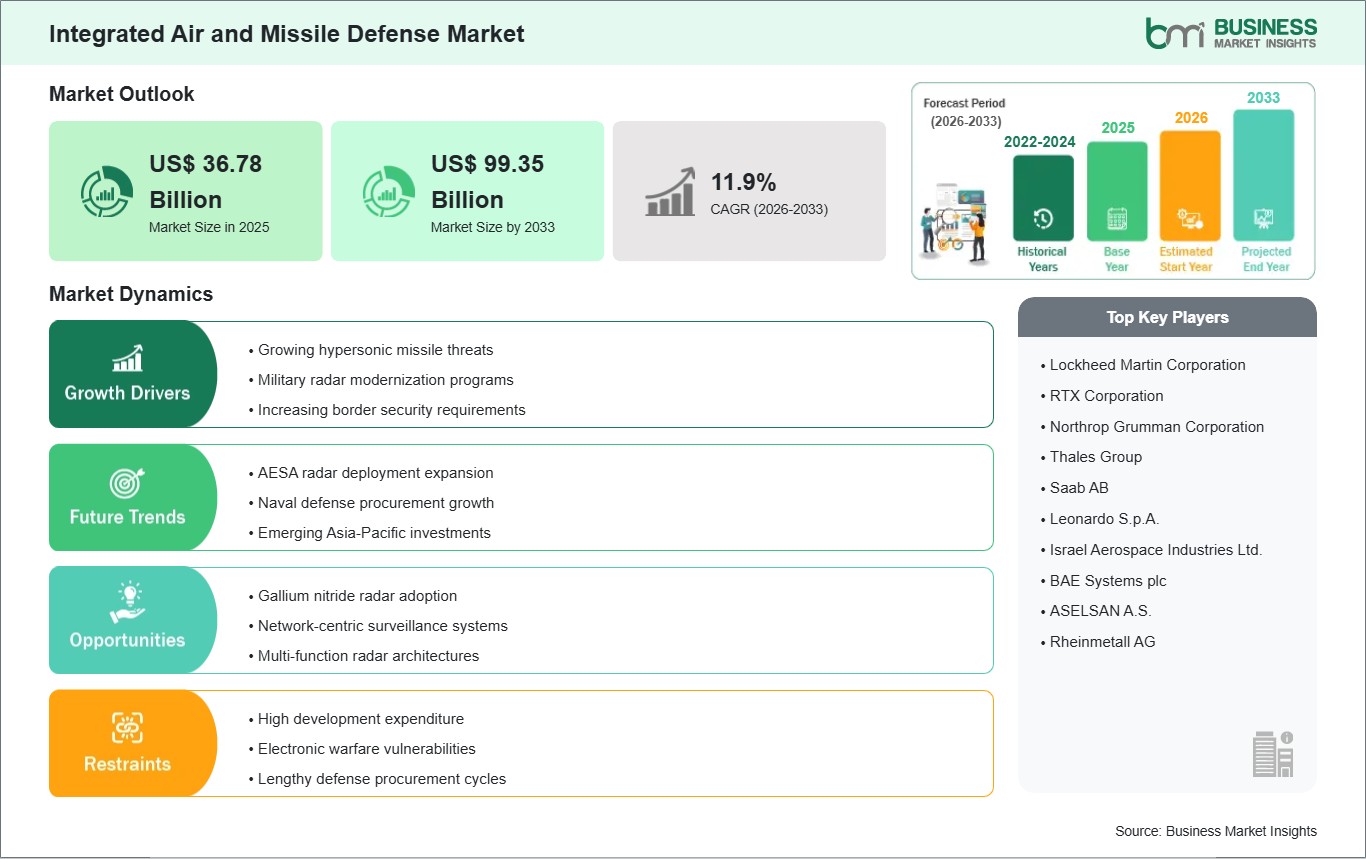

The Integrated Air and Missile Defense market size is projected to grow from US$ 36.78 Billion in 2025 to US$ 99.35 Billion by 2033, registering a CAGR of 11.9% during 2026 - 2033.

Executive Summary and Global Market Analysis:

Integrated air and missile defense refers to a layered military architecture that detects, tracks, classifies, and neutralizes airborne threats through coordinated sensors, command networks, launch systems, and interceptors. Its purpose extends beyond single-platform protection by linking engagement assets across land, sea, and air environments. This architecture is designed to respond to ballistic missiles, cruise missiles, aircraft, rockets, drones, and increasingly complex maneuvering threats.

Procurement momentum reflects the operational need for persistent surveillance, faster engagement cycles, and better coordination between distributed defense assets. Defense forces are refining networked architectures to address simultaneous attacks involving drones, cruise missiles, and tactical missiles. This requirement is encouraging investment in resilient command structures, radar modernization, and mobile defense configurations suited to contested operating environments.

System demand spans missile defense, anti-aircraft protection, counter-unmanned aircraft systems, counter-rocket artillery and mortar capabilities, and emerging counter-hypersonic layers. On the supply side, radars and sensors, fire control systems, launchers, weapon systems, command and control, and integration services form the technical backbone of deployment. Range-based requirements also vary across short, medium, and long-range interception missions, shaping procurement priorities for army, navy, and air force operators.

Technology evolution within this sector centers on sensor fusion, open-architecture command networks, data-driven engagement planning, and interoperability across allied platforms. Programs are increasingly structured to connect legacy assets with new interceptors and battle management software rather than replace entire force structures at once. That transition supports more flexible responses against saturation attacks and improves layered engagement efficiency across multiple threat classes.

Competitive conditions remain shaped by long program cycles, sovereign procurement priorities, integration complexity, and the need for validated operational performance. Vendors compete through system interoperability, upgrade pathways, production scalability, and alignment with national modernization agendas. As multi-threat defense becomes a central planning requirement, the industry is moving toward broader mission integration rather than isolated capability procurement.

Integrated Air and Missile Defense Market - Strategic Insights:

Get more information on this report

Integrated Air and Missile Defense Market Segmentation Analysis:

The market is segmented by system, component, range, and end user, reflecting layered defense planning across operational domains.

By System

Missile Defense: Prioritized for layered interception against ballistic and cruise threat envelopes.

Anti-aircraft: Maintains airspace protection against fixed-wing and rotary-wing intrusions.

C-UAS: Expands to counter small, low-signature, and swarming unmanned systems.

C-RAM: Supports force protection around bases and forward operating locations.

Counter-Hypersonics:Gains attention as defense planners address compressed engagement timelines.

Weapon Systems: Central to engagement credibility across diverse aerial threat profiles.

Fire Control Systems: Improve targeting precision and engagement sequencing efficiency.

Radars & Sensors: Provide early warning, tracking continuity, and threat discrimination.

Launchers: Enable mobile deployment and responsive interceptor positioning.

C2: Connects detection, decision, and engagement across distributed assets.

System Integration: Ensures interoperability between legacy systems and new architectures.

By Range

SHORAD: Essential for point defense against low-altitude and short-notice threats.

MRAD: Balances area coverage with deployment flexibility for layered missions.

LRAD: Supports strategic defense against high-value and extended-range threats.

Integrated Air and Missile Defense Market Drivers and Opportunities:

Escalating Multi-Threat Airspace Complexity

Air defense planning has become more demanding as forces confront overlapping threats from drones, cruise missiles, rockets, and maneuvering projectiles. Traditional point systems cannot consistently manage this threat mix without networked sensors and coordinated fire control. That operational gap is increasing procurement focus on integrated architectures that connect detection, decision, and interception into a unified response framework.

The impact extends beyond homeland defense into expeditionary protection, maritime security, and critical infrastructure shielding. Defense organizations require systems that can sustain engagement capacity under saturation conditions while preserving command visibility. This makes integrated air and missile defense relevant not only for strategic deterrence, but also for operational continuity across dispersed and contested theaters.

Open-Architecture Integration Across Legacy and Emerging Systems

A significant opportunity is emerging around open-architecture integration that links older defense assets with new sensors, battle management software, and interceptors. Governments are looking for flexible modernization paths that avoid complete system replacement. This trend favors integration platforms capable of combining different effectors and detection layers into a common operating picture for faster mission execution.

Future scope is broad because integrated frameworks can expand across land formations, naval fleets, and joint command environments with lower structural disruption. As procurement shifts toward software-defined coordination and interoperable nodes, suppliers that support modular upgrades may gain wider program access. This expansion can improve readiness, strengthen coalition compatibility, and extend mission coverage across evolving threat scenarios.

Integrated Air and Missile Defense Market Size and Share Analysis:

The Integrated Air and Missile Defense market size is projected to grow from US$ 36.78 Billion in 2025 to US$ 99.35 Billion by 2033, registering a CAGR of 11.9% during 2026 - 2033. This trajectory reflects sustained investment in layered defense architectures as armed forces seek broader threat coverage, improved engagement coordination, and stronger protection for strategic assets and deployed formations.

Among system categories, missile defense and integrated multi-threat configurations hold strategic prominence because procurement increasingly favors architectures that combine surveillance, command, and interception across several engagement layers. Within components, radars and sensors, fire control systems, and command networks remain central because performance depends on detection accuracy and coordinated battle management.

From an end-user perspective, army-led deployments account for a substantial share of operational demand due to land-based force protection and mobile air defense requirements. Application intensity also remains high in base defense, border surveillance, and maritime protection, where integrated engagement planning supports continuous readiness against dynamic aerial and missile threats.

Integrated Air and Missile Defense Market Report Highlights:

China, Japan, South Korea, India, Australia, New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Taiwan, Bangladesh

South and Central America

Brazil, Argentina, Chile, Colombia, Peru

Middle East and Africa

Saudi Arabia, United Arab Emirates, Kuwait, Bahrain, Qatar, Oman, Turkiye, South Africa, Egypt, Nigeria, Algeria

Market leaders and key company profiles

Lockheed Martin Corporation

RTX Corporation

Northrop Grumman Corporation

Thales Group

Saab AB

Leonardo S.p.A.

Israel Aerospace Industries Ltd.

BAE Systems plc

ASELSAN A.S.

Rheinmetall AG

Get more information on this report

Integrated Air and Missile Defense Market Report Coverage and Deliverables:

The "Integrated Air and Missile Defense Market Size and Forecast (2022–2033)" report provides a detailed analysis of the market covering below areas:

Market size and forecast at global, regional, and country levels for all the key market segments covered under the scope

Market trends, as well as market dynamics such as drivers, restraints, and key opportunities

Market analysis covering key market trends, global and regional framework, major players, regulations, and recent market developments

Industry landscape and competition analysis covering market concentration, heat map analysis, prominent players, and recent developments for the market

Detailed company profiles, including SWOT analysis

Integrated Air and Missile Defense Market Geographic Insights:

The Integrated Air and Missile Defense market shows diverse regional adoption patterns influenced by threat perceptions, defense modernization priorities, alliance commitments, and the maturity of command-and-control infrastructure. Global procurement programs increasingly emphasize layered architectures that can coordinate sensors, launchers, and battle management across service branches. This direction is strengthening demand for interoperable systems able to respond to drones, missiles, rockets, and aircraft within a single operational framework.

North America remains a principal center for capability development, field integration, and doctrinal advancement in this sector. Procurement focus is shaped by homeland defense, expeditionary protection, and the need to connect established missile defense assets with newer battle management networks. The regional landscape also benefits from a strong industrial base and established testing infrastructure, supporting sustained upgrades across land and maritime defense programs.

Asia Pacific is gaining strategic weight as governments strengthen defenses against expanding missile inventories, low-altitude incursions, and unmanned threats. Regional programs increasingly prioritize short-range and medium-range layers, networking capabilities, and faster decision support across distributed operating areas. Procurement strategies often combine domestic development with international collaboration, creating a dynamic environment for radar, command, and interceptor integration.

Europe continues to advance integrated defense through interoperability requirements, multi-country security coordination, and renewed emphasis on protecting critical infrastructure and forward positions. Emerging markets in the Middle East, Africa, and South and Central America are also examining layered defense models, although adoption paths differ according to budget structure, threat urgency, and local industrial capacity. These regions are creating selective opportunities for modular, scalable, and mission-specific deployments.

Get more information on this report

Integrated Air and Missile Defense Market Research Report Guidance:

The report includes qualitative and quantitative data in the Integrated Air and Missile Defense market across system, component, range, and geography.

The report starts with the key takeaways (chapter 2), highlighting the key trends and outlook of the Integrated Air and Missile Defense market.

Chapter 3 focuses on the research methodology of the study.

Chapter 4 includes ecosystem analysis.

Chapter 5 highlights the major industry dynamics in the Integrated Air and Missile Defense market, including factors that are driving the market, prevailing deterrents, potential opportunities, as well as future trends. Impact analysis of these drivers and restraints is also covered in this section.

Chapter 6 discusses the Integrated Air and Missile Defense marketscenario, in terms of historical market revenues, and forecast till the year 2033.

Chapters 7 to 10 cover Integrated Air and Missile Defense marketsegments by system, component, range, and geography across North America, Europe, Asia Pacific, Middle East and Africa, and South and Central America. They cover the market revenue, forecast, and factors driving the market.

Chapter 11 describes the competitive analysis along with the heat map analysis for the key players operating in the market.

Chapter 12 describes the industry landscape analysis. It provides detailed descriptions of business activities such as market initiatives, new developments, mergers, and joint ventures globally, along with a competitive landscape.

Chapter 13 provides detailed profiles of the major companies operating in the Integrated Air and Missile Defense market. Companies have been profiled on the basis of their key facts, business descriptions, products and services, financial overview, SWOT analysis, and key developments.

Chapter 14, i.e., the appendix, is inclusive of a brief overview of the company, list of abbreviations, and disclaimer.

Integrated Air and Missile Defense Market News and Key Development:

The Integrated Air and Missile Defense market is evaluated by gathering qualitative and quantitative data post primary and secondary research, which includes important corporate publications, association data, and databases. A few of the key developments in the Integrated Air and Missile Defense marketare.

In March 2026, Thales Group has launched SkyDefender, an integrated air and missile defence dome that combines radar, command-and-control systems, AI, cybersecurity, and space-based sensors to protect against a wide range of threats, including drones, cruise missiles, ballistic missiles, and hypersonic weapons. The system uses a multi-layered defence architecture with short-, medium-, and long-range capabilities, supported by AI-driven threat analysis and an open architecture that can integrate with existing national and allied defence networks. SkyDefender is designed to provide comprehensive airspace protection and faster decision-making in response to increasingly sophisticated modern missile and aerial threats.

In June 2026: RTX Corporation announced a $100 million investment in its Portsmouth, Rhode Island facility to expand radar testing and missile-interceptor production capacity. The project is expected to create about 150 high-tech jobs and support growing demand for advanced air and missile defense systems. The expansion will increase testing for the U.S. Army’s Lower Tier Air and Missile Defense Sensor (LTAMDS) radar and boost production of key components for Patriot GEM-T interceptors, helping accelerate deliveries to U.S. and allied customers. The move is part of RTX’s broader effort to strengthen defense manufacturing and meet rising global security requirements.

Key Sources Referred:

World Bank – Global Trade IndicatorsWorld Trade Organization (WTO)(International Monetary Fund )IMFInternational Trade Administration (ITA)Company websiteCompany annual reportsCompany investor presentations

The List of Companies - Integrated Air and Missile Defense Market

Lockheed Martin Corporation

RTX Corporation

Northrop Grumman Corporation

Thales Group

Saab AB

Leonardo S.p.A.

Israel Aerospace Industries Ltd.

BAE Systems plc

ASELSAN A.S.

Rheinmetall AG

Frequently Asked Questions

How big is the Integrated Air and Missile Defense Market?

The Integrated Air and Missile Defense Market is valued at US$ 36.78 Billion in 2025, it is projected to reach US$ 99.35 Billion by 2033.

What is the CAGR for Integrated Air and Missile Defense Market by (2026 - 2033)?

As per our report Integrated Air and Missile Defense Market, the market size is valued at US$ 36.78 Billion in 2025, projecting it to reach US$ 99.35 Billion by 2033. This translates to a CAGR of approximately 11.9% during the forecast period.

What segments are covered in this report?

The Integrated Air and Missile Defense Market report typically cover these key segments-

System (Missile Defense, Anti-aircraft, C-UAS, C-RAM, Counter-Hypersonics, Integrated Multi-Threat)

Component (Weapon Systems, Fire Control Systems, Radars & Sensors, Launchers, C2, System Integration)

Range (SHORAD, MRAD, LRAD)

What is the historic period, base year, and forecast period taken for Integrated Air and Missile Defense Market?

The historic period, base year, and forecast period can vary slightly depending on the specific market research report. However, for the Integrated Air and Missile Defense Market report:

Historic Period : 2022-2024

Base Year : 2025

Forecast Period : 2026-2033

Who are the major players in Integrated Air and Missile Defense Market?

The Integrated Air and Missile Defense Market is populated by several key players, each contributing to its growth and innovation. Some of the major players include:

Lockheed Martin Corporation

RTX Corporation

Northrop Grumman Corporation

Thales Group

Saab AB

Leonardo S.p.A.

Israel Aerospace Industries Ltd.

BAE Systems plc

ASELSAN A.S.

Rheinmetall AG

Who should buy this report?

The Integrated Air and Missile Defense Market report is valuable for diverse stakeholders, including:

Investors: Provides insights for investment decisions pertaining to market growth, companies, or industry insights. Helps assess market attractiveness and potential returns.

Industry Players: Offers competitive intelligence, market sizing, and trend analysis to inform strategic planning, product development, and sales strategies.

Suppliers and Manufacturers: Helps understand market demand for components, materials, and services related to concerned industry.

Researchers and Consultants: Provides data and analysis for academic research, consulting projects, and market studies.

Financial Institutions: Helps assess risks and opportunities associated with financing or investing in the concerned market.

Essentially, anyone involved in or considering involvement in the Integrated Air and Missile Defense Market value chain can benefit from the information contained in a comprehensive market report.

Get Free Sample For Integrated Air and Missile Defense Market

Get Free Sample For Integrated Air and Missile Defense Market