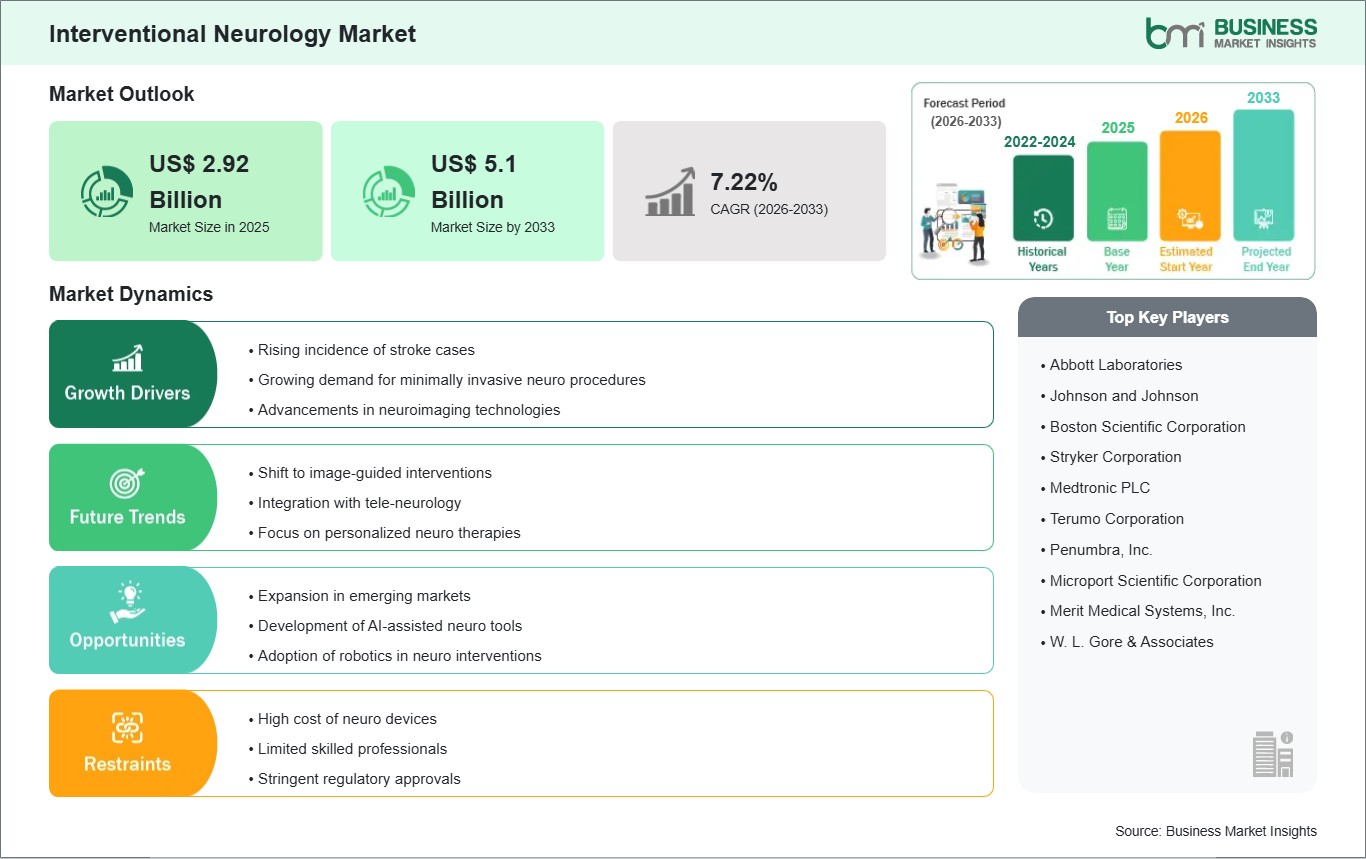

The Interventional Neurology Market size is expected to reach US$ 5.1 Billion by 2033 from US$ 2.92 Billion in 2025. The market is estimated to record a CAGR of 7.22% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Interventional Neurology, also referred to as neuro intervention or endovascular neurosurgery, comprises minimally invasive, catheter-based procedures to diagnose and treat cerebrovascular conditions such as ischemic stroke, intracranial aneurysms, arteriovenous malformations (AVMs), and carotid artery disease. Core device classes include stent retrievers and aspiration systems for thrombectomy, flow-diverters and intrasaccular implants for aneurysm repair, microcatheters and guidewires, and carotid stents. The clinical value proposition is faster recovery, reduced procedural risk compared to open surgery, and expanding indications underpinned by advances in imaging, navigation, and materials science.

Yet, the sector navigates material and regulatory complexity. Recalls and field actions can disrupt adoption and raise scrutiny. Supply-side pressures (e.g., platinum pricing for coils) and reimbursement variability also affect economics and capital planning for hospital neuro-IR suites. Despite these restraints, enduring demand drivers, aging demographics, broader stroke system-of-care readiness, and rapid device iteration continue to open opportunities. Integration of robotics and AI-guided imaging, collaborative ecosystems between imaging and device leaders, and portfolio expansion by neurovascular pure-plays and diversified medtechs underscore a constructive outlook. Strategic partnerships (e.g., Stryker with Siemens Healthineers on neurovascular robotics) and ongoing product innovation (e.g., Penumbra access and embolization platforms; Terumo Neuro's expanded brand and pipeline) are enabling precision, speed, and workflow gains that expand patient access and sustain market growth.

Key segments that contributed to the derivation of the Interventional Neurology market analysis are product type, disease, and end user.

By Product Type, the market is segmented into Embolic Coils, Neurovascular Stents, Flow-Diverter Devices, Thrombectomy Devices, Embolic Protection Devices, Access & Intermediate Catheters, and Guidewires & Micro-catheters.

By Disease, the market is segmented into Ischemic Stroke, Hemorrhagic Stroke, Cerebral Aneurysm, Arteriovenous Malformation & Fistulas, and Others.

By End User, the market is segmented into Hospitals, Specialty Neurology Centers, and Ambulatory Surgical Centers.

Interventional Neurology Market Drivers and Opportunities:

Expansion of Mechanical Thrombectomy in Stroke Pathways

Mechanical thrombectomy has firmly established itself as the gold standard for treating large vessel occlusion (LVO) ischemic strokes, driven by compelling clinical evidence and evolving stroke care protocols. As global stroke systems of care mature, hospitals and neuro-interventional centers are investing heavily in infrastructure and training to ensure rapid access to thrombectomy procedures.

The technology landscape continues to advance with next-generation stent retrievers and aspiration catheters designed for improved trackability, clot engagement, and faster reperfusion. These device innovations, combined with AI-powered imaging platforms and workflow optimization tools, are reducing door-to-reperfusion times and expanding treatment windows beyond traditional limits. Furthermore, integrated stroke networks and tele-neurointervention models are enabling broader patient access, even in resource-constrained geographies. This sustained momentum is reinforced by favorable reimbursement policies and strong clinical outcomes, making thrombectomy a cornerstone of neurovascular intervention and a key driver of capital investment in neuro-interventional radiology suites worldwide.

Emergence of Robotics and Image-Guided Ecosystems in Neurovascular Care

The convergence of robotic navigation systems with advanced image-guided technologies represents a transformative opportunity for neurovascular interventions. Robotics enhances procedural precision, minimizes operator fatigue, and significantly reduces radiation exposure, while image-guided platforms deliver real-time visualization and AI-driven decision support. This synergy is paving the way for remote intervention capabilities and hub-and-spoke care models, which are critical for time-sensitive conditions like acute stroke.

Strategic collaborations between leading medtech companies and imaging giants, such as the partnership between Siemens Healthineers and Stryker, signal a clear industry shift toward integrated ecosystems that combine access devices, implants, imaging modalities, and software into a unified workflow. Early adopters of these technologies stand to gain competitive advantages through improved clinical outcomes, higher throughput, and enhanced staff recruitment and retention. Additionally, these innovations open new service lines for complex aneurysm repairs and emergent stroke interventions, positioning providers at the forefront of next-generation neurovascular care.

Interventional Neurology Market Size and Share Analysis:

The Interventional Neurology market demonstrates steady growth, with size and share analysis revealing evolving trends and competitive positioning among key players. The report further examines subsegments categorized within product type, disease, and end user, offering insights into their contribution to overall market performance.

For instance, among product types, flow-diverter devices have emerged as a critical solution for managing complex cerebral aneurysms, offering durable occlusion and reducing retreatment rates compared to traditional coil embolization. Within disease segment, ischemic stroke dominates procedural volumes due to the growing adoption of mechanical thrombectomy as a standard of care for large vessel occlusions, supported by robust clinical evidence and system-level investments in stroke networks. For end users, hospitals remain the primary setting for neurointerventional procedures, driven by their integrated imaging infrastructure, multidisciplinary teams, and ability to manage high-acuity cases, while specialty neurology centers and ASCs are gradually expanding select interventions under optimized reimbursement frameworks.

Australia, China, India, Japan, South Korea, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Bangladesh, New Zealand, Taiwan

South and Central America

Brazil, Argentina, Peru, Chile, Colombia

Middle East and Africa

Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, United Arab Emirates, Turkiye, South Africa, Egypt, Algeria, Nigeria

Market leaders and key company profiles

Abbott Laboratories

Johnson and Johnson

Boston Scientific Corporation

Stryker Corporation

Medtronic PLC

Terumo Corporation

Penumbra, Inc.

Microport Scientific Corporation

Merit Medical Systems, Inc.

W. L. Gore & Associates

Get more information on this report

Interventional Neurology Market Report Coverage and Deliverables:

The Interventional Neurology Market Size and Forecast (2022–2033) report provides a detailed analysis of the market covering below areas:

Interventional Neurology market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Interventional Neurology market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Interventional Neurology market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the Interventional Neurology market

Detailed company profiles, including SWOT analysis

The geographical scope of the Interventional Neurology market report is divided into five regions: North America, Asia Pacific, Europe, the Middle East & Africa, and South & Central America.

North America focuses on comprehensive stroke centers, robust clinical trial participation, and early integration of imaging-AI into neuro-IR workflows. Europe emphasizes evidence-led adoption and training through pan-European societies, with growing interest in robotics pilots. Asia Pacific accelerates capacity building, China, India, and Southeast Asia expand neuro-IR programs and local manufacturing, supporting cost-effective access. The Middle East & Africa prioritize capability development within tertiary hubs to reduce outbound care. South & Central America modernize neurovascular pathways and imaging infrastructure, with select centers scaling thrombectomy volumes and aneurysm programs.

Get more information on this report

Interventional Neurology Market Research Report Guidance:

The report includes qualitative and quantitative data in the Interventional Neurology market across product type, disease, end user, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Interventional Neurology market.

Chapter 3 includes the research methodology of the study.

Chapter 4 further includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Interventional Neurology market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Interventional Neurology market scenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Interventional Neurology market segments by product type, disease, end user, and geography across North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. They cover the market volume, revenue forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Interventional Neurology market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, a list of abbreviations, and a disclaimer.

Interventional Neurology Market News and Key Development:

The Interventional Neurology market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Interventional Neurology market are:

In February 2025, Brainomix, a pioneer in stroke AI imaging software and European market leader, announced a strategic partnership with Medtronic Neurovascular, a global leader in medical technology. The collaboration aims to enhance stroke care for patients across Western Europe by integrating cutting-edge artificial intelligence (AI) solutions into clinical practice, expanding access to life-changing treatments, and improving patient outcomes.

In September 2025, Siemens Healthineers and Stryker announced a strategic partnership in the field of neurovascular robotics. The collaboration aims to develop a unique robotic system capable of performing a comprehensive range of elective and emergency neurovascular procedures, including treatment for strokes and aneurysms.

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)International Monetary Fund (IMF)International Trade Administration (ITA)Company WebsitesCompany Annual ReportsCompany Investor Presentations

The List of Companies - Interventional Neurology Market

Abbott Laboratories

Johnson and Johnson

Boston Scientific Corporation

Stryker Corporation

Medtronic PLC

Terumo Corporation

Penumbra, Inc.

Microport Scientific Corporation

Merit Medical Systems, Inc.

W. L. Gore & Associates

Frequently Asked Questions

How big is the Interventional Neurology Market?

The Interventional Neurology Market is valued at US$ 2.92 Billion in 2025, it is projected to reach US$ 5.1 Billion by 2033.

What is the CAGR for Interventional Neurology Market by (2026 - 2033)?

As per our report Interventional Neurology Market, the market size is valued at US$ 2.92 Billion in 2025, projecting it to reach US$ 5.1 Billion by 2033. This translates to a CAGR of approximately 7.22% during the forecast period.

What segments are covered in this report?

The Interventional Neurology Market report typically cover these key segments-

End User (Hospitals, Specialty Neurology Centers, Ambulatory Surgical Centers)

What is the historic period, base year, and forecast period taken for Interventional Neurology Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Interventional Neurology Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Interventional Neurology Market?

The Interventional Neurology Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Abbott Laboratories

Johnson and Johnson

Boston Scientific Corporation

Stryker Corporation

Medtronic PLC

Terumo Corporation

Penumbra, Inc.

Microport Scientific Corporation

Merit Medical Systems, Inc.

W. L. Gore & Associates

Who should buy this report?

The Interventional Neurology Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Interventional Neurology Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Interventional Neurology Market

Get Free Sample For Interventional Neurology Market