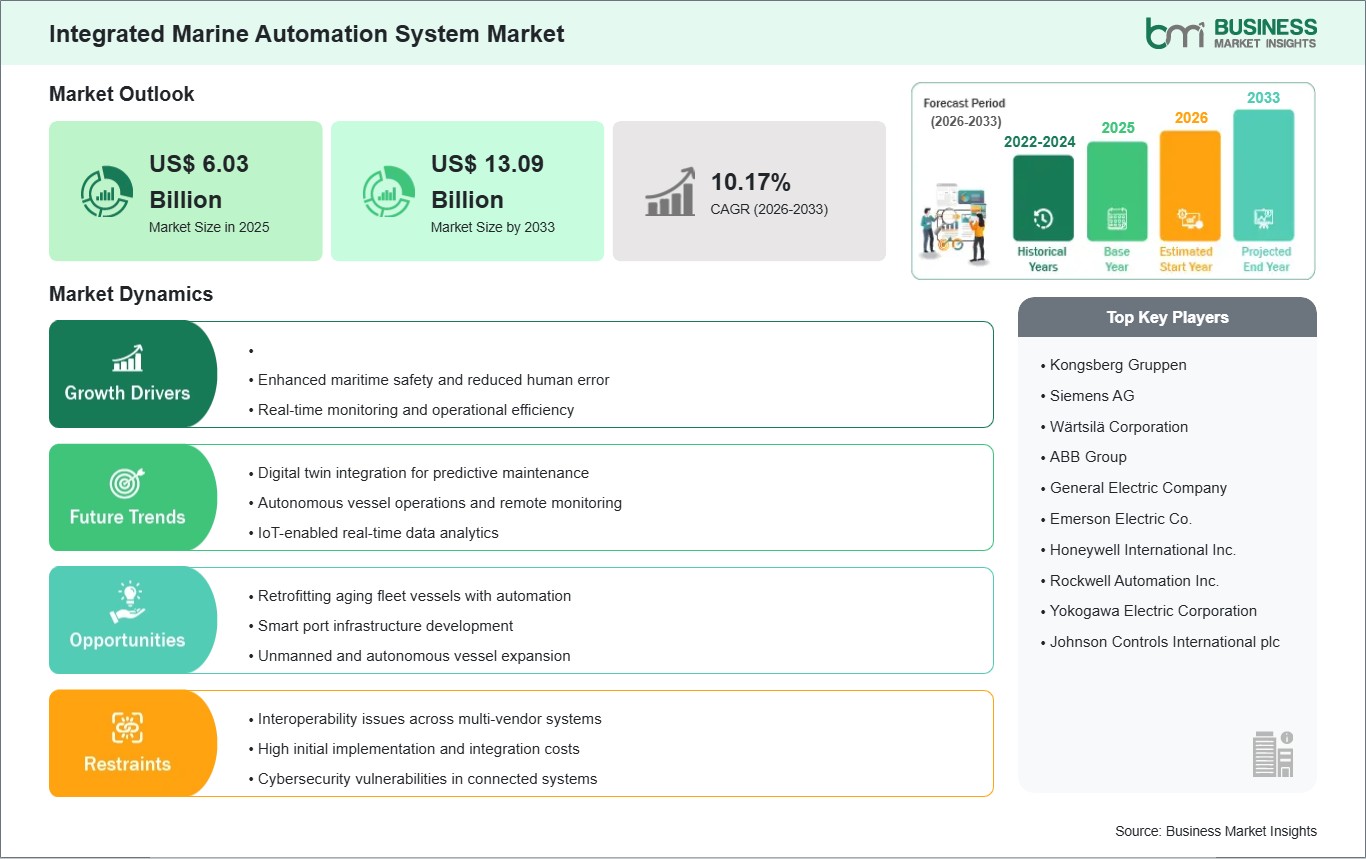

The Integrated Marine Automation System market size is expected to reach US$ 13.09 Billion by 2033 from US$ 6.03 Billion in 2025. The market is estimated to record a CAGR of 10.17% from 2026 to 2033.

Executive Summary and Global Market Analysis:

Integrated marine automation systems combine onboard monitoring, control, alarm handling, and decision support within a unified vessel architecture. These platforms connect propulsion, electrical distribution, machinery supervision, safety controls, and operator interfaces to sustain reliable ship operations. Their functional value lies in reducing manual intervention while maintaining continuity across mission-critical marine processes.

Fleet operators are prioritizing integrated control environments as vessels become more software-defined and operational transparency gains importance. Automation consolidation supports tighter equipment coordination, improves fault visibility, and simplifies response workflows for engine room and bridge personnel. Retrofit programs also reinforce demand as owners modernize aging assets to improve reliability, energy oversight, and compliance readiness.

Segment positioning reflects distinct operational priorities across system design and vessel deployment. Power management remains central where electrical stability, load balancing, and fuel efficiency shape automation investments. Commercial vessels represent a broad implementation base, while defense platforms emphasize resilience, redundancy, and mission assurance. OEM demand stays prominent because automation architecture is increasingly specified early in ship design.

Technology development is shifting the industry toward interoperable platforms with stronger analytics, remote diagnostics, and distributed control intelligence. System suppliers are improving data fusion across subsystems so crews can manage vessel health through fewer interfaces and clearer exception alerts. This evolution supports more adaptive maintenance planning and sharper operational awareness during complex voyages.

Competitive conditions are shaped by platform breadth, service capability, integration expertise, and lifecycle support rather than isolated hardware supply. Buyers assess vendors on system reliability, commissioning experience, cybersecurity preparedness, and long-term upgrade pathways. As procurement shifts toward connected ship ecosystems, solution depth and installed-base familiarity remain decisive differentiators.

Integrated Marine Automation System Market - Strategic Insights:

Get more information on this report

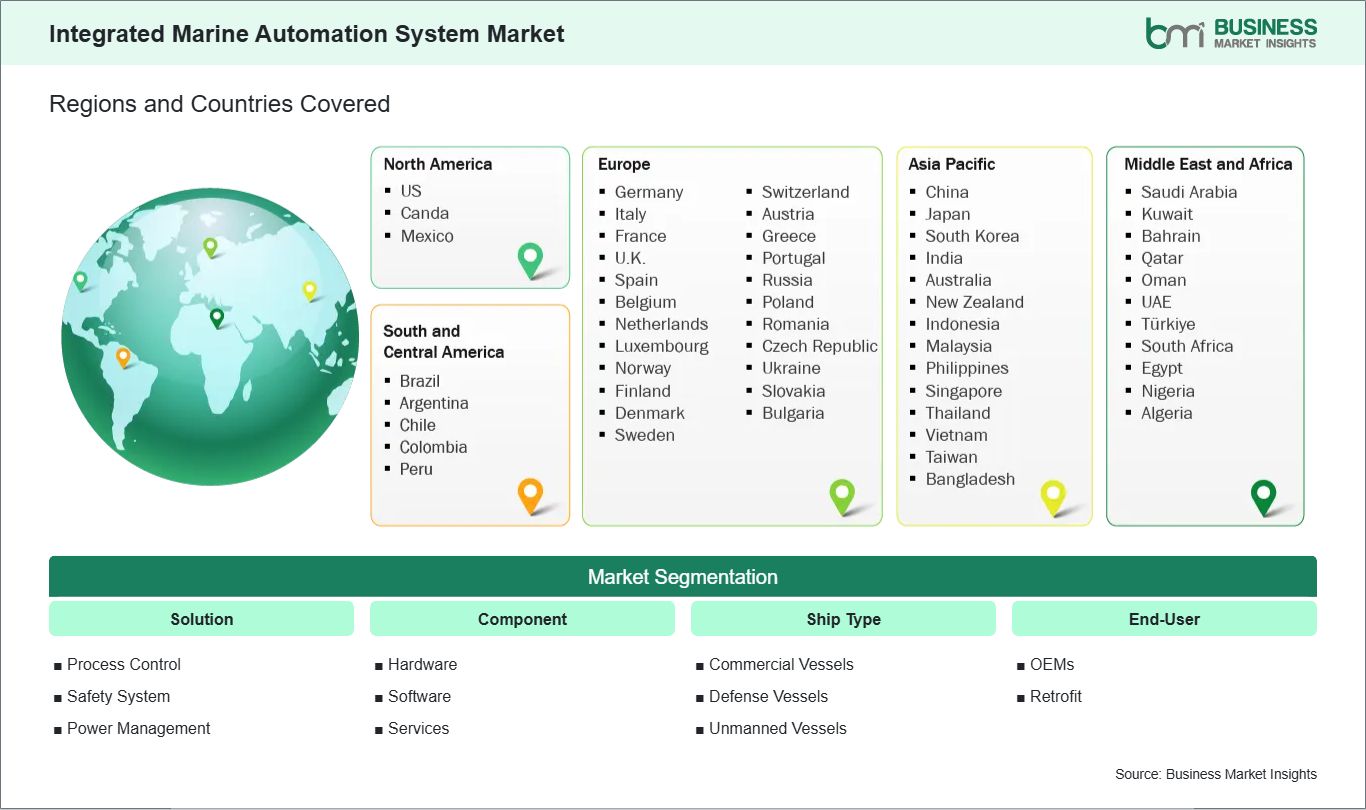

Integrated Marine Automation System Market Segmentation Analysis:

The market is segmented by solution, component, ship type, and end-user to reflect deployment priorities across vessel programs.

By Solution

Process Control: Coordinates machinery functions through centralized monitoring and command logic.

Safety System: Maintains alarm visibility and protective response during abnormal vessel conditions.

Power Management: Optimizes electrical distribution, load sharing, and onboard energy stability.

By Component

Hardware: Provides controllers, sensors, interfaces, and communication infrastructure for vessel automation.

Software: Enables supervisory control, analytics, visualization, and system coordination functions.

Services: Covers integration, commissioning, maintenance, and lifecycle support activities.

By Ship Type

Commercial Vessels: Account for wide-scale deployment across cargo, passenger, and offshore operations.

Defense Vessels: Require resilient automation for mission continuity and system redundancy.

Unmanned Vessels: Depend on integrated control layers for remote supervision and autonomous functions.

OEMs: Specify automation architecture during shipbuilding and original platform integration.

By End-User

OEMs: Shape early-stage design choices and platform-level automation configuration.

Retrofit: Extends automation functionality across existing fleets through modernization projects.

Integrated Marine Automation System Market Drivers and Opportunities:

Rising Digital Control Requirements Across Modern Vessel Operations

Marine operators are handling more interconnected onboard systems, which raises the need for unified control environments. Separate monitoring layers create fragmented visibility, slower fault diagnosis, and higher crew workload during demanding operating conditions. Integrated automation addresses this gap by centralizing alarms, control actions, and equipment feedback into a coordinated operating framework suited to complex vessel routines.

The effect is stronger operational consistency across propulsion, power, machinery, and safety domains. This matters in commercial and defense programs where downtime, manual dependency, and delayed response can disrupt voyage performance. As shipowners place greater emphasis on controllability and lifecycle efficiency, integrated marine automation systems become more relevant to both newbuild and upgrade decisions.

Expansion of Smart Vessel Modernization and Remote Operations

A broader shift toward intelligent shipping is opening room for advanced automation upgrades across fleet categories. Vendors are introducing platforms with stronger analytics, remote diagnostics, and modular integration, allowing owners to extend functionality without redesigning entire control environments. These capabilities are particularly useful where operators seek cleaner workflows, better situational visibility, and smoother coordination across onboard subsystems.

Future scope is notable in retrofit programs, unmanned vessel development, and digitally managed commercial fleets. Expansion in these areas can strengthen recurring service demand while widening software-led differentiation across suppliers. The market stands to benefit as ship operators pursue flexible automation layers that support scalable upgrades, operational continuity, and sharper control over distributed marine assets.

Integrated Marine Automation System Market Size and Share Analysis:

The Integrated Marine Automation System market size is expected to reach US$ 13.09 Billion by 2033 from US$ 6.03 Billion in 2025. The market is estimated to record a CAGR of 10.17% from 2026 to 2033. This trajectory indicates sustained expansion as vessel operators prioritize integrated control visibility, equipment coordination, and lifecycle modernization across increasingly digital marine environments.

By solution, power management holds a leading position because energy stability, load control, and electrical efficiency remain central to ship performance. Within components, hardware forms the operational backbone through controllers, interfaces, and communication modules, while software deepens system intelligence and service layers strengthen long-term platform continuity.

Commercial vessels represent the principal application base as operators seek broad automation coverage across cargo movement, propulsion management, and onboard safety supervision. OEM engagement remains prominent because automation design is increasingly embedded during vessel construction, while retrofit activity continues to expand through fleet renewal initiatives.

Integrated Marine Automation System Market Report Highlights:

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Kongsberg Gruppen

Siemens AG

Wartsila Corporation

ABB Group

General Electric Company

Emerson Electric Co.

Honeywell International Inc.

Rockwell Automation Inc.

Yokogawa Electric Corporation

Johnson Controls International plc

Get more information on this report

Integrated Marine Automation System Market Report Coverage and Deliverables:

The "Integrated Marine Automation System Market Size and Forecast (2022-2033)" report provides a detailed analysis of the market covering the areas below:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Integrated Marine Automation System Market Geographic Insights:

The Integrated Marine Automation System market shows diverse regional adoption patterns influenced by shipbuilding priorities, fleet modernization cycles, digital control maturity, and operational safety expectations. Across the broader market, automation demand reflects how shipowners balance efficiency, reliability, and centralized oversight in increasingly connected marine environments.

North America maintains a steady role through defense modernization, offshore support requirements, and demand for resilient vessel control platforms. Buyers in this region often emphasize integration quality, redundancy, and supportability, which favors established automation architectures suited to complex operating conditions and extended service obligations.

Asia Pacific remains a strong center for implementation because commercial shipbuilding scale, port-linked trade activity, and industrial supply depth support automation deployment. Regional demand is reinforced by shipyard integration programs and the need for efficient control systems across newbuild commercial fleets, specialized vessels, and emerging autonomous platforms.

Europe retains strategic influence through advanced maritime engineering, decarbonization-focused modernization, and early movement toward intelligent ship operations, while emerging markets in the Middle East, Africa, and South and Central America present selective expansion potential tied to fleet renewal and infrastructure-linked marine investment. Together, these regions broaden the industry’s installation base and service opportunities.

Get more information on this report

Integrated Marine Automation System Market Research Report Guidance:

The report encompasses both qualitative and quantitative data pertaining to the market, categorized by solution, component, ship type, and end-user, and geographical regions.

Beginning with Chapter 2, the report presents key takeaways that underscore the primary trends and market outlook.

Chapter 3 is dedicated to outlining the research methodology employed in this study.

In Chapter 4, an ecosystem analysis is provided.

Chapter 5 delves into the significant industry dynamics affecting the market, including driving factors, existing challenges, potential opportunities, and emerging trends. This section also includes an impact analysis of these drivers and constraints.

Chapter 6 reviews the market scenario, detailing historical revenue figures and forecasts extending to the year 2033.

Chapters 7 through 10 analyze market segments based on solution, component, ship type, and end-user, and geography, covering regions such as North America, Europe, Asia Pacific, the Middle East and Africa, and South and Central America. These chapters include market revenue data, forecasts, and driving factors.

Chapter 11 presents a competitive analysis, featuring a heat map of key players within the market.

Chapter 12 offers an industry landscape analysis, detailing business activities such as market initiatives, recent developments, mergers, and joint ventures on a global scale, alongside a competitive overview.

In Chapter 13, comprehensive profiles of major companies operating in the market are provided. These profiles include key facts, business descriptions, product and service offerings, financial overviews, SWOT analyses, and significant developments.

Finally, Chapter 14, the appendix, includes a brief company overview, a list of abbreviations, and a disclaimer.

Integrated Marine Automation System Market News and Key Development:

The market assessment incorporates recent industry actions that reflect product development and regulatory movement. Below are two notable updates arranged from latest to earlier developments.

In May 2026, ABB has secured a contract with Sri Lankan shipbuilder Colombo Dockyard PLC to supply a fully integrated electrical power, propulsion and automation system for two newbuild cable repair vessels for shipowner Orange Marine, a wholly owned subsidiary of the Orange Group specializing in submarine cable work. Scheduled for delivery in 2028 and 2029, the hybrid-electric ships will be responsible for maintaining cables in the Atlantic and Indian oceans as well as the Mediterranean, Black and Red seas. This order follows the previous successful collaboration with both Orange Marine and Colombo Dockyard PLC.

In June 2025, Valmet, a major supplier of ship automation, introduces the Valmet DNAe Integrated Automation System for the marine industry. Valmet DNAe is a fully web-based marine control system that integrates seamlessly with all onboard equipment, providing ship owners with a unified platform for efficient operations. It is the first web-based automation system to receive the ISASecure SSA Level 1 certification for its built-in cybersecurity approach.

Key Sources Referred:

International Maritime Organization publications and regulatory updatesGovernment maritime transport and trade data repositoriesPeer-reviewed maritime engineering journalsCompany annual reports and investor presentationsShipbuilding and marine technology industry reportsAcademic studies on vessel automation and control systemsCorporate product releases and technical disclosures

The List of Companies - Integrated Marine Automation System Market

Kongsberg Gruppen

Siemens AG

Wärtsilä Corporation

ABB Group

General Electric Company

Emerson Electric Co.

Honeywell International Inc.

Rockwell Automation Inc.

Yokogawa Electric Corporation

Johnson Controls International plc

Frequently Asked Questions

How big is the Integrated Marine Automation System Market?

The Integrated Marine Automation System Market is valued at US$ 6.03 Billion in 2025, it is projected to reach US$ 13.09 Billion by 2033.

What is the CAGR for Integrated Marine Automation System Market by (2026 - 2033)?

As per our report Integrated Marine Automation System Market, the market size is valued at US$ 6.03 Billion in 2025, projecting it to reach US$ 13.09 Billion by 2033. This translates to a CAGR of approximately 10.17% during the forecast period.

What segments are covered in this report?

The Integrated Marine Automation System Market report typically cover these key segments-

Solution (Process Control, Safety System, Power Management)

Component (Hardware, Software, Services)

Ship Type (Commercial Vessels, Defense Vessels, Unmanned Vessels)

End-User (OEMs, Retrofit)

What is the historic period, base year, and forecast period taken for Integrated Marine Automation System Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Integrated Marine Automation System Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Integrated Marine Automation System Market?

The Integrated Marine Automation System Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Kongsberg Gruppen

Siemens AG

Wartsila Corporation

ABB Group

General Electric Company

Emerson Electric Co.

Honeywell International Inc.

Rockwell Automation Inc.

Yokogawa Electric Corporation

Johnson Controls International plc

Who should buy this report?

The Integrated Marine Automation System Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Integrated Marine Automation System Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Integrated Marine Automation System Market

Get Free Sample For Integrated Marine Automation System Market