and clinics, Diagnostic centers, Ambulatory surgical centers, Other End users)

What is the historic period, base year, and forecast period taken for IV Equipment Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the IV Equipment Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in IV Equipment Market?

The IV Equipment Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Becton, Dickinson and Company,

B. Braun Melsungen AG,

Baxter International,

Terumo Corporation,

ICU Medical,

Fresenius Kabi,

AngioDynamics,

Moog Inc.,

Nipro Corporation,

Medtronic

Who should buy this report?

The IV Equipment Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the IV Equipment Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For IV Equipment Market

Get Free Sample For IV Equipment Market